|

시장보고서

상품코드

2063575

레베르 선천성 흑암시 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Leber Congenital Amaurosis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

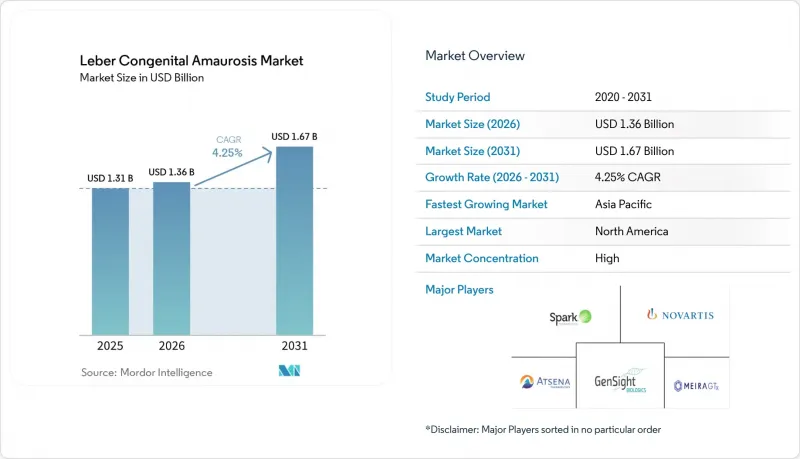

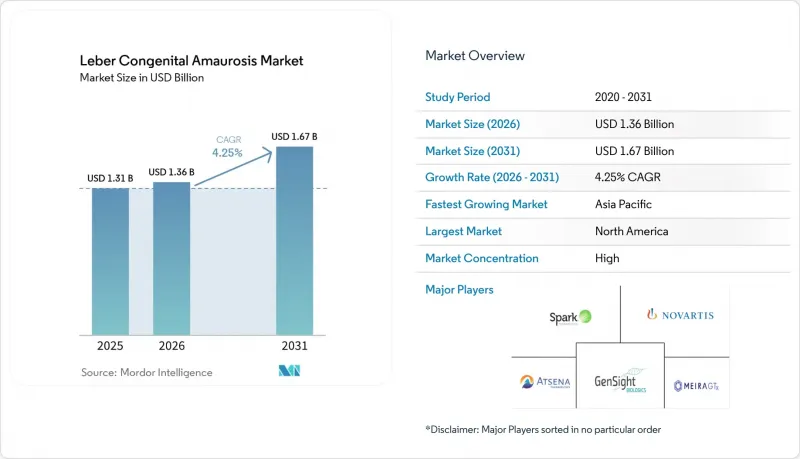

레베르 선천성 흑암시 시장 규모는 2025년에 13억 1,000만 달러로 평가되었습니다. 2026년 13억 6,000만 달러에서 2031년까지 16억 7,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 4.25%를 나타낼 전망입니다.

본 보고서는 치료법(유전자 치료, 약물 요법 등), 표적 유전자(RPE65, CEP290, GUCY2D 등), 최종 사용자(병원, 전문 안과 클리닉, 안과 연구센터 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 세분화되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 레베르 선천성 흑암시 시장 동향 및 분석

룩스타나의 급속한 시장 침투와 향후 유전자 치료제 승인

Voretigene neparvovec은 AAV를 이용한 안구 내 유전자 증강에 대한 개념 증명(PoC)을 확립했으며, 소아기 발병 실명에 대한 일회성 치료 전략을 뒷받침하는 임상적 선례로서 여전히 자리매김하고 있습니다. 이러한 채택 현황은 높은 정가와 지정된 망막하 주사 센터 네트워크 내에서 투여가 집중되는 상황에 따라 좌우되고 있습니다. 차세대 치료제가 규제상 지정에 근거한 임상시험의 방향을 모색하는 가운데, 파이프라인은 여러 LCA 유전자형에 걸쳐 다양화되고 있습니다. Opus Genetics사는 OPGx-LCA5에 대해 재생의학 첨단 치료법(Regenerative Medicine Advanced Therapy) 지정을 획득하고, 초기 기능적 개선 효과를 확증적인 결과로 전환하는 것을 목표로 하는 제3상 임상시험 설계를 수립했습니다. MeiraGTx사는 LCA4 소아 환자를 대상으로 한 AAV-AIPL1 치료에서 임상적으로 유의미한 시력 개선을 보고했으며, 해당 프로그램은 영국 규제 당국의 심사 및 미국 당국과의 협의를 위한 준비가 진행 중입니다.

신생아, 보균자 및 집단 대상 유전자 검사 패널 확대

신생아 유전체 선별 검사 프로그램과 확대된 보인자 검사는 영아기나 유아기에 발병하는 유전성 망막 질환의 진단 범위를 넓히고 있습니다. 미국의 ‘Early Check’ 시범 연구에서는 일반 신생아 코호트를 대상으로 한 유전체 시퀀싱을 통해, 실용적인 소견이 측정 가능한 비율로 도출되었으며, 임상시험 참여 및 임상적 모니터링에 도움이 되는 초희귀질환의 조기 식별이 입증되었습니다. 보인자 선별 검사 지침에서는 관련 보인자 빈도를 보이는 질환에 대해 민족성을 불문하는 보편적인 접근 방식이 권장되고 있으며, 여기에는 많은 LCA 관련 유전자가 포함됩니다. ACOG는 확대 보인자 선별 검사에 대한 폭넓은 지지를 표명했습니다. 이는 산과 진료를, 자손에게 증상이 나타나기 전에 위험에 처한 가족을 파악할 수 있는 유전학적 접근법과 연계하는 것입니다. 조기 진단과 상담을 통해 전문 기관으로의 적시 의뢰 및 유전자 치료의 조기 도입 가능성이 높아지면서, 라벨 선천성 흑내장 시장에 활기가 불어넣어지고 있습니다.

한쪽 눈당 40만 달러가 넘는 치료비가 보험사의 도입을 제한하고 있습니다.

유일하게 승인된 안과용 유전자 치료제의 높은 정가는 소아 환자에게 엄격한 증거 기준과 장기화되는 사전 승인 절차를 초래하고 있습니다. 대형 보험사들은 치료를 승인하기 전에 유전학적 확인과 생존 가능한 망막 세포의 입증을 요구하고 있으며, 많은 보험 상품에서는 과거에 주사 치료를 받은 눈에 대한 재치료를 제한하고 있습니다. 후원사는 대상 환자를 위해 본인 부담금 지원 및 자선 지원으로의 연계 경로를 마련하고 있으며, 이는 도움이 되는 조치일 뿐, 행정적 마찰을 해소하는 것은 아닙니다. 기능적 시력을 평가 지표로 삼는 성과 연계형 계약이 지불자의 위험을 줄이기 위해 추진되고 있으며, 이에 따라 실제 임상 현장에서의 지속성에 대한 관심이 높아지고 있습니다. 세포 및 유전자 치료 분야의 성과 연계형 계약을 일원화하는 연방 모델은 공적 보험 프로그램에서 주 차원의 협상 부담을 줄이는 것을 목적으로 하고 있으며, 이것이 선례가 되어 유전성 망막 질환 분야로도 확대될 가능성이 있습니다.

부문별 분석

유전자 치료는 2025년에 라벨 선천성 흑내장(LCA) 시장의 41.50%를 차지했으며, 2031년까지 연평균 4.78%의 성장률을 기록할 전망입니다. 또한, 단일 투여 치료와 엄격한 기능적 평가 지표로 특징지어지는 이 분야에서 선도적인 위치를 유지하고 있습니다. 높은 가격 책정이 단기적인 보급에 걸림돌이 되고 있지만, 중앙 집중화된 수술 네트워크, 지불자 측의 경로, 명확한 적격 기준이 적격 후보자들에 대한 꾸준한 도입을 뒷받침하는 체계를 형성하고 있습니다. 차세대 구조체가 소아 코호트에서 개선 효과를 보였으며, 특히 AIPL1 관련 질환을 앓고 있는 어린이들의 시기능이 현저히 향상되는 등, 관련 증거가 계속해서 축적되고 있습니다. OPGx-LCA5는 RMAT에 따라 개발이 진행 중이며, 임상시험 계획은 유전성 망막 질환에서 임상적으로 의미 있는 평가 지표에 대한 신뢰도가 높아지고 있음을 반영하고 있습니다. 약물 치료의 선택지는 여전히 대증 요법에 국한되어 있으며, 질환의 경과를 실질적으로 바꾸지는 못합니다. 이러한 사실은 레이블 선천성 백내장 시장에서 유전자 치료가 차지하는 핵심적인 역할을 더욱 공고히 하고 있습니다.

유전자 치료 분야의 라벨 선천성 흑내장 시장 규모는 주요 프로그램이 성숙 단계에 접어들고, 지불 기관의 승인 절차가 발전함에 따라 2031년까지 연평균 성장률(CAGR) 4.78%로 성장할 전망입니다. CRISPR-Cas9 및 기타 유전자 편집 기술을 활용한 프로그램은 특정 CEP290 돌연변이에 대해 개념 증명(PoC)을 달성했으며, 각 후원사는 구조적 바이오마커와 시력 기능의 개선을 연관 짓는 임상시험 설계를 추진하고 있습니다. 보조 기기나 의안·의족은 후원사나 임상의들이 치료가 가능한 유전자형에서 내인성 광수용체 기능의 유지 또는 회복에 주력하고 있기 때문에 수익 측면에서의 역할은 제한적입니다. 소아 관련 평가 지표에 대한 규제상의 유연성과 RMAT(규제상의 유연성에 기반한 승인)에 따른 반복적인 지침은 유의미한 결과를 평가할 수 있도록 적절히 설계된 임상시험을 지원하고 있으며, 이는 라벨 선천성 흑내장 시장에 이점을 가져다주고 있습니다.

지역별 분석

북미는 지정 치료 네트워크, 유전자 검사의 높은 보급률, 그리고 소아 유전자 치료를 위한 성숙한 임상 인프라라는 강점을 바탕으로 2025년 시점에서 45.18%의 점유율을 유지했습니다. 미국 내 소수의 시설들은 투여 관리를 효율화하고, 투여량 및 경과 관찰에 관한 지식을 통합함으로써 안전성과 데이터의 일관성에 기여하고 있습니다. 사전 승인 요건으로 일반적으로 유전자 확인이나 생존 가능한 망막 세포에 대한 증거가 요구되므로, 투여 전에 추가적인 시간과 행정 절차가 소요됩니다. 성과 기반 계약에 관한 연방 모델은 주 정부의 프로그램 부담을 줄이는 것을 목표로 하고 있으며, 향후 더 광범위한 접근성을 실현하기 위한 본보기가 될 가능성이 있습니다. 2025년, 각 후원사는 임상시험의 주요 단계로의 전환을 위해 규제 당국과 대화를 진행했으며, 이는 선천성 흑내장 치료제 시장에서 대규모 확인 시험을 향한 추진력이 지속되고 있음을 시사했습니다.

유럽은 유전성 망막 질환에 대해 시판 의약품과 임상시험용 의약품 모두를 제공하는 확립된 센터를 보유하고 있어, 두 번째 축을 이루고 있습니다. 영국의 소아 안과 병원에서는 AAV 기반 벡터를 이용한 소아 치료를 실시하고 있으며, 심사 준비를 위한 프로그램을 추진하기 위해 임상 및 학술 파트너들과의 협력을 지속하고 있습니다. 동료 심사를 거친 보고서에서는 AAV 매개형 AIPL1 벡터를 투여받은 LCA4 소아 환자에서 시기능의 현저한 개선이 확인되었으며, 소아 환자에게 유의미한 이점을 제공할 가능성이 부각되었습니다. 독일의 대규모 코호트 연구에 따르면, 최근 10년 동안의 진단율이 54.3%에 달한 것으로 나타났으며, 이는 광범위한 검사 패널과 표현형 분석의 개선이 시너지 효과를 발휘했음을 뒷받침합니다. 유럽의 참조 네트워크와 전문 학회는 공유 치료 경로 및 가상 클리닉을 조정하여, 레버 선천성 암점증 시장에서 회원국 간 일관된 기준을 유지하고 있습니다.

아시아태평양에서는 정부의 지원을 통한 생산 능력 확충과 조기 발견률을 높이는 신생아 선별 검사 프로그램의 확대로 인해, 2031년까지 연평균 4.67%의 성장이 예상됩니다. 호주의 한 시설이 지역 및 국제 스폰서를 대상으로 한 임상 및 상업적 공급을 뒷받침하는 GMP 등급 벡터 생산을 제공하고 있는 만큼, 아시아태평양의 선천성 간성 암점증 시장 규모는 연평균 성장률(CAGR) 4.67%로 확대될 것으로 전망됩니다. 호주는 조기 발견의 범위를 확대하고 유전성 질환에 대한 적시 의뢰의 기반을 마련하기 위해 전국적인 신생아 선별검사의 확충에 자금을 지원했습니다. 유럽과 미국의 주요 거점 이외 지역에서 지정 치료 인프라가 지속적으로 확대됨에 따라, 선천성 간성 암점증 시장에서 아시아태평양의 임상 개발 및 공급 물류에 대한 영향력은 커질 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the leber congenital amaurosis market size was valued at USD 1.31 billion in 2025 and is estimated to grow from USD 1.36 billion in 2026 to reach USD 1.67 billion by 2031, at a CAGR of 4.25% during the forecast period (2026-2031).

This report is Segmented by Treatment Type (Gene Therapy, Pharmacological Therapy, and More), Target Gene (RPE65, CEP290, GUCY2D, and More), End User (Hospitals, Specialized Eye Clinics, Ophthalmology Research Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

Global Leber Congenital Amaurosis Market Trends and Insights

Rapid Commercial Uptake of Luxturna and Forthcoming Gene-Therapy Approvals

Voretigene neparvovec established proof-of-concept for AAV-mediated ocular gene augmentation and remains a clinical precedent that validates one-time treatment strategies in pediatric-onset blindness. Adoption is shaped by the high list price and the concentration of administration within a network of designated subretinal injection centers. The pipeline is diversifying across multiple LCA genotypes as next-generation constructs pursue pivotal paths backed by regulatory designations. Opus Genetics advanced OPGx-LCA5 with Regenerative Medicine Advanced Therapy status, setting up a pivotal design that aims to convert earlier functional gains into confirmatory outcomes. MeiraGTx reported clinically meaningful visual acuity gains with AAV-AIPL1 in children with LCA4, and the program is being positioned for regulatory review in the United Kingdom and dialogue with U.S. authorities .

Expansion of Newborn, Carrier, and Population Genetic-Testing Panels

Genomic newborn screening programs and expanded carrier testing are broadening the diagnostic funnel for inherited retinal diseases that present in infancy or early childhood. A U.S. pilot, Early Check, showed a measurable yield of actionable findings through genome sequencing in a general newborn cohort, supporting earlier identification of ultra-rare conditions that can inform trial enrollment and clinical surveillance. Carrier screening guidance encourages universal, ethnicity-agnostic approaches for conditions with relevant carrier frequencies, which cover many LCA-associated genes. ACOG affirmed broad support for expanded carrier screening, which aligns obstetric practice with genetic approaches that can identify at-risk families before symptom onset in offspring. Earlier diagnosis and counseling increase the likelihood of timely referral to specialized centers and faster entry into gene-therapy pathways, adding momentum to the Leber congenital amaurosis market.

400k-Plus Per-Eye Therapy Costs Restricting Payer Uptake

The high list price for the only approved ocular gene therapy creates a demanding evidence bar and protracted prior authorization workflows for pediatric patients. Large payers require genetic confirmation and documentation of viable retinal cells before authorizing treatment, and many plans limit retreatment for previously injected eyes. Sponsors have implemented co-pay assistance and referral pathways to charitable support for eligible patients, which helps but does not eliminate administrative friction. Outcomes-based contracts tied to functional vision endpoints have been advanced to reduce payer risk, which shifts focus toward real-world durability. A federal model that centralizes outcomes-based contracting for cell and gene therapies aims to reduce state-level negotiation burden in public coverage programs, creating a precedent that could extend to inherited retinal diseases.

Other drivers and restraints analyzed in the detailed report include:

- Orphan-Drug, Priority Review, and Rare Pediatric Disease Incentives

- Rising Venture, Pharma, and Public Funding for Inherited Retinal Disease R&D

- Scarcity Of Accredited Sub-Retinal Surgery Centers Outside the U.S. and the EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gene therapy captured 41.50% of the Leber congenital amaurosis market share in 2025 and is on track to grow at 4.78% annually through 2031, maintaining leadership in a category shaped by single-dose treatments and rigorous functional endpoints. The premium price point weighs on near-term uptake, but concentrated surgical networks, payer pathways, and clear eligibility criteria create a framework that supports steady adoption in qualified candidates. Evidence continues to accumulate as next-generation constructs demonstrate improvements in pediatric cohorts, including notable gains in visual function for children with AIPL1-associated disease. OPGx-LCA5 progressed under RMAT, and pivotal planning reflects growing confidence in clinically meaningful endpoints for inherited retinal diseases. Pharmacologic options remain limited to supportive care and do not materially change disease trajectory, which reinforces gene therapy's central role in the Leber congenital amaurosis market.

The Leber congenital amaurosis market size for gene therapy is set to expand at a 4.78% CAGR through 2031 as pivotal programs mature and payer pathways evolve. Programs that deploy CRISPR-Cas9 and other editing modalities showed proof-of-concept in defined CEP290 mutations, and sponsors are advancing trial designs that link structural biomarkers with functional gains in vision. Supportive devices and prosthetics have a minor revenue role as sponsors and clinicians focus on preserving or restoring endogenous photoreceptor function in amenable genotypes. Regulatory flexibility around pediatric endpoints and iterative guidance under RMAT support well-designed trials that can read out on meaningful outcomes, which benefits the Leber congenital amaurosis market.

Geography Analysis

North America retained 45.18% in 2025 on the strength of designated treatment networks, high genetic testing penetration, and mature clinical infrastructure for pediatric gene therapy. The limited set of U.S. centers streamlines administration and consolidates experience in dosing and follow-up, which contributes to safety and data consistency. Prior authorization requirements commonly request genetic confirmation and evidence of viable retinal cells, which adds time and administrative steps before dosing. A federal model for outcomes-based contracting seeks to reduce the burden on state programs, which could provide a template for broader access over time. Sponsors engaged in regulatory dialogue for pivotal progression during 2025, signaling continued momentum toward larger confirmatory studies in the Leber congenital amaurosis market.

Europe is the second pillar with established centers that deliver both commercial and investigational therapies for inherited retinal diseases. U.K. pediatric eye hospitals have treated children with AAV-based constructs and continue to collaborate across clinical and academic partners to advance programs toward review. A peer-reviewed report documented significant visual function gains in LCA4 children who received an AAV-mediated AIPL1 construct, highlighting the potential for meaningful pediatric benefit. A large German cohort showed that the diagnostic yield reached 54.3% in the most recent decade, which underscores the synergy between broader panels and improved phenotyping. European reference networks and professional societies coordinate shared care pathways and virtual clinics that support consistent standards across member countries in the Leber congenital amaurosis market.

Asia-Pacific is expected to grow at 4.67% through 2031 with government-backed manufacturing capacity and expanding newborn screening programs that raise early identification. The Leber congenital amaurosis market size in Asia-Pacific is forecast to expand at a 4.67% CAGR as facilities in Australia provide GMP-grade vector production that supports clinical and commercial supply for regional and international sponsors. Australia funded national newborn screening enhancements that broaden the scope of early detection and lay the groundwork for timely referral in inherited disorders. As designated treatment infrastructure outside Western hubs continues to scale, APAC's influence on clinical development and supply logistics is poised to rise within the Leber congenital amaurosis market.

- 4D Molecular Therapeutics, Inc.

- Abbvie

- Adverum Biotechnologies, Inc.

- Aerie Pharmaceuticals, Inc.

- Astellas Pharma

- Atsena Therapeutics, Inc.

- Beacon Therapeutics plc

- Biogen

- Editas Medicine, Inc.

- Editas Medicine Allergan Collaboration

- GenSight Biologics S.A.

- Horama S.A.

- MeiraGTx Holdings plc

- Novartis

- Ocugen, Inc.

- Pfizer

- ProQR Therapeutics N.V.

- REGENXBIO

- Santen Pharmaceuticals

- Spark Therapeutics, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid commercial uptake of Luxturna and forthcoming gene-therapy approvals

- 4.2.2 Expansion of newborn, carrier and population genetic-testing panels

- 4.2.3 Orphan-drug, Priority Review and Rare Pediatric Disease incentives

- 4.2.4 Rising venture, pharma and public funding for inherited retinal disease R&D

- 4.2.5 Asia-Pacific viral-vector manufacturing hubs delivering 20-30 % lower COGS

- 4.2.6 AI-guided adaptive-optics retinal imaging platforms

- 4.3 Market Restraints

- 4.3.1 $400k-Plus Per-Eye Therapy Costs Restricting Payer Uptake

- 4.3.2 Scarcity Of Accredited Sub-Retinal Surgery Centers Outside U.S./EU

- 4.3.3 Global Viral-Vector Fill-Finish Capacity Bottlenecks Delaying Launches

- 4.3.4 Highly Fragmented Mutation Landscape Diluting ROI For Long-Tail Gene Targets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

5 Market Size & Growth Forecasts

- 5.1 By Treatment Type

- 5.1.1 Gene Therapy

- 5.1.2 Pharmacological Therapy

- 5.1.3 Retinal Prosthesis

- 5.1.4 Assistive Devices

- 5.1.5 Other Supportive Treatments

- 5.2 By Target Gene

- 5.2.1 RPE65

- 5.2.2 CEP290

- 5.2.3 GUCY2D

- 5.2.4 AIPL1

- 5.2.5 CRB1

- 5.2.6 RPGRIP1

- 5.2.7 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialized Eye Clinics

- 5.3.3 Ophthalmology Research Centers

- 5.3.4 Home Care Settings

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 4D Molecular Therapeutics, Inc.

- 6.3.2 AbbVie Inc.

- 6.3.3 Adverum Biotechnologies, Inc.

- 6.3.4 Aerie Pharmaceuticals, Inc.

- 6.3.5 Astellas Pharma Inc.

- 6.3.6 Atsena Therapeutics, Inc.

- 6.3.7 Beacon Therapeutics plc

- 6.3.8 Biogen Inc.

- 6.3.9 Editas Medicine, Inc.

- 6.3.10 Editas Medicine Allergan Collaboration

- 6.3.11 GenSight Biologics S.A.

- 6.3.12 Horama S.A.

- 6.3.13 MeiraGTx Holdings plc

- 6.3.14 Novartis AG

- 6.3.15 Ocugen, Inc.

- 6.3.16 Pfizer Inc.

- 6.3.17 ProQR Therapeutics N.V.

- 6.3.18 REGENXBIO Inc.

- 6.3.19 Santen Pharmaceutical Co., Ltd.

- 6.3.20 Spark Therapeutics, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment