|

시장보고서

상품코드

2063610

치과용 에이펙스 로케이터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Dental Apex Locator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

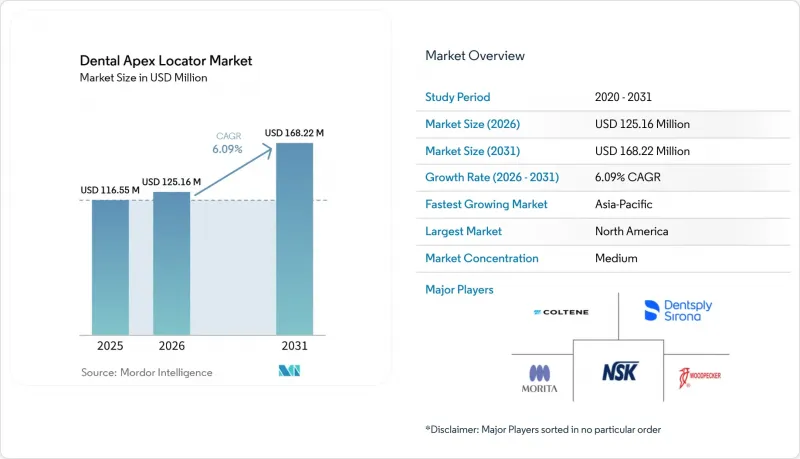

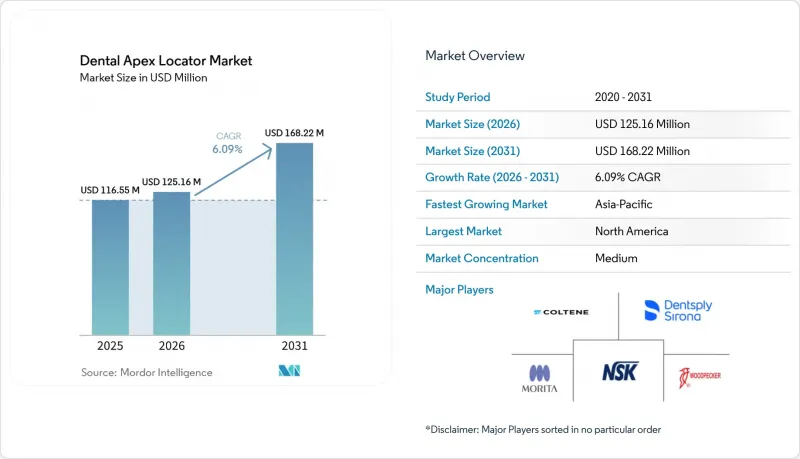

Mordor Intelligence에 의하면, 치과용 에이펙스 로케이터 시장 규모는 2025년 1억 1,655만 달러에서 2026년에는 1억 2,516만 달러로 확대되어 2031년까지 1억 6,822만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.09%로 성장할 전망입니다.

본 보고서는 제품(전자식 에이펙스 로케이터 및 기계식 에이펙스 로케이터), 기술(주파수식 및 임피던스식), 최종 사용자(치과, 병원, 기타 최종 사용자), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 치과용 에이펙스 로케이터 시장 동향 및 인사이트

충치의 확산과 고령화로 인한 근관 치료 건수 증가

세계적으로 높은 충치 발생률이 현재 근관 치료 사례 수의 꾸준한 증가로 이어지고 있으며, 이로 인해 치과용 에이펙스 로케이터 시장 수요가 증가하고 있습니다. 공중보건 감시 데이터에 따르면, 미국 성인의 상당수가 치료받지 않은 충치를 앓고 있으며, 그 유병률은 고령층에서 더 높은 것으로 나타났습니다. 이는 전자식 작업 시간 측정과 연계되어 지속적인 치료 건수를 뒷받침하는 것입니다. 2026년에도 인구 고령화는 구조적인 추세로 지속될 것이며, 공중보건 기관들은 21세기 중반까지 60세 이상 인구의 비율이 증가할 것으로 예측했습니다. 이는 시간이 지남에 따라 더 복잡한 수복 치료나 근관 치료가 필요하게 되는 것과도 관련이 있습니다. 미국에서는 전문의 주도의 진료 모델이 일반적이며, 2024년에는 치내요법 전문의가 담당하는 근관 치료의 비율이 2010년대 초반에 비해 증가하고 있습니다. 이는 정밀한 워크플로우에서 에이펙스 로케이터의 사용을 촉진하는 것입니다. 또한, 조사 데이터에 따르면 환자들은 발치보다는 근관 치료를 통해 자연치를 보존하는 것을 선호하는 경향이 있으며, 이것이 치내치료 전문의에게 의뢰되는 건수를 뒷받침하고 있습니다. 한편, 환자들의 선호는 치아 보존 쪽으로 결정적으로 바뀌고 있습니다. 2025년 AAE 소비자 조사에 따르면, 성인의 94%가 자연 치아 유지를 우선시했으며, 근관 치료를 받은 환자의 71%는 발치보다는 치료를 원했습니다. 이러한 요인들이 복합적으로 작용하여, 고성능 위치 추적기나 모터와 위치 추적기가 일체화된 시스템을 선호하는 기기의 교체 주기가 유지되고 있습니다.

근관 치료용 모터와 디지털 치과의 통합이 워크플로우와 치료 결과를 향상시킵니다.

모터와 에이펙스 로케이터를 통합한 이 시스템은 길이 측정과 형상 가공을 효율화하여 진료 시간을 단축하고, 진료실 내 장비 설치 공간을 줄이고 있습니다. 덴츠프라이 시로나의 ‘모터 앤 어펙스 모듈’은 미국에서 승인을 받았으며, 시술 중에 실시간으로 길이를 측정할 수 있습니다. 기존 제품을 바탕으로 한 안전성과 성능에 대한 주장이 입증되었으며, 이는 규제 당국이 통합 설계를 인정하고 있음을 반영합니다. 각 제조업체는 브러쉬리스 모터, 토크 제어, 그리고 설정된 치근단 목표 위치에서의 자동 역회전 기능을 로케이터의 피드백과 결합함으로써, 수동으로 일시 정지 및 측정하거나 엑스레이 검사를 실시할 필요성을 줄이고 있습니다. 그 결과, 근관 내 시술이 신속해지며, 습윤·건조 상태에 관계없이 작업 길이의 제어가 더욱 일관성 있게 이루어져, 여러 번 내원하는 경우와 1회 내원 프로토콜 모두에서 근단 감지기의 임상적 유용성이 높아집니다. 또한, 이러한 시스템은 영상 진단, 치료 계획, 기록 관리를 통합한 디지털 치의학 생태계와도 연동되어, 여러 진료소의 운영 및 의뢰 환자 조정을 지원합니다. 상호 운용성이 향상됨에 따라, 치과용 에이펙스 로케이터 시장에서 통합 플랫폼은 전문의와 환자 회전율이 높은 클리닉에게 표준적인 선택지로 자리 잡고 있습니다.

고급 모델의 높은 장비 비용과 총 소유 비용

가격대의 차이에 따라 독립형 치근단 위치 측정 장치와 모터 및 위치 측정 장치가 통합된 시스템은 구분되며, 이는 가격에 민감한 환경에서 도입에 영향을 미치고 있습니다. 카탈로그의 비교 데이터에 따르면, 통합 시스템은 독립형보다 가격이 비쌀 수 있으며, 이러한 가격 차이로 인해 효율성 향상이라는 이점이 분명하더라도 소규모 독립 클리닉에서는 구매 결정이 늦어지는 경우가 있습니다. 교체 부품, 배터리, 유지보수 비용은 수년에 걸친 총 소유 비용(TCO)에 가산되기 때문에 장비 구매를 신중하고 단계적으로 진행하는 경향이 있습니다. 번들 계약이 협상될 경우, 클리닉은 우선 진료용 의자, 영상 진단 장비 또는 멸균 장비를 우선시할 수 있으며, 그 결과 에이펙스 로케이터의 업그레이드가 후반 분기로 미뤄질 가능성이 있습니다. 유통업체은 제한 보증이 적용된 리퍼브 제품이나 인증 중고 제품을 제공함으로써 도입 시기를 앞당기고, 이러한 장벽을 극복하고 있습니다. 비용 면에서 역풍이 불고 있음에도 불구하고, 각 제조업체들은 치과용 에이펙스 로케이터 시장에서 통합 시스템 도입의 정당성을 입증하기 위해 신뢰성, 지원 및 워크플로우 효율화를 계속해서 강조하고 있습니다.

부문별 분석

전자식 에이펙스 로케이터는 2025년에 치과용 에이펙스 로케이터 시장 점유율의 82.79%를 차지해 2031년까지 연평균 성장률(CAGR) 6.34%로 성장할 것으로 전망됩니다. 이는 정확성, 통합성, 연결성을 중시하는 임상의들의 폭넓은 선호도를 반영한 것입니다. 치과용 에이펙스 로케이터 시장의 이 부문에서 주요 제품은 다중 주파수 임피던스 측정과 노이즈 관리 기술을 결합하여, 습윤 근관 내에서의 측정값 안정화를 도모하고 있습니다. 일체형 배터리 설계, 컴팩트한 콘트라 앵글 헤드, 그리고 원활한 사용자 인터페이스를 통해 다양한 근관 해부학적 구조에서 형성 및 재치료 중의 연속 측정을 지원합니다. 각 제조업체는 1회 치료 주기당 배터리 지속 시간, 페어 모터에서의 토크 제어 향상, 그리고 과도한 기구 조작의 위험을 줄이기 위해 자동으로 역회전하는 사전 설정된 치근단 목표값을 강조하고 있습니다. 비용이나 모듈성 등의 이유로 모터와 로케이터를 별도의 장치로 사용하는 것을 선호하는 임상의들 사이에서는 독립형 전자식 로케이터에 대한 수요가 여전히 존재합니다. 이러한 환경에서는 정확도는 물론, 간편한 메뉴 조작과 내구성이 뛰어난 클립이 중요시되고 있습니다.

기계식 에이펙스 로케이터는 초기 비용이 저렴하고 유지보수가 최소화되는 점을 중시하는 치과를 비롯해, 예산에 제약이 있는 사용자들 사이에서 계속해서 사용되고 있습니다. 기계식 시스템은 구매 가격이 저렴하지만, 습기에 민감하고 통합 제어 기능이 부족하기 때문에 전자식 시스템에 비해 복잡한 증례에서의 사용이 제한됩니다. 모터와 로케이터가 일체화된 패키지가 보급됨에 따라, 임상의들이 설치 공간 절약이나 워크플로우 중단을 최소화하기를 원하는 상황에서는 기계식 장치가 시장 점유율을 더욱 잃을 위험이 있습니다. 그렇긴 하지만, 전원 공급이 불안정한 경우나 기본 기능만으로도 충분한 경우에는 기계식 장치가 내구성이 뛰어난 백업 장치로 기능합니다. 가격대 폭이 넓은 시장에서는 유통업체이 진료소의 예산과 환자 구성에 맞추어 두 가지 가격대의 제품을 모두 판매하고 있습니다. 이러한 계층화는 환자 유입을 유지하면서, 치과용 에이펙스 로케이터 업계에서 전자식을 기본 표준으로 정착시키는 데 기여하고 있습니다.

지역별 분석

2025년에는 북미가 매출 점유율 44.56%로 1위를 차지했습니다. 이는 탄탄한 전문의 네트워크, 첨단 진료실 인프라, 그리고 치근관 치료에 대한 안정적인 보험 급여 체계에 힘입은 결과입니다. 최근 미국에서 모터와 에이펙스 모듈을 통합한 장치가 승인된 것은 연결형 다기능 치근관 치료 시스템에 대한 규제 측면에서의 지속적인 지지를 반영하고 있습니다. 자연치를 보존하고자 하는 환자의 의향이 근관 치료 건수를 지속적으로 증가시키고 있으며, 이에 따라 전문의나 환자 회전율이 높은 일반 치과에서 근단 감지기의 사용이 확대되고 있습니다. 미국 치내치료학회(AAE)의 보험 청구 데이터에 따르면, 치내치료 전문의가 시행한 근관 치료의 비율은 2020년 34.6%에서 2024년 44.4%로 증가했으며, 이는 전문의들이 정밀 측정 도구와 워크플로우 통합형 시스템을 도입한 것을 반영한 것입니다. 성숙기에 접어든 치과 병원의 장비 교체 주기와 연결성 향상이 맞물리면서, 2031년까지 한 자릿수 중반대의 성장이 예상됩니다. 연수 프로그램과 지속 교육을 통해 신입 의사부터 경험이 풍부한 임상 의사까지 기기에 대한 숙련도를 유지하고 있으며, 이는 기기 사용의 안정화를 더욱 뒷받침하고 있습니다. 이러한 요인들이 치과용 에이펙스 로케이터 시장의 꾸준한 수요를 뒷받침하고 있습니다.

유럽은 민간 클리닉 및 그룹 진료소의 높은 임상 기준과 기술 도입률 덕분에 여전히 큰 시장 점유율을 유지하고 있습니다. MDR(의료기기 규정)로의 전환 과정은 기기 교체를 촉진하고, 현재의 적합성 요건을 충족하는 모델로 교체하려는 수요를 뒷받침하고 있습니다. 연수 및 학술 활동에 대한 투자를 통해, 복잡한 증례에 대한 전자적 수술 범위 결정이 표준 치료법으로 자리 잡아가고 있습니다. 고령화가 진행되고 치과 의료에 대한 관심이 높은 시장에서는 치수 치료 시술 건수가 꾸준한 추세를 보이고 있습니다. 독일, 영국, 프랑스, 이탈리아, 북유럽 국가들에서 입지를 다진 브랜드를 보유한 각 벤더들은 정밀도, 시스템 통합 대응 능력, 서비스 모델을 놓고 경쟁하고 있습니다. 이러한 동향이 치과용 에이펙스 로케이터 시장의 견조한 중기 수요에 기여하고 있습니다.

아시아태평양은 민간 클리닉의 확대와 지역 허브로 유입되는 국경 간 환자 증가에 힘입어, 2031년까지 가장 빠르게 성장하는 지역이 될 것입니다. 그룹 진료의 발전과 기술 주도형 클리닉 설계는 치료의 복잡성이 심화되는 추세와 맞물려, 모터와 로케이터를 통합한 시스템의 조기 도입으로 가는 길을 열어줍니다. ISO 13485 인증을 획득한 시설을 보유한 현지 제조업체들은 저비용 대안에 대한 접근성을 확대하며 도입 대수를 늘리고 있습니다. 연수 및 소개 네트워크가 성숙해짐에 따라, 도시 지역의 치과에서는 더 많은 증례를 관리하고 검사실 및 영상진단센터와 연계하기 위해 앱 기반의 기록 기능을 도입하고 있습니다. 경쟁이 치열해짐에 따라, 의자, 멸균기, 모터, 에이펙스 로케이터를 통합된 서비스 계약 하에 묶어 구매하는 패키지 구매가 활성화되고 있습니다. 이러한 접근성, 가격, 통합성의 조합이 치과용 에이펙스 로케이터 시장의 추가적인 성장을 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the dental apex locator market size is expected to increase from USD 116.55 million in 2025 to USD 125.16 million in 2026 and reach USD 168.22 million by 2031, growing at a CAGR of 6.09% over 2026-2031.

This report is Segmented by Product (Electronics Apex Locators, and Mechanical Apex Locators), Technology (Frequency-Based, and Impedance-Based), End User (Dental Clinics, Hospitals, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Dental Apex Locator Market Trends and Insights

Rising Root Canal Procedure Volumes from Caries Prevalence and Aging Populations

A high global burden of dental caries is now translating into steady case inflows for endodontic treatment, which lifts demand in the dental apex locator market. Public health surveillance confirms a meaningful share of United States adults live with untreated cavities, and prevalence is higher in older cohorts, supporting persistent procedure volumes that align with electronic working length measurement. In 2026, population aging remains a structural trend, with public health agencies projecting a larger share of people over 60 by mid-century, which correlates with more complex restorative and endodontic care over time. Specialist-led practice models are more common in the United States, where endodontists handled a larger fraction of root canal procedures in 2024 than earlier in the decade, which reinforces the use of apex locators in precision workflows. Survey data also show patients often prefer saving a natural tooth with root canal treatment over extraction, which sustains referral volumes to endodontic specialists. Meanwhile, patient preference has shifted decisively toward tooth preservation. The 2025 AAE consumer survey found 94% of adults prioritize retaining natural teeth, and 71% of root-canal recipients preferred the procedure over extraction. Together, these factors maintain an equipment replacement cycle that favors advanced locators and integrated motor-plus-locator systems.

Integration With Endodontic Motors and Digital Dentistry Improves Workflow and Outcomes

Integrated motor-plus-apex-locator systems are streamlining length determination and shaping, which reduces chair time and consolidates equipment footprints in operatories. Dentsply Sirona's Motor and Apex Module received United States clearance and enables real-time length readings during active instrumentation, with predicate-supported safety and performance claims, reflecting regulator comfort with integrated designs. Manufacturers pair brushless motors, torque control, and auto-reverse at preset apical targets with locator feedback, which lowers the need for manual pause-and-measure steps and radiographic checks. The result is faster canal negotiation and more consistent working length control across wet and dry conditions, which increases the clinical utility of apex locators in multi-visit and single-visit protocols. These systems also align with digital dentistry ecosystems that integrate imaging, planning, and documentation to support multi-clinic operations and referral coordination. As interoperability improves, integrated platforms become a default choice for specialists and high-throughput clinics in the dental apex locator market.

High Device Cost and Total Cost of Ownership for Advanced Models

Price tiers separate standalone apex locators from integrated motor-plus-locator systems, which influences adoption in price-sensitive settings. Catalog benchmarks show integrated systems can cost more than standalone units, and that differential can slow purchase decisions for small independent clinics even when the efficiency gains are clear. Replacement parts, batteries, and maintenance add to total cost of ownership over several years, which encourages careful staging of equipment purchases. Where bundles are negotiated, clinics may prioritize chairs, imaging, or sterilization first, which can defer locator upgrades to later quarters. Distributors address these hurdles by offering refurbished or certified pre-owned units with limited warranties to pull forward adoption. Despite the cost headwinds, manufacturers continue to emphasize reliability, support, and workflow savings to justify integrated systems in the dental apex locator market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Dental Clinics and Dental Tourism Increases Equipment Uptake

- Dental Education and Continuing Training: Embed EAL Use in Clinical Curricula

- Regulatory Approval and Evidence Requirements Slow New Model Launches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electronics apex locators captured 82.79% of the dental apex locator market share in 2025 and are projected to grow at a 6.34% CAGR through 2031, reflecting broad clinician preference for accuracy, integration, and connectivity. Within this slice of the dental apex locator market size, leading products combine multi-frequency impedance measurement with noise management to stabilize readings in wet canals. Integrated battery designs, compact contra-angle heads, and smooth user interfaces support continuous measurement during shaping and retreatments across a range of canal anatomies. Manufacturers highlight charge longevity per treatment cycle, improved torque control in paired motors, and preset apical targets that activate auto-reverse to reduce over-instrumentation risk. Standalone electronic locators remain relevant where clinicians prefer separate motor and locator units for cost or modularity reasons. In these settings, menu simplicity and durable clips are valued alongside accuracy.

Mechanical apex locators continue to serve budget-constrained users, including clinics that prioritize low upfront costs and minimal maintenance. Although mechanicals carry lower acquisition prices, moisture sensitivity and the lack of integrated controls limit usage in complex cases compared with electronic systems. As integrated motor-plus-locator packages gain traction, mechanical devices risk ceding further ground where clinicians want consolidated footprints and fewer workflow interruptions. That said, mechanical units function as durable backups where power reliability is variable or where basic functionality suffices. In markets with wide price dispersion, distributors promote both tiers to match clinic budgets and case mixes. This tiering helps sustain access while reinforcing electronics as the default in the dental apex locator industry.

Geography Analysis

North America led in 2025 with 44.56% revenue share, supported by robust specialist networks, advanced operatory infrastructure, and stable reimbursement pathways for endodontic care. A recent U.S. clearance for an integrated motor and apex module reflects ongoing regulatory momentum for connected multi-function endodontic systems. Patient preference for preserving natural teeth continues to reinforce root canal volumes, which strengthens the utilization of apex locators in specialist and high-throughput general practices. Insurance claims data from the American Association of Endodontists reveals that the share of endodontic treatments performed by endodontists climbed from 34.6% in 2020 to 44.4% in 2024, reflecting specialist adoption of precision measurement tools and workflow-integrated systems. Replacement cycles in mature clinics, combined with connectivity upgrades, support mid-single-digit growth through 2031. Training programs and continuing education sustain device proficiency across new graduates and experienced clinicians, which further stabilizes usage. These ingredients anchor steady demand in the dental apex locator market.

Europe maintains a sizeable share with strong clinical standards and high technology adoption across private clinics and group practices. MDR transition milestones encourage device updating, which supports replacement purchases for models that align with current conformity requirements. Training and academic investments help embed electronic working length determination as standard-of-care for complex cases. In markets with aging populations and high dental-awareness, procedure volumes remain robust for endodontic treatments. Vendors with established brands in Germany, the United Kingdom, France, Italy, and the Nordics compete on accuracy claims, integration readiness, and service models. These dynamics contribute to resilient mid-term demand in the dental apex locator market.

Asia-Pacific is the fastest-growing region through 2031, driven by private clinic expansion and the growth of cross-border patient flows into regional hubs. Group practice development and technology-forward clinic designs create an early path for integrated motor-plus-locator systems, which aligns with rising procedural complexity. Local manufacturers with ISO 13485-certified facilities increase access to lower-cost options, which broadens the installed base. As training and referral networks mature, clinics in urban centers integrate app-based documentation features to manage larger caseloads and collaborate with labs and imaging centers. Competitive intensity encourages packaged purchases, with chairs, sterilizers, motors, and apex locators bundled under unified service agreements. This combination of access, pricing, and integration fuels higher growth in the dental apex locator market.

- Changzhou Haili Medical Co.,Ltd.

- Changzhou Sifary Medical Technology Co.,Ltd.

- COLTENE Group

- Dentsply Sirona

- DiaDent

- Envista

- Forumtec

- Foshan COXO Medical Instrument Co., Ltd.

- Foshan Tuojian Stomatological Medical Instrument Co., Ltd.

- Good Doctors Co.,Ltd.

- IONYX

- J. Morita

- Medidenta

- META BIOMED CO,. LTD.

- Nakanishi inc.

- Osada, Inc.

- Shenzhen Rogin Medical Co., Ltd.

- Woodpecker Medical Instrument Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Root Canal Procedure Volumes from Caries Prevalence and Aging Populations

- 4.2.2 Integration With Endodontic Motors and Digital Dentistry Improves Workflow and Outcomes

- 4.2.3 Expansion of Dental Clinics and Dental Tourism Increases Equipment Uptake

- 4.2.4 Dental Education and Continuing Training: Embed EAL Use in Clinical Curricula

- 4.2.5 Connectivity (Bluetooth/Cloud) Enabling Documentation and QA Workflows

- 4.2.6 HF-conduction Modules and 2-In-1 Apex Locator + Pulp Tester Expand Use-Cases

- 4.3 Market Restraints

- 4.3.1 High Device Cost and Total Cost of Ownership for Advanced Models

- 4.3.2 Regulatory Approval and Evidence Requirements Slow New Model Launches

- 4.3.3 EMC/Pacemaker Cautions and Hospital Policies Constrain Usage Scenarios

- 4.3.4 Accuracy Variability with Anatomy and User Training Needs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Electronics Apex Locators

- 5.1.2 Mechanical Apex Locators

- 5.2 By Technology

- 5.2.1 Frequency-based

- 5.2.2 Impedance-based

- 5.3 By End User

- 5.3.1 Dental Clinics

- 5.3.2 Hospitals

- 5.3.3 Other End Users (Academic & Research Institutes, Mobile Dental Units, and Among Others)

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Changzhou Haili Medical Co.,Ltd.

- 6.3.2 Changzhou Sifary Medical Technology Co.,Ltd.

- 6.3.3 COLTENE Group

- 6.3.4 Dentsply Sirona

- 6.3.5 DiaDent

- 6.3.6 Envista Holdings Corporation

- 6.3.7 Forumtec

- 6.3.8 Foshan COXO Medical Instrument Co., Ltd.

- 6.3.9 Foshan Tuojian Stomatological Medical Instrument Co., Ltd.

- 6.3.10 Good Doctors Co.,Ltd.

- 6.3.11 IONYX

- 6.3.12 J. MORITA CORP

- 6.3.13 Medidenta

- 6.3.14 META BIOMED CO,. LTD.

- 6.3.15 Nakanishi inc.

- 6.3.16 Osada, Inc.

- 6.3.17 Shenzhen Rogin Medical Co., Ltd.

- 6.3.18 Woodpecker Medical Instrument Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment