|

시장보고서

상품코드

2065586

HCM 및 급여계산 통합 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)HCM And Payroll Convergence Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

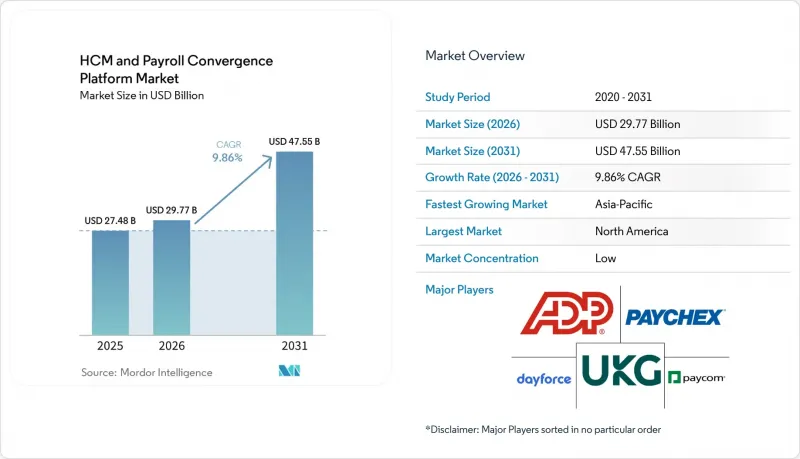

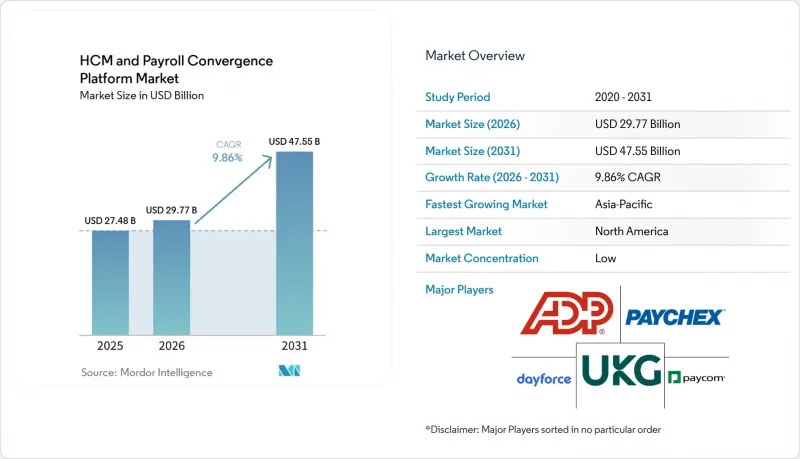

Mordor Intelligence에 의하면, HCM 및 급여계산 통합 플랫폼 시장 규모는 2025년 274억 8,000만 달러로 평가되었고, 2026년에는 297억 7,000만 달러로 추정되고, 2031년까지 476억 5,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 9.86%로 성장할 전망입니다.

본 보고서는 구성 요소별(소프트웨어 및 서비스), 배포 모델별(클라우드 기반, 온프레미스형, 하이브리드형), 기업 규모별(대기업 및 중소기업), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 정보기술·통신, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 HCM 및 급여 계산 통합 플랫폼 시장 동향과 인사이트

기존 인사 및 급여 시스템에서 클라우드로의 전환

기존의 인사 및 급여 시스템은 유지 관리가 어려워지고 업데이트에도 시간이 많이 소요됨에 따라, 클라우드 전환은 여전히 HCM 및 급여 계산 통합 플랫폼 시장에서 가장 강력한 구조적 요인으로 작용하고 있습니다. 2026년 5월 SAP SE와 타타 컨설팅 서비스(TCS)가 완료한 급여 업무 혁신을 통해, SAP Cloud ERP Private으로의 전환 후 급여 처리 주기가 30-40% 단축되었으며, 클라우드 환경이 실제 기업 환경에서 가져다주는 운영상의 이점이 입증되었습니다. 또한, 클라우드 네이티브 플랫폼에서는 벤더가 테넌트 환경 전체에 규칙 변경 사항을 일괄적으로 적용할 수 있으므로, 규정 준수 관련 업데이트가 용이해집니다. 반면, 온프레미스 사용자들은 여전히 사내 패치 적용 일정과 현지 테스트 주기에 의존하고 있습니다. 규제 변경이 빈번해지고, 급여 계산 팀이 정책 및 설정 변경 사이에 발생하는 지연에 대한 허용 범위가 좁아짐에 따라, 이러한 격차는 점점 더 중요해지고 있습니다. SAP의 온프레미스형 HCM 소프트웨어에 대한 표준 유지보수는 2027년에 종료될 예정이며, 이에 따라 많은 기업 고객들이 마이그레이션에 대한 수동적인 관심에서 적극적인 계약 결정으로 전환하고 있습니다. 이와 유사한 압박은 운영 실태에서도 드러나고 있으며, Strada가 2026년 5월에 발표한 보고서에 따르면, 대기업의 77%가 HCM 플랫폼을 이용하고 있음에도 불구하고 여전히 수동 급여 계산 백업 프로세스에 의존하고 있으며, 레거시 환경의 기술적 부채가 계속해서 현대화를 지연시키고 있는 것으로 나타났습니다.

다국적 급여 계산 및 노동 규정 준수의 복잡화

컴플라이언스의 복잡성은 많은 급여 계산 팀이 감당하기 어려울 정도의 속도로 진행되고 있으며, HCM 및 급여 계산 통합 플랫폼 시장은 단순한 소프트웨어 선호 문제가 아니라 규제 준수와 밀접하게 연관되어 있습니다. EU의 ‘임금 투명성 지침’은 2026년 6월 7일을 국내법 반영 기한으로 정하고 있으며, 해당 고용주에게는 2027년 6월에 첫 번째 남녀 간 임금 격차 보고 주기가 의무화됩니다. 이는 급여 계산 시스템과 인사 시스템 간에 공통된 보상 데이터 모델이 필요함을 여실히 보여주고 있습니다. 유럽 이외의 지역에서도 브라질의 ‘eSocial’이나 인도의 ‘직원적립기금기구(EPFO)’의 신고 요건과 같은 디지털 보고 프레임워크로 인해 지역별 설정 작업이 증가하고 있으며, 전 세계 기업들은 파편화된 시스템으로는 이를 적절히 관리할 수 없습니다. 따라서 구매자들은 통합 관리와 현지 규제 대응, 그리고 현지 문서 작성 지원을 결합할 수 있는 플랫폼을 점점 더 중요하게 여기고 있습니다. 이러한 운영상의 부담은 대규모 제품군에만 이점을 가져다주는 것은 아닙니다. 현지 규정 준수에 대한 심도 있는 지식은 신뢰할 수 있는 관할 구역 내 대응을 실현할 수 있는 각국의 엔진 전문가들에게도 강점이 됩니다. 그 결과, HCM(인적 자본 관리) 및 급여 계산 통합 플랫폼 시장은 소프트웨어 구독뿐만 아니라, 기업이 여러 국가에서 규정 준수를 유지할 수 있도록 지원하는 도입, 검증 및 관리형 급여 계산 서비스를 통해 성장하고 있습니다.

높은 전환 비용과 급여 데이터 이전의 위험

급여 데이터 이전에는 재무적, 법적, 평판상의 위험이 직접 수반되기 때문에 전환 비용은 여전히 HCM 및 급여 계산 통합 플랫폼 시장의 가장 큰 걸림돌 중 하나입니다. Strada가 2026년 5월에 발표한, 수동 급여 처리 백업에 대한 의존도와 관련된 조사 결과에 따르면, HCM 플랫폼을 도입한 조직조차 여전히 대체 프로세스에 의존하고 있는 것으로 나타나, 급여 변경 프로그램에 대한 운영상의 신중함이 얼마나 큰지 엿볼 수 있습니다. 이러한 어려움은 시스템 전환에만 그치지 않습니다. 기업은 과거 기록을 변환하고, 동시에 검증을 수행하며, 현지 규정을 테스트하고, 감사에 대비해 모든 단계를 문서화해야 하기 때문입니다. 따라서 기존 공급업체를 대체하는 것은 더욱 어려워집니다. 왜냐하면, 해당 벤더의 급여 계산 설정에는 대개 수년에 걸쳐 형성된 조직 고유의 논리가 포함되어 있어, 구매자가 이를 변경하는 것을 주저하기 때문입니다. 그 결과, HCM 및 급여 계산 통합 플랫폼 시장에서는 불만만으로는 교체로 이어지는 경우가 드물며, 신규 진출기업은 일반적으로 제품의 경제성 우위를 입증하기 전에 전환 위험이 낮다는 점을 입증해야 합니다.

부문별 분석

2025년, 소프트웨어는 총 매출의 68.14%를 차지했으며, 구독형 라이선싱이 여전히 기업 예산에서 가장 큰 비중을 차지함에 따라 HCM 및 급여 계산 통합 플랫폼 시장의 핵심으로 자리매김했습니다. 2025년, 소프트웨어는 HCM 및 급여 계산 통합 플랫폼 시장 점유율의 68.14%를 차지했으며, 이는 구매자들이 외부 지원을 추가하기 전에 여전히 핵심 플랫폼의 소유를 우선시하고 있음을 보여줍니다. 이 부문에서 핵심이 되는 인사 및 급여 계산은 대부분의 구매자에게 여전히 기본 계약으로 남아 있으며, 이를 기반으로 공급업체들은 근태 관리, 복리후생 관리, 인재 관리 도구 및 인력 관리 분야로 사업을 확장하고 있습니다. 고용주들이 관할 구역을 넘나드는 급여 대장, 인건비, 규정 준수 현황을 통합적으로 파악하기를 요구함에 따라, 수요는 전 세계적인 급여 관리 조정 및 분석 모듈로 빠르게 이동하고 있습니다. 이러한 확장 패턴 덕분에 소프트웨어는 공급업체의 수익에서 여전히 핵심적인 위치를 차지하고 있습니다. 왜냐하면 모듈이 추가될 때마다 플랫폼을 대체하기가 어려워지고, 재무 및 인사 팀에게 더 큰 가치가 생기기 때문입니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 12.47%로 확대될 것으로 예상되며, 수익 기반은 작지만 HCM 및 급여 계산 통합 플랫폼 시장에서 가장 빠르게 성장하는 분야가 될 전망입니다. 이러한 성장은 많은 구매자들이 거버넌스 구축, 현지 규정 검토, 각국에서 본격 전환 관리를 수행하는 것보다 소프트웨어를 구매하는 것이 더 신속하게 이루어질 수 있다는 사실을 반영하고 있습니다. 다국적 도입의 경우, 특히 사내 인사팀에 관할 지역별 전문 지식이 부족한 상황에서는 여전히 도입 컨설팅, 급여 계산 관리 지원, 병렬 가동 테스트 및 변경 관리가 필요합니다. AI를 활용한 템플릿이나 사전에 설정된 각국의 워크플로우를 통해 도입 과정의 일부를 단축할 수는 있겠지만, 전문 서비스에 대한 수요가 사라지는 것은 아닙니다. 오히려 HCM 및 급여 계산 통합 플랫폼 업계에서는 서비스의 중점이 거버넌스, 예외 처리, 그리고 장기적인 최적화로 옮겨가고 있습니다.

2025년에는 클라우드 기반 도입이 매출의 70.82%를 차지한 것으로 평가되었으며, 이는 HCM 및 급여 계산 통합 플랫폼 시장 전체에서 신규 도입 시 SaaS가 오랫동안 선호되어 온 추세를 반영하고 있습니다. 클라우드 플랫폼은 업데이트 과정을 간소화하고, 사내 인프라의 부담을 줄이며, 많은 구식 온프레미스형 시스템보다 더 정교한 직원용 셀프 서비스 경험을 제공하기 때문에 여전히 매력적입니다. 이러한 장점은 규정 준수 사항을 신속하게 업데이트하고자 하거나, 인사, 급여, 인력 관리 전반에 걸쳐 보다 통합된 인터페이스를 필요로 하는 조직에서 가장 두드러지게 나타납니다. 그렇긴 하지만, 규제 대상 기업의 도입 기반이 여전히 존재하기 때문에 일부 워크로드를 퍼블릭 클라우드 환경으로 완전히 이전할 수 있는 속도에는 한계가 있습니다. 따라서 데이터 저장 장소, 감사 관행 또는 내부 위험 관리의 관점에서 여전히 온프레미스 처리가 선호되는 분야에서는 온프레미스형 시스템이 계속해서 중요한 역할을 수행하고 있습니다.

하이브리드 방식은 2031년까지 연평균 성장률(CAGR) 14.63%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 모델인 동시에 단계적인 현대화를 위한 HCM 및 급여 계산 통합 플랫폼 시장 규모에 관한 논의에서 중요한 요소로 대두되고 있습니다. Mercans와 PayrollOrg는 2025년 보고서에서 조직의 37%가 사내 처리와 외부 위탁을 결합한 하이브리드형 급여 계산 모델을 채택하고 있으며, 21%는 국내 공급업체에 완전히 위탁하고 있다고 보고했습니다. 이는 유연한 제공 아키텍처가 여전히 상업적으로 중요한 이유를 여실히 보여줍니다. 대기업들은 셀프 서비스, 인력 관리, 분석 기능을 클라우드로 이전하는 한편, 계산 엔진이나 기밀성이 높은 국가별 프로세스는 현 상태를 유지하는 것을 선호하는 경향이 있습니다. 구형 SAP, Oracle, PeopleSoft 시스템과의 연동 기능을 갖춘 벤더들은 이러한 추세로 인해 혜택을 보고 있습니다. 이는 도입 첫날부터 시스템을 완전히 교체하도록 강요하지 않으면서도 전환 위험을 줄일 수 있기 때문입니다. HCM 및 급여 계산 통합 플랫폼 업계에서 하이브리드 모델은 일시적인 타협안이라기보다는 다층적인 ERP 환경을 갖추고 엄격한 거버넌스 요건을 준수해야 하는 조직에게 실용적인 장기 모델로 자리 잡고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 41.26%를 차지했으며, HCM 및 급여 계산 통합 플랫폼 시장에서 가장 규모가 큰 지역 점유율을 기록했습니다. 북미는 기업용 HCM 제품군의 광범위한 도입 실적과 성숙한 인사 기술 조달 관행에 힘입어, 2025년 HCM 및 급여 계산 통합 플랫폼 시장 점유율의 41.26%를 차지했습니다. 미국은 여전히 주요 견인 역할을 하고 있습니다. 이는 고용주들이 급여세 납부 의무를 자주 부담해야 하고, 주 차원의 휴가 및 임금 규제가 다양해지고 늘어나고 있기 때문에 플랫폼에 대한 지속적인 투자가 촉진되고 있기 때문입니다. Paylocity의 2026년 조사에 따르면, 인사 및 재무 업무를 단일 네이티브 플랫폼에서 운영하고 있는 조직은 고작 13%에 불과한 것으로 나타났으며, 이는 이 분야에서 여전히 대규모 시스템 교체 및 통합의 기회가 존재함을 뒷받침하고 있습니다. 캐나다와 멕시코에서는 국경을 넘는 노동력 이동과 하청업체에 대한 대금 지급의 복잡성으로 인해 이러한 수요가 더욱 증가하고 있으며, 이는 중견 기업들이 다중 관할권 대응 기능을 도입하도록 촉진하고 있습니다.

유럽은 HCM 및 급여 계산 통합 플랫폼 시장에서 여전히 2위의 규모를 유지하고 있으며, 가장 큰 규제 부담을 안고 있습니다. EU의 임금 투명성 지침은 2026년 6월 7일을 국내법 반영 기한으로 정하고 있으며, 2027년 6월부터는 해당 고용주에게 매년 남녀 간 임금 격차 보고가 의무화될 예정입니다. 이로 인해 조직은 보상 분석 및 보고를 뒷받침할 수 있는 인사 및 급여 통합 기록 시스템을 구축해야 할 필요에 직면해 있습니다. 독일과 영국은 공동 결정 원칙, 계약직 직원의 지위가 복잡한 점, 그리고 현지 규정 준수 요건 등이 모두 통합의 필요성을 높이고 있기 때문에 이 지역에서 여전히 두 개의 주요 시장으로 자리 잡고 있습니다. Personio는 2026년 1분기에 사상 첫 흑자 결산을 달성했으며, 고객사 1만 6,000곳, 최종 사용자 150만 명을 기록했습니다. 이는 유럽의 중소기업(SME) 부문에서 통합형 인사·급여 관리에 대한 수요가 상당한 규모에 이르렀음을 보여줍니다. 또한, 브라질의 eSocial 프레임워크와 아르헨티나의 임금 지수화의 복잡성으로 인해, 지역별 규정 준수 대응 기능이 강화된 플랫폼에 대한 수요가 높아지고 있어 남미의 중요성도 커지고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.12%를 나타낼 것으로 예측되며, HCM 및 급여 계산 통합 플랫폼 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. ADP는 2026년 3월, 해당 지역의 조직 중 49%가 급여 계산 업무에 AI 도입을 검토하고 있으며, 33%는 향후 2-3년 동안의 기술 투자에서 AI를 최우선 과제로 삼고 있다고 보고했습니다. 이는 업무 현대화의 시급성과 새로운 급여 계산 도구를 도입하려는 의지를 모두 여실히 보여주고 있습니다. 인도 및 동남아시아에서는 급여 계산의 표준화가 진행되고 있는 반면, 중국, 호주, 일본에서는 플랫폼 업그레이드를 뒷받침할 전자 신고에 대한 기대가 계속해서 높아지고 있습니다. 중동 및 아프리카에서는 인력 현지화 프로그램, 급여 계산 인프라 구축, 그리고 초기 단계 시장에 ‘모바일 퍼스트’ 전략 도입이 수요를 견인하고 있으며, HCM 및 급여 계산 통합 플랫폼 시장의 기회는 가장 성숙한 기업 지역을 넘어 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the hCM and payroll convergence platform market size is expected to increase from USD 27.48 billion in 2025 to USD 29.77 billion in 2026 and reach USD 47.65 billion by 2031, growing at a CAGR of 9.86% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM And Payroll Convergence Platform Market Trends and Insights

Cloud Migration from Legacy HR and Payroll Stacks

Cloud migration remains the strongest structural force in the HCM and payroll convergence platform market because older HR and payroll estates are becoming harder to maintain and slower to update. A May 2026 payroll transformation completed by SAP SE and Tata Consultancy Services delivered 30-40% faster payroll processing cycles after migration to SAP Cloud ERP Private, showing the operating advantage that cloud environments are now producing in live enterprise settings. Cloud-native platforms also make compliance updates easier because vendors can push rule changes across tenant environments at once, while on-premise users still depend on internal patching schedules and local testing cycles. This gap matters more as regulatory changes become more frequent and payroll teams have less tolerance for the lag between policy and configuration changes. SAP's standard maintenance for on-premises HCM software is due to end in 2027, turning passive interest in migration into active contract decisions for many enterprise accounts. The same pressure is evident in operating practice, as Strada reported in May 2026 that 77% of large employers still relied on manual payroll backup processes despite using an HCM platform, indicating that technical debt in legacy environments continues to slow modernization.

Rising Complexity of Multi-country Payroll and Labor Compliance

Compliance complexity is rising faster than many payroll teams can absorb, keeping the HCM and payroll convergence platform market closely tied to regulatory execution rather than software preference alone. The EU Pay Transparency Directive set a June 7, 2026, transposition deadline and will require the first gender pay gap reporting cycle in June 2027 for covered employers, underscoring the need for shared compensation data models across payroll and HR systems. Outside Europe, digital reporting frameworks such as Brazil's eSocial and India's Employees' Provident Fund Organization filing requirements are adding local configuration work that global employers cannot manage well through fragmented systems. That is why buyers increasingly value platforms that can combine centralized oversight with local rule execution and local documentation support. The operational strain does not benefit only the biggest suites; deep local compliance knowledge also protects in-country engine specialists who can deliver trusted jurisdiction coverage. As a result, the HCM and payroll convergence platform market is expanding not only through software subscriptions but also through implementation, validation, and managed payroll services that help enterprises stay compliant across multiple countries.

High Switching Costs And Payroll Data Migration Risk

Switching costs remain one of the strongest brakes on the HCM and payroll convergence platform market, as payroll migration carries direct financial, legal, and reputational risks. Strada's May 2026 findings on manual payroll backup dependence show that even organizations with HCM platforms still rely on fallback processes, indicating the extent of operational caution around payroll change programs. The difficulty is not limited to system cutover, since enterprises must also convert historical records, run parallel validations, test local rules, and document every step for audit readiness. That makes established vendors harder to displace because their embedded payroll configurations often hold years of organization-specific logic that buyers hesitate to disturb. The result is an HCM and payroll convergence platform market where dissatisfaction alone is rarely enough to trigger replacement, and challengers must usually prove lower migration risk before they can prove better product economics.

Other drivers and restraints analyzed in the detailed report include:

- Demand For Unified Employee Experience and Self-service

- AI-enabled Payroll Automation and Workforce Intelligence

- Data Privacy, Cybersecurity, And Cross-border Data Transfer Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 68.14% of total revenue in 2025 and remained the anchor of the HCM and payroll convergence platform market, as subscription licensing still accounts for the largest share of enterprise budgets. Software held 68.14% of the HCM and payroll convergence platform market share in 2025, showing that buyers continue to prioritize core platform ownership before layering external support. Within this layer, core HR and payroll remained the base contract for most buyers, and that base is still the point from which vendors expand into time and attendance, benefits administration, talent tools, and workforce management. Demand is moving quickly toward global payroll orchestration and analytics modules, as employers seek a single view of payroll registers, workforce costs, and compliance status across jurisdictions. That expansion pattern keeps software central to vendor revenue because each additional module makes the platform harder to replace and more valuable to finance and HR teams.

Services are projected to expand at a 12.47% CAGR through 2031, making them the fastest-growing component of the HCM and payroll convergence platform market, despite starting from a smaller revenue base. This growth reflects the fact that many buyers can purchase software faster than they can configure governance, validate local rules, and manage live cutovers across countries. Multi-country deployments still need implementation consulting, managed payroll support, parallel-run testing, and change management, especially when internal HR teams lack jurisdiction-specific expertise. AI-assisted templates and pre-configured country workflows may shorten parts of the deployment process, but they do not eliminate the need for specialist services. Instead, they are shifting service effort toward governance, exception handling, and long-term optimization inside the HCM and payroll convergence platform industry.

Cloud-based deployment accounted for 70.82% of revenue in 2025, reflecting the long-standing preference for SaaS in new implementations across the HCM and payroll convergence platform market. Cloud platforms remain attractive because they simplify updates, reduce internal infrastructure burdens, and support a cleaner employee self-service experience than many older local installations. That advantage is strongest in organizations that want faster compliance updates and a more unified interface across HR, payroll, and workforce management. Even so, the installed base of regulated enterprises still limits how quickly some workloads can be fully migrated to public cloud environments. On-premises systems, therefore, retain a meaningful role in sectors where data residency, audit practice, or internal risk controls still favor local processing.

Hybrid deployment is projected to record a 14.63% CAGR through 2031, making it the fastest-growing model and an important part of the HCM and payroll convergence platform market size discussion for phased modernization. Mercans and PayrollOrg reported in 2025 that 37% of organizations used a hybrid in-house and outsourced payroll model, while 21% fully outsourced to in-country providers, underscoring why a flexible delivery architecture remains commercially important. Large enterprises often prefer to keep calculation engines or sensitive country processes in place while moving self-service, workforce management, and analytics to the cloud. Vendors with connectors to older SAP, Oracle, and PeopleSoft estates are benefiting from this pattern, as it reduces cutover risk without forcing a full replacement on day 1. In the HCM and payroll convergence platform industry, hybrid is acting less like a temporary compromise and more like a practical long-term model for organizations with layered ERP estates and strict governance requirements.

Geography Analysis

North America accounted for 41.26% of global revenue in 2025 and represented the largest regional position in the HCM and payroll convergence platform market. North America held 41.26% of the HCM and payroll convergence platform market share in 2025, supported by a deep installed base of enterprise HCM suites and mature HR technology procurement practices. The United States remains the main engine because employers face frequent payroll tax obligations and a growing mix of state-level leave and wage rules that favor ongoing platform investment. Paylocity's 2026 survey also showed that only 13% of organizations operated HR and finance on a single native platform, which confirms that large replacement and consolidation opportunities still exist in the region. Canada and Mexico add to this demand through cross-border workforce mobility and the complexity of contractor payments, pushing mid-market firms toward native multi-jurisdictional capability.

Europe remained the second-largest region in the HCM and payroll convergence platform market and carried the heaviest regulatory burden. The EU Pay Transparency Directive set a June 7, 2026, transposition deadline and will require annual gender pay gap reporting for covered employers from June 2027, pushing organizations toward unified HR and payroll records that support compensation analysis and reporting. Germany and the United Kingdom remained the two largest national markets in the region because codetermination rules, contractor status complexity, and local compliance expectations all increase integration needs. Personio reported its first profitable quarter in Q1 2026, with 16,000 customers and 1.5 million end users, demonstrating that integrated HR and payroll demand in the European SME base has reached meaningful scale. South America is also gaining relevance as Brazil's eSocial framework and Argentina's wage indexation complexity increase demand for platforms with stronger native regional compliance support.

Asia-Pacific is projected to grow at a 15.12% CAGR through 2031, making it the fastest-growing region in the HCM and payroll convergence platform market. ADP reported in March 2026 that 49% of organizations in the region were exploring AI for learner payroll operations, and 33% viewed AI as their primary technology investment priority for the next 2-3 years, highlighting both the urgency of modernization and the willingness to adopt new payroll tools. India and Southeast Asia are benefiting from payroll formalization, while China, Australia, and Japan continue to raise digital filing expectations that support platform upgrades. In the Middle East and Africa, demand is being shaped by workforce nationalization programs, the formalization of payroll infrastructure, and mobile-first adoption in early-stage markets, extending the HCM and payroll convergence platform market opportunity beyond the most mature enterprise regions.

- Automatic Data Processing, Inc.

- Dayforce, Inc.

- UKG Inc.

- Paychex, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Gusto, Inc.

- Rippling People Center Inc.

- Deel Inc.

- Papaya Global Ltd.

- Bamboo HR LLC

- Hi Bob Limited

- Personio SE and Co. KG

- Darwinbox Digital Solutions Private Limited

- Workday, Inc

- isolved, inc.

- Zellis UK Limited

- Zalaris ASA

- Remote Technology, Inc.

- Oyster HR, Inc.

- Namely, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration From Legacy HR and Payroll Stacks

- 4.2.2 Rising Complexity of Multi-country Payroll and Labor Compliance

- 4.2.3 Demand for Unified Employee Experience and Self-service

- 4.2.4 AI-enabled Payroll Automation and Workforce Intelligence

- 4.2.5 EU Pay Transparency Directive Driving Shared Compensation Data Models

- 4.2.6 Convergence of Payroll With Workforce Payments and Contractor Payout Rails

- 4.3 Market Restraints

- 4.3.1 High Switching Costs and Payroll Data Migration Risk

- 4.3.2 Data Privacy, Cybersecurity, and Cross-border Data Transfer Exposure

- 4.3.3 In-country Payment Rail Fragmentation and Local Banking Mandates

- 4.3.4 Limited Native Country Engine Coverage Behind Aggregated Global Claims

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Core HR and Payroll

- 5.1.1.2 Workforce Management

- 5.1.1.3 Talent Management

- 5.1.1.4 Time and Attendance

- 5.1.1.5 Benefits Administration

- 5.1.1.6 Workforce Analytics and AI

- 5.1.1.7 Global Payroll Orchestration

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Dayforce, Inc.

- 6.4.3 UKG Inc.

- 6.4.4 Paychex, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Gusto, Inc.

- 6.4.8 Rippling People Center Inc.

- 6.4.9 Deel Inc.

- 6.4.10 Papaya Global Ltd.

- 6.4.11 Bamboo HR LLC

- 6.4.12 Hi Bob Limited

- 6.4.13 Personio SE and Co. KG

- 6.4.14 Darwinbox Digital Solutions Private Limited

- 6.4.15 Workday, Inc

- 6.4.16 isolved, inc.

- 6.4.17 Zellis UK Limited

- 6.4.18 Zalaris ASA

- 6.4.19 Remote Technology, Inc.

- 6.4.20 Oyster HR, Inc.

- 6.4.21 Namely, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment