|

시장보고서

상품코드

2063536

치과용 접착제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Dental Putty - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

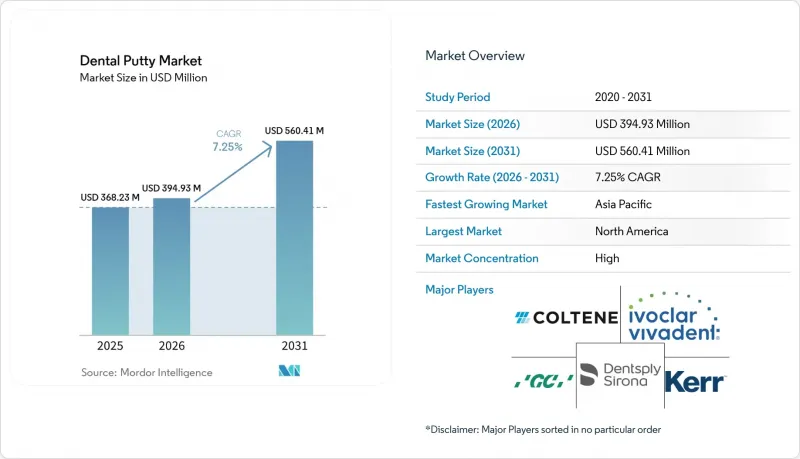

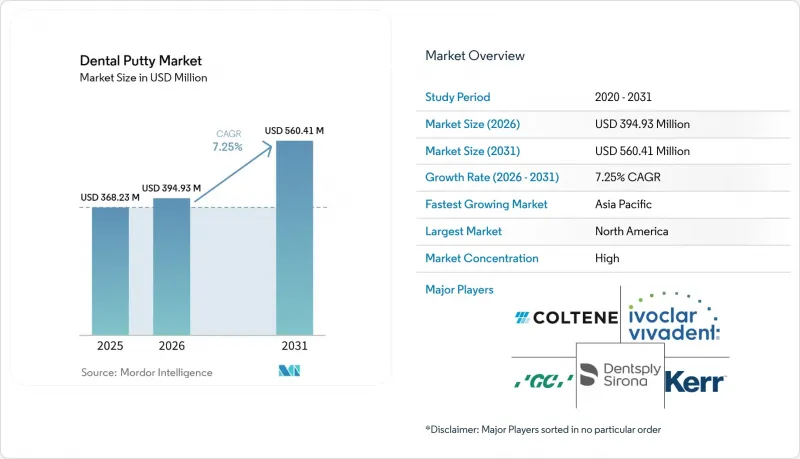

Mordor Intelligence에 의하면, 치과용 접착제 시장 규모는 2025년 3억 6,823만 달러, 2026년 3억 9,493만 달러에서 2031년까지 5억 6,041만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.25%를 나타낼 것으로 예측됩니다.

본 보고서는 유형(일반 경화형, 속경화형), 제품 유형(VPS(A-실리콘) 퍼티, 폴리에테르 퍼티, 축합형 실리콘(C-실리콘) 퍼티), 용도(보철 치과, 임플란트 치과 등), 공급 형태(수동 혼합용 용기, 오토믹스 카트리지 등), 최종 사용자(치과 병원, 병원 등), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계 치과용 접착제 시장 동향 및 분석

구강 질환 및 무치악의 유병률 증가

치과용 접착제 시장은 전 세계 구강 질환의 부담과 연동된 지속적인 임상 수요의 혜택을 받고 있습니다. 『Journal of Periodontal Research』에 따르면, 치주염은 여전히 전 세계에서 유병률이 가장 높은 질환 중 하나이며, 최신 세계 데이터는 “심각한 경고”라고 지적되고 있습니다. 이 저널은 중증 치주염이 전 세계 인구의 약 11%에 영향을 미치고 있음을 강조하고 있으며, 이는 ‘세계 질병 부담(GBD)’의 추산치와 일치합니다. 이로 인해 무치악은 장애를 유발하는 질환 중에서도 상위권에 위치하게 되었으며, 복잡한 수복 치료에 필요한 정밀한 인상 채취에 대한 간접적인 수요가 유지되고 있습니다. 중국에서는 2050년까지 1억 3,023만 명의 무치악 환자가 발생할 것으로 예측되며, 이는 전 세계 전체의 19.67%에 해당합니다. 이로 인해 방대한 치료 건수에서 정확한 인상 채취를 수행해야 할 필요성이 더욱 커지고 있습니다. 미국에서 2017년부터 2020년 초까지의 감시 데이터에 따르면, 20세에서 64세 성인 중 21%, 노인 중 13%에게 치료되지 않은 충치가 확인되었으며, 빈곤층이나 현재 흡연 중인 사람들의 경우 그 비율이 훨씬 더 높습니다. 이는 꾸준한 간접적 환자 유입과 정기적인 전악 수복 수요를 뒷받침하는 요인이 되고 있습니다. 또한 각 제조업체는 무치악화의 추세를 근거로, 의치 및 오버덴처의 워크플로우에 대한 투자를 정당화하고 있습니다. 예를 들어, Dentsply Sirona와 Formlabs의 제휴를 통해 재료, 프린터, 검증 프로세스를 연계하여, 임상적으로 적절한 경우에는 기존의 아날로그 방식을 유지하면서 디지털 의치 생산을 확대되고 있습니다. 세계 질병 부담 조사 프로그램의 분석에 따르면, 구강 질환을 앓는 총 인구의 감소폭은 극히 미미한 것으로 나타났으며, 이는 보철 치과 및 임플란트 분야의 치과용 접착제 시장 수요를 지속적으로 뒷받침하고 있습니다.

수복·보철 치료에 대한 수요 증가

치과용 패스트 시장은 더 많은 자연치를 보존하면서도 복잡한 간접 수복 치료가 필요한 고령층에 의해 형성되는 장기적인 수복 수요를 반영하고 있습니다. 65세 이상의 미국 성인은 평균 19.8개의 영구치를 가지고 있는 반면, 20세에서 34세 사이에서는 27개입니다. 이러한 추세로 인해 다단 브리지, 오버덴처, 정밀 부분 의치 프레임워크에 대한 수요가 고령층에 집중되고 있으며, 이러한 치료에서는 정확한 마진 캡처와 안정적인 교합 기록이 빈번히 요구됩니다. 치과 기공소나 클리닉에서는 디지털 기술 도입이 가속화되고 있지만, 복잡한 다단위 증례에 대한 검증 과정은 여전히 아날로그 방식에 머무르는 경우가 많으며, 특히 치은연하 마진이나 전악 패시브 핏의 경우에는 하이브리드 워크플로우 내에서 패티 워시 기법의 일상적인 사용이 계속되고 있습니다. 덴츠프라이 시로나와 폼랩이 협력하여 개발한 인쇄 가능한 의치 시스템 등, 검증된 제조 공정을 갖춘 소재를 통합하는 파트너십을 통해 아날로그 인상 정보가 디지털 설계 및 제조에 활용되는 하이브리드 프로토콜이 더욱 정착되고 있습니다. 북미의 그룹 진료소와 통합 실험실 네트워크 역시 수복 과정을 표준화하고 있으며, 아날로그와 디지털이 서로 대체하는 것이 아니라 상호 보완함으로써, 수정이나 재제작을 줄여주는 고품질 패티 재료에 대한 안정적인 수요를 뒷받침하고 있습니다. 유럽 시장에서는 많은 국가에서 필수적인 수복 서비스에 대한 광범위한 보험 급여가 유지되고 있으며, 치과 병원들은 진료석에서의 조정이나 재진료를 줄이기 위해 적합성이 매우 중요한 재료에 투자하고 있습니다. 이러한 치료 및 지불 측면의 동향이 맞물리면서, 치과용 패스트 시장의 장기적인 전망을 뒷받침하는 안정적인 수복 기반이 유지되고 있습니다.

EU MDR 준수 비용 및 유럽 내 SKU 합리화

유럽의 규제는 인상재 공급업체의 투자 및 제품 포트폴리오 선택에 계속해서 영향을 미치고 있으며, 이로 인해 치과용 접착제 시장에 다소 부정적인 영향을 주고 있습니다. 유럽집행위원회가 2025년 12월에 제안한 MDR 개정안은 맞춤형 기기에 대한 선택적 간소화를 추구한 것이었으나, 표준적인 기성 인상재에 대해서는 여전히 엄격한 임상 평가, 문서화, 지속적인 모니터링 요건이 부과되고 있어 규제 관련 업무 부담은 높은 수준을 유지하고 있습니다. 요구되는 ‘안전성 및 임상 성능 요약’ 문서, 동등성 평가 또는 데 노보 임상 증거, 인증 기관(노티파이드 바디)의 심사 주기는 갱신이나 새로운 변형 제품 출시 소요 기간을 연장시켜, 특정 이용 사례에 특화된 소규모 SKU 제품의 갱신 주기를 지연시킬 가능성이 있습니다. 대형 기존 기업들은 이러한 고정비를 보다 광범위한 제품 라인 전체에 분산함으로써 쉽게 흡수할 수 있으므로, 중소 기업들이 포트폴리오를 합리화하는 과정에서 핵심 시장에서의 입지를 강화할 가능성이 있습니다. 2025년 기업 공시 정보에 따르면, 규제상의 마찰에 직면한 가운데, 핵심 화학 성분 및 판매 속도가 빠른 포맷에 집중하겠다는 방침에 따라 유럽에서는 포트폴리오 합리화가 신중하게 진행되고 있는 것으로 보고되었습니다. 다중 브랜드 생태계와 통합된 유통망을 갖춘 다국적 공급업체들은 이러한 환경에서 탄력성을 발휘하고 있으며, 이는 미세한 변종 제품의 난립이 아닌 주요 페이스트 제품군의 안정적인 공급이 이루어질 것임을 시사합니다. 전반적인 영향으로 볼 때, 유럽 내 단기적인 혁신 확산에는 다소 제약을 주고 있지만, 주요 VPS 및 폴리에테르계 시스템 시장 진입에는 변화가 없습니다.

부문별 분석

2025년 기준으로, 일반 경화형 치과용 접착제는 59.12%의 시장 점유율을 차지하고 있으며, 이는 긴 가소 시간을 활용한 다단계 프로토콜에서의 지속적인 사용을 반영한 것입니다. 속경화형 제품은 임플란트 및 멀티 유닛 적응증 분야에서 임상의들이 진료실 내 효율적인 시간 관리와 진료 과정의 합리화를 중시하는 추세에 힘입어 연평균 성장률(CAGR) 7.98%로 성장할 것으로 전망됩니다. 임상 사용자들은 마진의 정밀도를 유지하면서 구강 내 작업 시간을 단축하기 위해 속경화형을 채택하고 있으며, 이를 통해 여전히 아날로그 방식의 검증이 필요한 증례에서 발생하는 조정 및 재제작 작업을 줄이고 있습니다. 해당 공급업체의 제품 라인업은 예측 가능한 반응 속도와 조작성을 중시한 폴리에테르계 제품에서 볼 수 있듯이, 치은 하부 영역으로의 유입성을 저해하지 않으면서 경화 시간을 단축할 수 있도록 개선되었습니다. 디지털 데이터와 물리적 인상 모두를 수용하는 이 연구소에서는 여전히 인상면의 품질에 주의를 기울이고 있으며, 이것이 크라운·브릿지 치료에서 검증된 일반 경화형 화학 조성물의 지속적인 사용을 뒷받침하고 있습니다. 그 결과, 장시간 경화형에서 급격하게 전환하는 것이 아니라, 증례의 복잡성이 허용하는 범위 내에서 더 빠른 경화형으로의 단계적 전환이 진행되고 있습니다.

속경화형의 발전은 치은연에서 세부적인 재현성을 확보하면서도 구강 내 경화 속도를 높이는 것을 목표로 한 제품 설계를 반영하고 있습니다. 즉시 후방 치아 치료나 재인상 채취 등 시간적 제약이 있는 치료 절차에서는 속경화형 패트를 사용함으로써 총 치료 시간을 단축할 수 있지만, 트레이의 정확한 장착이나 세척 시 형상 유지 측면에서는 여전히 일반 경화형이 표준적인 선택지로 남아 있습니다. 뛰어난 유동성 제어 기능과 빠른 최종 경화 시간을 갖춘 이 첨단 제품군은 수분이나 혈액으로 인해 경계가 불분명해지기 쉬운 치은열구의 랜드마크를 보호하도록 설계되었습니다. 또한, 속경화 유형의 공정 순서나 트레이 관리는 기존의 일상적인 절차와 다를 수 있으므로, 교육 및 팀의 숙련도도 중요한 요소가 됩니다. 예측 기간 동안 두 가지 경화 유형 모두 널리 사용될 것으로 보이지만, 진료 시간 단축과 일일 처리 능력 향상을 추구하는 치과가 늘어남에 따라 속경화 유형의 성장률은 전체 카테고리 평균을 상회할 것으로 보입니다.

VPS 패치는 안정적인 가성비와 다양한 제공 형태를 통한 폭넓은 접근성을 바탕으로, 2025년에는 58.91%의 시장 점유율을 차지했습니다. 한편, 폴리에테르는 연평균 성장률(CAGR) 8.13%로 더 빠른 성장이 예상됩니다. 이는 임플란트 전문의나 보철 전문의가 모형 제작 과정에서 탄성 회복을 최소화함으로써 이점을 얻을 수 있는 다유닛이며 습윤 환경이 까다로운 증례에서 고유한 친수성과 경화 후의 높은 강성을 우선시하기 때문입니다. 임상 실적과 제품 사양을 통해, 폴리에테르가 지혈 시점을 조절하는 데 도움이 되는 스냅셋 특성을 유지하면서도, 빈 공간을 최소화하여 치은연 하부를 확실하게 포착할 수 있는 능력이 강조되고 있습니다. 한편, VPS는 취급이 간편하고 카트리지를 이용한 혼합이 쉬우며, 많은 팀이 트레이와 세척액의 조합에 적용하고 있는 일관된 탄성 회복성 덕분에 일반 치과 진료에서 여전히 주력 제품으로 자리 잡고 있습니다. 각 제조업체들은 크라운·브릿지 치료에 사용되는 더블 믹스법을 지원하는 서로 보완적인 점도를 가진 제품을 지속적으로 출시하고 있으며, 이 분야에서 VPS는 확고한 입지를 다지고 있습니다.

두 화학 계열을 모두 아우르는 멀티 브랜드 포트폴리오 덕분에, 클리닉과 연구소는 공급업체를 변경하지 않고도 사례별 요구 사항에 맞추어 재료를 선택할 수 있게 됩니다. 이를 통해 훈련 시간이 단축되고, 연구실과의 의사소통의 일관성이 유지됩니다. 어려운 임플란트 인상 채취 시, 폴리에테르의 강성은 마스터 캐스트 제작 및 타워 정렬 과정에서 코핑의 안정성을 유지하는 데 도움이 됩니다. 한편, VPS는 조작이 빠르고 익숙한 사용감 덕분에 많은 단일 치아 및 다수 치아 지지 사례에서 여전히 선호되고 있습니다. 장기적인 관점에서 볼 때, VPS는 광범위한 적응증을 기반으로 하고, 폴리에테르는 습윤 상태에서 가장자리의 정밀도가 필수적인 까다로운 조건의 부위에서 점차 적용 범위를 넓혀가는 등, 지속적인 공존 관계가 예상됩니다. 전반적으로, 치과용 접착제 시장은 한 기술이 다른 기술을 대체하는 것이 아니라, 화학 성분의 선택지가 다양화됨에 따라 발전하고 있으며, 이는 하이브리드 방식의 아날로그·디지털 워크플로우 내에서 사례별로 선택이 이루어지고 있음을 반영합니다.

지역별 분석

북미는 2025년에 36.74%의 점유율을 차지했습니다. 이는 그룹 진료소의 성숙한 조달 체계, 첨단 재료에 대한 접근성, 그리고 실험실과의 긴밀한 협력 관계에 힘입은 결과입니다. 아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 중국, 인도, 동남아시아에서 진료소의 수용 능력이 강화되고, 치과 관광이 확대되며, 중산층 환자층이 확대됨에 따라 2031년까지 연평균 성장률(CAGR)은 9.73%를 나타낼 것으로 전망됩니다. 유럽은 2025년에 중요한 위치를 차지하고 있었지만, 기업들은 소모품 및 교체와 관련된 MDR(의료기기 규정)로 인한 규제 대응 업무에 계속해서 매진하고 있으며, 이는 주요 인상재 제품군에 대한 접근성에는 변화를 주지 않으면서 비용과 시간을 증가시키고 있습니다. 라틴아메리카에서는 무치악의 유병률이 높아, 정확한 인상 채취에 의존하는 보철 치과 및 임플란트 지지형 솔루션에 구조적인 호재가 되고 있습니다. 북미와 서유럽에서는 임상 워크플로우에서 아날로그와 디지털 공정이 결합되는 경우가 많으며, 증례의 복잡성이 높아지면 아날로그 방식에 의한 검증이 이루어지기 때문에 다수 치아 치료나 전악 치료에서 프리미엄 퍼티의 사용이 여전히 유지되고 있습니다. 이러한 경향은 적합 정확도를 중시하면서도 실험실의 생산성 향상을 반영하는 하이브리드 모델과 일치합니다.

아시아태평양 전체에서는 고령화와 구강 위생에 대한 인식이 높아짐에 따라, 정확한 인상 채취에 의존하는 간접 수복 치료에 대한 지속적인 수요가 발생하고 있습니다. 질병 부담에 관한 조사에 따르면, 구강 질환을 앓고 있는 전 세계 인구는 여전히 많으며, 개선 폭은 극히 미미한 것으로 나타났는데, 이는 수요가 많은 시장에서 정밀 소재의 지속적인 소비를 뒷받침하고 있습니다. 북미의 그룹 진료소에서는 디지털 플랫폼과 공동 조달을 통해 진료 사례 배정 및 재료 선택을 지속적으로 표준화하고 있으며, 이로 인해 각 지점의 소모품 수요가 안정적으로 유지되고 있습니다. 캐나다에서는 최근 조사 결과 무치악의 유병률을 측정할 수 있음이 밝혀졌으며, 이는 보철 치료에 대한 안정적인 수요가 있음을 뒷받침하고 있습니다. 한편, 미국의 감시 조사 결과, 특정 성인 하위 집단에서 치료받지 않은 충치 비율이 높은 것으로 드러났으며, 이는 간접 보철 사례의 꾸준한 유입으로 이어지고 있습니다. 유럽공급업체들은 MDR(의료기기 규정)에 따라 제품 포트폴리오를 합리화하는 한편, 주력 퍼티 제품군에 대한 지속적인 접근성을 확보함으로써, 보다 집중된 제품 라인업 범위 내에서 안정적인 공급을 보여주고 있습니다.

중동 및 아프리카에서는 진료소 및 연수에 대한 투자를 통해 첨단 재료에 대한 접근성이 확대되고 있지만, 많은 국가에서는 여전히 치과의사와 인구 비율이 치료 건수를 제한하고 있습니다. 라틴아메리카에서는 높은 무치악 유병률이 보철 치료 수요를 뒷받침하고 있으며, 연령 조정율의 변화를 보여주는 연구도 있지만, 절대적인 사례 수 증가로 인해 보철 치료 수요는 계속해서 두드러지게 나타나고 있습니다. 유럽의 주요 경제국에서 각 벤더 기업들은 엄격한 문서화 기준을 충족하는 핵심 제품 라인업에 주력하고 있으며, 규제 비용을 분산할 수 있는 다양한 브랜드 제품군에 의해 뒷받침되고 있습니다. 지역 전체의 동향을 살펴보면, 선진국 시장에서는 수요가 안정적이며, 아시아태평양에서는 수요가 급속히 증가하고, 라틴아메리카에서는 환자 수가 꾸준히 늘어나고 있어, 이러한 전반적인 추세가 치과용 접착제 시장의 장기적인 전망을 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the dental putty market size is projected to expand from USD 368.23 million in 2025 and USD 394.93 million in 2026 to USD 560.41 million by 2031, registering a CAGR of 7.25% between 2026 to 2031.

This report is Segmented by Type (Regular Set, and Fast Set), Product Type (VPS (A-Silicone) Putty, Polyether Putty, Condensation Silicone (C-Silicone) Putty), Application (Prosthodontics, Implantology, and More), Delivery Form (Hand-Mix Jars, Automix Cartridges, and More), End-User (Dental Clinics, Hospitals, and More), and Geography (North America, Europe, and More). The Market and Forecasted in Terms of Value (USD).

Global Dental Putty Market Trends and Insights

Rising Prevalence of Oral Diseases and Edentulism

The dental putty market benefits from a sustained clinical need that tracks the global burden of oral disease. According to the Journal of Periodontal Research, periodontitis remains one of the most prevalent global diseases, calling the newest global data a "serious wake-up call." It emphasized that severe periodontitis affects ~11% of the world's population, consistent with Global Burden of Disease (GBD) estimates, moving edentulism higher among conditions that drive disability, which sustains indirect restorative demand for precision impressions in complex rehabilitations. China is expected to account for 130.23 million edentulous individuals by 2050, or 19.67% of the global total, reinforcing the need for accurate impression capture across large treatment volumes. In the United States, surveillance data for 2017 to early 2020 show untreated caries in 21% of adults aged 20 to 64 and 13% of seniors, with much higher rates among high-poverty groups and current smokers, which underpins steady indirect case flow and periodic full-arch rehabilitations. Manufacturers also cite edentulism trends to justify investments in denture and overdenture workflows, such as the Dentsply Sirona partnership with Formlabs that aligns materials, printers, and validation to scale digital denture production while maintaining analog intake when clinically appropriate. Analyses from global disease-burden programs have recorded minimal progress in reducing the total population affected by oral conditions, which continues to reinforce the dental putty market across prosthodontics and implantology.

Growing Demand for Restorative and Prosthodontic Procedures

The dental putty market tracks long-term restorative needs shaped by aging cohorts who retain more natural teeth yet require complex indirect treatments. U.S. adults aged 65 and older retain a mean of 19.8 permanent teeth compared with 27 among those aged 20 to 34, a pattern that concentrates multi-unit bridges, overdentures, and precision partial frameworks in senior populations who often need accurate margin capture and stable occlusal records. Digital technologies are accelerating in labs and clinics, yet verification steps for intricate multi-unit cases often remain analog, especially for subgingival margins or full-arch passive fits, which sustain routine use of putty-wash techniques within hybrid workflows. Partnerships that integrate materials with validated production routes, such as Dentsply Sirona's collaboration with Formlabs on printable denture systems, further normalize hybrid protocols where analog impressions feed digital design and manufacture. North American group practices and integrated lab networks also standardize restorative pathways, where analog and digital complement each other rather than displace, supporting steady demand for premium putty chemistries that reduce rework and remakes. European markets maintain broad reimbursement for essential restorative services in many countries, and clinics invest in fit-critical materials to reduce chairside adjustments and follow-up visits. Together these procedural and payment dynamics maintain a stable restorative base that underpins long-run visibility for the dental putty market.

EU MDR Compliance Costs and SKU Rationalization in Europe

European regulations continue to shape investment and portfolio choices for impression-material suppliers, which modestly weighs on the dental putty market. The European Commission's targeted MDR revision proposal in December 2025 pursued selective simplifications for custom-made devices, yet standard off-the-shelf impression materials remain subject to strict clinical evaluation, documentation, and ongoing surveillance requirements, keeping regulatory workloads elevated. The required Summary of Safety and Clinical Performance documentation, equivalence assessments, or de novo clinical evidence, and notified-body cycles extend timeframes for updates and new variants, which can slow the refresh cadence for smaller SKUs that serve narrow use cases. Larger incumbents can absorb these fixed costs more easily by spreading them across wider catalogs, which can reinforce their position in core markets as smaller players rationalize portfolios. Company disclosures in 2025 reported measured portfolio streamlining in Europe, consistent with a focus on core chemistries and high-velocity formats in the face of regulatory friction. Multinational suppliers with multi-brand ecosystems and integrated distribution have highlighted resilience in this environment, which points to a steady supply of key putty families rather than a proliferation of micro-variants. The overall effect is a modest dampener on near-term innovation breadth in Europe, yet market access for major VPS and polyether systems remains unchanged.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in VPS/Polyether Putty Performance

- Lab Digitalization Steering Clinicians Toward Scan-First Workflows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Regular-set dental putty held 59.12% share in 2025, reflecting consistent use in multi-step protocols that benefit from longer workable time. Fast-set variants are projected to grow at 7.98% CAGR, helped by clinicians' focus on efficient chairside timing and streamlined case progression in implant and multi-unit indications. Clinical users adopt fast-set to reduce intraoral time while sustaining margin fidelity, which reduces adjustments and remakes in cases that still need analog verification. Vendor portfolios have been updated to bring shorter set times without sacrificing flow into subgingival areas, as seen in polyether families that emphasize predictable kinetics and handling control. Labs that accept both digital files and physical impressions remain attentive to impression surface quality, which supports sustained use of proven regular-set chemistries in crown-and-bridge work. The result is a gradual shift toward faster options where case complexity allows them, rather than a sharp pivot away from longer sets.

Fast-set progress reflects product design aimed at faster intraoral set while protecting detail capture at the margin. In time-sensitive protocols such as immediate posterior work or retakes, fast-set putties can keep total chair time low, while regular-set options remain the default for precise tray seating and wash capture. Advanced families with robust flow control and rapid final set times are designed to protect sulcular landmarks where moisture or blood can obscure lines. Training and team familiarity also play a role, since the step sequence and tray management in fast-set variants can differ from legacy routines. Over the forecast period, both sets remain in broad use, with fast-set growth outpacing the category as more clinics pursue shorter appointments and higher daily throughput.

VPS putty accounted for 58.91% share in 2025, supported by a stable cost-to-performance balance and wide availability across delivery formats. Polyether is set to grow faster at 8.13% CAGR as implantologists and prosthodontists prioritize intrinsic hydrophilicity and higher post-set rigidity for multi-unit, moisture-challenged cases that benefit from minimal elastic recovery during model work. Field evidence and product specifications emphasize polyether's ability to capture subgingival margins with fewer voids while maintaining the snap-set behavior that helps manage hemostasis windows. VPS remains the workhorse in general practice, given familiar handling, ease of mixing in cartridges, and consistent elastic recovery that many teams have built into their tray and wash combinations. Manufacturers continue to position complementary viscosities that support double-mix approaches for crown-and-bridge care, which is where VPS shows resilient traction.

Multi-brand portfolios that include both chemistries allow clinics and labs to match material choice to case needs without switching vendors, which reduces training time and supports consistency in lab communication. For challenging implant impressions, polyether's rigidity helps maintain coping stability during master-cast fabrication and tower alignment, while VPS remains favored for many single- and multi-unit tooth-borne cases due to handling speed and familiarity. The long-term picture shows durable co-existence, with VPS anchoring broad indications and polyether expanding in demanding sites where marginal fidelity under moisture is non-negotiable. Overall, the dental putty market advances through chemistry choice rather than displacement, reflecting case-by-case selection inside hybrid analog-digital workflows.

Geography Analysis

North America held 36.74% share in 2025, supported by mature procurement in group practices, access to advanced materials, and integrated lab relationships. Asia-Pacific is the fastest-growing region with a 9.73% projected CAGR to 2031 as clinics add capacity, dental tourism scales, and middle-income patient pools expand in China, India, and Southeast Asia. Europe held a significant position in 2025, though companies continue to navigate MDR-driven regulatory workloads for consumables and updates, which adds cost and time without changing access to core impression-material families. Latin America carries a high edentulism prevalence, which creates structural tailwinds for prosthodontics and implant-supported solutions that rely on accurate impression capture. In North America and Western Europe, clinical workflows often combine analog and digital steps, using analog verification when case complexity rises, which sustains premium putty use in multi-unit and full-arch work. These patterns align with a hybrid model that favors fit accuracy while absorbing lab productivity gains.

Across the Asia-Pacific region, aging populations and rising oral-health awareness create a persistent demand for indirect treatments that depend on accurate impressions. Disease-burden research indicates the global count of people affected by oral conditions remains large and shows minimal improvement, which supports continued consumption of precision materials in high-volume markets. North American group practices continue to standardize case routing and material choice through digital platforms and shared procurement, which keep consumables demand steady across locations. In Canada, recent cycles document measurable edentulism prevalence, reinforcing steady prosthodontic volume, while U.S. surveillance highlights higher untreated decay rates in certain adult subgroups, translating into stable indirect case flows 150. European suppliers report portfolio streamlining under MDR alongside continued access to flagship putty ranges, indicating steady supply within a more focused set of variants.

In the Middle East and Africa, investment in clinics and training expands access to advanced materials, though dentist-to-population ratios still limit procedural throughput in many countries. Latin America's high edentulism prevalence underpins prosthodontic care, with studies documenting shifts in age-standardized rates but growth in absolute case counts that keep restorative demand visible. In Europe's largest economies, vendors focus on core catalogues that meet stringent documentation standards, supported by diversified brand families that can amortize regulatory costs. Overall regional dynamics point to a stable demand profile in developed markets, a faster rise in Asia-Pacific, and steady case growth in Latin America that together support the long-run outlook for the dental putty market.

- Coltene Holding

- DenMat Holdings

- Dentsply Sirona

- DMG Chemisch-Pharmazeutische Fabrik

- GC Corporation

- Huge Dental Material Co., Ltd.

- Ivoclar Vivadent

- Kaniedenta GmbH & Co. KG

- Kerr Corporation (Envista Holdings Corporation)

- Kettenbach GmbH & Co. KG

- Kulzer GmbH (Mitsui Chemicals Group)

- Muller-Omicron GmbH & Co. KG

- Parkell, Inc.

- Solventum Corporation (3M Oral Care)

- VOCO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Oral Diseases and Edentulism

- 4.2.2 Growing Demand for Restorative and Prosthodontic Procedures

- 4.2.3 Advancements in VPS/Polyether Putty Performance

- 4.2.4 Aging Demographics Increasing Complex Indirect Cases

- 4.2.5 Analog Impressions Remain Preferred for Challenging Cases

- 4.2.6 Capital Constraints Slowing Scanner Adoption in Cost-Sensitive Clinics

- 4.3 Market Restraints

- 4.3.1 Rapid Adoption of Intraoral Scanners in Selected Specialties

- 4.3.2 Higher Cost of Premium Putties Vs Alginate nd Technique Sensitivity

- 4.3.3 EU MDR Compliance Costs and SKU Rationalization in Europe

- 4.3.4 Lab Digitalization Steering Clinicians Toward Scan-First Workflows

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Regular Set

- 5.1.2 Fast Set

- 5.2 By Product Type

- 5.2.1 VPS (A-silicone) Putty

- 5.2.2 Polyether Putty

- 5.2.3 Condensation Silicone (C-silicone) Putty

- 5.3 By Application

- 5.3.1 Prosthodontics (fixed and removable)

- 5.3.2 Implantology

- 5.3.3 Restorative Dentistry (indirect)

- 5.3.4 Orthodontics and Occlusal Records

- 5.4 Delivery Form

- 5.4.1 Hand-mix Jars

- 5.4.2 Automix Cartridges

- 5.4.3 Unit-dose / Preportioned Packs

- 5.5 End-User

- 5.5.1 Dental Clinics

- 5.5.2 Hospitals

- 5.5.3 Dental Laboratories

- 5.5.4 Academic & Research Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 COLTENE Holding AG

- 6.3.2 DenMat Holdings

- 6.3.3 Dentsply Sirona Inc.

- 6.3.4 DMG Chemisch-Pharmazeutische Fabrik GmbH

- 6.3.5 GC Corporation

- 6.3.6 Huge Dental Material Co., Ltd.

- 6.3.7 Ivoclar Vivadent AG

- 6.3.8 Kaniedenta GmbH & Co. KG

- 6.3.9 Kerr Corporation (Envista Holdings Corporation)

- 6.3.10 Kettenbach GmbH & Co. KG

- 6.3.11 Kulzer GmbH (Mitsui Chemicals Group)

- 6.3.12 Muller-Omicron GmbH & Co. KG

- 6.3.13 Parkell, Inc.

- 6.3.14 Solventum Corporation (3M Oral Care)

- 6.3.15 VOCO GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment