|

시장보고서

상품코드

2063539

로봇 반려동물 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Robotic Pet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

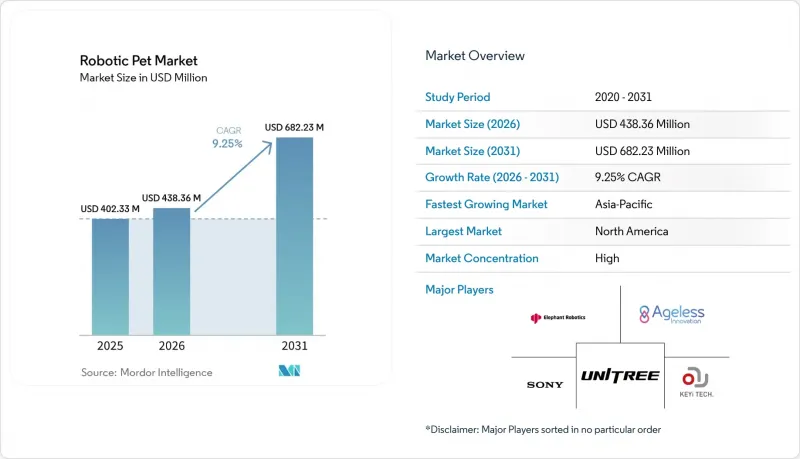

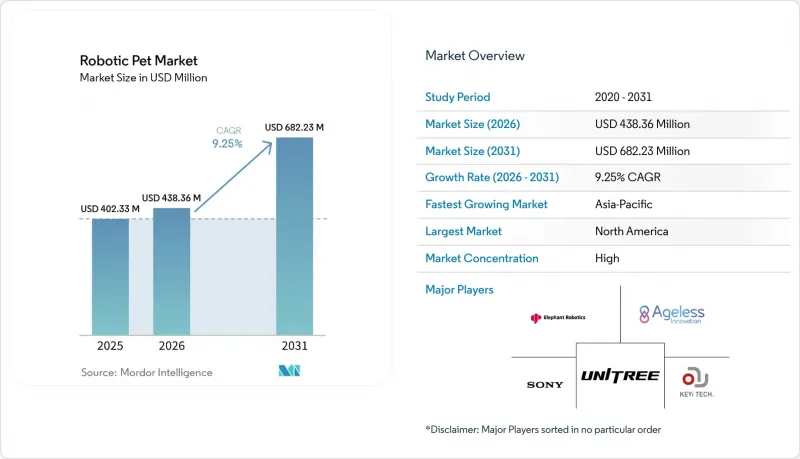

Mordor Intelligence에 의하면, 로봇 반려동물 시장 규모는 2025년에 4억 233만 달러, 2026년에 4억 3,836만 달러, 2031년까지 6억 8,223만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 9.25%로 성장할 전망입니다.

본 보고서는 제품 유형(4족 보행 로봇 등), 용도(가정용 등), 가격대(200달러 미만 등), 판매 채널(소매점·장난감 체인점 등) 및 지역(북미, 유럽, 아시아·태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 로봇 반려동물 시장 동향과 인사이트

고령화와 고독감이 동반자 로봇의 보급을 촉진하고 있습니다.

주요 시장에서 65세 이상 인구가 지속적으로 증가함에 따라, 사회적 고립을 완화하고 일상적인 교류를 지원할 수 있는 동반자 기술에 대한 시설 및 재택 환경에서 수요가 증가하고 있습니다. 중국의 공식적인 논의와 전국 언론 보도에서는 돌봄 인력 부족과 증가하는 돌봄 수요에 광범위하게 대응하기 위한 조치의 일환으로, 노인 돌봄의 부담과 새로운 로봇 동반자의 역할이 강조되고 있습니다. 이러한 인구 통계학적 요인의 뒷받침으로, 로봇 반려동물 시장은 단순한 신기함의 단계를 넘어, 요양 현장에서 인간과의 교류를 보완하는 확장성이 뛰어나고 비용 효율적인 존재로 자리매김하고 있습니다. 정책 입안자와 지역 의료 제공업체들은 재택 및 시설 거주자들에게 일관된 교류 패턴을 제공하고, 장기적인 이용을 지원할 수 있는 솔루션을 시범 운영하고 있습니다. 이러한 노력은 도입을 정착시키고 일상생활로의 통합을 위한 학습 곡선을 가속화하는 데 도움이 되며, 로봇 반려동물 시장의 성장세를 유지하고 있습니다.

치매 및 자폐증에 대한 임상적 유효성이 치료적 활용을 뒷받침하고 있습니다.

비약물 요법에서 입증된 성과는 병원 및 장기 요양 시설이 치매 돌봄 과정에서 스트레스 완화, 흥분 상태 관리, 사회적 참여 증진을 목적으로 로봇 동반자 도입을 검토하도록 촉진하고 있습니다. 일본에서 개발된 치료용 물개형 로봇 ‘PARO’는 미국에서 의료기기로 분류되고 있으며, 유럽의 국립 의료 시스템에서 진행된 프로그램 평가 결과도 이러한 접근 방식에 대한 신뢰가 높아지고 있음을 보여주고 있습니다. 이러한 증거 자료의 축적을 통해 세션 설계와 직원 교육의 일관성이 증진되었으며, 그 결과 촉각 민감도, 사실적인 반응, 안전한 소재와 같은 기능 세트에 대한 기준이 높아지고 있습니다. 치료 효과에 대한 주장이 조달 요건에 포함됨에 따라, 각 공급업체들은 문서화, 간병인을 위한 교육 자료, 수 주간에 걸친 참여 계획을 위한 통합 지원 등을 통해 차별화를 꾀하고 있습니다. 이러한 명확화를 통해 장난감 수준의 참신함과 요양 현장에서 즉시 활용 가능한 기기의 경계가 구분되면서, 로봇 반려동물 시장은 임상 및 노인 돌봄 분야로의 추가적인 확산을 위한 기반을 다지고 있습니다.

높은 총 소유 비용(기기 + 구독)

프리미엄 기기의 경우, 모든 기능을 이용하려면 지속적인 서비스 요금제가 필요할 수 있으며, 이로 인해 광고 게재 기본 가격에 비해 수년에 걸친 소유 비용이 더 높아집니다. 예를 들어, 소니의 ‘aibo’ 소유자는 개성 개발 및 컨텐츠 기능을 지원하는 클라우드 요금제를 추가할 수 있으며, 이로 인해 제품의 전체 수명 주기 동안 실질적인 지출이 증가합니다. 구독 갱신, 액세서리, 배터리 교체 주기 등도 이러한 부담에 더해지며, 그 결과 구매자들은 투명한 가격 정책과 신뢰할 수 있는 보증 지원을 중요하게 여기게 됩니다. 기기 수리비나 물류 비용도 해외 구매자들에게 영향을 미칩니다. 그들은 사후 서비스 과정에서 배송비, 관세, 지연 등의 문제에 직면할 가능성이 있습니다. 로봇 반려동물 시장에서 내구성, 모듈식 유지보수, 명확한 구독 가치를 중시하여 제품을 설계하는 기업들은 조달 및 소비자 채널 측면에서 구매에 대한 거부감이 줄어들고 있습니다. 가격 투명성, 현지 수리 네트워크, 예측 가능한 소프트웨어 로드맵은 높은 가격대의 부문에서 고객 참여에 대한 성과를 입증해야 하는 상황에서 발생하는 망설임을 줄일 수 있습니다.

부문별 분석

산업 분야와의 융합 트렌드 2025년 기준, 4족 보행 로봇은 로봇 반려동물 시장 점유율의 65.45%를 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 11.23%로 확대될 것으로 예측됩니다. 이러한 성장 추세는 이동 능력과 지형 적응 능력이 점검, 순찰 또는 치료 관련 활동을 필요로 하는 프로슈머와 기관들의 관심을 끌고 있음을 반영하며, 이로 인해 해당 카테고리의 고성능 제품군에 대한 관심이 높아지고 있습니다.

로봇 반려동물 시장은 현재 충돌을 줄이고 자율 주행에 대한 신뢰도를 높이는 더욱 강력한 센싱 스택과 모션 제어 기술의 혜택을 누리고 있습니다. 실내와 실외 모두에서 사용되는 기기는 문턱, 경사로, 변화하는 바닥면을 넘을 수 있는 플랫폼을 선호하기 때문에 더 혹독한 환경에서는 사족 보행 로봇이 제품 논의의 중심에 놓이고 있습니다. 또한, 로봇 반려동물 시장에서는 아시아의 서비스 로봇 생태계로부터 파급 효과가 나타나고 있습니다. 그곳에서는 부품 공급업체와 시스템 통합사업자들이 섀시 기반 설계의 반복 주기를 가속화하여 시장 출시까지의 시간을 단축하고 있습니다.

가성비가 향상됨에 따라, 저소음 작동, 안전한 토크 제한, 전도 시 복구 기능을 갖춘 4족 보행 로봇이 가정이나 요양 시설에서 점차 널리 보급되고 있습니다. 충분히 문서화된 API와 개발자 키트를 제공하는 벤더는 사족 보행 로봇을 학습 플랫폼으로 활용하는 교육 기관 및 연구시설로의 활용을 확대할 수 있습니다. 이를 통해 교육, 애호가 주도 프로젝트, 공공 시범 사업 등이 제품 전반에 걸친 인지도를 높여, 로봇 반려동물 시장에서 선순환이 이루어지고 있습니다.

2025년 로봇 반려동물 시장 규모에서 일반 가정이 45.90%의 점유율을 차지하고 있지만, 고령자 돌봄 및 요양 시설용 시장은 2031년까지 연평균 성장률(CAGR) 10.65%로 성장할 것으로 전망됩니다. 가족들은 계획적인 놀이, 사회적 존재감, 그리고 살아있는 반려동물을 대신할 알레르기 대책으로서 반려 로봇을 도입하고 있으며, 이는 보급형 및 중급형 기기에 안정적인 판매 기반을 제공합니다. 노인 돌봄 분야에서는 치매 돌봄과 관련해, 효과가 입증된 치료용 반려 로봇이 흥분을 가라앉히고 평정심을 되찾을 수 있도록 돕는 루틴을 지원함으로써 그 중요성이 점점 더 커지고 있습니다. 유럽의 의료 프로그램에서는 시설 환경 내에서 PARO를 활용한 로봇 치료에 대한 평가가 진행되고 있으며, 행동 관리를 위한 비약물적 치료 도구를 찾는 임상의와 관리자들의 신뢰를 높이고 있습니다. 아시아에서 진행 중인 정부 주도의 시범 사업에서는 정서적 지원 및 조기 경보 시스템에 관한 시나리오가 정의되어 있으며, 이는 노인 돌봄의 활용 사례와 잘 부합하여 운영상의 노하우 축적을 가속화하고 있습니다.

가정 내 사용 패턴에서는 거주 공간 내에서 직관적인 설정과 신뢰할 수 있는 자율성이 중요시되며, 간단한 탐색 기능과 반응이 빠른 상호작용을 겸비한 동반자형 기기가 선호되고 있습니다. 요양 시설에서는 청소가 용이한 소재, 재현성이 높은 세션 워크플로우, 일관된 작업 절차가 요구되고 있으며, 이에 따라 공급업체는 직원 교육 및 문서화된 프로토콜을 제공해야 하는 압박을 받고 있습니다. 로봇 반려동물 시장에서는 재미를 주는 일상적인 동반자를 목표로 하는 기기와 측정 가능한 치료 목표를 우선시하는 기기 사이에서 플랫폼 간 차별화가 진행되고 있습니다. 보급이 확대됨에 따라, 재택 간병 사업자가 이용자를 방문할 때 동반 로봇을 휴대하는 등 분야 간 융합 활용 사례가 등장하고 있으며, 이를 통해 다양한 환경에서의 친화성이 높아지고, 보다 광범위한 수용이 촉진되고 있습니다. 이러한 추세에 따라 가정 부문이 여전히 최대 시장으로 자리 잡고 있는 한편, 고령자 돌봄 및 요양 시설이 성장세를 주도하고 있습니다.

지역별 분석

2025년 기준으로 북미는 시장의 45.78%라는 큰 점유율을 차지했습니다. 이러한 우위는 특히 치매나 알츠하이머병 등의 증상을 앓고 있는 고령자를 위한 치료용 동반자 솔루션에 대한 수요가 증가함에 기인합니다. 미국과 캐나다는 첨단 기술의 높은 보급률과 높은 가처분 소득 수준에 힘입어 이러한 추세의 주요 견인차 역할을 하고 있습니다. 현재 시중에서 구할 수 있는 로봇 반려동물은 첨단 인공지능(AI), 머신러닝 기능, 클라우드 기반 학습 시스템, 음성 인식 및 촉각 센서 등 다중 모달 상호작용 기능을 갖추고 있습니다. 이러한 기술적 진보 덕분에 더욱 효과적이고 상호작용적인 솔루션을 개발할 수 있게 되었으며, 이는 해당 지역 시장 성장을 더욱 촉진하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 10.56%를 기록하며 성장할 것으로 전망됩니다. 중국의 시범 사업에서는 돌봄 로봇의 주요 활용 시나리오가 정의되고 도입을 위한 최소 기준이 설정되어 있으며, 이를 통해 행정 기관, 서비스 제공업체, 공급업체 간에 공통된 용어 체계가 구축되어 있습니다. 해당 지역의 제조거점과 풍부한 엔지니어링 인력은 개발 주기를 단축하고 폼 팩터의 다양성을 높여, 이를 통해 가격대에 맞는 이용 사례에 최적화된 디바이스를 제공할 수 있게 되었습니다. 일본의 임상 중심 접근 방식과 유럽의 개인정보 보호 중시 접근 방식은 특히 노인 돌봄의 맥락에서 전 세계적으로 적용 가능한 설계 청사진에 영향을 미치고 있습니다.

유럽에서는 엄격한 아동 개인정보 보호 원칙이 적용되고 있으며, 연결 기기에는 ‘프라이버시 바이 디자인’이 요구되고 있습니다. 이는 아이의 목소리나 행동을 기록하고 분석하는 동반자 기능에 영향을 미칩니다. 유럽의 병원 및 요양 시설에서의 치료 용도는 진정 효과와 사회적 이점을 입증한 검증된 기기에 대한 관심을 높이고 있으며, 이것이 시설 측의 구매를 촉진하는 근거가 되고 있습니다. 북미 시장 점유율은 가전제품의 높은 보급률과 고령자를 위한 치료 지원형 동반 기기에 대한 인식이 높아지고 있는 점을 반영하고 있습니다. 향후에는 보험 적용 방침이나 임상 프로토콜이 가정 내 보급률을 좌우할 가능성이 있으므로, 이해관계자들은 성과 데이터와 기기의 안전성에 계속해서 주목하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the robotic pet market size is projected to be USD 402.33 million in 2025, USD 438.36 million in 2026, and reach USD 682.23 million by 2031, growing at a CAGR of 9.25% from 2026 to 2031.

This report is Segmented by Product Type (Legged Quadrupeds, and More), Application (Households, and More), Price Range (Less Than USD 200, and More), Distribution Channel (Retail/Toy Chains, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Robotic Pet Market Trends and Insights

Aging Population and Loneliness Driving Companion Adoption

A sustained rise in the 65-plus population in large markets boosts institutional and at-home demand for companionship technologies that can mitigate social isolation and support routine engagement. Public discourse and national media coverage in China highlight the eldercare burden and the role of new robotic companions as part of a wider response to caregiver shortages and rising care needs. This demographic push elevates the robotic pet market beyond novelty and positions companions as a scalable, lower-cost supplement to human interaction in care settings. Policymakers and local health providers are piloting solutions that can reach residents at home and in facilities with consistent interaction patterns, which support longitudinal use. These initiatives help normalize procurement and accelerate learning curves for integration into daily routines, which sustains momentum in the robotic pet market.

Clinical Validation for Dementia and Autism Supports Therapeutic Use

Validated outcomes for non-pharmacological interventions guide hospitals and long-term care facilities to consider robotic companions for stress reduction, agitation management, and social engagement in dementia care. PARO, a therapeutic seal robot developed in Japan, has been positioned as a medical device in the United States, and program evaluations in national health systems in Europe signal growing confidence in the approach. The evidence context encourages consistent session design and staff training, which raises the standard for feature sets such as touch sensitivity, lifelike responses, and safe materials. As therapeutic claims enter procurement language, vendors differentiate with documentation, caregiver training materials, and integration support for multi-week engagement plans. The resulting clarity draws a line between toy-grade novelty and care-ready devices, and it positions the robotic pet market for deeper penetration in clinical and eldercare channels.

High Total Cost of Ownership (Device + Subscriptions)

Premium devices can require ongoing service plans to access full functionality, which raises multi-year ownership costs relative to the advertised base price. For example, Sony aibo owners can add a cloud plan that supports personality development and content features, which increases the effective spend over the lifetime of the product. Subscription renewals, accessories, and battery replacement cycles add to this burden, and this pushes buyers to favor transparent pricing and reliable warranty support. Device repair and logistics costs also impact international buyers, who may face shipping fees, customs charges, and delays during after-sales service. Companies in the robotic pet market that design for longevity, modular servicing, and clear subscription value see fewer objections in procurement and consumer channels. Pricing clarity, local repair networks, and predictable software roadmaps can mitigate hesitation in higher-value segments where return on engagement must be demonstrable.

Other drivers and restraints analyzed in the detailed report include:

- AI, Sensors, and Actuator Cost Curve Lowers the Bill of Materials

- Government Subsidies and Pilots for Care and Communication Robots

- Child Data Privacy Constraints in Connected Companions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amid Industrial Crossover Legged quadrupeds captured 65.45% of the robotic pet market share in 2025 and are projected to expand at an 11.23% CAGR through 2031. This trajectory reflects how mobility and terrain handling attract prosumers and institutions that want inspection, patrol, or therapy-adjacent engagement, which raises visibility at the higher-performance end of the category.

The robotic pet market now benefits from stronger sensing stacks and motion control that reduce collisions and improve confidence in unattended operation. Institutions with mixed indoor and outdoor use favor platforms that navigate thresholds, ramps, and variable flooring, which keeps quadrupeds at the front of product discussions for more demanding settings. The robotic pet market also sees spillovers from service-robot ecosystems in Asia, where component suppliers and integrators accelerate iteration cycles and reduce time to market for legged designs.

As price-performance improves, quadrupeds that achieve quiet operation, safe torque limits, and recoverable falls see higher acceptance in homes and care facilities. Vendors who offer well-documented APIs and developer kits can extend use into education and research labs that treat quadrupeds as learning platforms. This creates a flywheel in the robotic pet market where education, hobbyist projects, and public pilots amplify awareness across the full product spectrum.

Households accounted for 45.90% share of the robotic pet market size in 2025, while eldercare and nursing facilities are projected to grow at a 10.65% CAGR through 2031. Families adopt companions for structured play, social presence, and allergy-safe alternatives to living pets, which provides a steady volume base for entry and mid-tier devices. The eldercare segment builds momentum as validated therapeutic companions help reduce agitation and support calming routines in dementia care. European health programs have evaluated robotic therapy with PARO in institutional settings, reinforcing confidence among clinicians and administrators who want non-pharmacological tools for behavior management. Government-backed pilots in Asia define scenarios around emotional companionship and early-warning systems, which align well with eldercare use cases and accelerate operational learning.

Household usage patterns emphasize intuitive setup and reliable autonomy within living spaces, which favors companions that combine simple navigation and responsive interaction. Care facilities look for easy-to-clean materials, repeatable session workflows, and consistent behavior, which pushes vendors to include staff training and documented protocols. The robotic pet market sees platform differentiation between devices that target playful daily companionship and those that prioritize measurable therapeutic goals. As adoption grows, cross-over use emerges where home-care agencies bring companions to client visits, which raises multi-setting familiarity and supports broader acceptance. These dynamics keep households as the largest segment while eldercare and nursing facilities set the pace for growth.

Geography Analysis

North America accounted for a significant 45.78% share of the market in 2025. This dominance is attributed to the increasing demand for therapeutic companionship solutions, particularly for seniors managing conditions such as dementia and Alzheimer's. The United States and Canada are the primary contributors to this trend, driven by high adoption rates of advanced technologies and elevated levels of disposable income. The robotic pets available in the market today are equipped with advanced features, including enhanced artificial intelligence (AI), machine learning capabilities, cloud-based learning systems, and multi-modal interaction functionalities such as voice recognition and tactile sensors. These technological advancements are enabling the development of more effective and interactive solutions, further driving market growth in the region.

Asia-Pacific is projected to grow at a 10.56% CAGR through 2031. Public pilots in China specify core scenarios for care robots and set minimum deployment thresholds, which build shared vocabulary across agencies, providers, and vendors. The region's manufacturing base and engineering talent pool shorten development cycles and increase the variety of form factors, which helps match devices to use cases across price points. Japan's clinical orientation and Europe's privacy-centered approach influence design blueprints that can be applied globally, especially in eldercare contexts.

Europe applies strict child-privacy principles and expects privacy by design in connected devices, which affects companion features that log or analyze children's voices and behavior. Therapeutic use in hospitals and care facilities in Europe supports interest in validated devices that demonstrate calming and social benefits, which strengthens the case for institutional procurement. North America's share reflects strong consumer electronics adoption and a growing awareness of therapy-ready companions for older adults. Over time, coverage policies and clinical protocols could shape household penetration, which keeps stakeholders attentive to outcomes data and device safety.

- Ageless Innovation

- Consequential Robotics

- Elephant Robotics

- GROOVE X

- Hasbro / Just Play

- Innvo Labs

- Intelligent System Co.

- KEYi Technology

- Living.AI

- Panasonic

- Petoi

- Silverlit

- Sony

- Spin Master

- Tombot

- Unitree Robotics

- Vanguard Industries

- WowWee

- Yukai Engineering

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Loneliness Driving Companion Adoption

- 4.2.2 Clinical Validation for Dementia/Autism Supports Therapeutic Use

- 4.2.3 AI, Sensors, and Actuator Cost Curve Lowers the Bill of Materials

- 4.2.4 E-commerce and Crowdfunding Accelerate Go-to-Market

- 4.2.5 Government Subsidies and Pilots for Care/Communication Robots

- 4.2.6 Quadruped Price Drops Unlock Prosumer "Pet" Use Cases

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership (Device + Subscriptions)

- 4.3.2 Limited Runtime and Maintenance/Repair Friction

- 4.3.3 Vendor Longevity and Cloud-Dependency Risk

- 4.3.4 Child Data Privacy Constraints in Connected Companions

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Legged quadrupeds (dog-like)

- 5.1.2 Wheeled companions (pet-like)

- 5.1.3 Stationary plush robotic companions (e.g., seal, cushion)

- 5.2 By Application

- 5.2.1 Households

- 5.2.2 Eldercare / nursing and long-term care

- 5.2.3 Hospitals / healthcare and therapy

- 5.2.4 Education & research

- 5.2.5 Retail / experiential / visitor attractions

- 5.3 By Price Range

- 5.3.1 Less than USD 200 (toy/entry)

- 5.3.2 USD 200-USD 800 (mid-range)

- 5.3.3 USD 800-USD 2,000 (premium)

- 5.3.4 Greater than USD 2,000 (ultra-premium / prosumer)

- 5.4 By Distribution Channel

- 5.4.1 Retail/Toy Chains

- 5.4.2 Online Marketplaces

- 5.4.3 Direct-to-Consumer Online

- 5.4.4 Business-to-Business (B2B)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Ageless Innovation

- 6.3.2 Consequential Robotics

- 6.3.3 Elephant Robotics

- 6.3.4 GROOVE X

- 6.3.5 Hasbro / Just Play

- 6.3.6 Innvo Labs

- 6.3.7 Intelligent System Co.

- 6.3.8 KEYi Technology

- 6.3.9 Living.AI

- 6.3.10 Panasonic

- 6.3.11 Petoi

- 6.3.12 Silverlit

- 6.3.13 Sony

- 6.3.14 Spin Master

- 6.3.15 Tombot

- 6.3.16 Unitree Robotics

- 6.3.17 Vanguard Industries

- 6.3.18 WowWee

- 6.3.19 Yukai Engineering

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment