|

시장보고서

상품코드

2063632

사람의 고양이 알레르기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cat Allergy In Humans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

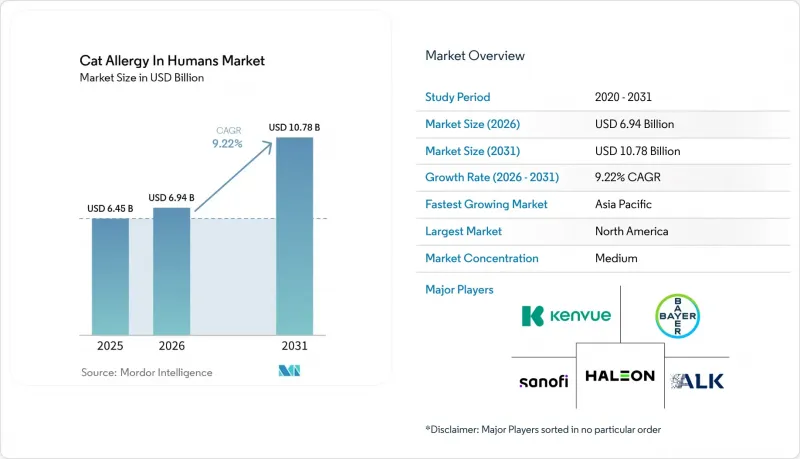

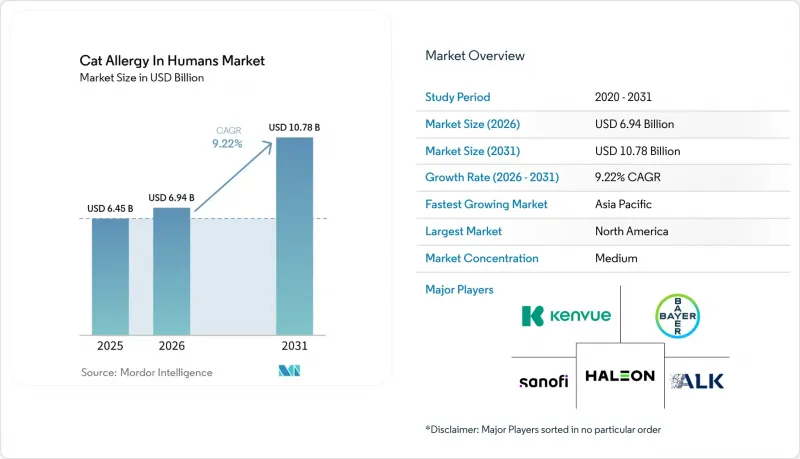

Mordor Intelligence에 의하면, 사람의 고양이 알레르기 시장 규모는 2025년 64억 5,000만 달러로 평가되었습니다. 2026년 69억 4,000만 달러에서 2031년까지 107억 8,000만 달러로 확대되어 2026-2031년 CAGR은 9.22%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(항히스타민제, 코르티코스테로이드, 알레르겐 차단 단일클론 항체, 면역요법, 기타), 투여 경로(경구, 비강 내, 안과용, 피하, 기타), 처방 현황(일반의약품, 처방약), 유통 채널(병원, 소매, 온라인 약국), 지역(북미, 유럽, 기타)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계 사람의 고양이 알레르기 시장 동향 및 인사이트

알레르기성 비염/천식 환자에서 고양이 알레르겐의 유병률 및 감작 증가

대도시권 코호트를 대상으로 한 임상 연구에 따르면, 실내에서의 장기적인 노출과 좁은 주거 공간에서 사람과 반려동물이 함께 생활하는 생활 방식의 경향과 맞물려, 고양이 비듬에 대한 감작이 꾸준히 증가하고 있는 것으로 나타났습니다. 중국 중부 지역에서는 지난 6년 동안 고양이 알레르기를 가진 알레르기성 비염 환자의 비율이 증가하고 있으며, 단기적인 증상 완화를 넘어 지속적인 관리가 가능한 치료 방법에 대한 명확한 필요성이 부각되고 있습니다. 소아 및 청소년 코호트에서는 고양이 배설물에 대한 감작이 진드기에 비해 늦게 정점에 도달하는 것으로 나타났으며, 이는 조기 선천적 감수성보다는 누적된 환경 노출과 행동의 변화가 감작의 시기와 중증도를 결정짓고 있음을 시사합니다.

이러한 경향은 면역요법이나 특정 알레르겐 프로파일에 맞춘 치료를 지원하는 ‘알레르겐 성분에 기반한 상담’ 등의 지원 조치의 대상 환자층을 확대합니다. 또한, 환자들은 종종 시판되는 항히스타민제로 치료를 시작하고, 자가 관리를 해도 증상이 지속될 경우 처방약이나 면역요법으로 단계적으로 전환하기 때문에 여러 접점을 통해 수요가 유지됩니다. 그 결과, 사람의 고양이 알레르기 시장은 대증 요법과 질환 수정 요법이라는 두 가지 치료 영역 모두에서 환자 수가 지속적으로 증가하고 있으며, 이는 지속적인 성장 전망을 더욱 공고히 하고 있습니다.

반려묘의 사육 수가 증가하고 실내에서 함께 생활하는 경우가 늘어나면서, 노출 정도가 높아지고 있습니다.

2024년, 미국에서 반려묘로 기르는 고양이의 수는 급격히 증가하여, 고양이를 키우는 가구 수는 4,900만 가구에 달했습니다. 이로 인해 실내에서 Fel d 1에 직접적이고 빈번하게 노출되는 사람들의 수도 증가하고 있습니다. 영국에서도 고양이 사육 수는 여전히 많은 편으로, 가구의 4분의 1이 고양이를 키우고 있는 것으로 보고되어, 생활 공간에 알레르겐이 장기간 잔류한다는 시장 전반에 걸친 추세가 입증되었습니다. 이러한 노출 동향은 증상을 신속하게 완화시켜 주는 1차 선택 OTC(일반의약품)에 대한 수요를 높이는 한편, 경구용 항히스타민제만으로는 호전되지 않는 지속적인 증상에 대해서는 의사의 지도에 따른 치료법에 대한 수요도 창출하고 있습니다. 가정 내 알레르겐의 지속성은 노출량이 많은 기간 동안 전반적인 증상 부담을 줄이기 위해 약물 요법과 병행할 수 있는 환경 대책 및 발생원 저감 전략에 대한 관심도 높이고 있습니다. 의료진은 이러한 상황을 고려하여 약물 요법, 적응증이 있는 경우 면역 요법, 그리고 환자의 선호도와 위험 감수 수준에 맞춘 일상적인 완화 조치를 결합한 통합적인 계획을 권장하고 있습니다. 이 생태계는 연령대나 증상의 중증도에 관계없이 폭넓은 계층을 아우르며, 균형 잡히고 빠르게 성장하는 사람의 고양이 알레르기 시장을 뒷받침하고 있습니다.

고양이용 SLIT 정제는 FDA 승인을 받지 않았으며, SLIT 점안액도 미국에서는 FDA 승인을 받지 않았습니다.

설하정은 벼과 식물, 쇼트래그위드 및 진드기에 대해 FDA 승인을 받았으나, 고양이 배설물에 대한 정제는 허가를 받지 못했으며, 고양이용 액제 역시 미국에서는 적응증 외 사용 상태입니다. 이로 인해 광범위한 보험 적용이 제한됨에 따라, 자택에서 투여를 희망하는 많은 환자들은 오프라벨 사용을 허용하는 일부 의료기관에서 처방받는 피하 면역요법(SCIT), 본인 부담이 되는 설하액제를 선택할 수밖에 없는 상황에 내몰리고 있습니다. 유럽에서는 다른 알레르겐에 대한 소아용 정제 확대 과정의 타당성이 입증되었습니다. 2024년 소아용 ACARIZAX의 승인 사례에서 볼 수 있듯이, 비록 고양이용 정제가 아직 시판되지 않았더라도, 제약사가 필요한 자료와 임상시험에 투자한다면 정제 플랫폼은 발전할 수 있음이 입증되었습니다. 후원사가 고양이 전용 알약 프로그램을 완료할 때까지는 이러한 격차로 인해 알약이 이미 확립된 알레르기 유발 물질에 비해 편의성을 중시하는 미국 시장에서의 도입이 계속해서 지연될 것입니다. 이는 유통 경로의 동향에 실질적인 영향을 미치고 있습니다. 왜냐하면, 클리닉 중심의 피하 면역요법(SCIT)이 여전히 보험 적용을 받기 가장 쉬운 방법인 반면, 각국 당국이 이미 고양이 알레르기에 대한 설하 면역요법(SLIT)을 표준 치료법으로 인정하고 있는 지역에서는 설하 용액이 더 쉽게 보급되기 때문입니다. 그 결과, 환자들의 재택 치료 옵션에 대한 관심이 높아지고 있음에도 불구하고, 미국의 고양이 알레르기 치료 시장은 여전히 병원 중심 모델에 의존하고 있습니다.

부문별 분석

항히스타민제는 2025년 판매량의 38.43%를 차지했으며, 증상을 신속하게 완화할 수 있고 의사의 진료를 받지 않고도 소매점에서 쉽게 구할 수 있기 때문에 많은 환자에게 여전히 기본적인 초기 치료법으로 자리 잡고 있습니다. 오랜 기간에 걸친 임상 실적과 다양한 경구 제형은 경증에서 중등도 증례에서 복약 순응도를 높여주며, 예측 가능한 투여를 중시하는 1차 선택 약물 사용자들 사이에서 폭넓은 보급을 유지하고 있습니다. 비강용 코르티코스테로이드는 경구용 항히스타민제로는 효과가 충분하지 않은 경우의 지속적인 코막힘이나 비강 염증을 치료하며, 더 강력한 국소 항염증 작용이 필요한 환자를 위한 의사의 치료 선택지를 확대되고 있습니다.

알레르겐 차단 단일클론 항체는 개발 기업이 확인 시험을 진행하고 시판에 대비한 보험 적용 전략을 수립함에 따라, 2031년까지 연평균 성장률(CAGR) 11.87%를 나타낼 것으로 전망됩니다. 이 치료법은 매일 약을 복용하거나 매달 병원을 방문할 필요 없이 신속한 증상 완화를 원하는 환자에게 가장 적합하며, 반면 면역요법은 의사의 감독 하에 수년에 걸친 질병 경과 조절 치료 과정을 원하는 환자에게 여전히 선택지로 남아 있습니다. 고양이 체내의 Fel d 1을 중화시키는 원천 관리형 영양 요법(3주 차까지 털 표면의 활성 알레르겐을 유의미하게 감소시킨 것으로 입증된 IgY 기반 식이 요법을 포함)은 반려동물을 계속 키우고자 하는 가정에서 약물 요법이나 면역 요법을 보완할 수 있습니다. 소비자 대상 소매, 처방전 채널, 전문 생물학적 제제에 걸쳐 있는 이 제품 포트폴리오는 사람의 고양이 알레르기 시장이 증거 기반과 적응증의 확대에 따라 선택의 폭을 넓혀가며, 다양한 환자의 요구에 부응할 수 있도록 합니다.

경구용 제제는 병원에 방문하지 않고도 사용할 수 있는 2세대 항히스타민제의 장점 덕분에 2025년에는 45.34%의 시장 점유율을 차지했습니다. 경구용 정제나 액제는 즉각적인 효과와 예측 가능성에 대한 소비자의 기대에 부응하며, 계절에 따른 사용이나 경미한 증상에 대한 일상적인 유지 요법을 뒷받침하고 있습니다. 비강 내 코르티코스테로이드는 경구제로는 완전히 해소하기 어려운 경우가 많은 코의 염증이나 코막힘을 억제하는 데 있어 독자적인 역할을 수행하고 있으며, 상기도 증상이 주된 경우에는 비강 내 투여가 여전히 매력적인 선택지로 남아 있습니다.

사람의 고양이 알레르기 치료 시장에서 피하 투여 방식 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 9.87%로 확대될 것으로 전망됩니다. 이는 의료기관이 피하 면역요법(SCIT)의 경로를 지속적으로 표준화하고 있으며, 바이오의약품이 내원 횟수를 줄이면서도 지속적인 증상 완화를 원하는 환자층을 대상으로 하고 있기 때문입니다. 1회 피하 투여로 3개월간 효과가 지속되는 바이오의약품 프로그램은 확인 시험에서 유효성과 안전성이 일관되게 유지된다면, 편의성을 중시하는 환자들에게 주사 투여 경로의 유효성을 한층 더 입증해 줄 것입니다.

지역별 분석

북미는 2025년 사람의 고양이 알레르기 시장에서 42.44%의 점유율을 차지했습니다. 이는 긴밀한 알레르기 전문의 네트워크, 확립된 SCIT(피하 면역요법) 절차, 그리고 환자 선정 및 투여량 결정을 개선하는 성분별 검사의 일관된 활용에 힘입은 결과입니다. 2024년에는 고양이를 키우는 가구 수가 23% 급증하여 미국에서 4,900만 가구에 달했습니다. 이로 인해 알레르기 반응을 보인 사람들의 노출이 증가했고, 일반의약품 및 처방약에 의한 치료와 전문 의료 서비스 전반에 대한 수요가 높아졌습니다. 지역별 혁신의 밀도 또한 긍정적인 요인으로 작용하고 있습니다. 이는 Fel d 1을 억제하는 단일클론 항체가 후기 임상시험에서 계속해서 양호한 결과를 보이고 있으며, 개발사가 2026년 승인 신청을 목표로 한 임상시험 실시를 확약했기 때문입니다.

유럽에서는 면역요법을 지원하는 각국의 처방집과, 다른 알레르겐에 대한 오랜 기간에 걸친 설하 투여의 역사를 바탕으로 형성된 탄탄한 시장 기반이 유지되고 있습니다. 이는 고양이용 정제의 승인 사례가 없는 상황에서도 마찬가지입니다. 최근 진드기 알레르겐에 대한 소아용 정제가 승인된 것은 유효성과 안전성이 명확해지면 후원사 주도의 임상 프로그램이 성공적으로 확대될 수 있음을 보여주는 것으로, 향후 고양이 특이적 신청이 이루어질 경우의 모범 사례가 될 것입니다. 스페인에서 수집된 실제 임상 데이터는 일상 진료에서 피하 면역요법(SCIT)의 유효성을 입증하고 있으며, 적절한 환자를 대상으로 한 장기 치료의 일환으로 탈색·중합 추출물에 대한 알레르기 전문의들의 신뢰를 뒷받침하고 있습니다.

아시아태평양은 도시화, 반려동물 사육률 상승, 진단법 및 면역요법에 대한 접근성 확대가 맞물려 치료 시장이 확대되고 있으며, 연평균 성장률(CAGR) 11.95%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 중국에서는 최근 임상 코호트 연구를 통해 고양이 비듬에 대한 감작률이 높아지고 있는 것으로 나타났으며, 이는 치료법의 필요성을 뒷받침할 뿐만 아니라, 처방자가 수년에 걸친 치료 계획을 수립할 때 성분 분석 검사의 역할을 강화하는 계기가 됩니다. 중국에서는 다른 호흡기 알레르겐에 대한 표준화된 설하 투여 제품에 관한 과거의 경험도, 후원사가 프로그램 및 임상시험에 주력한다면 향후 고양이 특이적 치료 경로의 토대가 될 것입니다. 도시 지역에서 검사와 치료가 확대됨에 따라, 체계화된 성분 정보를 바탕으로 한 치료 서비스를 찾는 환자 수가 증가할 것으로 예상되며, 이는 사람의 고양이 알레르기 시장의 성장세를 더욱 공고히할 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the cat allergy in humans market size is projected to expand from USD 6.45 billion in 2025 and USD 6.94 billion in 2026 to USD 10.78 billion by 2031, registering a CAGR of 9.22% between 2026 to 2031.

This report is Segmented by Product Type (Antihistamines, Corticosteroids, Allergen-Blocking Monoclonal Antibodies, Immunotherapy, Others), Route of Administration (Oral, Intranasal, Ophthalmic, Subcutaneous, Others), Prescription Status (OTC, Rx), Distribution Channel (Hospital, Retail, Online Pharmacy), and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Cat Allergy In Humans Market Trends and Insights

Rising Prevalence And Sensitization To Cat Allergens Among Allergic Rhinitis/Asthma Patients

Clinical studies in large urban cohorts document a steady rise in cat-dander sensitization that coincides with extended indoor exposure and lifestyle patterns that keep people and pets together in smaller living spaces. In central China, the share of allergic rhinitis patients with cat sensitization climbed across a six-year period, highlighting a clear need for therapy pathways that can offer durable control beyond short-term symptomatic relief. Pediatric and adolescent cohorts show a delayed peak for cat dander compared with dust mite, which suggests that cumulative environmental exposure and behavioral shifts, rather than early innate susceptibility, shape timing and severity.

These patterns broaden the base of candidates for immunotherapy and for supportive measures such as component-informed counseling that help align treatment with the specific allergen profile. They also sustain demand across multiple access points because patients often begin with OTC antihistamines and later escalate to prescription therapies or immunotherapy when symptoms persist despite self-management. As a result, the cat allergy in humans market continues to add patients across both symptomatic and disease-modifying care streams, reinforcing a durable growth outlook

Growing Pet Cat Ownership And Indoor Cohabitation Increasing Exposure Intensity

Pet-cat ownership in the United States rose quickly in 2024, lifting cat-owning households to 49 million and increasing the number of people who experience direct and frequent exposure to Fel d 1 indoors. The United Kingdom maintained a large cat population as well, and a quarter of households reported owning cats, confirming cross-market patterns that keep the allergen present in living spaces for long periods. These exposure trends feed demand for front-line OTC options that provide quick relief, followed by physician-directed regimens for persistent symptoms that fail to resolve on oral antihistamines alone. Allergen persistence within homes also supports interest in environmental and source-reduction strategies that can be paired with drug therapy to lower overall symptom burden during high-exposure periods. Providers apply this context to recommend integrated plans combining medication, immunotherapy when indicated, and everyday mitigation steps that match patient preference and risk tolerance. This ecosystem supports a balanced and growing cat allergy in humans market that serves a broad population across age groups and severity profiles.

No FDA-Approved SLIT Tablets For Cat, And SLIT Drops Not FDA-Approved In The U.S.

Sublingual tablets are FDA approved for grasses, short ragweed, and dust mite, but no cat dander tablet is licensed and liquid drops for cat remain off-label in the United States. This limits broad reimbursement and pushes many patients who prefer home administration toward SCIT or cash-pay sublingual drops prescribed in select practices that accept off-label use. Europe has demonstrated the process integrity for pediatric tablet expansion in other allergens, as seen in the 2024 approval of ACARIZAX for children, which shows that tablet platforms can progress when sponsors invest in the necessary dossiers and trials even if cat tablets are not yet available. Until a sponsor completes a cat-specific tablet program, the gap will continue to slow convenience-driven adoption in the United States relative to tablet-established allergens. This has a practical effect on channel dynamics because clinic-centered SCIT remains the most reimbursable pathway while sublingual drops scale more readily where national authorities already accept cat SLIT as standard of care. As a result, the cat allergy in humans market in the United States continues to rely on clinic-based models despite growing patient interest in home-use options.

Other drivers and restraints analyzed in the detailed report include:

- Demonstrated Disease-Modifying Benefit And Physician Confidence In SCIT For Animal Dander

- Emerging biologics enlarging addressable pool

- SCIT Safety/Logistics Burden Limits Uptake And Adherence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Antihistamines accounted for 38.43% of 2025 volume and remain the default starting point for many patients because they offer rapid symptom relief and easy access through retail aisles without a physician visit. Their longevity in practice and multiple oral formats support adherence for mild to moderate cases and sustain broad reach among first-line users who value predictable dosing. Intranasal corticosteroids address persistent congestion and nasal inflammation when oral antihistamines underperform, expanding physician-directed choices for patients who require stronger local anti-inflammatory control.

Allergen-blocking monoclonal antibodies are projected to expand at an 11.87% CAGR through 2031 as sponsors progress confirmatory trials and define coverage strategies for launch. Their fit is clearest for patients who want fast relief without daily pills or clinic visits every month, while immunotherapy remains the choice for those seeking a disease-modifying course of care over several years with physician oversight. Source-control nutrition that neutralizes Fel d 1 at the cat, including IgY-based diets that showed meaningful reductions in active allergen on hair by week three, can complement both drug therapy and immunotherapy inside homes that prefer to retain pets. This product mix, spanning consumer retail, prescription channels, and specialty biologics, helps the cat allergy in humans market serve heterogenous patient needs while keeping options open as evidence and labeling evolve.

Oral formulations held 45.34% share in 2025 on the strength of second-generation antihistamines that people can use without clinic visits. Oral tablets and liquids meet consumer expectations for immediacy and predictability, supporting seasonal use and daily maintenance for milder phenotypes. Intranasal corticosteroids occupy a distinct role because they suppress nasal inflammation and congestion that oral agents often fail to resolve completely, which keeps the nasal route attractive when upper-airway symptoms dominate.

The cat allergy in humans market size for subcutaneous administration is projected to expand at a 9.87% CAGR over 2026-2031 as clinics continue to standardize SCIT pathways and as biologics target cohorts that want fewer visits with sustained relief. Biologic programs that offer three-month durability after a single subcutaneous dose may further validate the injection route for convenience-focused patients if efficacy and safety remain consistent in confirmatory studies.

Geography Analysis

North America held 42.44% in 2025 in the cat allergy in humans market, supported by a dense allergist network, established SCIT pathways, and consistent use of component-informed testing that improves patient selection and dosing decisions. Cat ownership surged by 23% in 2024 to reach 49 million U.S. households, which increased exposure among sensitized individuals and lifted demand across OTC and prescription therapies as well as specialty services. Regional innovation density adds momentum because Fel d 1-blocking monoclonal antibodies continue to generate positive results in late-stage studies, and sponsors have committed to registration-enabling trials in 2026.

Europe maintains a substantial footprint shaped by national formularies that support immunotherapy and by a long history of sublingual use across other allergens, even as there is no approved cat tablet. Recent pediatric tablet approvals in dust mite show that sponsor-led clinical programs can scale successfully once efficacy and safety are clear, which offers a template for future cat-specific filings if pursued. Real-world evidence from Spain confirms SCIT effectiveness in routine practice and supports allergists' confidence in depigmented, polymerized extracts as part of long-term care for appropriate patients.

Asia-Pacific is the fastest-growing region with an 11.95% forecast CAGR as urbanization, rising pet ownership, and increasing access to diagnostics and immunotherapy combine to expand treatment. In China, clinical cohorts show higher cat-dander sensitization in recent years, which supports the need for therapies and reinforces the role for component-resolved testing when prescribers consider multi-year plans. China's prior experience with standardized sublingual products for other respiratory allergens also provides a platform for future cat-specific pathways if sponsors dedicate programs and trials. As testing and therapy broaden across urban centers, patient flow into structured, component-informed care is expected to accelerate and reinforce the cat allergy in humans market trajectory.

- Alcon

- ALK-Abello A/S

- Allergy Laboratories, Inc.

- Amgen

- AstraZeneca

- Bausch + Lomb

- Bayer

- Church & Dwight

- Glenmark Pharmaceuticals

- Haleon

- Hikma Pharmaceuticals

- HollisterStier Allergy

- Kenvue

- Perrigo

- Regeneron Pharmaceuticals

- Sanofi

- Stallergenes Greer

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence and Sensitization to Cat Allergens Among Allergic Rhinitis/Asthma Patients

- 4.2.2 Growing Pet Cat Ownership and Indoor Cohabitation Increasing Exposure Intensity

- 4.2.3 Demonstrated Disease-Modifying Benefit and Physician Confidence in SCIT for Animal Dander

- 4.2.4 Expansion of Treatment Options Across OTC, Rx, AIT and Emerging Biologics

- 4.2.5 Allergen-Exposure Reduction Solutions Broadening Adjunct Management

- 4.2.6 Emerging Biologics Enlarging Addressable Pool

- 4.3 Market Restraints

- 4.3.1 No FDA-Approved SLIT Tablets for Cat

- 4.3.2 SCIT Safety/Logistics Burden (In-Clinic Dosing, Anaphylaxis Risk) Limits Uptake

- 4.3.3 Multi-Year Adherence Challenges and Discontinuations in AIT Reduce Outcomes

- 4.3.4 Extract Variability and Product Standardization Differences Affect Consistency

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Antihistamines

- 5.1.2 Corticosteroids

- 5.1.3 Allergen-blocking Monoclonal Antibodies

- 5.1.4 Immunotherapy

- 5.1.5 Others (Nasal Decongestant, etc)

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Intranasal

- 5.2.3 Ophthalmic

- 5.2.4 Subcutaneous

- 5.2.5 Others

- 5.3 By Prescription Status

- 5.3.1 Over-the-Counter (OTC)

- 5.3.2 Prescription (Rx)

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacy

- 5.4.2 Retail Pharmacy

- 5.4.3 Online Pharmacy

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Alcon

- 6.3.2 ALK-Abello A/S

- 6.3.3 Allergy Laboratories, Inc.

- 6.3.4 Amgen

- 6.3.5 AstraZeneca

- 6.3.6 Bausch + Lomb

- 6.3.7 Bayer AG

- 6.3.8 Church & Dwight

- 6.3.9 Glenmark

- 6.3.10 Haleon

- 6.3.11 Hikma Pharmaceuticals PLC

- 6.3.12 HollisterStier Allergy

- 6.3.13 Kenvue

- 6.3.14 Perrigo

- 6.3.15 Regeneron Pharmaceuticals Inc.

- 6.3.16 Sanofi

- 6.3.17 Stallergenes Greer

- 6.3.18 Teva Pharmaceutical Industries Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment