|

시장보고서

상품코드

2063612

항체 요법 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Antibody Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

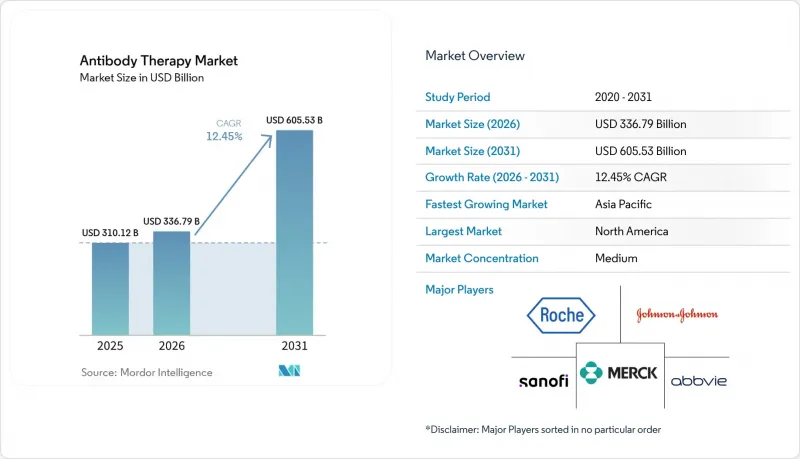

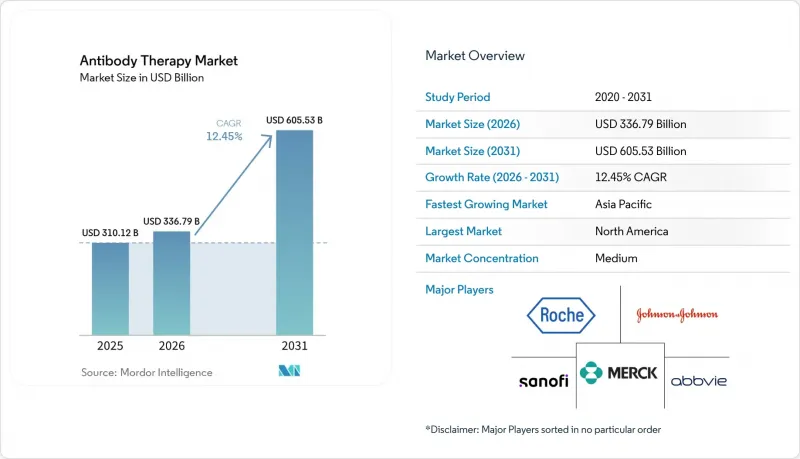

Mordor Intelligence에 의하면, 항체 요법 시장 규모는 2025년에 3,101억 2,000만 달러, 2026년에 3,367억 9,000만 달러, 2031년까지 6,055억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 12.45%로 성장할 전망입니다.

본 보고서는 제품 유형(단일클론 항체, 이중 특이성 항체 등), 질환 분야(종양학, 자가면역·염증성 질환 등), 투여 경로(정맥 내, 피하, 근육 내, 유리체 내 등), 최종 사용자(병원, 전문 클리닉, 재택치료/자가 투여), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 항체 요법 시장 동향과 인사이트

면역관문 억제제 및 종양학 분야의 적응증 확대가 환자층 확대를 가속화

규제 측면에서의 진전에 따라 체크포인트 억제제의 적용 범위가 확대되고 있습니다. 여기에는 근층 침윤성 방광암의 수술 전후 사용도 포함됩니다. 이 분야에서 PADCEV와 펨브롤리주맙의 병용 요법은 EV-304 임상시험 결과를 바탕으로 FDA의 우선 심사(Priority Review) 지정을 받았습니다. 이 임상시험에서 화학요법과 비교했을 때 무사건 생존 위험이 감소하고, 병리학적 완전 반응률이 향상된 것으로 나타났습니다. 해당 전문 분야의 기업들도 새로운 틈새 시장을 개척하고 있으며, 예를 들어 전이성 피부 편평상피암에 대한 코시베리맙-ipdl은 지속적인 치료 효과를 보였으며, 이후 장기적인 예후를 바탕으로 적응증 확대가 승인되었습니다. 자가면역 치료 분야도 확대되고 있으며, 구셀쿠맙의 승인 범위가 현재 염증성 장질환 분야까지 확대됨에 따라 면역조절 생물학적 제제의 만성 사용량이 더욱 증가하고 있습니다.

이러한 승인으로 인해 제제당 수익 잠재력이 높아졌으며, 주요 종양 유형 전반에 걸쳐 종양학 분야의 기반이 강화되고 있습니다. 이에 따라 항체 요법 시장은 수술 전후 및 전이성 병변 모두에 계속해서 초점을 맞출 것입니다. 동시에, 지불 주체나 정책적 요구에 따라 종양학 분야의 가격 책정 및 보험 적용 결정 과정에서 더 많은 실제 임상 데이터가 요구되고 있으며, 이에 따라 각 제약사는 기존의 임상 평가 지표를 넘어서는 결과를 계획하도록 촉구받고 있습니다.

면역학 분야: IL-23/IL-4/IL-13 계열의 성장이 만성 질환 치료제의 투여량을 뒷받침합니다.

면역학 분야의 기반은 만성 질환에 대한 치료 접근성과 복약 순응도를 개선하는 경구 및 피하 투여 옵션에 의해 확대되고 있습니다. 이코트로킨라는 2026년 일반 건선에 대한 최초의 경구용 IL-23 억제제로 승인되었으며, 주요 임상시험에서 피부의 완전하거나 거의 완전한 개선이라는 목표를 달성함으로써, 피부과 분야에서 경구용 펩타이드 제제를 주사제의 대안으로 자리매김했습니다. 피하 투여용 생물학적 제제는 사프네로가 프리필드 펜을 이용한 자가 투여 방식으로 EU 승인을 획득한 사례에서 볼 수 있듯이, 투여 방식이 지속적으로 변화하고 있으며, 이는 루푸스 등의 질환에서 환자들이 정맥 주사 이외의 투여 방식을 선호하는 경향과 일치합니다.

가정 환경에서의 복약 순응도의 이점은 면역글로불린 요법에서도 충분히 입증되었습니다. 피하 투여 요법은 실제 임상 현장에서 매우 높은 복약 순응도를 달성하고 있으며, 이는 편의성이 높은 투여법에 대한 광범위한 행동적 선호를 시사합니다. 이에 따라 보험사 및 HTA 기관들은 고가의 면역학 계열 바이오의약품을 보다 저렴한 가격의 비교 대상 약물과 비교하고 있으며, 이로 인해 항체 요법 시장에서 가격 규율과 근거 기준이 모두 강화되고 있습니다.

높은 치료비와 바이오 제조 비용이 접근성을 제한하고 있습니다.

장기적으로 볼 때, 상업적 규모의 항체 생산은 고역가의 포유류 세포 배양과 자본 집약적인 시설에 의존하고 있기 때문에 비용 구조가 계속해서 접근성에 영향을 미치고 있습니다. 공정의 발전으로 1그램당 비용은 시간이 지남에 따라 감소해 왔지만, ADC와 같은 복잡한 치료법은 고활성 페이로드의 관리나 약물 대 항체 비율과 같은 중요한 품질 특성 등으로 인해 새로운 개발 및 CMC(화학·제조·품질 관리)상의 부담을 초래합니다. 결합 및 규모 확대와 관련된 실패 사례는 확장되는 ADC 파이프라인에서 초기 CMC 위험 완화와 플랫폼 일관성의 필요성을 더욱 강조하고 있습니다.

또한, 많은 제약사가 피하 투여를 지원하기 위해 프리필드 주사기나 자동 주사기를 목표로 삼고 있기 때문에 의뢰사나 CDMO는 무균 충전 및 마무리 공정의 리드타임과 설비 용량을 둘러싼 경쟁에도 대응해야 합니다. 일회용 시스템은 특정 공정에서 유연성을 높여 시설의 점유 면적을 줄이고 이관을 신속하게 하는 데 기여하지만, 대규모 생산에서는 소모품으로 인한 운영 비용이 상당한 부담이 됩니다.

부문별 분석

2025년, 단일클론 항체는 항체 요법 시장 점유율의 64.23%를 차지했습니다. 이는 체크포인트 억제제나 만성 면역 질환 치료제가 대규모 환자 집단 및 전체 치료 단계에서 사용을 주도했기 때문입니다. 이중 특이성 항체는 2026년부터 2031년까지 연평균 성장률(CAGR) 16.84%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 제품 카테고리로, 면역 관여 및 혈관 신생 조절, 기타 종양 미세환경 표적을 결합한 견고한 후기 임상 개발 파이프라인과 전략적 제휴에 힘입어 성장하고 있습니다.

레제네론사의 림보셀타맙은 2025년에, 최소 4회의 선행 치료를 받은 재발성 또는 난치성 다발성 골수종에 대해 신속 승인을 획득했습니다. 이는 T세포를 표적으로 하는 이중 특이성 항체가, 명확한 위험 관리 프로그램 하에서 혈액종양학의 핵심 치료법이 될 가능성을 시사합니다. 또한, 각 스폰서사가 페이로드와 링커의 다양화를 추진하고 검증 시험을 실시함에 따라, 항체-약물 복합체(ADC)도 고형암 및 림프종 분야에서 계속해서 그 적용 범위를 넓혀가고 있습니다. 플랫폼 제휴 및 인수는 혁신의 속도와, 특허 만료에 앞서 해당 치료법 분야의 주도권을 확보하려는 의도를 여실히 드러내고 있습니다.

항체 요법 시장에서 ADC는 상업적 규모에서 특수한 격리 환경, 신뢰할 수 있는 결합 제어, 재현성 있는 약물 대 항체 비율을 필요로 하기 때문에 제조 및 CMC(화학·제조·품질 관리) 요인이 이 새로운 치료 방식의 규모 확대를 좌우하고 있습니다. 이러한 요건들은 비용과 복잡성을 증가시키지만, 공정 설계, 플랫폼 표준화 및 외부 생산 능력에 대한 투자를 통해 점차 충족되고 있습니다. 각 후원사는 일회용 시스템 도입에 있어 시설의 유연성과 비용 간의 균형을 맞추고 있습니다. 일회용 시스템은 개발 기간을 단축할 수 있는 반면, 상업적 생산량이 증가함에 따라 소모품 비용이 증가할 가능성이 있습니다.

한편, 차세대 ADC 페이로드 및 종양 선택적 설계 분야의 혁신으로 인해 치료 적용 범위가 확대되면서, 한때 포화 상태에 이른 것으로 여겨졌던 표적에 대한 관심이 다시 높아지고 있습니다. 파이프라인이 확대되는 가운데, 항체 요법 업계 전체가 자본 효율성을 유지하기 위해서는 포트폴리오의 합리화와 선택적인 제휴가 여전히 중요합니다.

2025년, 종양학 분야는 항체 요법 시장 규모의 48.62%를 차지했습니다. 이는 체크포인트 억제제, ADC, 그리고 새롭게 등장한 이중 특이성 항체가 수술 전후 및 재발 치료 분야에서 사용 범위가 확대되었기 때문입니다. 주술기 근층 침윤성 방광암에 대한 PADCEV와 펨브롤리주맙 병용 요법에 대한 FDA의 우선 심사 결정은 EV-304 임상시험의 견실한 결과를 바탕으로, 전이성 질환 분야 이외에서도 항체 요법의 사용이 확대되고 있음을 여실히 보여주고 있습니다. 코시베리맙-ipdl을 이용한 피부 편평상피암에 대한 적응증 확대의 진전과, 이중 특이성 항체 프로그램의 보다 광범위한 혈액종양 분야로의 적용은 종양학 분야 수요 증가를 반영하고 있습니다.

ADC 프로그램은 림프종 분야에서도 지속적으로 발전하고 있으며, 이는 표적 치료의 기반이자 2차 치료 전략을 뒷받침하는 것입니다. 호흡기 분야는 가장 빠르게 성장하고 있는 질환 분야로, 장시간 작용형 RSV 단일클론 항체와 소아용 권장 사항의 뒷받침에 힘입어 2026년부터 2031년까지 연평균 성장률(CAGR) 16.09%를 나타낼 것으로 전망됩니다. 크레스로비맙의 임상적 발전과 영아에 대한 예방적 사용을 권장하는 ACIP의 지침에 따라, 인구 수준에서 계절적 예방 효과가 확대되고 있습니다. 유럽의 실제 임상 데이터에 따르면, 도입 초기 단계에서 RSV로 인한 입원 건수가 대폭 감소했으며, 이는 의료 시스템의 가치를 높이는 동시에 계절을 넘나드는 안정적인 공급과 계획의 중요성을 입증하고 있습니다. 이러한 동향들은 종합적으로 볼 때, 2031년까지 항체 요법 시장에서 호흡기 질환의 예방 및 치료 분야의 지속적인 성장을 뒷받침하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 42.44%를 차지했습니다. 이는 개발 과정의 가속화, 피하 투여 방식의 혁신, 그리고 바이오시밀러의 꾸준한 시장 진입이 종양학 및 면역학 분야에서 이 치료법의 보급을 주도했기 때문입니다. 방광암 수술 전·수술 후 단계에서 PADCEV와 펨브롤리주맙의 병용 요법에 대한 우선 심사는 항체 병용 요법 분야의 ‘퍼스트-인-클래스’ 및 새로운 적응증 분야에서 해당 지역이 주도적인 입지를 차지하고 있음을 강조하고 있습니다. 또한, 2025년에 레제네론이 진행성 다발성 골수종에 대한 림보셀타맙의 신속 승인을 획득한 것은 혈액종양학 분야에서 T세포를 표적으로 하는 이중 특이성 항체의 개발 경로를 더욱 명확히 보여주는 사례입니다. 2026년 미국에서 출시될 데노스마브 바이오시밀러의 상호교환성 승인은 골다공증 및 종양학 보조요법 분야에서 경쟁을 심화시킬 것입니다. 이와 동시에, 실세계 증거가 종양학 약물의 정책 및 가격 협상에서 더 큰 역할을 수행하고 있으며, 이는 항체 요법 시장의 가격 동향에 영향을 미치고 있습니다. RSV 예방에 관한 정책 또한 영유아 보호를 위한 명확한 권고 사항을 통해 수요를 뒷받침하고 있으며, 이를 통해 계절별 계획이 유지되고 있습니다.

유럽에서는 더 많은 기업들이 회원국 전역에 단일클론 항체 바이오시밀러를 출시하고, 해당 카테고리의 깊이가 더해짐에 따라 바이오시밀러의 채택 및 접근성 측면에서 지속적인 진전이 나타나고 있습니다. 우스테키누맙 바이오시밀러의 시판 및 헨리우스(Henlius) 등 제약사들과 진행 중인 종양학 분야 제휴는 면역 및 암 치료 분야에서 경쟁이 지속될 것임을 시사합니다. 피하 투여의 적응증이 추가로 승인됨에 따라, 유럽의 의료 시스템은 정맥 주사의 부담을 줄이고 환자의 희망에 부응할 수 있게 되어, 이를 통해 의료의 분산이 촉진될 것입니다. 또한, 유럽의 실제 임상 현장 및 정책에서는 고가의 생물학적 제제에 대한 보험 적용을 유지하기 위해, 가치에 관한 근거에 대한 강한 관심이 지속되고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR)이 15.27%를 나타낼 것으로 예측되며, 가장 빠르게 성장하고 있는 지역입니다. 이는 현지 개발, 제조 파트너십, 그리고 해당 카테고리공급 범위를 확대하는 국경을 초월한 라이선싱을 바탕으로 하고 있습니다. 여러 국가에서 임상시험 단계에 있는 달라줌맙 바이오시밀러의 보험 적용을 목표로 한 헨리우스(Henlius)사와 닥터 레이디스(Doctor Ladies)사 등의 제휴는 종양학 분야에 대한 접근 경로를 확대되고 있습니다. 인도의 개발 기업도 데노스마브 바이오시밀러를 통해 미국 시장에 진출하고 있으며, 이는 전 세계 제품 출시에서 아시아태평양(APAC)의 역할이 커지고 있음을 보여줍니다. 또한, 아시아를 거점으로 하는 이중 특이성 항체 및 ADC(항체-약물 복합체) 프로그램은 다국적 기업의 개발을 보완하는 지역 내 파이프라인을 부각시키고 있으며, 여기에는 전 세계적인 증거 축적에 기여하는 NMPA(국가의약품감독관리국) 승인 임상시험도 포함됩니다. BNT327과 관련된 BMS와 BioNTech의 제휴와 같은 다국적 제휴에는 아시아태평양의 연구 거점을 포함한 대규모 범지역 프로그램이 포함되어 있으며, 이를 통해 항체 요법 시장에서 새로운 치료 방식의 세계 확장이 강화되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the antibody therapy market size is projected to be USD 310.12 billion in 2025, USD 336.79 billion in 2026, and reach USD 605.53 billion by 2031, growing at a CAGR of 12.45% from 2026 to 2031.

This report is Segmented by Product Type (Monoclonal Antibodies, Bispecific Antibodies, and More), Disease Area (Oncology, Autoimmune & Inflammatory Disorders, and More), Route of Administration (Intravenous, Subcutaneous, Intramuscular, Intravitreal, and More), End-User (Hospitals, Specialty Clinics, Homecare/Self-administration), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Antibody Therapy Market Trends and Insights

Checkpoint Inhibitors And Oncology Label Expansions Accelerate Patient Pools

Regulatory momentum is widening checkpoint inhibitor reach, including perioperative use in muscle-invasive bladder cancer, where PADCEV plus pembrolizumab secured FDA Priority Review based on EV-304 results that reduced event-free survival risk and improved pathological complete response versus chemotherapy. Specialty players also opened new niches, such as cosibelimab-ipdl for metastatic cutaneous squamous cell carcinoma, which delivered durable responses and later received a label update based on longer-term outcomes. Autoimmune pathways are expanding as well, with guselkumab approvals that now span inflammatory bowel disease segments, further reinforcing chronic-use volumes for immune-modulating biologics.

These approvals increase per-asset revenue potential and strengthen oncology backbones across major tumor types, which keeps the antibody therapy market focused on both perioperative and metastatic settings. At the same time, payer and policy demands are pulling in more real-world evidence for oncology pricing and coverage decisions, which encourages manufacturers to plan for outcomes beyond traditional clinical endpoints.

Immunology IL-23/IL-4/IL-13 Class Growth Sustains Chronic-use Volumes

The immunology backbone is broadening with oral and subcutaneous options that improve access and adherence for chronic conditions. Icotrokinra became the first oral IL-23 inhibitor approved for plaque psoriasis in 2026, supporting clear or almost clear skin targets in pivotal studies and positioning oral peptides as alternatives to injectables in dermatology. Subcutaneous biologics continue to shift administration patterns as illustrated by Saphnelo's EU approval for self-administration with a pre-filled pen, which aligns with patient preferences for non-infusion formats in diseases such as lupus.

Adherence advantages in home settings are also well documented in immunoglobulin therapy, where subcutaneous regimens achieve very high adherence in real-world use, which indicates the broader behavioral pull toward convenient administration. Payers and HTA bodies are in turn benchmarking high-cost immunology biologics against more affordable comparators, which heightens both price discipline and evidence standards in the antibody therapy market.

High Therapy And Biomanufacturing Costs Constrain Access

Over the long term, cost structures continue to influence access as commercial-scale antibody production depends on high-titer mammalian cell culture and capital-heavy facilities. Process advances have reduced per-gram costs over time, but complex modalities like ADCs bring new development and CMC burdens that include high-potency payload controls and critical quality attributes such as drug-to-antibody ratio. Failures linked to conjugation and scale-up reinforce the need for early CMC risk mitigation and platform consistency for growing ADC pipelines.

Sponsors and CDMOs are also navigating lead times and competition for sterile fill-finish capacity as many brands target pre-filled syringes and autoinjectors to support subcutaneous use. Single-use systems can improve flexibility in selected steps, which helps reduce facility footprint and speed transfers, although consumables add meaningful operating costs at scale.

Other drivers and restraints analyzed in the detailed report include:

- Subcutaneous And Long-Acting Formats Enable Home/Self-Administration

- Biosimilar Monoclonal Antibodies Expand Access In Mature Categories

- Patent Expiries And Biosimilar Price Erosion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monoclonal antibodies commanded 64.23% of the antibody therapy market share in 2025 as checkpoint inhibitors and chronic immunology brands anchored use across large patient populations and treatment lines. Bispecific antibodies are the fastest-growing product class with a projected 16.84% CAGR over 2026-2031, supported by robust late-stage pipelines and strategic alliances that combine immune engagement with angiogenesis modulation and other tumor microenvironment targets.

Regeneron's linvoseltamab received accelerated approval in 2025 for relapsed or refractory multiple myeloma after at least four prior lines, which illustrates the potential for T-cell-engaging bispecifics to become hematology backbones under defined risk management programs. Antibody-drug conjugates also continue to expand in solid tumors and lymphomas as sponsors push payload and linker diversity and execute confirmatory programs. Platform partnerships and acquisitions underscore the pace of innovation and the intent to secure modality leadership ahead of patent expiries.

Manufacturing and CMC factors shape scale-up for newer modalities in the antibody therapy market as ADCs require specialized containment, reliable conjugation controls, and reproducible drug-to-antibody ratios at commercial scale. These requirements raise cost and complexity but are being met by process design, platform standardization, and investments in external capacity. Sponsors are balancing facility flexibility and cost when adopting single-use systems, which can shorten timelines yet add consumable costs as commercial volumes rise.

Meanwhile, innovation in next-generation ADC payloads and tumor-selective designs is expanding therapeutic windows and renewing interest in targets once thought to be saturated. As pipelines grow, portfolio rationalization and selective partnering remain central to sustaining capital efficiency across the antibody therapy industry.

The oncology segment accounted for a 48.62% share of the antibody therapy market size in 2025 as checkpoint inhibitors, ADCs, and emerging bispecifics expanded use across perioperative and relapsed settings. FDA Priority Review for PADCEV plus pembrolizumab in perioperative muscle-invasive bladder cancer highlights deepening use of antibodies outside metastatic-only settings based on strong EV-304 outcomes. Label progress in cutaneous squamous cell carcinoma with cosibelimab-ipdl and the conversion of bispecific programs to broader hematology use reflect the breadth of oncology demand.

ADC programs also continued to advance in lymphomas, which supports targeted therapy backbones and second-line strategies. Respiratory is the fastest-growing disease area with a projected 16.09% CAGR from 2026 to 2031 on the strength of long-acting RSV monoclonal antibodies and supportive pediatric recommendations. Clesrovimab's clinical progress and ACIP guidance that endorses preventive use in infants broaden seasonal protection at a population level. Real-world experience in Europe shows large reductions in RSV hospitalizations during initial rollouts, which reinforces health-system value while prioritizing reliable supply and planning across seasons. Collectively, these dynamics support sustained growth for respiratory prevention and treatment in the antibody therapy market through 2031.

Geography Analysis

North America accounted for 42.44% of global revenue in 2025 as accelerated development paths, subcutaneous innovations, and steady biosimilar entry shaped uptake in oncology and immunology. Priority Review for PADCEV plus pembrolizumab in perioperative bladder cancer underscores the region's leadership in first-in-class and new-setting indications for antibody combinations. Regeneron's 2025 accelerated approval for linvoseltamab in advanced multiple myeloma further demonstrates the path for T cell engaging bispecifics in hematology-oncology. U.S. launches of interchangeable denosumab biosimilars in 2026 add competition in osteoporosis and oncology supportive care. In parallel, real-world evidence plays a larger role in policy and negotiation for oncology drugs, which influences pricing dynamics in the antibody therapy market. RSV prophylaxis policy also supports demand through clear recommendations for infant protection, which sustains seasonal planning.

Europe shows sustained progress in biosimilar adoption and access as more companies launch monoclonal biosimilars across member states and extend category depth. Commercial availability of ustekinumab biosimilar options and ongoing oncology collaborations with manufacturers such as Henlius point to continued competition in immune and cancer pathways. As more subcutaneous indications receive approval, European systems can reduce infusion burden and align with patient preferences, which supports decentralization of care. Real-world practice and policy in Europe also maintain a strong focus on value evidence to sustain coverage for high-cost biologics.

Asia-Pacific is the fastest-growing region at a projected 15.27% CAGR from 2026 to 2031, supported by local development, manufacturing partnerships, and cross-border licensing that broaden category availability. Partnerships such as Henlius and Dr. Reddy's for investigational daratumumab biosimilar coverage across many countries expand access pathways for oncology. Indian developers have also moved into the United States with denosumab biosimilars, which demonstrates APAC's rising role in global launches. Additional Asia-based programs in bispecific antibodies and ADCs highlight regional pipelines that complement multinational development, including NMPA-cleared studies that add to global evidence generation. ultinational alliances such as the BMS and BioNTech partnership for BNT327 include large pan-regional programs that touch APAC centers, which reinforces global reach for new modalities in the antibody therapy market.

- Abbvie

- Amgen

- AstraZeneca

- BeOne Medicines

- Biogen

- Bristol-Myers Squibb

- Daiichi Sankyo

- Roche

- Genmab

- GlaxoSmithKline

- Innovent

- Jiangsu Hengrui Pharmaceuticals Co., Ltd.

- Johnson & Johnson

- Eli Lilly and Company

- Merck

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Takeda Pharmaceuticals

- UCB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Checkpoint Inhibitors and Oncology Label Expansions Accelerate Patient Pools

- 4.2.2 Immunology IL-23/IL-4/IL-13 Class Growth Sustains Chronic-use Volumes

- 4.2.3 Subcutaneous And Long-Acting Formats Enable Home/Self-Administration

- 4.2.4 Biosimilar Monoclonal Antibodies Expand Access in Mature Categories

- 4.2.5 ADCs and Bispecifics Open High-Value Oncology Niches

- 4.2.6 Long-Acting Antibodies for Infectious Disease Prevention

- 4.3 Market Restraints

- 4.3.1 High Therapy and Biomanufacturing Costs Constrain Access

- 4.3.2 Patent Expiries and Biosimilar Price Erosion

- 4.3.3 Biologics/ADC Supply Chain and Capacity Bottlenecks

- 4.3.4 HTA and Real-world Evidence Hurdles to Reimbursement

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Monoclonal Antibodies (mAbs)

- 5.1.2 Bispecific Antibodies

- 5.1.3 Antibody-Drug Conjugates (ADCs)

- 5.1.4 Polyclonal Antibodies

- 5.1.5 Others (Antibody Fragments, Radiolabeled antibodies)

- 5.2 By Disease Area

- 5.2.1 Oncology

- 5.2.2 Autoimmune & Inflammatory Disorders

- 5.2.3 Infectious Diseases

- 5.2.4 Respiratory

- 5.2.5 Hematology

- 5.2.6 Cardiometabolic

- 5.2.7 Others (Ophthalmology, Neurology)

- 5.3 By Route of Administration

- 5.3.1 Intravenous (IV)

- 5.3.2 Subcutaneous (SC)

- 5.3.3 Intramuscular (IM)

- 5.3.4 Intravitreal

- 5.4 By End-user

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Homecare / Self-administration

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca

- 6.3.4 BeOne Medicines

- 6.3.5 Biogen

- 6.3.6 Bristol-Myers Squibb Company

- 6.3.7 DAIICHI SANKYO COMPANY, LIMITED

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 Genmab A/S

- 6.3.10 GSK plc.

- 6.3.11 Innovent

- 6.3.12 Jiangsu Hengrui Pharmaceuticals Co., Ltd.

- 6.3.13 Johnson & Johnson

- 6.3.14 Lilly

- 6.3.15 Merck & Co., Inc.

- 6.3.16 Novartis AG

- 6.3.17 Pfizer Inc.

- 6.3.18 Regeneron Pharmaceuticals Inc.

- 6.3.19 Sanofi

- 6.3.20 Takeda Pharmaceutical Company Limited

- 6.3.21 UCB S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment