|

시장보고서

상품코드

2063825

디지털 의약품 공급망 관리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Digital Pharmaceutical Supply Chain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

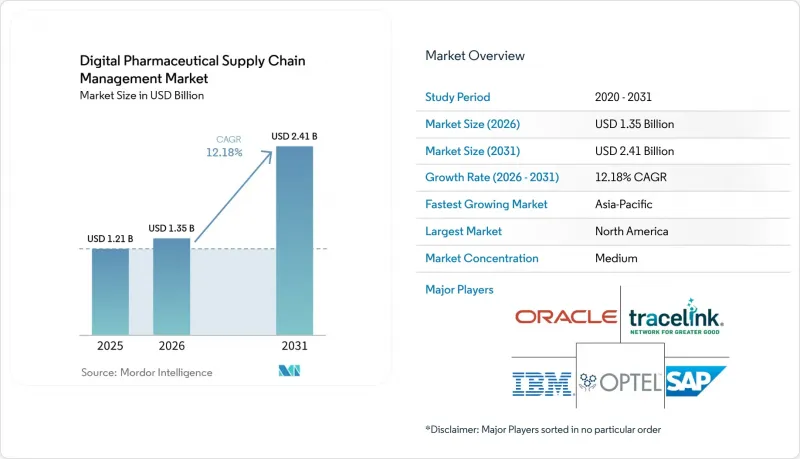

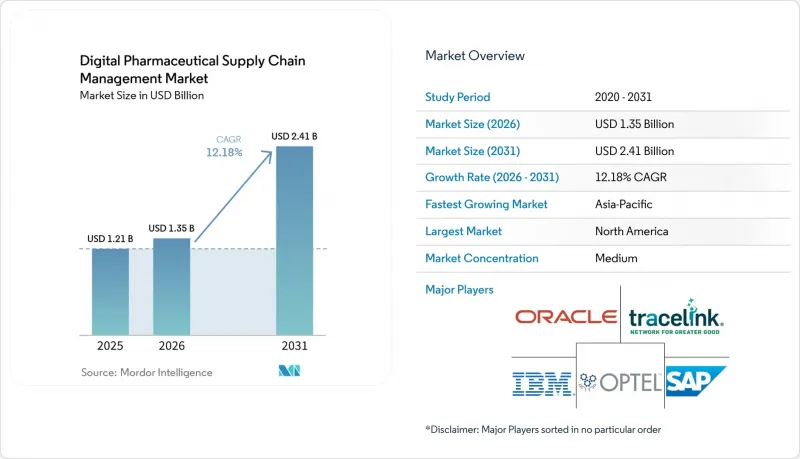

Mordor Intelligence에 의하면, 디지털 의약품 공급망 관리 시장 규모는 2025년에 12억 1,000만 달러로 평가되었습니다. 2026년 13억 5,000만 달러에서 2031년까지 24억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 12.18%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어, 서비스, 하드웨어), 용도(재고·창고 관리 등), 배포 방식(클라우드 기반 등), 기술(RFID·2차원 바코드 등), 서비스 유형(도입·통합 등), 최종 사용자(제약 회사 등) 및 지역별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 산출되었습니다.

세계의 디지털 의약품 공급망 관리 시장 동향 및 인사이트

의약품 일련번호 부여 및 추적·추적 가능성 관련 규제 강화

세계 각국의 규제 당국은 단위별 일련번호 부여 규정을 강화하고 있으며, 제조업체와 유통업체는 2027년 11월 DSCSA 상호운용성 기한까지 기존의 추적성 플랫폼을 클라우드 기반이며 GS1 표준을 준수하는 솔루션으로 업그레이드해야 합니다. 2025년, TraceLink의 보고서에 따르면 323개의 수탁 제조 기업이 EPCIS 테스트를 적극적으로 실시했으며, 100개사가 실제 운영이 가능한 단계에 도달했는데, 이는 업계 전반에 걸쳐 표준화된 파트너 온보딩을 향한 급속한 움직임을 보여주었습니다. SAP와 Oracle은 각각의 시리얼화 제품군과 관련해 여러 건의 조기 도입 계약을 체결했습니다. 이는 기업들이 독자적인 바코드에서 2차원 데이터 매트릭스로 전환하는 과정에서 기업 소프트웨어의 교체 주기가 도래했음을 보여줍니다. 지역별 기준의 차이로 인해 상황이 더욱 복잡해지고 있어, 여러 관할 구역에 걸쳐 사업을 영위하는 유통업체들은 식별자를 실시간으로 전환할 수 있는 멀티테넌트형 플랫폼을 도입해야 하는 상황에 직면해 있습니다. 또한, 도매업체들이 브랜드 소유자와의 관계를 유지하기 위해 유통 계약에 추적 및 추적 가능성 기능을 직접 포함시킴으로써 수직 통합이 가속화되고 있습니다.

클라우드 네이티브이자 AI 주도형 공급망 오케스트레이션

제약 기업들은 계획 및 실행 업무 부하를 On-Premise ERP 시스템에서 수요 예측 및 재고 최적화에 머신러닝을 도입한 유연한 클라우드 플랫폼으로 이전하고 있습니다. 사노피의 AI 기반 도구는 80%의 정확도로 재고 부족을 감지함으로써, 2025년에 3억 달러 규모의 매출 손실 위험을 방지하고 긴급 운송 비용을 최대 28% 절감했습니다. 화이자는 디지털 트윈을 활용하여 물리적 확장을 하지 않고도 300만 회분 이상의 추가 투여량을 확보했습니다. 로슈는 NVIDIA의 GPU와 ‘Lab-in-the-Loop’ 워크플로를 결합하여 제조 공정을 시뮬레이션하고, 고성능 컴퓨팅이 필요한 공장으로의 전환을 보여주었습니다. 아스트라제네카의 ‘AskAZ’와 같은 생성형 AI 도구는 2025년에 수동으로 진행되는 검사 의뢰 조정 업무를 3만 시간 절감하고, 대화형 에이전트를 통해 조달 주기를 당일 처리로 단축할 수 있음을 보여주었습니다. 환자 맞춤형 세포 및 유전자 치료의 경우, SAP의 오케스트레이션 및 릴리스 기능을 통해 아페레시스 예약, 바이러스 벡터 처리, 그리고 병원에서의 정맥 주입이 일관된 관리 체계를 따라 조정되게 되었습니다.

높은 통합 비용과 변경 관리 비용

기존의 제조 실행 시스템에서 클라우드 스택으로의 전환에는 500만-5,000만 달러의 비용이 소요될 수 있으며, FDA 21 CFR Part 11 및 EU Annex 11에 따른 검증 주기는 18-36개월에 달할 전망입니다. Chanelle Pharma는 S/4HANA로 업그레이드하는 기간 동안 14개월간의 병행 운영을 예상하고 있으며, 이는 중소규모 기업이 감당해야 할 운영 리스크의 부담을 여실히 보여주고 있습니다. CMO(수탁 제조업체)는 각각 고유한 집계 계층을 가진 수십 개의 브랜드 소유자와의 연계 관계를 유지해야 하기 때문에 불균형한 부담을 안고 있습니다. 이러한 압박으로 인해 턴키 방식의 EPCIS 준수 솔루션을 제공하는 경쟁사들에게 수주를 빼앗기는 소규모 CMO들이 도태되면서, 업계 재편이 진행되고 있습니다. TraceLink, Optel, Korber의 종량제 요금 체계는 통합 비용을 거래량에 분산시켜 자본 부담을 경감시키는 한편, 외부 위탁 업체에 대한 의존도를 높이고 있습니다.

부문별 분석

2025년, 소프트웨어는 디지털 의약품 공급망 관리 시장 점유율의 56.81%를 차지했습니다. 이는 기업들이 전 세계 데이터 거주 규정을 준수하면서도 다양한 기능을 갖춘 직렬화 제품군을 선호했기 때문입니다. 서비스 부문은 규모는 작지만 연평균 성장률(CAGR) 14.57%로 성장하고 있으며, 공급업체들이 하드웨어, 라이선싱, 변경 관리를 단일 단가 요금제로 통합하고 있기 때문에 2031년까지 디지털 의약품 공급망 관리 시장 규모에서 점유율을 확대할 것으로 전망됩니다. 하드웨어 부문은 뒤처져 있지만, 실시간 콜드체인 데이터를 클라우드 대시보드로 전송하는 임베디드형 IoT 센서의 이점을 누리고 있으며, 이를 통해 품질 저하의 위험을 최소화하고 있습니다.

SAP, Oracle, IBM은 이상 감지 및 예측 유지보수를 도입하는 클라우드 네이티브 방식으로 소프트웨어를 전환하고 있습니다. 한편, TraceLink는 99.9%의 가동률을 보장하는 SLA를 관리형 계약에 포함시켜 제약사의 사이버 책임 부담을 덜어주고 있습니다. 하드웨어의 발전은 Cryoport의 파리 센터와 같은 극저온 보관 시설을 중심으로 집중되고 있으며, 다수의 센서가 장착된 냉동고가 5분 간격으로 원격 측정 데이터를 전송하고 있습니다. 이러한 변화는 자본 구매에서 제품 출하량에 따라 규모가 조정되는 종량제 서비스로의 장기적인 전환을 보여줍니다.

재고 및 창고 관리는 2025년 매출의 27.47%를 차지했으나, 의약품 추적성 및 일련번호 부여는 연평균 성장률(CAGR) 13.28%를 기록하며, 2026년부터 2031년까지 디지털 의약품 공급망 관리 시장 규모 내에서 가장 빠르게 성장할 분야가 될 것으로 전망됩니다. 수송 모듈은 바이오의약품 콜드체인 수요의 수혜를 입고 있는 반면, AI 기반 수요 계획 엔진은 사노피의 비용 절감 사례를 계기로 경영진의 주목을 받고 있습니다.

시리얼화의 급속한 확대는 기업들이 독자적인 전자 페디그리 도구를 폐지하고 GS1 데이터 매트릭스 및 EPCIS 1.2 프로세스를 채택하는 등, 일시적인 규정 준수상의 변화를 반영하고 있습니다. 각 벤더사는 도입 속도를 놓고 경쟁하고 있으며, TraceLink는 CMO 파트너의 출범 기간을 6개월로 단축하고 있습니다. 현재 창고 솔루션에는 실시간 주문 대기열에 대응하는 동적 슬롯 배정 알고리즘이 탑재되어 있지만, 운송 모듈은 Controlant Saga 카드를 통한 분 단위 온도 가시화 기능으로 차별화를 꾀하고 있습니다.

지역별 분석

북미는 2025년 매출의 36.65%를 차지하며, DSCSA 시행과 더불어 136억 달러 규모의 의약품 IT 지출에 힘입어 디지털 의약품 공급망 관리 시장의 핵심 축으로 자리매김했습니다. IBM의 Pulse는 이미 연간 100만 건 이상의 검증 요청을 처리하고 있으며, TraceLink의 CMO 네트워크는 이 지역에서의 선도적 입지를 확고히 하고 있습니다. 니어쇼어링을 통해 캐나다와 멕시코에 대한 투자가 확대되는 한편, Energize의 전력 구매 계약과 같은 ESG 관련 자금 조달이, 자금 조달 결정 시 지속가능성 지표를 중시하는 추세를 뒷받침하고 있습니다.

아시아태평양은 16.59%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있으며, 화이자 우한, 다케다 오사카, 삼성바이오로직스 마츠시마의 대형 바이오의약품 프로젝트가 이를 주도하고 있습니다. 인도의 30억 달러 규모의 인센티브 사업에 더해, 일본 내 On-Premise 도입에 대한 선호도가 해당 지역의 도입 형태를 형성하고 있습니다. 크라이오제닉 네트워크는 확대되는 세포 치료 거점 네트워크에 대응하기 위해 확장을 진행 중이며, 크라이오포트와 월드 쿠리어는 싱가포르와 멜버른에 물류 센터를 신설하고 있습니다.

유럽은 ‘중요 의약품법’ 및 ‘위조 의약품 지침’의 혜택을 받아 큰 시장 점유율을 차지하는 한편, 데이터 거주 요건을 충족하기 위해 하이브리드형 사업 전개를 지향하고 있습니다. 노보노르디스크, 사노피, 아스트라제네카는 총 100억 달러 이상을 생산 능력 확충에 투자한 반면, 은행들은 지역 회복탄력성을 강화하기 위해 이집트와 사우디아라비아의 그린 창고에 자금을 지원하고 있습니다. 남미에서는 ANVISA가 일련번호 코드를 미국 및 유럽연합의 체계에 부합하도록 조정함으로써 진전이 보이고 있지만, 통합 비용이라는 장벽으로 인해 도입 속도는 더딘 임베디드니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the digital pharmaceutical supply chain management market size was valued at USD 1.21 billion in 2025 and is estimated to grow from USD 1.35 billion in 2026 to reach USD 2.41 billion by 2031, at a CAGR of 12.18% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Services, and Hardware), Application (Inventory & Warehouse Management, and More), Deployment (Cloud-Based, and More), Technology (RFID & 2D Barcoding, and More), Service Type (Implementation & Integration, and More), End User (Pharmaceutical Companies, and More), and Geography. The Market and Forecasted in Terms of Value (USD).

Global Digital Pharmaceutical Supply Chain Management Market Trends and Insights

Rising Pharmaceutical Serialization & Track-and-Trace Mandates

Global regulators are tightening unit-level serialization rules, compelling manufacturers and distributors to upgrade legacy pedigree platforms to cloud-ready, GS1-compliant solutions before the November 2027 DSCSA interoperability deadline. In 2025, TraceLink reported that 323 contract manufacturing organizations were in active EPCIS testing, while 100 reached production-ready status, signaling an industry-wide sprint toward standardized partner onboarding. SAP and Oracle secured multiple early adopter contracts for their serialization suites, marking an enterprise software replacement cycle as firms abandon proprietary barcodes for 2D data matrices. Divergent regional standards intensify complexity, prompting distributors that span multiple jurisdictions to adopt multi-tenant platforms able to switch identifiers in real time. Vertical integration is accelerating as wholesalers embed track-and-trace capabilities directly into distribution agreements to retain brand-owner relationships.

Cloud-Native & AI-Driven Supply-Chain Orchestration

Pharmaceutical companies are shifting planning and execution workloads from on-premise ERP stacks to elastic cloud platforms that infuse machine learning into demand forecasting and inventory optimization. Sanofi's AI-enabled tool averted USD 300 million in revenue risk in 2025 by flagging low-stock events with 80% accuracy, cutting expedited freight costs by up to 28%. Pfizer used a digital twin to unlock more than 3 million extra doses without brick-and-mortar expansion. Roche paired NVIDIA GPUs with lab-in-the-loop workflows to simulate manufacturing steps, signaling a pivot toward compute-rich factories. Generative AI tools such as AstraZeneca's AskAZ cut manual lab-request coordination by 30,000 hours in 2025, showing that conversational agents can collapse procurement cycles into a same-day activity. For patient-specific cell-and-gene therapies, SAP's orchestration release now coordinates apheresis bookings, viral vector runs, and hospital infusions along a contiguous chain of custody.

High Integration & Change-Management Costs

Moving from legacy manufacturing execution systems to cloud stacks can cost between USD 5 million and USD 50 million, with validation cycles stretching 18-36 months under FDA 21 CFR Part 11 and EU Annex 11. Chanelle Pharma expects 14 months of dual-run operations during its S/4HANA upgrade, illustrating the operational risk burden on smaller firms. CMOs shoulder an asymmetric load because they must keep interfaces live for dozens of brand owners, each with its own aggregation hierarchy. This pressure triggers consolidation as sub-scale CMOs lose bids to rivals offering turnkey EPCIS compliance. Consumption-based pricing from TraceLink, Optel, and Korber spreads integration costs across transaction volumes, easing capital strain but increasing dependency on outsourced operators.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Biologics, Cell-&-Gene Therapies Requiring Cold-Chain

- Surge in DSCSA Interoperability & EPCIS 1.2 Deployments

- Cyber-Security Risk in Connected Logistics Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 56.81% digital pharmaceutical supply chain management market share in 2025 as enterprises favored feature-rich serialization suites that comply with global data-residency rules. Services, though smaller, are advancing at a 14.57% CAGR and are projected to account for a growing slice of the digital pharmaceutical supply chain management market size by 2031 because vendors roll hardware, licenses, and change-management into single per-unit fees. Hardware trails yet gains from embedded IoT sensors that feed real-time cold-chain data to cloud dashboards, minimizing spoilage risk.

SAP, Oracle, and IBM are steering software toward cloud-native formats that deploy anomaly detection and predictive maintenance, while TraceLink bundles 99.9% uptime SLAs into managed contracts, shifting cyber-liability away from drug makers. Hardware growth clusters around cryogenic depots like Cryoport's Paris center, where sensor-rich freezers stream telemetry at five-minute intervals. The divergence signals a long-term migration from capital purchases to pay-as-you-go services that scale with product volumes.

Inventory and warehouse management held 27.47% of 2025 revenues, yet drug traceability and serialization are forecast to log a 13.28% CAGR and become the fastest-growing slice of the digital pharmaceutical supply chain management market size between 2026 and 2031. Transportation modules benefit from biologics cold-chain demand, while AI-driven demand-planning engines secure executive attention after Sanofi's cost-avoidance case study.

The serialization boom reflects a one-time compliance shock as firms scrap proprietary e-pedigree tools in favor of GS1 DataMatrix and EPCIS 1.2 flows. Vendors compete on onboarding speed, with TraceLink cutting CMO partner ramp-up windows to six months. Warehouse solutions now embed dynamic slotting algorithms that adapt to real-time order queues, whereas transportation modules differentiate on minute-by-minute temperature visibility via Controlant Saga cards.

Geography Analysis

North America held 36.65% of 2025 revenue and remains the anchor of the digital pharmaceutical supply chain management market due to DSCSA enforcement plus USD 13.6 billion in pharma IT outlays. IBM's Pulse already fields more than 1 million verification calls annually and TraceLink's CMO network solidifies the region's leadership. Near-shoring pushes investments into Canada and Mexico, while ESG-linked financing, such as Energize's power purchase pact, drives sustainability metrics into sourcing decisions.

Asia-Pacific delivers the fastest CAGR at 16.59%, led by large-ticket biologics projects from Pfizer Wuhan, Takeda Osaka, and Samsung Biologics Songdo. India's USD 3 billion incentive pipeline plus Japan's preference for on-premise execution shapes the regional deployment mix. Cryogenic networks expand to service growing cell-therapy corridors, with Cryoport and World Courier adding depots in Singapore and Melbourne.

Europe benefits from the Critical Medicines Act and Falsified Medicines Directive, posting a significant share while leaning toward hybrid deployments to meet data-residency rules. Novo Nordisk, Sanofi, and AstraZeneca pour more than USD 10 billion combined into capacity, while banks finance green warehouses in Egypt and Saudi Arabia to shore up regional resiliency. South America edges forward as ANVISA aligns serialization codes with United States and European Union frameworks, though adoption pace lags due to integration cost barriers.

- Antares Vision Group

- Arvato Supply Chain Solutions

- AVERY DENNISON

- Blue Yonder Group, Inc.

- Cardinal Health

- Exostar, LLC

- Global Healthcare Exchange, LLC (GHX)

- IBM

- Infor Global Solutions

- Kinaxis Inc.

- Korber Pharma Software GmbH

- Manhattan Associates, Inc.

- Mckesson

- Optel Group

- Oracle

- project44, Inc.

- SAP

- Tecsys Inc.

- TraceLink, Inc.

- UPS Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Pharmaceutical Serialization & Track-and-Trace Mandates

- 4.2.2 Cloud-Native & AI-driven Supply-Chain Orchestration

- 4.2.3 Growth of Biologics, Cell-&-Gene Therapies Requiring Cold-Chain

- 4.2.4 Near-Shoring & Dual-Sourcing of API/finished-Dose Production

- 4.2.5 Surge in DSCSA Interoperability & EPCIS 1.2 Deployments

- 4.2.6 ESG-linked Supply-Chain Financing Incentives

- 4.3 Market Restraints

- 4.3.1 High Integration & Change-Management Costs

- 4.3.2 Multi-Jurisdiction Compliance Complexity

- 4.3.3 Legacy IT & Data-Silo Technical Debt

- 4.3.4 Cyber-Security Risk in Connected Logistics Networks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.2 By Application

- 5.2.1 Inventory & Warehouse Management

- 5.2.2 Drug Traceability & Serialization

- 5.2.3 Transportation & Logistics Management

- 5.2.4 Demand Forecasting & Planning

- 5.2.5 Compliance & Risk Management

- 5.2.6 Others

- 5.3 By Deployment

- 5.3.1 Cloud-based

- 5.3.2 On-premise

- 5.3.3 Hybrid

- 5.4 By Technology

- 5.4.1 RFID & 2D Barcoding

- 5.4.2 IoT Sensors & Edge Devices

- 5.4.3 Blockchain & Distributed Ledger

- 5.4.4 Advanced Analytics & AI/ML

- 5.4.5 Others

- 5.5 By Service Type

- 5.5.1 Implementation & Integration

- 5.5.2 Managed Services

- 5.5.3 Consulting & Training

- 5.5.4 Others

- 5.6 By End User

- 5.6.1 Pharmaceutical Companies

- 5.6.2 Biotechnology Companies

- 5.6.3 Contract Manufacturing Organizations (CMOs)

- 5.6.4 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Antares Vision Group

- 6.3.2 Arvato Supply Chain Solutions

- 6.3.3 Avery Dennison Corporation

- 6.3.4 Blue Yonder Group, Inc.

- 6.3.5 Cardinal Health, Inc.

- 6.3.6 Exostar, LLC

- 6.3.7 Global Healthcare Exchange, LLC (GHX)

- 6.3.8 IBM Corporation

- 6.3.9 Infor Global Solutions

- 6.3.10 Kinaxis Inc.

- 6.3.11 Korber Pharma Software GmbH

- 6.3.12 Manhattan Associates, Inc.

- 6.3.13 McKesson Corporation

- 6.3.14 Optel Group

- 6.3.15 Oracle Corporation

- 6.3.16 project44, Inc.

- 6.3.17 SAP SE

- 6.3.18 Tecsys Inc.

- 6.3.19 TraceLink, Inc.

- 6.3.20 UPS Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment