|

시장보고서

상품코드

2063574

아연 폴리카복실산염 시멘트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Zinc Polycarboxylate Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

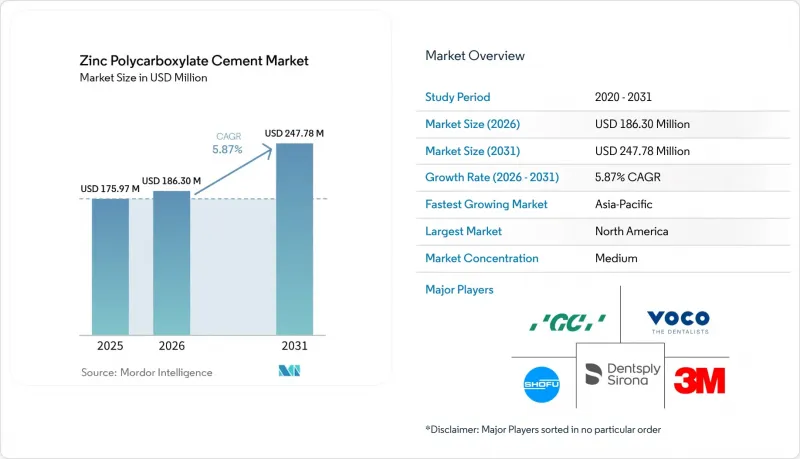

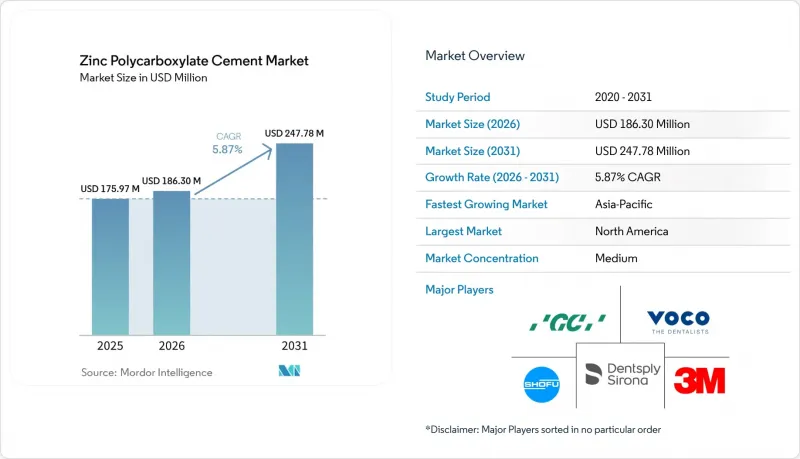

아연 폴리카복실산염 시멘트 시장 규모는 2025년 1억 7,597만 달러로 평가되었습니다. 2026년 1억 8,630만 달러에서 2031년까지 2억 4,778만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.87%를 나타낼 것으로 예측됩니다.

본 보고서는 형태(분말, 액체), 용도(크라운·브릿지 시멘트 고정, 교정용 밴드·브래킷 접착, 우식 부위 베이스·라이너 등), 최종 사용자(병원, 치과, 학술·연구 기관, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 아연 폴리카복실산염 시멘트 시장 동향 및 분석

단관용 금속 및 지르코니아 수복물 증가

지르코니아 및 금속 크라운의 체어사이드 제작이 증가함에 따라 아연 폴리카복실산염 시멘트 시장의 성장을 견인하고 있습니다. 이 시멘트는 별도의 프라이머 없이도 화학적으로 결합하기 때문에 고처리량 환경에서 작업 시간을 대폭 단축할 수 있습니다. 지르코니아의 낮은 투과성은 약간 불투명한 시멘트 라인을 효과적으로 가려주며, 임상의가 적당한 습윤 조건에서 보철물을 장착할 수 있게 해주기 때문에 소수성 레진 시멘트에 비해 실용적인 이점이 있습니다. 태국이나 멕시코와 같은 치과 관광의 중심지에서는 ISO 9917 표준을 준수하는 제품이 선호되고 있습니다. 이로 인해 외딴 지역의 진료소에서는 광중합용 램프가 더 이상 필요하지 않게 됩니다. 미국에서는 단체 구매 조직이 메디케이드의 아동 대상 프로그램을 위해 아연 폴리카복실산염 시멘트와 스테인리스 스틸 크라운 키트를 세트로 판매하고 있으며, 이는 이 틈새 시장의 견조한 성장세를 보여주고 있습니다. CAD/CAM 워크플로우가 확대되는 가운데, 이 시멘트의 얇은 두께는 여전히 가장자리 틈새 요건을 충족하고 있어, 디지털 시대에도 그 유용성이 보장되고 있습니다.

소아 치과 및 노인 치과에서의 도입 가속화(레진 시멘트에 대한 과민증)

소아 및 고령 환자 대상 임상 프로토콜에서는 비스페놀 A 및 기타 감작성 단량체를 피하는 생체적합성이 높은 시멘트법이 점점 더 중요시되고 있으며, 이는 아연 폴리카복실산염 시멘트 시장의 꾸준한 성장에 기여하고 있습니다. 유치 어금니에 장착된 스테인리스 스틸 크라운은 기존의 산-염기 시멘트로 고정했을 경우, 5년 생존율이 93-97%를 기록하여, 복합 레진 재료를 이용한 대체 방법보다 현저히 우수한 성과를 보이고 있습니다. 미국 65세 이상 성인의 치근 우식 유병률은 60%에 달하며, 이 시멘트의 불소 방출 기능과 내습성은 이러한 증례에 특히 적합합니다. 또한, 다제 병용으로 인한 구강 건조증은 레진계 시멘트의 유효성을 더욱 제한하기 때문에 기존의 화학적 조성을 가진 시멘트가 선호되는 경향이 더욱 강해지고 있습니다. 유럽연합(EU)의 소아용 BPA 금지 조치는 이러한 추세를 더욱 가속화하고 있으며, 각 공급업체들은 가족 진료소를 유치하기 위해 BPA가 함유되지 않았음을 강조하는 표시를 하고 있습니다.

수지 개질 유리 이오노머 및 레진 시멘트의 대체재

현재, 레진 하이브리드 시멘트는 지르코니아에 대해 1.39 MPa의 전단 접착 강도를 나타내며, 기존 유리 이오노머의 0.85 MPa라는 접착 강도를 상회하고 있습니다. 또한, 이러한 시멘트는 교합 하중 하에서 세척에 대한 강한 내성을 보입니다. 디지털 밀링 센터에서는 CAD/CAM 온레이의 고정력을 확보하기 위해 이러한 수지의 사용이 표준화되었으며, 이전에는 아연 폴리카복실산염 시멘트 시장이 주도하던 고가 사례를 확보하고 있습니다. 특히 주목할 만한 진전으로, 2026년 3월 GC America가 SprintRay와 제휴를 맺음으로써 CAD 파일을 성형기에 직접 연동하여, 수지 접착에 최적화된 10개의 유닛을 불과 10분 만에 제조할 수 있게 되어 생산 공정이 효율화되었습니다. 보험사가 디지털 크라운 비용을 기존과 동일하게 보상하게 됨에 따라, 임상의들은 이러한 솔루션으로의 전환을 가속화하고 있으며, 기존 시멘트의 사용량은 감소 추세를 보이고 있습니다.

부문별 분석

2025년, 분말 부문은 아연 폴리카복실산염 시멘트 시장에서 58.40%라는 압도적인 점유율을 차지했습니다. 이는 다양한 점도를 얻기 위해 진료실에서 직접 조제를 하는 병원 및 교육 기관 수요에 힘입은 결과입니다. 이들 조직은 장기 계약을 통해 Kg 단위의 드럼통을 구매하고 있으며, 이를 통해 예산을 효과적으로 관리하고 제품의 유통기한 만료로 인한 손실을 줄이고 있습니다. 또한, 분말 및 액체 형태의 키트는 플라스틱 캡슐의 폐기를 줄이는 데 도움이 되며, 의료시설의 지속가능성 목표에도 부합합니다.

한편, 액상 캡슐은 연평균 성장률(CAGR) 5.98%를 기록하며 꾸준히 성장하고 있습니다. 이는 특히 코로나19 팬데믹 이후 도입된 엄격한 감염 관리 지침에 따라, 클리닉들이 1회 투여의 편의성과 신속한 정리 정돈을 점점 더 중요하게 여기고 있기 때문입니다. 캡슐화된 투여 시스템은 시술자의 혼합 실수를 최소화해 주며, 유리판이 없는 이동식 치과 유닛에 특히 매력적입니다. 인도에서는 신생 브랜드들이 액체에 직접 녹일 수 있는 호일 파우치 포장 분말을 출시하고 있으며, 이로 인해 부문 간의 구분이 더욱 모호해지고 시장 침투가 촉진되고 있습니다.

지역별 분석

2025년, 북미는 아연 폴리카복실산염 시멘트 시장 점유율의 39.67%를 차지했습니다. 이는 ISO 기준을 준수하고 BPA가 함유되지 않은 시멘트 사용을 의무화하는 메디케이드 및 재향군인부 계약에 근거한 것입니다. 통합된 공급망을 통해 다년 계약이 확보되어 안정적인 공급이 보장될 뿐만 아니라, 소아 치과 치료에서 적응증 외 레진 사용에 따른 위험도 줄어들고 있습니다. 이 지역에서는 미국이 주도적인 위치를 차지하고 있으며, 매출의 약 85%를 차지하고 있고, 나머지는 캐나다와 멕시코가 공적 의료보험 제도 및 국경을 넘는 진료를 통해 차지하고 있습니다.

아시아태평양은 가장 빠른 성장이 예상되며, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.15%를 기록할 전망입니다. 이러한 성장은 수입 관세를 인하하고 제품 등록 절차를 가속화하는 중국과 인도의 현지화 이니셔티브에 힘입어 이루어지고 있습니다. 인도네시아와 베트남에서 가처분 소득이 증가함에 따라, 복원 치료에 대한 본인 부담 비용이 늘어나고 있습니다. 또한, 인도 농촌 지역의 정부 치과 프로그램에서는 열대 기후의 보관 조건을 견딜 수 있다는 이유로 분말 키트가 선호되고 있습니다. 일본에서는 고령화가 진행됨에 따라, 시멘트의 불소 방출 특성을 활용한 비침습적 수복 치료에 대한 수요가 꾸준히 증가하고 있습니다.

유럽, 남미, 중동 및 아프리카가 나머지 시장 수요를 합쳐 차지하고 있습니다. 유럽에서는 임상의들이 BPA 금지 조치에 적응해 나가고 있으며, 소아용 제품의 경우 기존의 화학 성분을 선호하는 경향이 있어 완만한 성장세를 보이고 있습니다. 브라질의 공적 의료 제도인 SUS 네트워크에서는 비용 관리를 병행하면서 ISO 9917의 방사선 불투과성 기준을 충족하기 위해 국내에서 조제된 분말을 조달하고 있습니다. 두바이에서는 민간 클리닉들이 환자의 결제 방식에 따라 고급 레진과 기존의 분말을 번갈아 사용하고 있습니다. 남아프리카의 이동 진료 프로그램에서는 휴대성이 뛰어난 호일 팩 형태의 분말 키트가 사용되고 있으며, 아연 폴리카복실산염 시멘트 시장에서 각 주별로 안정적인 수요가 유지되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the zinc polycarboxylate cement market size is projected to expand from USD 175.97 million in 2025 and USD 186.30 million in 2026 to USD 247.78 million by 2031, registering a CAGR of 5.87% between 2026 to 2031.

This report is Segmented by Form (Powder, Liquid), Application (Crown & Bridge Cementation, Orthodontic Band/Bracket Luting, Cavity Base/Liner, and More), End User (Hospitals, Dental Clinics, Academic & Research Institutes, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Zinc Polycarboxylate Cement Market Trends and Insights

Rising Volume of Single-Unit Metal and Zirconia Restorations

The increasing chairside production of zirconia and metal crowns is driving growth in the zinc polycarboxylate cement market. This cement chemically bonds without requiring separate primers, offering significant time savings in high-throughput environments. Zirconia's low translucency effectively conceals the slightly opaque cement line, and clinicians can seat units under moderate moisture, providing a practical advantage over hydrophobic resin cements. Dental tourism hubs such as Thailand and Mexico prefer ISO 9917-compliant products, which eliminate the need for light-curing lamps in remote outreach clinics. In the United States, group purchasing organizations bundle zinc polycarboxylate cements with stainless-steel crown kits for Medicaid children's programs, demonstrating the niche's resilience. As CAD/CAM workflows expand, the cement's low film thickness continues to meet marginal gap requirements, ensuring its relevance in the digital era.

Accelerating Adoption in Pediatric & Geriatric Dentistry (Hypersensitivity to Resin Cements)

Clinical protocols for pediatric and geriatric patients increasingly favor biocompatible cementation methods that avoid bisphenol A and other sensitizing monomers, contributing to the steady growth of the zinc polycarboxylate cement market. Stainless-steel crowns on primary molars exhibit a five-year survival rate of 93-97% when seated with conventional acid-base cements, significantly outperforming composite alternatives. Among U.S. adults aged 65 and older, root caries prevalence reaches 60%, making the cement's fluoride release and moisture tolerance particularly suitable for these cases.Additionally, xerostomia caused by polypharmacy further limits the effectiveness of resin-based cements, reinforcing the preference for traditional chemistries. The European Union's pediatric BPA ban has further accelerated this trend, with suppliers emphasizing BPA-free labeling to attract family clinics.

Substitution by Resin-Modified Glass Ionomers & Resin Cements

Resin-hybrid cements now deliver a shear bond strength of 1.39 MPa to zirconia, outperforming the 0.85 MPa bond strength of conventional glass ionomers. These cements also exhibit strong resistance to washout under occlusal stress. Digital milling centers have standardized the use of these resins to ensure retention on CAD/CAM onlays, capturing higher-value cases that were previously dominated by the zinc polycarboxylate cement market. In a notable development, GC America's collaboration with SprintRay in March 2026 has streamlined production by linking CAD files directly to a press capable of producing ten units optimized for resin bonding in just ten minutes. With insurers now reimbursing digital crowns at parity, clinicians are increasingly transitioning to these solutions, reducing the volume of legacy cements.

Other drivers and restraints analyzed in the detailed report include:

- Cost Advantage Over Resin-Based Cements in Emerging Markets

- Demand for Self-Adhesive, Faster-Setting ZPC Formulations

- Higher Water Solubility & Marginal Leakage Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the powder segment held a dominant 58.40% share of the zinc polycarboxylate cement market, driven by hospitals and teaching institutions that mix chairside for varied viscosities. These organizations procure kilogram drums through long-term contracts, effectively managing budgets and reducing losses due to product expiration. Additionally, powder-liquid kits help avoid plastic capsule waste, aligning with sustainability objectives in healthcare facilities.

Liquid capsules, however, are growing at a steady 5.98% CAGR as clinics increasingly prefer single-dose consistency and faster cleanup, particularly under stringent infection-control protocols introduced after the COVID-19 pandemic. The capsulated delivery system minimizes operator mixing errors and is particularly appealing to mobile dental units that lack glass slabs. In India, emerging brands are introducing foil-pouch powders that dissolve directly in proprietary liquids, further narrowing the distinction between segments and enhancing market penetration.

Geography Analysis

In 2025, North America captured 39.67% of the zinc polycarboxylate cement market share, supported by Medicaid and Veterans Affairs contracts that require ISO-compliant, BPA-free cements. Integrated delivery networks secure multiyear tenders, ensuring consistent supply and reducing risks associated with off-label resin use in pediatric applications. The United States dominates the region, contributing approximately 85% of sales, while Canada and Mexico account for the remainder through public benefit plans and cross-border clinics.

Asia-Pacific is projected to experience the fastest growth, with a 6.15% CAGR from 2026 to 2031. This growth is driven by localization initiatives in China and India, which lower import tariffs and accelerate product registration. Increasing disposable incomes in Indonesia and Vietnam are boosting out-of-pocket spending on restorative treatments. Additionally, government dental programs in rural India prefer powder kits due to their ability to withstand tropical storage conditions. Japan's aging population is driving consistent demand for atraumatic restorative treatments, leveraging the cement's fluoride release properties.

Europe, South America, and the Middle East & Africa collectively account for the remaining market demand. Europe is witnessing moderate growth as clinicians adapt to BPA bans and prefer traditional chemistries for pediatric applications. Brazil's public SUS network procures domestically blended powders to meet ISO 9917 radiopacity standards while managing costs. In Dubai, private clinics alternate between premium resins and conventional powders based on patient payment methods. South Africa's mobile outreach programs rely on foil-pack powder kits for their portability, maintaining steady demand across provinces in the zinc polycarboxylate cement market.

- 3M

- Dentsply Sirona

- DMP Dental

- GC Corporation

- Harvard Dental International

- Hoffmann Dental Manufaktur

- Imicryl Dental

- Kerr (Envista)

- Medental International

- Pentron (Coltene)

- Perfection Plus

- Prevest DenPro

- Prime Dental Products

- Septodont

- Shanghai Medical Instrument Co.

- Shanghai Qing Pu Dental Materials

- Shanghai Rongxiang Dental Material

- Shanghai Yuwei Dental Materials

- Shofu

- VOCO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Volume of Single-Unit Metal and Zirconia Restorations

- 4.2.2 Accelerating Adoption in Pediatric & Geriatric Dentistry (Hypersensitivity to Resin Cements)

- 4.2.3 Cost Advantage Over Resin-Based Cements in Emerging Markets

- 4.2.4 Demand For Self-Adhesive, Faster-Setting ZPC Formulations

- 4.2.5 OEM Outsourcing by Global Brands to Asian Toll Manufacturers

- 4.2.6 Regulatory Shift Toward BPA-Free Materials Pushing Legacy Chemistries

- 4.3 Market Restraints

- 4.3.1 Substitution By Resin-Modified Glass Ionomers & Resin Cements

- 4.3.2 Higher Water Solubility & Marginal Leakage Concerns

- 4.3.3 Stringent Radiopacity & Biocompatibility Testing Raising Costs

- 4.3.4 Supply Volatility of High-Purity Zinc Oxide Feedstock

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Form

- 5.1.1 Powder

- 5.1.2 Liquid

- 5.2 By Application

- 5.2.1 Crown & Bridge Cementation

- 5.2.2 Orthodontic Band/Bracket Luting

- 5.2.3 Cavity Base / Liner

- 5.2.4 Temporary / Pediatric Restorations

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Dental Clinics

- 5.3.3 Academic & Research Institutes

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Dentsply Sirona

- 6.3.3 DMP Dental

- 6.3.4 GC Corporation

- 6.3.5 Harvard Dental International

- 6.3.6 Hoffmann Dental Manufaktur

- 6.3.7 Imicryl Dental

- 6.3.8 Kerr (Envista)

- 6.3.9 Medental International

- 6.3.10 Pentron (Coltene)

- 6.3.11 Perfection Plus

- 6.3.12 Prevest DenPro

- 6.3.13 Prime Dental Products

- 6.3.14 Septodont

- 6.3.15 Shanghai Medical Instrument Co.

- 6.3.16 Shanghai Qing Pu Dental Materials

- 6.3.17 Shanghai Rongxiang Dental Material

- 6.3.18 Shanghai Yuwei Dental Materials

- 6.3.19 Shofu

- 6.3.20 VOCO GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment