|

시장보고서

상품코드

2063601

제트 네뷸라이저 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Jet Nebulizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

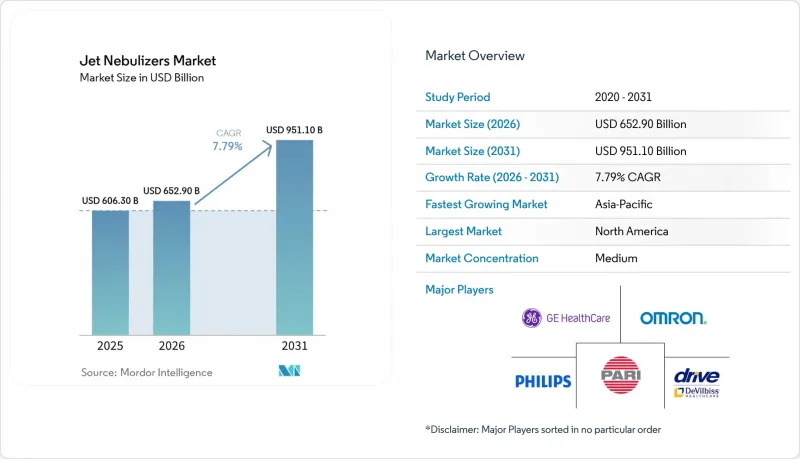

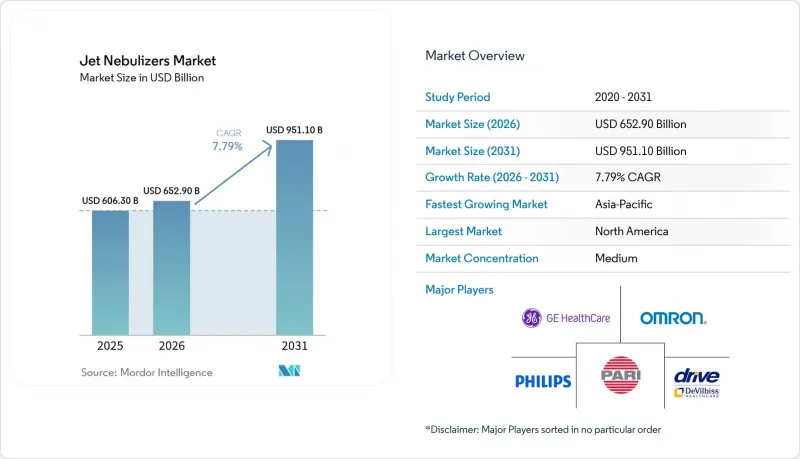

Mordor Intelligence에 의하면, 제트 네뷸라이저 시장 규모는 2025년에 6,063억 달러로 평가되었고 2026년 6,529억 달러에서 2031년까지 9,511억 달러에 이를 것으로 추정되고 있어 예측 기간(2026-2031년) CAGR은 7.79%를 나타낼 전망입니다.

본 보고서는 제트 네뷸라이저의 유형(호흡 구동식, 호흡 보조식, 통기식/연속 출력식), 용도(천식, COPD, 낭포성 섬유증, 기타 호흡기 질환), 최종 사용자(병원 및 클리닉, 재택치료, 외래·응급·응급의료센터), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 제트 네뷸라이저 시장 동향 및 인사이트

전 세계적인 COPD 및 천식 위기가 흡입 요법 수요의 급증을 부추기고 있습니다.

세계적으로 5억 명 이상이 만성 폐쇄성 폐질환(COPD)이나 천식을 앓고 있으며, 매년 400만 명이 사망하고 있습니다. COPD 관련 사망자의 약 60%는 아시아·태평양 지역에 집중되어 있으며, 중국에서는 9,990만 명, 인도에서는 5,530만 명의 환자가 보고되었습니다. 도시 지역의 대기 오염은 이러한 질환을 악화시키고 있으며, 특히 베이징, 델리, 자카르타와 같은 대도시에서는 PM2.5 농도가 권장 기준치를 초과하고 있습니다. 2004년부터 2023년까지의 영국 등록 데이터에 따르면, 진단을 받은 환자 수는 1,000만 명을 넘어섰으며, 부유층이 많은 지역에서는 발병률이 안정적인 반면, 도시 지역의 저소득층 지역에서는 증가 추세를 보이고 있습니다. 이러한 막대한 역학적 부담으로 인해, 특히 정량 분무식 흡입기 사용에 어려움이 있는 분이나 인지 기능 장애가 있는 분들을 중심으로 제트 네뷸라이저 시장에 대한 수요는 안정적으로 유지될 것으로 전망됩니다.

재택 호흡 관리와 DME 보험 적용이 압축기식 네뷸라이저의 보급을 촉진하고 있습니다.

미국 메디케어·메디케이드 서비스 센터(CMS)는 2025년 DMEPOS 요금표에서 압축기식 네뷸라이저에 대한 사전 승인 절차를 간소화하여 공급업체와 환자 모두에게 혜택을 제공했습니다. 재택의료 선불 제도(HHPS)의 기기 기능에 대한 연례 재조사 결과, 특히 지방 지역에서는 배터리 구동형 메쉬 유닛보다 벽면 콘센트 전원 공급 방식의 내구성이 뛰어난 압축기가 더 선호되는 것으로 나타났습니다. 중국에서는 ‘건강 중국 2030’ 이니셔티브의 일환으로, 2024년에 호흡기 기기의 보험 적용 범위가 확대되었으며, 재입원을 줄이기 위한 재택 치료가 장려되고 있습니다. 인도의 국가 보건 미션에서는 약물 복용 순응도 향상과 응급실 방문 감소를 목적으로, 보조금을 지원받아 제트 네뷸라이저를 지역에 시범적으로 배포하고 있습니다. 압축기식 제트 네뷸라이저의 가격이 30-100달러인 반면, 메쉬식 대체 제품의 가격은 400달러부터 시작하므로, 압축기식의 가격 면에서의 우위는 분명합니다.

임상 현장에서의 감염 관리 관련 우려 사항 및 에어로졸화 위험

2024년 합의 성명에서는 연속 출력 제트 네뷸라이저가 환기가 불충분한 실내에서 SARS-CoV-2를 포함한 병원체를 최대 30분 동안 운반할 수 있는 에어로졸 기둥을 생성할 수 있다는 점이 강조되었습니다. 이에 대응하여 병원에서는 일회용 회로에 대한 투자와 음압실 도입이 진행되고 있습니다. 이러한 조치들은 안전성을 높이는 한편, 1회당 치료 비용을 증가시켜 제트 네뷸라이저의 비용 대비 효과를 떨어뜨리고 있습니다. 환기 능력이 제한적인 외래 진료소에서는 네뷸라이저 사용을 제한하고 있어, 급성기 의료 이외 시장 성장을 저해하고 있습니다.

부문별 분석

2025년, 호흡 작동식 시스템은 낭포성 섬유증 및 기관지 확장증 치료에서 정확한 투여 능력을 바탕으로 제트 네뷸라이저 시장 점유율의 42.15%를 차지했습니다. 이러한 시스템은 흡입 시에만 작동하는 기계식 밸브를 채택하여 투여량을 높이는 동시에 실내로의 오염을 줄여줍니다. 호흡 구동식 제트 네뷸라이저 시장은 낭비 감소와 고가의 항생제와의 호환성이 임상의들로부터 높이 평가받고 있어, 꾸준히 성장할 것으로 예측됩니다. 그러나 가격 경쟁의 압박으로 인해 병원들은 재고 최적화 전략의 일환으로 중가형 호흡 보조 기기의 도입을 검토하기 시작했습니다.

벤트식 또는 연속 분사식 제트 네뷸라이저는 기술적으로 그다지 고도화되어 있지는 않지만, 2031년까지 연평균 성장률(CAGR) 9.14%로 성장할 것으로 전망됩니다. 이러한 성장은 교차 감염을 줄이기 위해 일회용 키트 사용을 권장하는 병원의 감염 관리 방침에 힘입은 것입니다. 일회용 제품은 멸균 관련 규정 준수를 간소화하고 간호 업무의 부담을 줄여주기 때문에 응급실 비축품으로 선호되는 선택지입니다.

지역별 분석

2025년, 북미는 매출의 38.19%를 차지했습니다. 이는 메디케어 파트 B에 따른 급여와 응급실에서의 소용량 제트 프로토콜의 광범위한 도입에 힘입은 결과입니다. 미국에서는 약 1,600만 명의 성인이 만성 폐쇄성 폐질환(COPD)을 앓고 있으며, 기관지 확장제 키트에 대한 수요는 안정적인 상태를 유지하고 있습니다. 그러나 병원 통합과 가치 기반 지불 모델로의 전환으로 인해, 재입원을 줄이기 위해 의료 제공업체들이 예방 의료에 주력하는 경향이 강해지고 있어 판매량 증가세가 억제되고 있습니다. 캐나다에서는 압축기 플랫폼에 대한 일부 환급이 이루어지고 있지만, 각 주의 처방약 목록에서는 약제비 절감을 목적으로 제네릭 알부테롤이 우선적으로 지정되어 있습니다. 이러한 경향으로 인해 고부가가치의 항생제·의료기기 번들 제품의 도입이 제한되고 있습니다. 멕시코에서는 멕시코 사회보장원(IMSS)이 만성 호흡기 질환에 대한 보험 적용을 실시하고 있지만, 인구의 40%에 달하는 상당한 비율이 무보험 상태이며, 이는 시장에 대한 광범위한 확산을 저해하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 부상하고 있으며, 2031년까지의 연평균 성장률(CAGR)은 9.41%로 예측됩니다. 이러한 성장은 주로 의료기기 접근성을 높이고 있는 중국과 인도의 공적 보험 제도 확대에 힘입은 것입니다. 중국의 ‘건강 중국 2030’ 이니셔티브는 보험 적용 범위를 확대하고 있으며, 인도의 2선 도시에서 진행 중인 시범 프로그램은 상당수의 환자를 병원에서 재택 간호로 전환시키고 있습니다. 또한, 주요 도시의 대기 오염 문제가 질환의 중증도를 높이고 있어, 네뷸라이저를 이용한 응급 치료 처방이 증가하고 있습니다. 일본에서는 고령화로 인해 안정적인 수요가 예상되지만, 엄격한 가격 통제로 인해 이익률은 제한되고 있습니다. 한편, 한국과 호주에서는 국민건강보험 제도와 도시 지역의 천식 유병률 상승이 완만한 성장을 이끌고 있습니다. 반면, 인도네시아, 태국, 베트남 등의 국가들은 가격에 매우 민감하여 저가형 압축기나 일회용 회로를 선호하는 경향이 있습니다.

유럽 시장의 역학 관계는 다양합니다. 2024년 5월로 설정된 의료기기 규정(MDR)의 더 엄격한 기한으로 인해, 많은 소규모 제조업체들은 재인증을 받지 못한 SKU의 판매를 중단할 수밖에 없게 되었으며, 그 결과 제품 라인업이 축소되고 교체 수요가 위축되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the jet nebulizers market size was valued at USD 606.30 billion in 2025 and is estimated to grow from USD 652.90 billion in 2026 to reach USD 951.10 billion by 2031, at a CAGR of 7.79% during the forecast period (2026-2031).

This report is Segmented by Jet Nebulizer Type (Breath-Actuated, Breath-Enhanced, Vented/Continuous Output), Application (Asthma, COPD, Cystic Fibrosis, Other Respiratory), End-User (Hospitals & Clinics, Home Healthcare, Ambulatory/Urgent Care/Emergency Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Jet Nebulizers Market Trends and Insights

Global COPD and Asthma Crisis Fuels Surge in Inhaled Therapy Demand

Over 500 million individuals suffer from COPD or asthma globally, resulting in 4 million annual fatalities. The Asia-Pacific region accounts for approximately 60% of COPD-related deaths, with China reporting 99.9 million cases and India 55.3 million. Urban air pollution exacerbates these conditions, particularly in megacities like Beijing, Delhi, and Jakarta, which exceed recommended PM2.5 limits. Data from the UK registry spanning 2004-2023 indicates over 10 million diagnosed patients, with stable incidence in affluent areas but rising in underprivileged urban zones. This significant epidemiological burden ensures a consistent demand for the Jet nebulizers market, particularly among individuals facing challenges with metered-dose inhalers or cognitive impairments.

Home Respiratory Care and DME Coverage Boosts Compressor Therapy Adoption

The Centers for Medicare & Medicaid Services, in its 2025 DMEPOS fee schedule, simplified prior authorization for compressor nebulizers, benefiting both suppliers and patients. The Home Health Prospective Payment System's annual device functionality resurveys favor durable wall-powered compressors over battery-dependent mesh units, particularly in rural areas. China's 2024 expansion of insurance coverage for respiratory devices under its "Healthy China 2030" initiative promotes home treatments to reduce hospital readmissions. India's National Health Mission is piloting community distribution of subsidized jet nebulizers to improve adherence and reduce emergency department visits. With compressor jets priced between USD 30-100 and mesh alternatives starting at USD 400, the affordability of compressors is evident.

Infection-Control Concerns and Aerosolization Risks in Clinical Settings

In 2024, consensus statements emphasized that continuous-output jets generate aerosol plumes capable of transporting pathogens, including SARS-CoV-2, for up to 30 minutes in poorly ventilated rooms. In response, hospitals are investing in disposable circuits and implementing negative-pressure rooms. These measures, while enhancing safety, increase per-treatment costs and reduce the cost-efficiency of jets. Outpatient clinics with limited ventilation are restricting nebulizer use, constraining market growth outside acute care.

Other drivers and restraints analyzed in the detailed report include:

- Emergency Departments Favor Cost-Effective, Reliable SVNs for Acute Care

- Jet Nebulizers Outshine Alternatives in Cost-Effectiveness and Drug Compatibility

- Competition From Vibrating Mesh Nebulizers in Hospitals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, breath-actuated systems captured 42.15% of the Jet nebulizers market share, driven by their precise dosing capabilities in therapies for cystic fibrosis and bronchiectasis. These systems use mechanical valves that activate only during inhalation, enhancing the delivered dose while reducing cabin contamination. The market for breath-actuated jet nebulizers is expected to grow steadily as clinicians value their reduced wastage and compatibility with high-cost antibiotics. However, competitive pricing pressures are prompting hospitals to explore mid-priced breath-enhanced models as part of inventory optimization strategies.

Vented or continuous-output jets, though less advanced, are projected to grow at a 9.14% CAGR through 2031. This growth is supported by hospital infection-control policies that favor single-use kits to reduce cross-contamination. Disposable versions simplify sterilization compliance and decrease nursing labor, making them a preferred choice for emergency department stocking.

Geography Analysis

In 2025, North America accounted for 38.19% of the revenue, supported by Medicare Part B coverage and a widespread adoption of small-volume jet protocols in emergency departments. With approximately 16 million U.S. adults affected by COPD, there is consistent demand for bronchodilator kits. However, hospital consolidations and a shift to value-based payment models are limiting volume growth, as providers increasingly focus on preventive care to reduce readmissions. While Canada offers partial reimbursements for compressor platforms, its provincial formularies prioritize generic albuterol to manage drug costs. This focus restricts the adoption of premium antibiotic-device bundles. In Mexico, while the Instituto Mexicano del Seguro Social provides coverage for chronic respiratory diseases, a significant 40% of the population remains uninsured, hindering broader market penetration.

Asia-Pacific emerges as the fastest-growing region, with a 9.41% CAGR projected through 2031. This growth is primarily driven by expanding public insurance schemes in China and India, which are enhancing access to medical devices. China's "Healthy China 2030" initiative is broadening reimbursements, and pilot programs in India's tier-2 cities are redirecting substantial patient volumes from hospital settings to home care. Additionally, air quality issues in major cities are intensifying disease severity, leading to increased prescriptions for nebulized rescue therapies. Japan's aging demographic ensures steady demand, though stringent price controls limit profit margins. Meanwhile, universal coverage and a rising prevalence of asthma in urban areas are driving moderate growth in South Korea and Australia. In contrast, countries like Indonesia, Thailand, and Vietnam are highly price-sensitive, showing a preference for economy-grade compressors and disposable circuits.

Europe's market dynamics are varied. With tighter Medical Device Regulation deadlines set for May 2024, many small manufacturers have been compelled to withdraw non-recertified SKUs, leading to a reduction in product variety and a slowdown in replacements.

- 3A Health Care S.r.l

- Allied Healthcare Products (Schuco)

- Besco Medical Co., Ltd.

- Beurer

- Bremed Ltd.

- CA-MI S.r.l.

- Drive DeVilbiss Healthcare Inc.

- Flaem Nuova S.p.A.

- GE Healthcare

- Koninklijke Philips

- Medline Industries

- Microlife

- Monaghan Medical

- OMRON Healthcare, Inc.

- PARI GmbH / PARI Respiratory Equipment, Inc.

- Rossmax

- SunMed (Salter Labs)

- Teleflex Incorporated (Hudson RCI)

- Trudell Medical International

- Yuwell (Jiangsu Yuyue)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising COPD and Asthma Burden Expanding Inhaled Therapy Demand

- 4.2.2 Shift to Home-Based Respiratory Care and DME Coverage Supports Compressor-Based Therapy

- 4.2.3 Hospital Workflow Preference for Reliable, Low-Cost Svns in Acute Care

- 4.2.4 Cost-Effectiveness and Broad Drug Compatibility of Jet Systems Vs. Alternatives

- 4.2.5 Breath Actuated Jet Designs Reduce Waste and Improve Deposition

- 4.2.6 Drug Device Labeling Lock Ins for Certain Inhaled Antibiotics Sustain Installed Base

- 4.3 Market Restraints

- 4.3.1 Infection Control Concerns and Aerosolization Risks on Clinical Settings

- 4.3.2 Competition From Vibrating Mesh Nebulizers in Hospitals

- 4.3.3 EU MDR Transition/Recertification Burden Curtails Legacy Skus

- 4.3.4 Performance Variability/Residual Volume in Jets Complicates Dose Consistency

- 4.4 Value / Supply/Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Jet Nebulizer Type

- 5.1.1 Breath-actuated (BAN)

- 5.1.2 Breath-enhanced (BE)

- 5.1.3 Vented/continuous output

- 5.2 By Application

- 5.2.1 Asthma

- 5.2.2 COPD

- 5.2.3 Cystic Fibrosis

- 5.2.4 Other Respiratory (e.g., bronchiolitis, bronchiectasis)

- 5.3 By End-user

- 5.3.1 Hospitals & Clinics

- 5.3.2 Home Healthcare

- 5.3.3 Ambulatory/Urgent Care/Emergency Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3A Health Care S.r.l

- 6.3.2 Allied Healthcare Products (Schuco)

- 6.3.3 Besco Medical Co., Ltd.

- 6.3.4 Beurer GmbH

- 6.3.5 Bremed Ltd.

- 6.3.6 CA-MI S.r.l.

- 6.3.7 Drive DeVilbiss Healthcare Inc.

- 6.3.8 Flaem Nuova S.p.A.

- 6.3.9 GE Healthcare

- 6.3.10 Koninklijke Philips N.V.

- 6.3.11 Medline Industries

- 6.3.12 Microlife AG

- 6.3.13 Monaghan Medical

- 6.3.14 OMRON Healthcare, Inc.

- 6.3.15 PARI GmbH / PARI Respiratory Equipment, Inc.

- 6.3.16 Rossmax International

- 6.3.17 SunMed (Salter Labs)

- 6.3.18 Teleflex Incorporated (Hudson RCI)

- 6.3.19 Trudell Medical International

- 6.3.20 Yuwell (Jiangsu Yuyue)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment