|

시장보고서

상품코드

2063627

의료기기용 열가소성 엘라스토머 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Thermoplastic Elastomers In Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

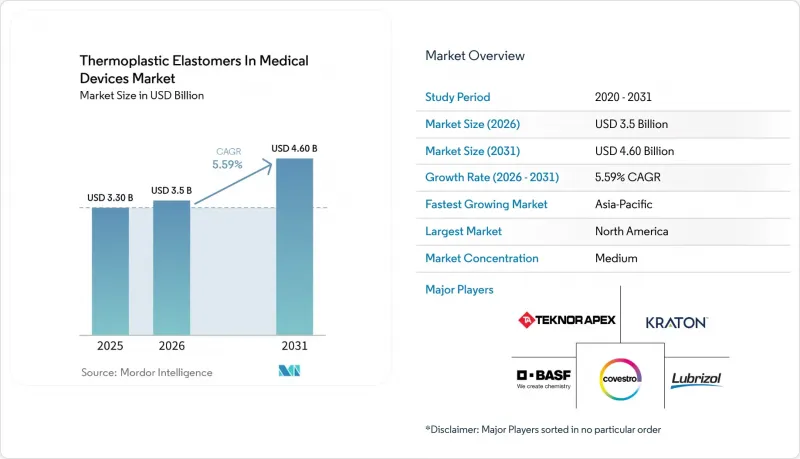

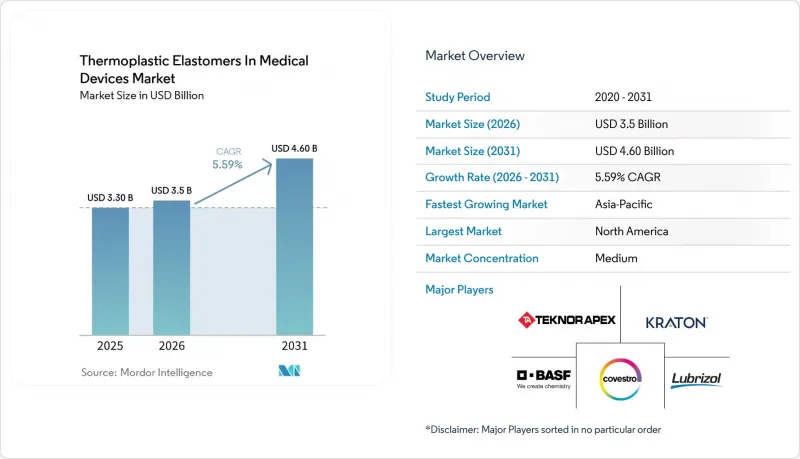

Mordor Intelligence에 의하면, 의료기기용 열가소성 엘라스토머 시장 규모는 2025년에 33억 달러로 평가되었습니다. 2026년 35억 달러에서 2031년까지 46억 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.59%를 나타낼 전망입니다.

본 보고서는 재료 유형(열가소성 엘라스토머 - 스티렌계/스티렌·에틸렌·부틸렌·스티렌(TPE-S/SEBS) 등), 용도(카테터·튜브 등), 가공 기술(압출 성형, 사출 성형, 블로우 성형·필름 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 의료기기용 열가소성 엘라스토머 시장 동향 및 인사이트

민감한 용도에서의 PVC/프탈레이트류로부터의 이온화

유럽 규정 2023/2482는 DEHP를 우려 물질로 지정하고, DEHP를 포함하는 의료기기의 최종 적용 기한을 2029년 1월 1일로 정하고 있습니다. 이에 따라 OEM 제조업체에는 36개월간의 재조성 기간이 주어졌으며, 가소제 용출에 대한 우려를 해소할 수 있는 SEBS나 열가소성 폴리우레탄(TPU) 등의 대체 소재로의 전환이 촉진되고 있습니다. 2024년에 발간된 지침에 따르면, 1일당 체중 1kg당 10µg을 초과하는 가소제를 방출하는 의료기기에 대해서는 위험-이익 분석이 의무화되어 있으며, 이에 따라 기존의 PVC 제품 라인은 사실상 사용이 불가능해집니다. 북미 제조업체들은 전 세계적인 일관성을 유지하기 위해 유럽 제조업체들과 일정을 조율하고 있으며, 의료기기용 열가소성 엘라스토머 분야에서 프탈레이트 무첨가 소재로의 집단적인 전환을 추진하고 있습니다.

저침습·카테터 치료의 확대

카테터 검사실에서는 굴곡 저항성이 뛰어나고 삽입하기 쉬운 샤프트가 필요한 심혈관, 신경혈관, 비뇨기과 분야의 시술 범위가 확대되고 있습니다. Pebax Rnew와 같은 폴리에테르 블록 아미드(PEBA) 컴파운드는 나일론 12에 비해 추진력을 50% 감소시켜 혈관 손상을 최소화하고 시술 시간을 단축합니다. 굽힘 피로 시험 결과, PEBA 재질의 샤프트는 90도 굽힘 상태에서 1만 사이클의 내구성을 보였으며, 이는 기존 폴리우레탄 재질 카테터의 수명보다 약 3배에 해당합니다. 이로 인해 당일 퇴원이 가능한 환경에서의 채용 확대가 촉진되고 있습니다. FDA 510(k) 승인 절차를 통해 제조업체는 기존의 마스터 파일을 활용하여 카테터 설계를 업데이트할 수 있게 되었으며, 이로 인해 승인 기간이 절반으로 단축되어 의료기기용 열가소성 엘라스토머의 보급이 더욱 확대되고 있습니다.

E&L 검증 및 멸균에 따른 물성 변화

ISO 10993-18 : 2020에서는 상세한 화학 프로파일 시험이 요구되며, 각 E&L; 프로그램에는 약 30만 달러의 비용이 소요되고 완료까지 9개월이 걸립니다. 50 kGy의 감마선 멸균은 미개질 PEBA의 인장 강도를 25% 저하시킬 가능성이 있으므로, 컴파운더는 산화 방지제 패키지를 배합하게 되지만, 그 결과 새로운 추출물이 도입되게 됩니다. 에틸렌옥사이드 멸균 시 잔류 에틸렌클로로히드린이 발생하지만, ISO 10993-7 : 2024 기준에 따르면 이를 기기당 4µg 미만으로 억제해야 합니다. 이러한 과학적 및 규제상의 과제로 인해 개발 기간이 길어지면서, 의료기기용 열가소성 엘라스토머의 단기적인 성장이 저해되고 있습니다.

부문별 분석

2025년, 스티렌계 블록 공중합체는 비용 효율이 뛰어난 투명성과 50 kGy의 감마선 조사 안정성을 갖추고 있어, 의료기기용 열가소성 엘라스토머 시장 규모의 43.18%를 차지했습니다. PEBA는 극히 얇으면서도 비틀림에 강한 벽면이 필요한 신경혈관 및 말초혈관용 카테터에 대한 수요 증가에 힘입어, 2031년까지 연평균 7.12%의 성장률을 나타낼 것으로 예측됩니다. 아르케마(Arkema)사의 바이오 제품인 ‘Pebax Rnew 30R53’은 피마자유 30%를 함유하고 있으며, 쇼어 D 경도 53을 달성하여 EU 그린딜의 조달 규정을 준수하고 있습니다. TPU는 2025년에 매출의 22%를 차지했으며, 7일간 착용 및 사용에 견딜 수 있도록 설계된, 펌프 구동으로 인한 마모에 강한 수액 세트용 튜브에 주로 사용되고 있습니다. TPE-E 및 TPC는 121℃까지의 오토클레이브 용도에 적합하지만, 에스테르 결합으로 인해 감마선 안정성에는 한계가 있습니다. TPV와 TPO는 불투명성과 높은 추출물 함량으로 인해 제약받고 있어, 시장 점유율은 8% 미만에 그치고 있습니다.

지역별 분석

2025년, 의료기기용 열가소성 엘라스토머 시장에서 북미는 매출의 36.33%를 차지했습니다. 이러한 우위는 미네소타주, 매사추세츠주, 캘리포니아주의 주요 클러스터에 의해 뒷받침되고 있으며, 이 지역에서는 메드트로닉, 애보트, 보스턴 사이언티피크와 같은 업계 선도 기업들이 FDA의 감독 하에 새로운 카테터 및 웨어러블 제품 라인을 확대되고 있습니다. 한편, 시장 매출의 28%를 안정적으로 차지하고 있는 유럽은 더욱 엄격해진 MDR(의료기기 규정)의 문서화 요건으로 인해 그 위상을 유지하고 있으며, 이는 종합적인 E&L(안전성 및 적합성) 자료를 제공할 수 있는 입지가 확고한 소재 공급업체에 유리하게 작용하고 있습니다. 현재 시장의 26%를 차지하는 아시아·태평양 지역은 2031년까지 7.63%의 성장률을 나타낼 것으로 전망되며, 성장을 주도할 것으로 예측됩니다.

이 지역의 성장은 세 가지 주요 요인에 의해 주도되고 있습니다. 첫째, 중국과 인도가 현지 조달을 추진하고 있는 만큼, 테크노아펙스가 DCM 슈리람과 2026년에 설립한 합작회사 ‘폴리테크’는 업무 효율화를 도모할 예정입니다. 동일 지역 내에서 배합 및 제조를 진행함으로써 리드타임을 6주 단축할 수 있습니다. 둘째, 연속 혈당 모니터링의 보험 적용 범위가 확대됨에 따라 수백만 명의 환자가 추가로 대상에 포함되면서, 센서 제조업체들의 현지 조립이 촉진되고 있습니다. 마지막으로, 일본 및 한국의 OEM 제조업체들은 고순도 등급에 주력하고 있으며, ISO 10993-18 규격을 충족하는 공급업체는 10-15%의 가격 프리미엄을 확보할 수 있습니다.

반면, 라틴아메리카와 중동 및 아프리카을 합친 시장은 의료기기용 열가소성 엘라스토머 시장의 매출에서 고작 8%만을 차지할 뿐입니다. 높은 수입 관세와 제한된 도입 실적이 첨단 2색 사출성형기에 대한 투자를 가로막고 있습니다. 또한, 기존의 PVC는 단기적인 소모품으로서 여전히 허용되고 있지만, 주요 다국적 기업들이 서방 국가들의 잉여 생산 능력을 이러한 지역으로 전환할 가능성이 있다는 점은 주목할 만합니다. 이러한 변화는 유럽이나 북미에서 DEHP 판매 규제가 도입될 경우 발생할 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the thermoplastic elastomers in medical devices market size was valued at USD 3.30 billion in 2025 and is estimated to grow from USD 3.5 billion in 2026 to reach USD 4.60 billion by 2031, at a CAGR of 5.59% during the forecast period (2026-2031).

This report is Segmented by Material Type (Thermoplastic Elastomer - Styrenic / Styrene-Ethylene-Butylene-Styrene (TPE-S/SEBS), and More), Application (Catheters & Tubing, and More), Processing Technology (Extrusion, Injection Molding, Blow Molding & Film, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Value (USD).

Global Thermoplastic Elastomers In Medical Devices Market Trends and Insights

Shift Away from PVC/Phthalates in Sensitive Uses

European Regulation 2023/2482 identifies DEHP as a substance of concern, setting a final application deadline of January 1, 2029, for medical devices containing DEHP. This provides OEMs with a 36-month window to reformulate, prompting a shift toward SEBS and thermoplastic polyurethane (TPU) alternatives that eliminate plasticizer leaching concerns. Guidance issued in 2024 requires a benefit-risk analysis for devices releasing more than 10 µg/kg body weight/day of plasticizer, effectively disqualifying traditional PVC lines. North American manufacturers are aligning their timelines with European counterparts to maintain global consistency, driving a collective shift in the thermoplastic elastomers in the medical devices market toward phthalate-free materials.

Growth in Minimally Invasive, Catheter-Based Therapies

Catheter laboratories are expanding their range of cardiovascular, neurovascular, and urological procedures, which rely on kink-resistant, pushable shafts. Polyether block amide (PEBA) compounds, such as Pebax Rnew, reduce advancement force by 50% compared to nylon 12, minimizing vessel trauma and shortening procedure times. Flexural-fatigue testing demonstrates that PEBA shafts endure 10,000 cycles at 90-degree bends, nearly tripling the lifespan of conventional polyurethane catheters, supporting broader adoption in same-day discharge environments. FDA 510(k) pathways enable manufacturers to update catheter designs using existing master files, reducing approval times by half and driving further penetration in the thermoplastic elastomers in medical devices market.

E &L Validation and Sterilization-Induced Property Shifts

ISO 10993-18:2020 requires detailed chemical-profile testing, with each E&L program costing approximately USD 300,000 and taking nine months to complete. Gamma sterilization at 50 kGy can decrease the tensile strength of unmodified PEBA by 25%, prompting compounders to include antioxidant packages, which subsequently introduce new extractables. Ethylene-oxide sterilization leaves residual ethylene chlorohydrin, which must remain below 4 µg/device under ISO 10993-7:2024 limits. These scientific and regulatory challenges extend development timelines, restraining near-term growth of the thermoplastic elastomers in the medical devices market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Wearable and Home-Care Devices

- OEM Change-Control Burden Under EU MDR Favors Stable Suppliers

- Cost Premium vs PVC and Silicone in Volume Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, styrenic block copolymers accounted for 43.18% of the thermoplastic elastomers in medical devices market size due to their cost-effective transparency and 50 kGy gamma stability. PEBA is expected to grow at an annual rate of 7.12% through 2031, driven by the increasing demand for neurovascular and peripheral-vascular catheters requiring ultra-thin, kink-resistant walls. Arkema's bio-based Pebax Rnew 30R53, with 30% castor-oil content, achieves Shore D 53 hardness, aligning with EU Green Deal procurement rules. TPU held 22% of revenue in 2025, preferred for infusion-set tubing designed to withstand pump-driven abrasion for seven days of wearable use. TPE-E and TPC are suitable for autoclave applications up to 121 °C, although their ester linkages limit gamma stability. TPV and TPO remain below 8%, constrained by opacity and higher extractables.

Geography Analysis

In 2025, North America accounted for 36.33% of the revenue in the thermoplastic elastomers for medical devices market. This dominance is supported by key clusters in Minnesota, Massachusetts, and California, where industry leaders such as Medtronic, Abbott, and Boston Scientific are scaling new catheter and wearable lines under FDA scrutiny. Meanwhile, Europe, contributing a steady 28% to the market revenue, maintains its position due to stricter MDR documentation, which benefits established material suppliers capable of providing comprehensive E&L dossiers. Asia-Pacific, currently holding 26% of the market, is expected to drive growth, with an expansion rate of 7.63% projected through 2031.

The region's growth is driven by three key factors. Firstly, with China and India promoting local sourcing, Teknor Apex's 2026 joint venture, PolyTek, with DCM Shriram, is set to streamline operations. Their in-region compounding reduces lead times by six weeks. Secondly, as reimbursement for continuous-glucose monitoring expands, millions more lives are covered, encouraging sensor manufacturers to localize assembly. Lastly, Japanese and South Korean OEMs are focusing on high-purity grades; suppliers meeting ISO 10993-18 standards can secure price premiums of 10-15%.

In contrast, Latin America and the combined regions of the Middle East & Africa account for a mere 8% of the thermoplastic elastomers in medical devices market revenue. High import duties and a limited installed base discourage investments in advanced two-shot injection presses. Additionally, while legacy PVC remains acceptable for short-term consumables, it is notable that major multinationals might redirect surplus capacity from the West to these regions. This shift could occur once DEHP sales face restrictions in Europe and North America.

- Actega DS GmbH

- Arkema S.A.

- Avient Corporation

- BASF

- Celanese Corporation

- Compagnie de Saint-Gobain S.A.

- Covestro

- Duke Extrusion

- Dynasol Group

- Elastron Kimya A.S.

- HEXPOL AB

- KRAIBURG TPE GmbH & Co. KG

- Kraton

- Kuraray Co., Ltd.

- Lubrizol

- Mitsubishi Chemical

- Nordson MEDICAL

- RTP Company

- Tekni-Plex, Inc.

- Teknor Apex Company

- TSRC Corporation

- Zeus Company Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Away from PVC/Phthalates in Sensitive Uses

- 4.2.2 Growth in Minimally Invasive, Catheter-Based Therapies

- 4.2.3 Expansion of Wearable and Home-Care Devices

- 4.2.4 OEM Change-Control Burden Under EU MDR Favors Stable Suppliers

- 4.2.5 Overmolding-Driven Part Consolidation (Bonding To PP/PA)

- 4.2.6 Gamma-Stable Transparent Tpes Enabling PVC-Free IV/Tubing

- 4.3 Market Restraints

- 4.3.1 E&L Validation and Sterilization-Induced Property Shifts

- 4.3.2 Cost Premium Vs PVC and Silicone in Volume Applications

- 4.3.3 OEM Material Change-Control Under MDR Extends Timelines

- 4.3.4 Supply-Chain Fragility for Medical-Grade Resins, Sterilization Bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter;s Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Thermoplastic Elastomer - Styrenic / Styrene-Ethylene-Butylene-Styrene (TPE-S/SEBS)

- 5.1.2 Thermoplastic Polyurethane (TPU)

- 5.1.3 Thermoplastic Elastomer - Amide / Polyether Block Amide (TPE-A/PEBA)

- 5.1.4 Thermoplastic Elastomer - Polyester / Thermoplastic Copolyester (TPE-E/TPC)

- 5.1.5 Thermoplastic Vulcanizate (TPV)

- 5.1.6 Thermoplastic Polyolefin (TPO)

- 5.2 By Application

- 5.2.1 Catheters & Tubing

- 5.2.2 Syringes & Plungers

- 5.2.3 Stoppers & Seals

- 5.2.4 Connectors & Device Housings

- 5.2.5 Wearables & Skin-Contact Interfaces

- 5.3 By Processing Technology

- 5.3.1 Extrusion

- 5.3.2 Injection Molding

- 5.3.3 Blow Molding & Film

- 5.3.4 Overmolding & 2K

- 5.3.5 Additive / Other

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Actega DS GmbH

- 6.3.2 Arkema S.A.

- 6.3.3 Avient Corporation

- 6.3.4 BASF SE

- 6.3.5 Celanese Corporation

- 6.3.6 Compagnie de Saint-Gobain S.A.

- 6.3.7 Covestro AG

- 6.3.8 Duke Extrusion

- 6.3.9 Dynasol Group

- 6.3.10 Elastron Kimya A.S.

- 6.3.11 HEXPOL AB

- 6.3.12 KRAIBURG TPE GmbH & Co. KG

- 6.3.13 Kraton Corporation

- 6.3.14 Kuraray Co., Ltd.

- 6.3.15 Lubrizol Corporation

- 6.3.16 Mitsubishi Chemical Corporation

- 6.3.17 Nordson MEDICAL

- 6.3.18 RTP Company

- 6.3.19 Tekni-Plex, Inc.

- 6.3.20 Teknor Apex Company

- 6.3.21 TSRC Corporation

- 6.3.22 Zeus Company Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment