|

시장보고서

상품코드

2063665

플랫폼 엔지니어링 및 내부 개발자 플랫폼(IDP) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Platform Engineering And Internal Developer Platform (IDP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

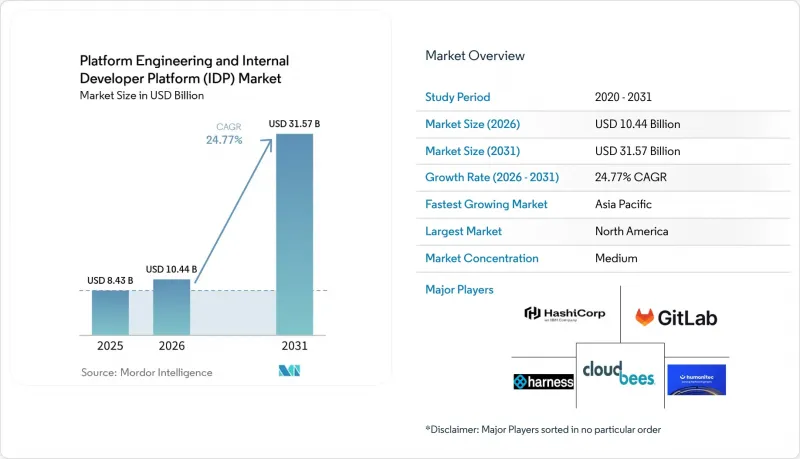

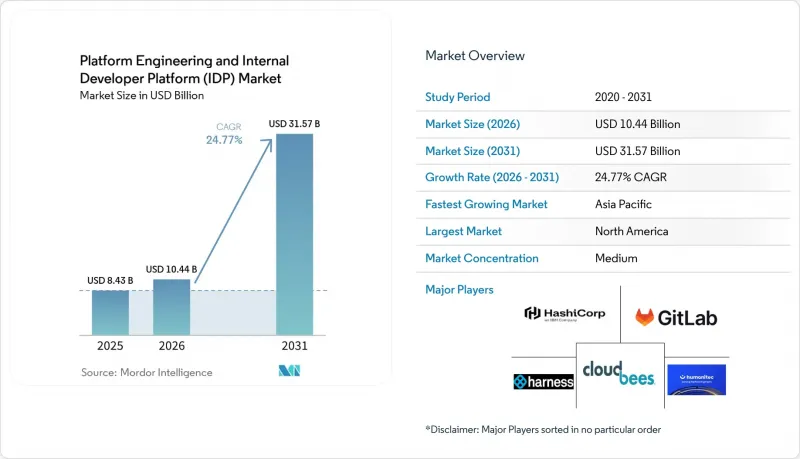

Mordor Intelligence에 의하면, 플랫폼 엔지니어링 및 내부 개발자 플랫폼(IDP) 시장 규모는 2026년 104억 4,000만 달러에서 2031년까지 315억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 24.77%를 나타낼 전망입니다.

본 보고서는 플랫폼 구성 요소(인프라 자동화 계층 등), 배포 모드(On-Premise, 클라우드, 하이브리드), 조직 규모(대기업, 중소기업), 최종 사용자 산업(기술·소프트웨어, 금융 서비스 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 플랫폼 엔지니어링 및 내부 개발자 플랫폼(IDP) 시장 동향 및 인사이트

클라우드 네이티브 아키텍처로의 전환 가속화

2025년에는 클라우드 네이티브 워크로드가 프로덕션 환경의 82%를 차지하게 되었지만, 쿠버네티스가 50종 이상의 핵심 리소스 유형을 도입하고 각 리소스마다 수십 개의 설정 매개변수를 갖게 되면서 운영 부담이 급증했습니다. 현재 내부 개발자 플랫폼은 기본적으로 네임스페이스, 인제스트, 정책 번들을 프로비저닝하므로, YAML의 확산을 방지하고 릴리스 주기를 단축하고 있습니다. 노키아의 5G 코어와 같은 초기 도입 사례에서는 수동으로 발생하는 클러스터 드리프트를 제거함으로써, 릴리스마다 수백 시간의 엔지니어링 공수를 절감했습니다. 금융기관에서는 바젤 III 및 감사 로그 정책을 템플릿에 직접 반영함으로써, 상품 출시 속도를 늦추지 않으면서도 규제 준수를 확보하고 있습니다. 관리형 쿠버네티스 서비스가 엣지 및 멀티 네트워킹 기능을 추가함에 따라, 개발자 경험을 단순하게 유지하기 위해서는 추상화 계층이 여전히 매우 중요합니다.

개발자의 생산성 향상에 대한 수요 증가

플랫폼 도입 전에는 개발자들이 주당 약 35%의 시간을 인프라 업무에 할애하고 있었으며, 이로 인해 기능 개발 속도가 둔화되고 있었습니다. 성숙한 플랫폼을 운영하는 조직에서는 배포 빈도가 40% 가까이 증가했고, 평균 복구 시간이 약 25% 단축된 것으로 보고되었습니다. 이러한 지표들은 경쟁 심화로 이어집니다. Shopify가 모듈형 관리 인터페이스로 전환한 결과, 101개 팀 전체에서 하루 평균 6,700만 페이지뷰를 처리할 수 있게 되었습니다. 이는 플랫폼 주도의 자동화를 통해 달성된 성과입니다. GDPR(EU 개인정보보호규정)과 같은 규제 체계는 ‘프라이버시 바이 디자인’ 원칙을 골든 패스에 통합하고 있어, 개발자가 기밀 데이터를 수동으로 처리할 필요가 없어집니다.월약 1,000달러라는 합리적인 가격의 SaaS 구독 서비스를 통해, 자원이 제한적인 중견 기업에서도 이러한 생산성 향상의 혜택이 확산되고 있습니다.

사내 플랫폼 구축에 따른 막대한 초기 투자

프로덕션 환경용 플랫폼을 구축하려면 대부분의 경우 3-5명의 전임 엔지니어가 최대 18개월 동안 필요하며, 툴 및 클라우드 비용을 제외하더라도 인건비만 15만-65만 달러에 달할 전망입니다. 이러한 자본적 장벽으로 인해 많은 중소기업은 시장 진입을 포기할 수밖에 없었으며, 세계 기업의 대다수를 차지하고 있음에도 불구하고 2025년 지출에서 차지하는 비중은 고작 38.62%에 그쳤습니다. 지속적인 기능 개선, 정기적인 보안 패치 적용, 사용자 경험 개선 등이 라이프사이클 비용을 증가시켜, 일부 기업들은 구독형 서비스 도입을 결정하고 있습니다. Software Defined Automation사가 1,000만 달러 규모의 시드 라운드를 유치한 후 2026년 2월에 ISO 27001 인증을 취득한 경위는 규정 준수 대응에 드는 간접비가 총비용을 부풀린다는 사실을 여실히 보여주고 있습니다.

부문별 분석

개발자용 셀프 서비스 포털은 2025년 매출의 34.87%를 차지했으며, 이는 기업들이 초기 단계에서 워크플로우 자동화를 중시하고 있음을 반영합니다. 포털은 새로운 서비스를 개발하는 개발자들에게 있어 주요 접점으로서의 역할을 계속할 것이므로, 플랫폼 엔지니어링 및 내부 개발자 플랫폼 시장 규모에서 이 점유율은 앞으로도 선도적인 위치를 유지할 것으로 예측됩니다. 한편, 가시성 및 텔레메트리 분야는 모든 골든 패스에서 ‘트레이스 퍼스트’ 설계를 의무화하는 OpenTelemetry의 도입에 힘입어 연평균 25.77%의 성장률을 나타낼 것으로 전망됩니다. 통합 제품군에는 현재 메트릭, 트레이스, 로그가 초기 기본 구조에 포함되어 있으므로, 개발자가 별도의 절차를 거치지 않아도 모든 마이크로서비스가 데이터를 전송하며, 성능 저하가 사용자에게 영향을 미치기 전에 확실하게 포착됩니다.

이와 동시에 플랫폼 설계도에 CI/CD 오케스트레이션을 통합하는 추세가 나타나고 있으며, 2025년 응답자의 67%가 GitOps를 최적의 배포 패턴으로 꼽았습니다. Pulumi의 OpenAPI 출시에서 알 수 있듯이, 인프라 자동화 구성 요소는 다양한 클라우드 REST 엔드포인트를 통합된 API 뒤에 추상화하여, 여러 공급자를 아우르는 워크플로우를 용이하게 합니다. 거버넌스 및 보안 계층에는 Open Policy Agent가 통합되어 있어, 어드미션 컨트롤러 단계에서 가드레일을 강제 적용합니다. 이러한 요소들을 종합해 보면, 플랫폼 엔지니어링 및 내부 개발자 플랫폼(IDP) 시장은 개별 모듈에서 설정 부채를 최소화하는 ‘의견이 반영된 번들’로 전환될 것으로 보입니다.

2025년, 운영 부담을 줄여주는 성숙한 관리형 쿠버네티스 서비스 덕분에 클라우드 배포는 플랫폼 엔지니어링 및 내부 개발자 플랫폼 시장의 46.32%를 차지했습니다. 그러나 하이브리드 토폴로지는 연평균 35.37%의 성장률을 나타낼 것으로 예상되며, 이는 시장 전체의 연평균 성장률(CAGR)보다 10포인트 이상 높은 수치입니다. 이러한 변화를 주도하고 있는 것은 유럽의 ‘디지털 운영 복원력 법(Digital Operational Resilience Act)’과 같은 규제 요건입니다. 이러한 조치들은 개발 환경에서 퍼블릭 클라우드의 확장성을 활용하는 한편, 은행 측에 On-Premise 재해 복구 구역을 유지하도록 요구하고 있습니다. 플랫폼 추상화는 이러한 서로 다른 환경을 통합하여, 워크로드가 최종적으로 어디에 배치되든 상관없이 개발자에게 단일 API를 제공합니다.

Vodafone의 검증된 OpenShift 패턴은 GitOps가 엣지 클러스터와 중앙 관리 플레인을 어떻게 동기화하는지 보여줍니다. 에어 갭이 적용된 방어 워크로드의 경우 여전히 On-Premise 배포가 필수적이지만, Oracle 등이 선보인 소버린 클라우드의 등장으로 인해 순수한 On-Premise 도입의 정당성은 점차 약화되고 있습니다. 멀티클라우드 도입이 확대됨에 따라, 플랫폼 청사진은 공급자 고유의 기본 요소를 숨겨야 합니다. 이러한 설계상의 전환은 하이브리드 환경의 성장을 가속하고 있으며, 벤더에 구애받지 않는 오케스트레이션을 필수 요건으로 자리매김하고 있습니다.

지역별 분석

북미는 쿠버네티스의 보급률이 높고 플랫폼 팀이 조기에 구성되었기 때문에 2025년 매출의 41.68%를 차지했습니다. 미국의 기업들은 PCI-DSS 4.0 및 SOC 2 Type 2의 통제 사항을 골든 패스에 직접 통합하여, 개발자들이 규정 준수의 세부 사항에 신경 쓰지 않고도 코드를 출시할 수 있도록 하고 있습니다. 이 지역의 급여 수준은 DevOps 기준치보다 27% 높아, 인재를 유치하는 한편 채용 파이프라인에 부담을 주고 있습니다. 따라서 기업들은 반복적인 플랫폼 유지보수 업무의 자동화를 추진하고 있습니다. 캐나다와 멕시코도 비슷한 경로를 밟고 있으며, GDPR(EU 개인정보보호규정)을 모델로 한 법령에 따라 규제되는 국경을 넘는 데이터 흐름을 관리하기 위해 파이프라인 현대화를 추진하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 24.89%로 성장하고 있으며, 그 원동력은 인도와 중국에서 주권 클라우드의 의무화입니다. 이에 따라, 통합된 개발자 인터페이스 뒤에서 다중 리전의 워크로드를 처리하기 위해서는 추상화 계층이 필수적입니다. Cloud Native Computing Foundation의 최신 조사에 따르면, 해당 지역 기업의 87%가 플랫폼 프로그램을 이미 도입했거나 도입을 계획 중인 것으로 나타났으며, 이는 플랫폼 엔지니어링 및 내부 개발자 플랫폼 시장이 지속적인 두 자릿수 성장을 기록할 것이라는 신호로 볼 수 있습니다. 일본과 한국은 성숙한 도입 단계를 선도하고 있는 반면, 인도의 주요 기술 서비스 기업들은 전 세계 고객에게 제공하는 서비스를 표준화하기 위해 사내 플랫폼을 도입하고 있습니다. 인력 부족 문제가 여전히 심각하기 때문에 AI를 활용한 플랫폼이 운영상의 공백을 메우고 있습니다.

유럽은 중간 수준의 점유율을 유지하고 있지만, ‘디지털 운영 복원력 법(Digital Operational Resilience Act)’, ‘네트워크 및 정보 보안 지침 2(NIS II)’, 그리고 ‘일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))’이 소프트웨어 공급망 보증 분야에서 서로 겹치는 부분에서는 도입이 가속화되고 있습니다. 영국, 독일, 프랑스에서는 플랫폼 차원의 정책 수립에 의존하는 은행 및 통신 분야의 활용 사례에 지출이 집중되고 있습니다. 남미에서의 보급은 이제 막 시작되었습니다. 브라질과 아르헨티나에서는 코어 뱅킹의 현대화가 진행되고 있지만, 소규모 IT 생태계로 인해 도입이 저해되고 있습니다. 중동 및 아프리카에서는 아랍에미리트와 사우디아라비아가 플랫폼 추상화가 필요한 주권형 클라우드에 대한 투자를 주도하고 있는 반면, 사하라 이남 아프리카에서는 인프라 격차에 직면해 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the platform engineering and internal developer platform (IDP) market size is expected to increase from USD 10.44 billion in 2026 to reach USD 31.57 billion by 2031, growing at a CAGR of 24.77% over 2026-2031.

This report is Segmented by Platform Component (Infrastructure Automation Layer, and More), Deployment Mode (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Technology and Software, Financial Services, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Platform Engineering And Internal Developer Platform (IDP) Market Trends and Insights

Accelerating Shift to Cloud-Native Architectures

Cloud-native workloads grew to 82% of production estates in 2025, but the operational burden ballooned as Kubernetes introduced more than 50 core resource types, each carrying dozens of configuration parameters. Internal developer platforms now provision namespaces, ingress, and policy bundles by default, eliminating YAML sprawl and shortening release cycles. Early deployments, such as Nokia's 5G core, saved hundreds of engineering hours per release by removing manual cluster drift. Financial institutions layer Basel III and audit logging policies directly into templates, ensuring regulatory alignment without slowing product delivery. As managed Kubernetes services add edge and multi-networking features, abstraction layers will remain pivotal for keeping the developer experience simple.

Rising Demand for Developer Productivity Gains

Prior to platform adoption, developers devoted roughly 35% of their week to infrastructure tasks, stalling feature velocity. Organizations running mature platforms report near-40% boosts in deployment frequency and around 25% faster mean-time-to-recovery, metrics that translate into sharper competitive positioning. Shopify's migration to a composable admin interface processed 67 million daily page views across 101 teams, an achievement made possible by platform-driven automation. Regulatory frameworks such as GDPR embed privacy-by-design principles into golden paths so developers never manually handle sensitive data. Affordable SaaS subscriptions, priced near USD 1,000 per month, extend these productivity gains to resource-constrained mid-market firms.

High Upfront Investment in Building Internal Platforms

A production-grade platform often needs three to five full-time engineers for up to 18 months, equating to labor costs between USD 150,000 and USD 650,000 before tooling or cloud fees. This capital hurdle sidelines many small and medium-sized enterprises, which accounted for only 38.62% of 2025 spending despite representing the majority of global businesses. Continuous feature evolution, routine security patching, and user-experience refinement compound lifetime costs, prompting some firms to adopt subscription offerings. Software Defined Automation's path to ISO 27001 certification in February 2026, following a USD 10 million seed round, highlights how compliance overhead inflates the total price tag.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Kubernetes Complexity Necessitating Abstraction

- Expansion of Platform Teams in Large Enterprises

- Talent Shortage of Platform Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Developer self-service portals captured 34.87% of 2025 revenue, reflecting early enterprise emphasis on workflow automation. This slice of the platform engineering and internal developer platform market size is expected to retain leadership as portals remain the primary touchpoint for developers creating new services. Observability and telemetry pieces, however, are set to grow 25.77% annually, driven by OpenTelemetry adoption that mandates trace-first design across all golden paths. Integrated suites now fold metrics, traces, and logs into the initial scaffolding, so every microservice emits data without extra developer steps, ensuring that performance regressions are caught before they impact users.

A parallel trend favors CI/CD orchestration woven into platform blueprints, with 67% of 2025 respondents citing GitOps as their delivery pattern of choice. Infrastructure automation components, exemplified by Pulumi's OpenAPI release, abstract diverse cloud REST endpoints behind uniform APIs, easing multi-provider workflows. Governance and security layers embed the Open Policy Agent to enforce guardrails at admission controller time. Collectively, these pieces suggest the platform engineering and internal developer platform (IDP) market will shift from discrete modules toward opinionated bundles that minimize configuration debt.

Cloud deployment held 46.32% of the platform engineering and internal developer platform market share in 2025, thanks to mature managed Kubernetes services that lower operational lift. Yet hybrid topologies are projected to compound at 35.37% each year, more than 10 percentage points above the headline CAGR. Driving the swing are regulatory mandates, such as Europe's Digital Operational Resilience Act, that push banks to maintain on-premises disaster-recovery zones even as they leverage public-cloud elasticity for dev environments. Platform abstraction stitches together these disparate estates, presenting developers with a single API regardless of where workloads eventually land.

Vodafone's validated OpenShift patterns exemplify how GitOps keeps edge clusters in sync with centralized control planes. On-prem deployments remain mandatory for air-gapped defense workloads, yet the arrival of sovereign cloud options from Oracle and others is eroding the case for purely local installations. As multi-cloud adoption climbs, platform blueprints must mask provider-specific primitives, a design shift that fuels hybrid growth and cements vendor-agnostic orchestration as table stakes.

Geography Analysis

North America held 41.68% of 2025 revenue due to deep Kubernetes penetration and early formation of platform teams. Enterprises in the United States weave PCI-DSS 4.0 and SOC 2 Type 2 controls directly into golden paths, enabling developers to ship code without wrangling compliance minutiae. The region's salary premium, 27% above DevOps baselines, creates talent gravity but also strains hiring pipelines, prompting firms to automate repetitive platform maintenance tasks. Canada and Mexico follow similar trajectories, modernizing pipelines to manage cross-border data flows governed by GDPR-inspired statutes.

Asia-Pacific is expanding at a 24.89% CAGR, fueled by sovereign-cloud mandates in India and China that make abstraction layers indispensable for multi-region workloads behind unified developer interfaces. The latest Cloud Native Computing Foundation pulse shows that 87% of regional enterprises are either implementing or planning platform programs, an indicator that the platform engineering and internal developer platform markets will post sustained double-digit growth. Japan and South Korea dominate mature adoption, while India's technology-services giants embed internal platforms to standardize global client delivery. Talent shortages remain acute, so AI-guided platforms fill operational gaps.

Europe maintains a mid-tier share but is accelerating where the Digital Operational Resilience Act, the Network and Information Security Directive 2, and GDPR converge on software supply-chain assurance. The United Kingdom, Germany, and France channel spending into banking and telecom use cases that rely on platform-level policy codification. South America's penetration is nascent; Brazil and Argentina are modernizing core banking, yet smaller IT ecosystems are curbing uptake. In the Middle East and Africa, the United Arab Emirates and Saudi Arabia anchor sovereign-cloud investments that require platform abstraction, whereas sub-Saharan Africa faces infrastructure gaps.

- Humanitec GmbH

- OpsLevel Inc.

- Port.io Ltd.

- Armory Inc.

- Harness Inc.

- Platform.sh SAS

- CloudBees Inc.

- D2iQ Inc.

- Upbound Inc.

- Pulumi Corporation

- Weaveworks Ltd.

- GitLab Inc.

- Atlassian Corporation Plc

- Red Hat Inc.

- HashiCorp Inc.

- Circle Internet Services Inc.

- Okteto Inc.

- ReleaseHub Inc.

- Mirantis Inc.

- Syntasso Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Shift to Cloud-Native Architectures

- 4.2.2 Rising Demand for Developer Productivity Gains

- 4.2.3 Increasing Kubernetes Complexity Necessitating Abstraction

- 4.2.4 Expansion of Platform Teams in Large Enterprises

- 4.2.5 Growing Compliance Requirements for Software Supply Chains

- 4.2.6 Emergence of AI-Augmented DevOps Toolchains

- 4.3 Market Restraints

- 4.3.1 High Upfront Investment in Building Internal Platforms

- 4.3.2 Talent Shortage of Platform Engineers

- 4.3.3 Integration Challenges with Legacy Systems

- 4.3.4 Security Concerns Around Self-Service Portals

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Component

- 5.1.1 Infrastructure Automation Layer

- 5.1.2 Developer Self-Service Portal

- 5.1.3 CI/CD Orchestration

- 5.1.4 Observability and Telemetry

- 5.1.5 Governance and Security Controls

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 Technology and Software

- 5.4.2 Financial Services

- 5.4.3 Telecommunications

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Retail and E-Commerce

- 5.4.6 Manufacturing

- 5.4.7 Energy and Utilities

- 5.4.8 Government and Public Sector

- 5.4.9 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Humanitec GmbH

- 6.4.2 OpsLevel Inc.

- 6.4.3 Port.io Ltd.

- 6.4.4 Armory Inc.

- 6.4.5 Harness Inc.

- 6.4.6 Platform.sh SAS

- 6.4.7 CloudBees Inc.

- 6.4.8 D2iQ Inc.

- 6.4.9 Upbound Inc.

- 6.4.10 Pulumi Corporation

- 6.4.11 Weaveworks Ltd.

- 6.4.12 GitLab Inc.

- 6.4.13 Atlassian Corporation Plc

- 6.4.14 Red Hat Inc.

- 6.4.15 HashiCorp Inc.

- 6.4.16 Circle Internet Services Inc.

- 6.4.17 Okteto Inc.

- 6.4.18 ReleaseHub Inc.

- 6.4.19 Mirantis Inc.

- 6.4.20 Syntasso Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment