|

시장보고서

상품코드

2063677

개복 수술용 스펀지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Laparotomy Sponges - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

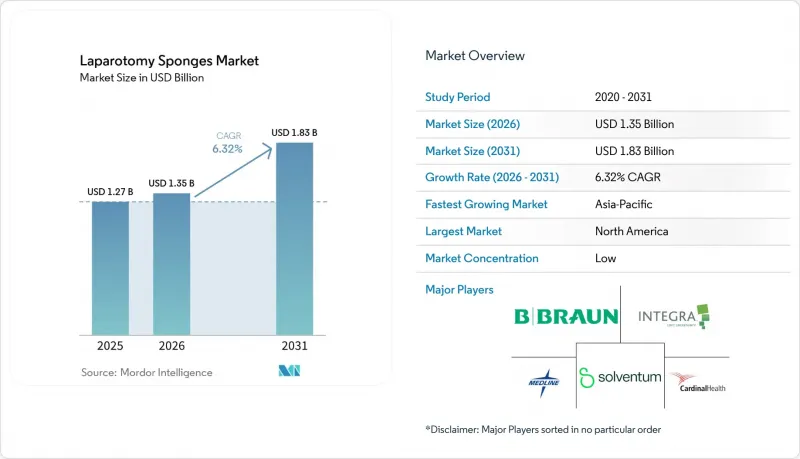

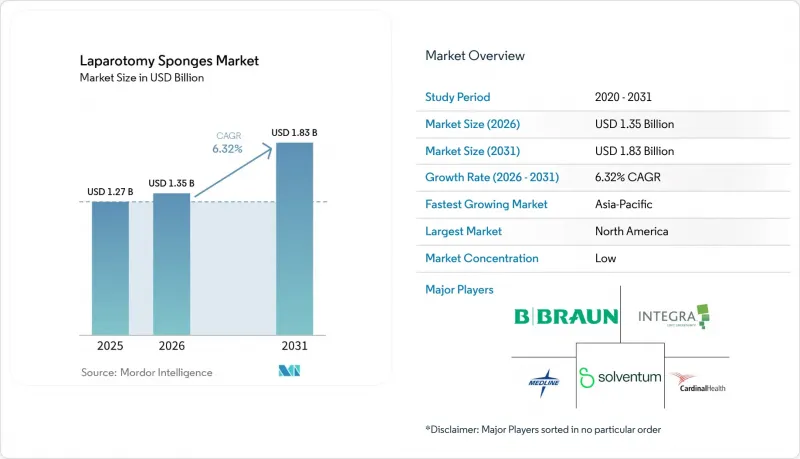

Mordor Intelligence에 의하면, 개복 수술용 스펀지 시장 규모는 2025년 12억 7,000만 달러로 평가되었습니다. 2026년에는 13억 5,000만 달러로 확대되어 2031년까지 18억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.32%를 나타낼 전망입니다.

본 보고서는 제품별(조영성 개복 수술용 스펀지, 기존 스펀지 등), 소재별(면, 레이온/비스코스, 부직포 및 합성섬유 혼방 등), 멸균 상태(멸균 처리된 제품 및 비멸균 제품), 최종 사용자(병원 및 클리닉, 외래수술센터(ASC) 등), 그리고 지역(북미, 유럽, 아시아태평양 등)에 따라 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계의 개복 수술용 스펀지 시장 동향 및 인사이트

수술 건수 증가

세계적으로 수술 건수는 계속 증가하고 있지만, 서중국병원 등 주요 의료기관에서는 당일 수술 프로토콜이 주류를 이루고 있습니다. 해당 병원에서는 전체 수술 건수 중 당일 퇴원 수술의 비율이 6.16%에서 25.11%로 증가했으며, 비용을 15% 절감했습니다. 인도의 2026-27년도 예산에서는 47억 달러가 ‘국가 보건 미션(National Health Mission)’에, 5억 7,300만 달러가 ‘PM-ABHIM’에 배정되어 있으며, 이로 인해 새로운 수술실(OR)의 수용 능력이 확보되는 한편, 수술 건수는 가격에 민감한 입찰 방식으로 전환되고 있습니다. 그 결과, 공급업체는 이익률을 유지하기 위해 스펀지에 물류, 위탁 판매 또는 수량 확인 서비스를 결합해야 합니다.

수술의 안전성과 기관 내 삽관 시 합병증(RSI) 예방에 대한 관심 증가

AORN(미국 수술실 간호협회)과 미국 외과학회는 2024년에 지침을 개정하여, 수동 계수가 신뢰할 수 없는 경우에는 조영제나 RFID(무선 주파수 식별)를 활용한 보조 수단을 권장하고 있습니다. 조인트 커미션은 2024년에 119건의 RSI 센티넬 사건을 기록했습니다. 건당 병원 비용은 약 52만 5,000달러에 달하기 때문에 리스크 관리 담당자들은 현재 단가보다 추적성 도구를 우선시하고 있습니다. 오거스틴 바이오메디컬(Augustine Biomedical)사의 2024년 RFID 특허는 태그가 134℃의 오토클레이브 처리를 견딜 수 있도록 하는 기술적 방안을 제시하고 있으며, 이에 따라 책임 소재에 대한 우려로 인해 구매 권한이 공급망 관리자에서 임상 품질 관리 팀으로 점차 이전되고 있습니다.

저침습 수술/지혈 대체 수단으로의 전환

영국에서 일반외과 수술 중 로봇 수술이 차지하는 비율은 2015년 0.4%에서 2024년에는 7.0%로 상승했으며, 5년 이내에 개복 수술을 추월할 것으로 예측됩니다. 로봇 플랫폼을 도입한 미국의 병원에서는 MIS(최소 침습 수술) 시행률이 65%를 넘으며, 1건당 스펀지 사용량을 최대 60%까지 줄이고 있습니다. 키토산-구리 복합체와 같은 새로운 지혈제는 출혈량이 많은 분야에서 기존의 스펀지를 점차 대체하고 있습니다. 따라서 공급업체는 복강경 포트 및 투시 하에서의 가시성을 고려하여 제품을 재설계해야 하며, 그렇지 않을 경우 판매량 감소의 위험에 직면하게 됩니다.

부문별 분석

2025년 기준으로, 조영성 스펀지는 개복 수술용 스펀지 시장의 42.57%를 차지하며 안전 기준의 토대로서의 역할을 재확인했습니다. 그러나 병원이 평균 52만 5,000달러에 달하는 RSI(수술실 내 출혈) 배상 책임과 30-50%의 가격 프리미엄 사이에서 저울질하는 가운데, RFID 탑재 제품은 2031년까지 연평균 성장률(CAGR) 7.56%를 나타낼 것으로 예측됩니다. Augustine Biomedical사의 2024년 특허는 RFID 태그가 134℃의 오토클레이브 처리를 견딜 수 있도록 하는 것으로, 도입에 따른 기술적 장벽을 해소하고 있습니다.

소송 위험이 높은 시장의 병원에서는 조영사 위에 RFID를 겹쳐서 사용하고 있지만, 인도나 아프리카의 자금 부족으로 어려움을 겪고 있는 공립 병원에서는 여전히 수작업으로 계수하는 방식을 선택하고 있습니다. 이러한 양극화로 인해 공급업체들은 이중 제품 포트폴리오를 구축할 수밖에 없게 되었습니다. 외상 센터 및 이식 센터용 프리미엄 RFID 팩과, 일상적인 충수 절제술용 저비용 조영제 제품 라인입니다. 이러한 접근 방식을 통해 개복 수술용 스펀지 시장 전체에서 시장 점유율을 극대화하고 있습니다.

개복 수술용 스펀지 시장에서 2025년 기준 면이 시장 점유율의 34.78%를 차지했습니다. 레이온과 비스코스는 상당한 성장이 예상되며, 2031년까지의 연평균 성장률(CAGR)은 7.54%로 전망됩니다. 2025년에는 인도, 브라질, 미국공급망 덕분에 면제품이 출하량을 주도했으나, 현물 가격은 1파운드당 60-78달러 사이에서 등락을 거듭하며 구매자들은 비용 위험에 노출되었습니다. 레이온이나 비스코스 혼방 제품은 가격 안정을 위해 다년 계약을 체결하는 의료 시스템의 공동 구매 조직들 사이에서 시장 점유율을 확대되고 있습니다.

캘리포니아주와 EU의 규제 당국은 생분해성 PLA 및 PHA 제품을 장려하고 있지만, 단가는 여전히 면의 2-3배 수준에 머물러 있습니다. 항균성 은·구리 코팅 제품은 감염 위험이 가장 높은 대장외과 및 외상외과 수술 분야에 널리 보급되고 있으며, 이를 통해 공급업체들은 개복 수술용 스펀지 시장 규모 내에서 치료 성과를 바탕으로 한 가치 제안을 통해 이익률을 유지할 수 있게 되었습니다.

지역별 분석

2025년에는 RSI 소송 비용 증가로 인해 병원들이 RFID 및 AI 기반 계수 시스템으로의 전환을 강요받은 결과, 북미가 매출 점유율 38.49%로 1위를 차지했습니다. 중대한 의료 사고 1건당 평균 비용이 52만 5,000달러에 달하기 때문에 조달위원회는 현재 스펀지를 위험 완화 수단으로 취급하고 있습니다. CMS의 2026년 ASC 규정에 따라 수요가 세분화되면서, 스펀지를 멸균 처리된 대용량 키트에 미리 장착한 상태로 공급하는 업체들이 유리한 입지를 점하고 있으며, 카디널 헬스의 2026년도 전망에서 지적된 관세로 인한 이익률 압박에도 불구하고 성장이 유지되고 있습니다.

아시아태평양은 인도의 127억 달러 규모의 의료 예산 배분과, 사양을 표준화하고 조달 물량을 확대하는 중국의 성(省) 전역에 걸친 조달 제휴 덕분에 2031년까지 연평균 성장률(CAGR) 12.68%로 가장 높은 성장률을 기록할 전망입니다. 다국적 기업들은 최저가 입찰을 따내기 위해 생산의 현지화를 추진하고 있는 반면, 일본과 호주의 사립 병원들은 의료 관광객을 대상으로 한 차원 높은 안전성을 어필하기 위해 RFID를 도입하고 있습니다.

유럽은 10%대 중반 시장 점유율을 유지하고 있지만, 로봇 수술에 따른 수요 둔화에 직면해 있습니다. 영국에서는 직장 전절제술의 30%가 이미 로봇 수술로 시행되고 있으며, 이러한 추세가 지속된다면 5년 이내에 1건당 스펀지 수요가 40-60% 감소할 가능성이 있습니다. 2026년 EUDAMED 등록에 따라 공급업체 수는 감소할 것으로 예상되며, MDR에 관한 풍부한 경험과 폭넓은 CE 마크 획득 제품 포트폴리오를 보유한 기업이 유리한 입지를 차지할 것입니다. GCC 국가들과 브라질은 CE 마크 또는 FDA 등록을 완료한 소모품이 필요한 의료 도시 메가 프로젝트나 공공 의료 시스템의 현대화에 자금을 투자하고 있어, 고성장 지역으로 꼽힙니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the laparotomy sponges market size is expected to increase from USD 1.27 billion in 2025 to USD 1.35 billion in 2026 and reach USD 1.83 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

This report is Segmented by Product (Radiopaque Laparotomy Sponges, Traditional Sponges, and More), Material (Cotton, Rayon / Viscose, Non-Woven & Synthetic Blends, and More), Sterility (Sterile and Non-Sterile), End-User (Hospitals & Clinics, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasted in Terms of Value (USD).

Global Laparotomy Sponges Market Trends and Insights

Rising Volume of Surgical Procedures

Global case counts continue to climb, yet day-surgery protocols now dominate at major centers such as West China Hospital, where same-day procedures rose from 6.16% to 25.11% of total surgical volume and cut costs by 15%. India's 2026-27 budget channels USD 4.7 billion into the National Health Mission and USD 573 million into PM-ABHIM, creating new OR capacity but driving volume toward price-sensitive tenders. Consequently, suppliers must package sponges with logistics, consignment, or count-verification services to protect margins.

Growing Focus on Surgical Safety & RSI Prevention

AORN and the American College of Surgeons updated guidelines in 2024 to recommend radiopaque or RFID adjuncts when manual counts are unreliable. The Joint Commission recorded 119 RSI sentinel events in 2024; each costs hospitals roughly USD 525,000, so risk officers now prioritize traceability tools over unit price. Augustine Biomedical's 2024 RFID patent shows the technical path forward, allowing tags to survive 134 °C autoclaves. Liability fears are therefore shifting purchasing power from supply managers to clinical-quality teams.

Shift Toward Minimally Invasive / Hemostatic Substitutes

Robotic surgery's share of U.K. general surgery rose from 0.4% in 2015 to 7.0% in 2024 and is on track to eclipse open techniques within five years. U.S. hospitals using robotic platforms push MIS rates above 65%, cutting sponge consumption per case by up to 60%. New hemostatic agents such as chitosan-copper composites further displace traditional sponges in high-bleed fields. Suppliers must therefore redesign products for laparoscopic ports and fluoroscopic visibility or risk volume loss.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements (Radiopaque, RFID, AI-Analytics)

- Expansion of Healthcare Infrastructure in Emerging Markets

- Regulatory & Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radiopaque sponges commanded 42.57% of the laparotomy sponges market share in 2025, reaffirming their role as the baseline safety standard. RFID-enabled products, however, are projected at a 7.56% CAGR through 2031 as hospitals weigh USD 525,000 average RSI liability against a 30-50% price premium. Augustine Biomedical's 2024 patent, which allows RFID tags to survive 134 °C autoclaving, removes a technical barrier to adoption.

Hospitals in litigation-prone markets are layering RFID on top of radiopaque threads, while cash-strapped public hospitals in India and Africa still opt for manual counts. The bifurcation forces suppliers to market dual portfolios: premium RFID packs for trauma and transplant centers and low-cost radiopaque lines for routine appendectomies, an approach that maximizes reach across the laparotomy sponges market.

The laparotomy sponges market saw cotton account for 34.78% of its share in 2025. Rayon and viscose are anticipated to witness significant growth, with a projected CAGR of 7.54% through 2031. Cotton dominated shipments in 2025 thanks to supply chains in India, Brazil, and the United States, though spot prices fluctuated between 60 and 78 per pound and exposed buyers to cost risk. Rayon and viscose blends are gaining share among health-system group purchasing organizations that lock in multi-year contracts for price stability.

Regulators in California and the EU are pushing biodegradable PLA and PHA options, yet unit prices remain 2-3 X higher than cotton. Antimicrobial silver-copper coatings are penetrating colorectal and trauma surgeries where infection risk is greatest, letting suppliers defend margins through outcome-based value propositions within the laparotomy sponges market size.

Geography Analysis

North America led with 38.49% revenue share in 2025 as RSI litigation costs pushed hospitals toward RFID and AI-count systems. Each sentinel event averages USD 525,000, so purchasing committees now treat sponges as risk-mitigation tools. CMS's 2026 ASC rule is fragmenting demand and favoring suppliers that preload sponges into sterile high-throughput kits, sustaining growth despite tariff-driven margin pressure flagged by Cardinal Health's FY2026 update.

Asia-Pacific will post the fastest 12.68% CAGR through 2031 thanks to India's USD 12.7 billion healthcare allocation and China's province-wide procurement alliances that standardize specifications and scale volumes. Multinationals localize production to win the lowest-bid tenders, while private hospitals in Japan and Australia adopt RFID to market premium safety credentials to medical tourists.

Europe sits in the mid-teens share bracket but faces volume drag from robotic surgery. Robotic anterior resections already represent 30% of U.K. rectal cases, a trajectory that may suppress sponge demand by 40-60% per case within five years. EUDAMED registration in 2026 will likely trim the supplier pool, advantaging firms with deep MDR experience and broad CE-marked portfolios. GCC countries and Brazil round out high-growth pockets as they fund medical-city mega projects and public-system upgrades that require CE- or FDA-listed consumables.

- A Plus International

- ACTIMED

- AdvaCare

- Allmed Medical Products

- B. Braun

- Cardinal Health

- DeRoyal Industries

- Dukal LLC

- Dynarex

- Haldor Advanced Technologies

- Integra LifeSciences

- Johnson & Johnson

- Medical Action Industries

- Medline Industries

- Medtronic

- Molnlycke Health Care

- Owens & Minor

- Premier Enterprises

- Smiths Group

- Solventum Corporation

- Stryker

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Volume of Surgical Procedures

- 4.2.2 Growing Focus on Surgical Safety & RSI Prevention

- 4.2.3 Technological Advancements (radiopaque, RFID, AI)

- 4.2.4 Expansion of Healthcare Infrastructure in Emerging Markets

- 4.2.5 AI-Enabled Real-Time Sponge-Count Systems

- 4.2.6 Sustainability Mandates Boosting Biodegradable Sponges

- 4.3 Market Restraints

- 4.3.1 Shift toward Minimally Invasive / Hemostatic Substitutes

- 4.3.2 Regulatory & Compliance Burden

- 4.3.3 Cotton-Price Volatility & Supply-Chain Disruptions

- 4.3.4 Data-Privacy Concerns Slowing RFID Uptake

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Radiopaque Laparotomy Sponges

- 5.1.2 Traditional (Conventional) Sponges

- 5.1.3 RFID-enabled Laparotomy Sponges

- 5.2 By Material

- 5.2.1 Cotton

- 5.2.2 Rayon / Viscose

- 5.2.3 Non-Woven & Synthetic Blends

- 5.2.4 Antimicrobial / Biodegradable Composites

- 5.3 By Sterility

- 5.3.1 Sterile

- 5.3.2 Non-sterile

- 5.4 By End-User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory Surgical Centers (ASCs)

- 5.4.3 Specialty Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of MEA

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 A Plus International

- 6.3.2 ACTIMED

- 6.3.3 AdvaCare Pharma

- 6.3.4 Allmed Medical Products

- 6.3.5 B. Braun Melsungen AG

- 6.3.6 Cardinal Health

- 6.3.7 DeRoyal Industries

- 6.3.8 Dukal LLC

- 6.3.9 Dynarex Corporation

- 6.3.10 Haldor Advanced Technologies

- 6.3.11 Integra LifeSciences

- 6.3.12 Johnson & Johnson (Ethicon)

- 6.3.13 Medical Action Industries

- 6.3.14 Medline Industries

- 6.3.15 Medtronic plc

- 6.3.16 Molnlycke Health Care

- 6.3.17 Owens & Minor

- 6.3.18 Premier Enterprises

- 6.3.19 Smith & Nephew

- 6.3.20 Solventum Corporation

- 6.3.21 Stryker Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment