|

시장보고서

상품코드

2063678

AI 기반 의약품 공급망 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI Enabled Pharma Supply Chain - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

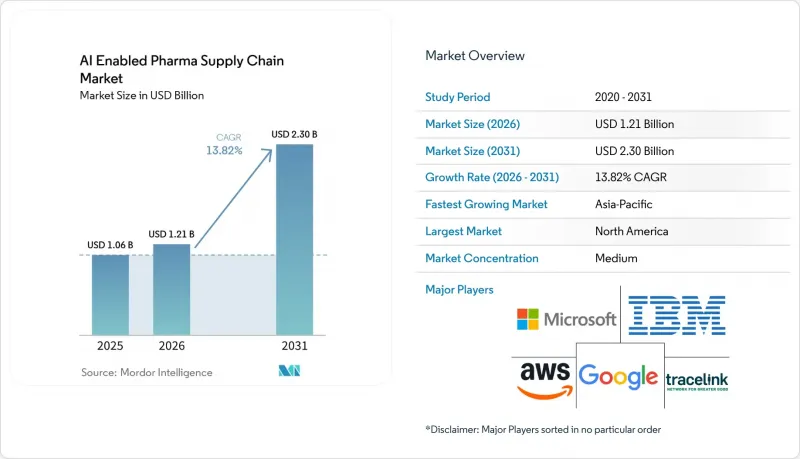

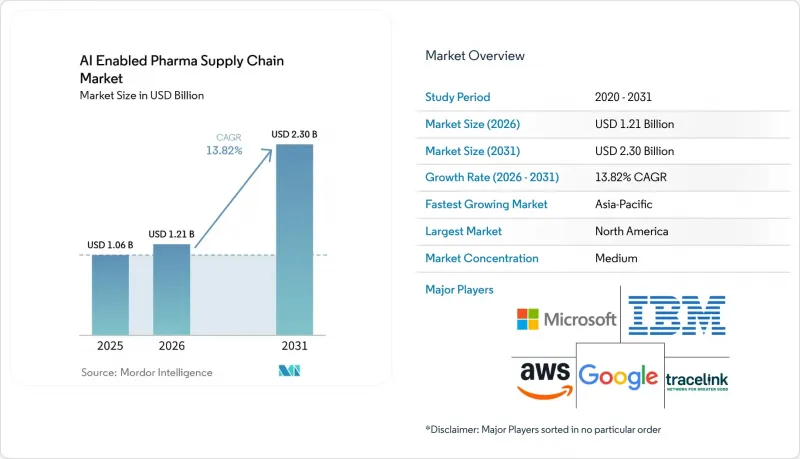

Mordor Intelligence에 의하면, AI 기반 의약품 공급망 시장 규모는 2025년 10억 6,000만 달러로 평가되었습니다. 2026년 12억 1,000만 달러에서 2031년까지 23억 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 13.82%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어, 서비스, 플랫폼/AI 모델), 용도( 수요 예측·계획, 물류·유통 관리 등), 배포 방식(클라우드 기반 등), 최종 사용자(제약 회사, 생명공학 기업 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계의 AI 기반 의약품 공급망 시장 동향 및 인사이트

예측형 공급망 관리에 대한 수요 증가

각 제약사는 임상시험 피험자 등록 현황, 보험 적용 의약품 목록 업데이트, 기상 데이터 등을 통합하여 향후 18개월까지 수요를 예측하는 상시 가동형 시스템으로 기존의 월별 계획 주기를 대체하고 있습니다. 머크사가 5년간 10억 달러를 투자해 추진하는 Vertex AI 도입은 안전 재고를 30% 줄이고, 파이프라인 인수를 위한 자금을 확보하는 것을 목표로 하고 있습니다. 상위 20개 기업의 경우, 재고율이 1% 상승할 때마다 2억-3억 달러의 운전자금이 묶이게 되므로, 예측의 정확도는 매우 중요합니다. AI를 통한 예측 정확도가 15-25포인트 향상되면, 30억-50억 달러의 자금이 확보되어 배당금 증액에 활용할 수 있게 됩니다. 2026년 1월 FDA 및 EMA의 지침에 따라 문서화 관련 요건이 명확해졌으며, 품질 관리 팀은 보충 워크플로우를 자동화할 법적 근거를 확보했습니다. 조기 도입 기업들로부터 이미 리드타임이 8-10일 단축되었습니다는 보고가 들어왔으며, 온도 관리가 필요한 항암제의 서비스 수준이 향상되고 있습니다.

세계 의약품 유통 네트워크의 복잡화

‘차이나 플러스 원’ 전략에 따라 원료의 조달처가 인도, 베트남, 멕시코로 분산되면서, 브랜드 소유자는 더 많은 공급업체를 관리할 수밖에 없게 되었습니다. IBM Watsonx는 87개국에서 230만 개의 의약품 SKU를 추적하여, 수출 허가 지연이나 항만 혼잡을 14일 전에 감지함으로써 기업이 사전에 승인된 대체품으로 전환할 수 있도록 지원합니다. 인도 전역에 위치한 1,300개 이상의 세계 역량 센터는 지역별 고유한 수요 모델에 대한 정보를 제공하고, 불투명한 유통업체의 판매 데이터를 가시화합니다. 브라질과 아르헨티나의 CMO(수탁 제조업체)는 AI 조달 엔진을 활용하여 분기 내 20%나 변동하는 원자재 비용의 원인이 되는 환율 변동 위험을 헤지하고 있습니다. 물류 경로가 길어질수록 가시성 부족이 위험을 가중시키고 있습니다. 실시간 선박 교통 데이터와 통관 신고 정보를 결합한 예측 ETA(예정 도착 시각) 도구를 통해 일정 준수율이 11-15% 향상됩니다. 이러한 변화로 인해, 분단된 지역 전체에 걸쳐 종단 간 투명성을 제공해야 한다는 AI 기반 의약품 공급망 시장에 대한 기본적인 수요가 높아지고 있습니다.

높은 도입 비용과 통합의 복잡성

매출액이 5억-30억 달러인 중견 기업들은 매출액의 약 3%를 IT 예산으로 편성하고 있지만, AI 플랫폼을 전면 도입하는 데는 1,500만-2,500만 달러의 비용이 소요될 수 있습니다. TraceLink의 2026년 조사에 따르면, 경영진의 68%가 통합을 가장 큰 장애물로 보고 있습니다. 그 이유는 각 API 인터페이스에 400-600시간의 엔지니어링 작업이 필요하고, GMP 검증으로 인해 가동 시작이 9개월 늦어지기 때문입니다. 순이익률이 12% 미만인 CMO(수탁 제조업체)는 수요 예측과 같이 영향력이 큰 단일 이용 사례에 특화된, 모듈식 ‘소규모로 시작할 수 있는’ 키트를 공급업체가 제공할 때까지 AI 도입을 미루는 경우가 많습니다. 1990년대의 레거시 ERP 시스템은 최신 REST 커넥터를 지원하지 않는 맞춤형 코드를 포함하고 있어 상황을 복잡하게 만들고 있습니다. 자본예산위원회는 24개월 이내에 투자 회수를 요구하고 있으며, 공급업체들은 성과 기반 가격 책정을 강요받고 있습니다. 이러한 현실로 인해 단기적인 지출은 억제되고 있지만, 도입 사례가 늘어남에 따라 위험에 대한 우려는 줄어들고 있으며, AI 기반 의약품 공급망 업계에서는 도입이 확대되고 있습니다.

부문별 분석

플랫폼과 AI 모델은 2031년까지 연평균 성장률(CAGR) 14.71%를 기록하며 성장할 것으로 예상되며, 이는 다른 모든 구성 요소를 상회할 전망입니다. 이 소프트웨어는 확고히 자리 잡은 도입 기반을 바탕으로 2025년에는 63.45%의 시장 점유율을 차지했습니다. Blue Yonder는 2026년에 자율형 에이전트를 도입하여, 이미 37개 물류 센터에 걸쳐 재고 관리를 수행하고 있습니다.

NVIDIA가 지원하는 GPU 시뮬레이션을 통해 Kinaxis는 2시간 만에 1만 건의 혼란 시나리오를 모델링할 수 있습니다. EU AI법의 투명성 테스트를 통과하는 ‘설명 가능한 AI’에 대한 수요가 높아짐에 따라, 블랙박스형 룰 엔진에서 업그레이드하는 움직임이 활발해지고 있습니다. 제약 기업들이 검증된 인프라를 기반으로 모델 튜닝을 외부에 위탁하고 있기 때문에 서비스 수익은 AI 기반 의약품 공급망 시장 전체의 성장률과 비슷한 수준으로 증가하고 있습니다.

유전자·세포 치료의 도입으로 초저온 운송이 3배 증가함에 따라, 콜드체인 모니터링 시장은 2031년까지 연평균 성장률(CAGR) 15.69%를 나타낼 것으로 전망됩니다. 수요 예측에 따르면 2025년 시점에서 AI 기반 의약품 공급망 시장 점유율은 32.48%를 차지했으나, 그 성장세는 정체 국면에 접어들고 있습니다. 엣지 센서는 현재 10초 간격으로 데이터를 예측 모델에 제공하고 있으며, 이를 통해 설비의 가동 중단 시간을 30% 줄이고 냉각 장치의 수명을 2년 연장하고 있습니다.

리스크·혁신 분석 엔진은 시범 운영 단계에서 본격적인 운영 단계로 전환되었으며, 매일 34만 건의 최신 데이터를 수집하여 공급업체의 취약성을 평가했습니다. 물류 최적화를 통해 15분 단위로 배송 시간대를 예측함으로써, 긴급 화물의 비용을 18-25% 절감하고 있습니다. 이러한 연쇄적인 활용 사례를 통해, AI 기반 의약품 공급망 시장은 현실 세계의 충격에 대응하며 그 적용 범위를 지속적으로 확대되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 38.51%를 차지했습니다. 이는 조기 도입 사례와 AI 검증 기준을 명확히 한 2026년 1월 FDA·EMA 지침을 반영한 것입니다. 머크의 10억 달러 규모 Vertex AI 도입, 예측 정확도를 92%로 높여 재고 부족을 35% 줄인 맥케슨의 IBM WatsonX 수요 예측 엔진 등은 해당 지역의 규모를 보여주는 대표적인 사례입니다. 캐나다에서는 AI를 활용해 각 주의 처방집 간 차이를 조정하고 있는 반면, 멕시코의 CMO(수탁 제조업체)는 AI 품질 관리 도구를 도입하여 미국 브랜드를 위한 니어쇼어 공급 체제를 강화하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 18.25%를 나타낼 것으로 예측되며, 이는 다른 어떤 지역보다도 높은 수치입니다. 인도 전역에 1,300곳 이상에 위치한 세계 역량 센터들은 AI 인재를 AI 기반 의약품 공급망 시장에 투입하여, 수출업체들이 54가지의 다양한 추적성 규제를 준수할 수 있도록 지원하고 있습니다. ‘차이나 플러스 원’에 따른 다각화로 인해 API(원료의약품) 생산이 베트남과 인도네시아로 이동하고 있으며, 2차 공급업체의 40%가 여전히 스프레드시트를 사용하고 있는 상황에서 실시간 가시화 플랫폼의 도입이 요구되고 있습니다. 일본에서 On-Premise 전환이 의무화됨에 따라, 지출은 국내 데이터센터로 향하고 있습니다. 한편, 호주에서는 AI 기반 규제 시범 사업을 통해 승인 주기가 9개월로 단축되었습니다.

Annex 22 및 GDPR(EU 개인정보보호규정)의 현지화로 인해 도입 시마다 300만-600만 달러의 추가 비용이 발생하고 있어, 설명 가능한 On-Premise형 솔루션의 도입이 촉진되고 있습니다. 독일, 영국, 프랑스, 이탈리아, 스페인은 해당 지역의 의약품 생산량의 65%를 차지했으며, 이들 국가의 제조업체들은 엄격하게 검증된 샌드박스 환경 내에서 자율적인 재고 보충 시범 테스트를 실시했습니다. 사우디아라비아와 아랍에미리트(UAE)의 현지화 프로그램이 주도하는 중동과, 브라질의 전자처방전 의무화에 힘입어 성장하는 남미가 신흥 추격 시장을 형성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the aI enabled pharma supply chain market size is projected to expand from USD 1.06 billion in 2025 and USD 1.21 billion in 2026 to USD 2.30 billion by 2031, registering a CAGR of 13.82% between 2026 to 2031.

This report is Segmented by Component (Software, Services, and Platforms / AI Models), Application (Demand Forecasting & Planning, Logistics & Distribution Management, and More), Deployment (Cloud-Based, and More), End-User (Pharmaceutical Companies, Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasted in Terms of Value (USD).

Global AI Enabled Pharma Supply Chain Market Trends and Insights

Rising Demand for Predictive Supply-Chain Management

Pharmaceutical companies are replacing monthly planning cycles with always-on engines that forecast demand 18 months ahead, blending clinical-trial enrollment signals, payer formulary updates, and weather data. Merck's five-year, USD 1 billion Vertex AI rollout aims to trim safety stock 30%, freeing cash for pipeline acquisitions. An extra percentage point of inventory ties up USD 200-300 million in working capital at a top-20 firm, so precision matters. AI-driven forecast accuracy gains of 15-25 points unlock USD 3-5 billion that can fund dividend increases. The January 2026 FDA-EMA principles clarified documentation expectations, giving quality teams the legal cover to automate replenishment workflows. Early adopters already report 8-10 day lead-time reductions, improving service levels for temperature-sensitive oncology drugs.

Growing Complexity of Global Pharmaceutical Distribution Networks

China-plus-one strategies now split active-ingredient sourcing across India, Vietnam, and Mexico, forcing brand owners to manage more suppliers. IBM Watsonx tracks 2.3 million pharmaceutical SKUs in 87 countries and flags export-license delays or port congestion 14 days early, letting firms switch to pre-qualified alternates. India's 1,300+ global capability centers feed region-specific demand models that surface opaque distributor sales data. Brazil and Argentina CMOs employ AI procurement engines to hedge currency swings that shift input costs 20% within a quarter. As logistics corridors stretch, visibility gaps amplify risk; predictive ETA tools that combine real-time vessel traffic with customs filings improve schedule adherence by 11-15%. These shifts raise the baseline need for the AI enabled pharma supply chain market to deliver end-to-end transparency across fragmented geographies.

High Implementation Cost and Integration Complexity

Mid-tier companies with USD 500 million-USD 3 billion in revenue run IT budgets near 3% of revenue, yet full AI platform rollouts can cost USD 15-25 million. TraceLink's 2026 survey reported 68% of executives view integration as the primary barrier, because each API interface needs 400-600 engineering hours and GMP validation that drags go-live by nine months. CMOs with net margins below 12% often defer AI until vendors offer modular "start small" kits focused on one high-impact use case, such as demand sensing. Legacy ERP instances from the 1990s complicate matters with customized code that resists modern REST connectors. Capital budgeting committees demand payback within 24 months, forcing suppliers to provide outcome-based pricing. These realities temper near-term spending, although as more reference sites emerge, perceived risk declines and the AI enabled pharma supply chain industry broadens adoption.

Other drivers and restraints analyzed in the detailed report include:

- Need for Cost Optimization and Operational Efficiency

- Rapid Digitalization of Pharma Operations

- Data Privacy, Compliance and Regulatory Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platforms and AI models will grow at 14.71% CAGR through 2031, outpacing every other component. Software captured 63.45% share in 2025 because of the entrenched installed base. Blue Yonder added autonomous agents in 2026 that already manage inventory across 37 distribution centers.

NVIDIA-backed GPU simulation lets Kinaxis model 10,000 disruption scenarios in two hours. Demand for explainable AI that passes EU AI Act transparency tests is driving upgrades away from black-box rules engines. Services revenues are rising at the broader AI enabled pharma supply chain market growth rate because drug makers outsource model tuning on validated infrastructure.

Cold-chain monitoring is forecast to post 15.69% CAGR through 2031 as gene and cell-therapy launches triple ultra-cold shipments. Demand-forecasting retained 32.48% of the AI enabled pharma supply chain market share in 2025, though its growth is plateauing. Edge sensors now feed 10-second interval data to predictive models that cut equipment downtime 30% and extend chiller life by two years.

Risk-and-disruption engines are graduating from pilot to production, ingesting 340,000 fresh data points daily to score supplier vulnerabilities. Logistics optimization saves 18-25% in expedited freight by forecasting delivery windows within 15 minutes. These cascading use cases ensure the AI enabled pharma supply chain market continues widening its application stack in response to real-world shocks.

Geography Analysis

North America commanded 38.51% of global revenue in 2025, reflecting early mover deployments and the January 2026 FDA-EMA principles that clarified AI validation. Merck's USD 1 billion Vertex AI roll-out and McKesson's IBM WatsonX demand engine, which improved forecast accuracy to 92% and cut stock-outs 35%, exemplify the region's scale. Canada uses AI to balance provincial formulary nuances, while Mexican CMOs employ AI quality tools to strengthen nearshore supply for U.S. brands.

Asia-Pacific is projected to grow at 18.25% CAGR, outstripping every other region. India's 1,300+ global capability centers funnel AI talent into the AI enabled pharma supply chain market, helping exporters satisfy 54 diverse serialization regimes. China-plus-one diversification pushes API work to Vietnam and Indonesia, compelling real-time visibility platforms where 40% of tier-2 vendors still use spreadsheets. Japan's on-premise mandates channel spending into sovereign data centers, while Australia's AI-assisted regulatory pilots shorten approval cycles to nine months

Annex 22 and GDPR localization add USD 3-6 million per roll-out, incentivizing explainable on-premise solutions. Germany, the United Kingdom, France, Italy, and Spain control 65% of regional pharmaceutical output, and manufacturers there are pilot-testing agentic replenishment within tightly validated sandboxes. The Middle East, spearheaded by Saudi and UAE localization programs, and South America, driven by Brazil's e-prescribing mandate, round out emerging catch-up markets.

- Accenture

- Amazon Web Services (AWS)

- Blue Yonder

- Cognizant

- Coupa Software / Llamasoft

- DHL Supply Chain

- Google Cloud

- IBM

- Infor

- Kinaxis

- Manhattan Associates

- Microsoft

- NVIDIA

- O9 Solutions

- OPTEL Group

- Oracle

- SAP

- SAS Institute

- TraceLink

- Zebra Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Predictive Supply-Chain Management

- 4.2.2 Growing Complexity of Global Pharmaceutical Distribution Networks

- 4.2.3 Need for Cost Optimization and Operational Efficiency

- 4.2.4 Rapid Digitalization of Pharma Operations

- 4.2.5 AI-Driven Sustainability Mandates

- 4.2.6 Oncology Cold-Chain Precision via Edge-AI Sensors

- 4.3 Market Restraints

- 4.3.1 High Implementation Cost and Integration Complexity

- 4.3.2 Data Privacy, Compliance and Regulatory Constraints

- 4.3.3 Scarcity of Annotated GMP-Grade Supply-Chain Datasets

- 4.3.4 Model Drift Risk Amid Volatile Demand Shocks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Platforms / AI Models

- 5.2 By Application

- 5.2.1 Demand Forecasting & Planning

- 5.2.2 Logistics & Distribution Management

- 5.2.3 Cold-Chain Monitoring

- 5.2.4 Risk & Disruption Management

- 5.2.5 Others

- 5.3 By Deployment

- 5.3.1 Cloud-based

- 5.3.2 On-premise

- 5.3.3 Hybrid

- 5.4 By End-User

- 5.4.1 Pharmaceutical Companies

- 5.4.2 Biotechnology Companies

- 5.4.3 Contract Manufacturing Organizations (CMOs)

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Accenture

- 6.3.2 Amazon Web Services (AWS)

- 6.3.3 Blue Yonder

- 6.3.4 Cognizant

- 6.3.5 Coupa Software / Llamasoft

- 6.3.6 DHL Supply Chain

- 6.3.7 Google Cloud

- 6.3.8 IBM

- 6.3.9 Infor

- 6.3.10 Kinaxis

- 6.3.11 Manhattan Associates

- 6.3.12 Microsoft

- 6.3.13 NVIDIA

- 6.3.14 O9 Solutions

- 6.3.15 OPTEL Group

- 6.3.16 Oracle

- 6.3.17 SAP SE

- 6.3.18 SAS Institute

- 6.3.19 TraceLink

- 6.3.20 Zebra Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment