|

시장보고서

상품코드

2063679

인도의 핵의학 영상 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Nuclear Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

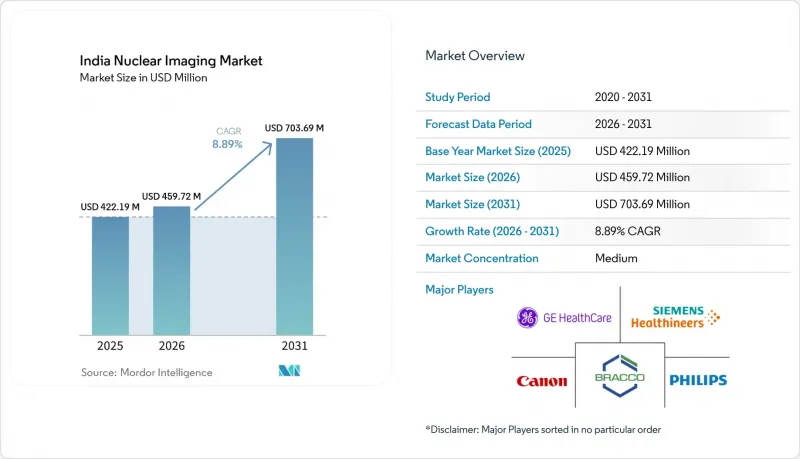

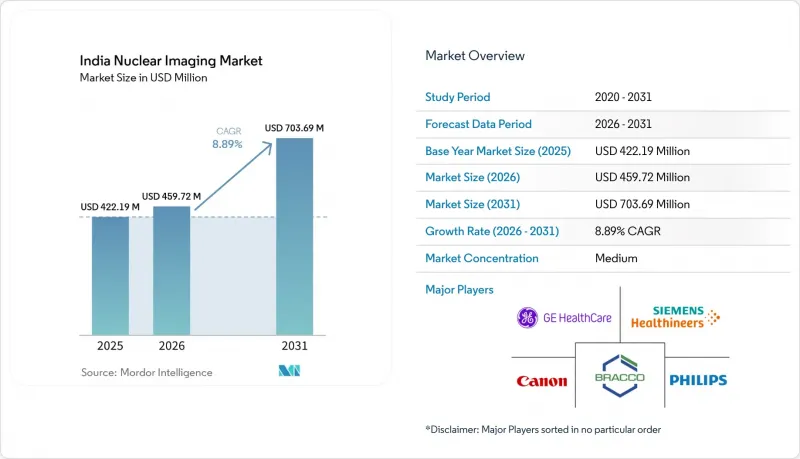

Mordor Intelligence에 의하면, 인도의 핵의학 영상 시장 규모는 2025년 4억 2,219만 달러로 평가되었습니다. 2026년에는 4억 5,972만 달러로 확대되어 2026-2031년 CAGR은 8.89%를 나타내, 2031년까지 7억 369만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품별(장치, 방사성 동위원소(SPECT용 방사성 동위원소(테크네튬-99m(Tc-99m) 등) 및 PET용 방사성 동위원소)), 용도별(심장학, 신경학, 갑상선, 종양학, 기타), 최종 사용자별(병원, 영상진단센터, 학술기관 및 연구기관)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 핵의학 영상 시장 동향 및 인사이트

암 및 심장 질환의 유병률 증가

인도에서는 2024년에 140만 건의 신규 암 사례가 기록되었으며, 국립암등록국은 2025년까지 12.8% 증가를 예측했습니다. 진행된 단계에서 진단되는 사례가 여전히 많으며, 조기에 발견되는 종양은 고작 29%에 불과하여, 질환의 확산 정도를 상세하게 파악할 수 있는 정밀한 PET 및 SPECT 검사에 대한 수요가 높아지고 있습니다. 관상동맥 질환이 젊은 층으로까지 확산되고 있는 만큼, 핵의학 심장 검사 건수가 증가하고 있습니다. 현재 25-45세 인도인의 3분의 2가 고혈압 위험군에 속해 있으며, 임상의들은 중재의 우선순위를 결정하기 위해 비침습적 심근 관류 영상 검사를 선택하고 있습니다. 따라서 생활습관병으로 인한 발병률 증가는 모든 핵의학 영상 기법의 활용을 직접적으로 촉진하며, 인도의 핵의학 영상 시장의 구조적 성장을 뒷받침하고 있습니다.

3차 의료기관에서의 하이브리드 PET-CT 및 SPECT-CT 도입

PET-CT 설치 대수는 전국적으로 50대를 넘어섰지만, SPECT-CT의 성장세는 1회당 스캔 비용이 높기 때문에 그 기세를 따라가지 못하고 있습니다. 그러나 비용 대비 효과 조사에 따르면, 인도에서 PET-CT 스캔 비용은 4,600-3만 1,000 루피(55-372 달러)로 세계 평균보다 훨씬 낮기 때문에 대규모 시설의 투자 회수 기간이 단축되고 있습니다. CZT 검출기와 AI 지원 재구성 기술을 통해 해상도가 향상되는 동시에 추적자 피폭 선량이 감소하여, 방사선 안전을 중시하는 시설에서 하이브리드 이미징의 매력을 높이고 있습니다. 3차 의료기관들이 장비를 교체함에 따라, 환자 의뢰 패턴이 종합적인 핵의학 영상 시설로 전환되고 있으며, 이로 인해 인도의 핵의학 영상 시장이 더욱 확대되고 있습니다.

높은 장비 도입 및 유지 비용

감마나이프나 PET-CT 시설을 설치하는 데는 부동산, 차폐, 인허가 비용을 포함하면 4억 루피(488만 달러)의 비용이 소요될 수 있습니다. 소규모 병원에서는 이러한 지출을 정당화할 만한 환자 수가 부족한 경우가 많기 때문에 대도시의 3차 의료기관이 주요 설치 장소로 자리 잡고 있어, 인도의 핵의학 영상 시장의 지리적 확산이 제한되고 있습니다. 보증 기간이 만료된 후의 서비스 계약은 설비 가치의 연간 8-10% 수준으로 가격이 책정되어 있으며, 특히 예비 부품이 수입품이고 달러로 결제되기 때문에 운영 예산에 부담을 주고 있습니다. 리스 프로그램이나 민관 협력 모델이 등장하고는 있지만, 이러한 방안들은 아직 초기 단계에 머물러 있어 고액의 설비 투자라는 장벽을 완전히 해소해 주지는 못합니다.

부문별 분석

2025년 기준으로 방사성 동위원소는 인도의 핵의학 영상 시장의 59.78%를 차지했으며, 이 하위 부문은 2031년까지 연평균 성장률(CAGR) 9.62%를 나타낼 것으로 전망됩니다. 테크네튬-99m은 여전히 SPECT의 주력 물질로, 단일광자 촬영의 약 80%를 차지하고 있지만, 원자로 기반의 생산 체인에는 잘 알려진 공급 위험이 수반됩니다. 플루오르-18과 같은 PET용 방사성 동위원소는 운송 중 추적자의 붕괴 손실을 줄여주는 첸나이와 하이데라바드의 새로운 사이클로트론에 힘입어 더욱 빠르게 성장하고 있습니다. 치료 분야에서는 신경내분비종양 및 전립선암 치료용 루테튬-177 표지 화합물이 2024년에 인도 의약품 규제청(DCGI)의 승인을 획득함에 따라 그 보급이 가속화되고 있습니다. BARC(바라트 원자력 연구센터)의 국내 Lu-177 생산량은 국내 수요의 65%를 충족하고 있으며, 수입품에 비해 치료 비용을 약 20% 절감하고 있습니다.

기기 분야에서는 하드웨어 혁신, 특히 저선량 스캔 시 감도를 향상시키는 고체 검출기 어레이를 통해 부가가치를 높이고 있습니다. GE 헬스케어와 지멘스 헬스인어즈의 현지화 노력 덕분에 2027년까지 단가를 10-12% 낮출 수 있을 것으로 기대되지만, 고정밀 결정체와 진공 부품은 여전히 해외 조달에 의존하고 있어 유지보수 비용은 여전히 높은 수준을 유지하고 있습니다. 그럼에도 불구하고, 장비 가격이 합리적으로 책정됨에 따라 고객 기반이 확대되고, 이는 방사성 동위원소 수요의 선순환을 뒷받침하며, 인도의 핵의학 영상 시장 규모를 더욱 확대시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the india nuclear imaging market size is expected to grow from USD 422.19 million in 2025 to USD 459.72 million in 2026 and is forecast to reach USD 703.69 million by 2031 at 8.89% CAGR over 2026-2031.

This report is Segmented by Product (Equipment, Radioisotopes [SPECT Radioisotopes {Technetium-99m (Tc-99m), and More} and PET Radioisotopes]), Application (Cardiology, Neurology, Thyroid, Oncology, and Other Applications), End User (Hospitals, Diagnostic Imaging Centres, and Academic & Research Institutes). The Market Forecasts are Provided in Terms of Value (USD).

India Nuclear Imaging Market Trends and Insights

Growing Prevalence of Cancer and Cardiac Diseases

India logged 1.4 million new cancer cases in 2024, and the National Cancer Registry projects a 12.8% jump by 2025. Late-stage diagnosis remains common, with only 29% of tumors detected early, raising demand for precise PET and SPECT procedures that can delineate disease spread. Nuclear cardiology volumes are climbing as coronary artery disease afflicts younger cohorts; two-thirds of Indians aged 25-45 are now pre-hypertensive, prompting clinicians to choose non-invasive myocardial perfusion imaging to triage intervention. Rising lifestyle-related morbidity therefore directly boosts utilization across all nuclear imaging modalities, reinforcing the structural growth of the India nuclear imaging market.

Adoption of Hybrid PET-CT and SPECT-CT in Tertiary Hospitals

PET-CT installations have surpassed 50 units nationwide while SPECT-CT growth trails because of higher per-scan costs. However, cost-effectiveness studies show a PET-CT scan in India is priced at INR 4,600-31,000 (USD 55-372), far below global averages, shortening payback periods for large centers. CZT detectors and AI-assisted reconstruction improve resolution while lowering tracer dose, making hybrid imaging more attractive in radiation-safety-conscious facilities. As tertiary hospitals upgrade equipment, referral patterns shift toward comprehensive nuclear imaging suites, which further enlarges the India nuclear imaging market.

High Equipment Acquisition and Maintenance Cost

Setting up a gamma-knife or PET-CT suite can cost INR 400 million (USD 4.88 million) when real estate, shielding, and licensing expenses are included. Smaller hospitals often lack patient throughput to justify such outlays, so metropolitan tertiary centers remain the primary installation sites, limiting geographic penetration of the India nuclear imaging market. Post-warranty service contracts priced at 8-10% of capital value per year strain operating budgets, particularly since spare parts are imported and dollar-denominated. Leasing programs and public-private partnerships are emerging, yet they remain nascent and do not fully erase the high-capex hurdle.

Other drivers and restraints analyzed in the detailed report include:

- Ayushman Bharat Imaging-Infrastructure Roll-out

- Expansion of Domestic Radioisotope Production at BARC

- Scarcity of Skilled Nuclear-Medicine Technologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radioisotopes generated 59.78% of the India nuclear imaging market share in 2025, and the subsegment is forecast to post a 9.62% CAGR through 2031. Technetium-99m remains the workhorse for SPECT, accounting for roughly 80% of single-photon studies, yet its reactor-based production chain presents well-documented supply risk. PET radioisotopes such as Fluorine-18 are growing more swiftly, aided by new cyclotrons in Chennai and Hyderabad that reduce tracer decay losses during transport. On the therapeutic front, Lutetium-177 labeled compounds for neuroendocrine tumors and prostate cancer secured Drug Controller General of India approvals in 2024, spurring wider adoption. Domestic Lu-177 output at BARC meets 65% of national demand, trimming procedure costs by nearly 20% versus imported doses.

The equipment segment adds incremental value through hardware innovation, especially solid-state detector arrays that boost sensitivity in low-dose scans. Localization initiatives by GE HealthCare and Siemens Healthineers promise to shave 10-12% off unit prices by 2027, but maintenance costs remain elevated because high-precision crystals and vacuum components still come from overseas. Even so, rising equipment affordability broadens the customer base, supporting a virtuous cycle of radioisotope demand that further scales the India nuclear imaging market size.

List of Companies Covered in this Report:

- Advanced Accelerator Applications S.A. (Novartis)

- Alliance Medical (Life Healthcare Group)

- Board of Radiation & Isotope Technology (BRIT)

- Bracco Imaging S.p.A.

- Canon

- Cardinal Health

- Curium Pharma

- GE Healthcare

- Koninklijke Philips

- Positron

- Shenzen Mindray Bio-Medical Electronics Co., Ltd.

- Siemens Healthineers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing prevalence of cancer and cardiac diseases

- 4.2.2 Rising adoption of hybrid imaging modalities in tertiary hospitals

- 4.2.3 Government initiatives under Ayushman Bharat to expand imaging infrastructure

- 4.2.4 Increasing domestic radioisotope production via BARC

- 4.2.5 Shift to low-dose CZT detectors driven by radiation-safety norms

- 4.2.6 Emergence of private-equity-funded standalone PET-CT chains

- 4.3 Market Restraints

- 4.3.1 High cost of equipment acquisition and maintenance

- 4.3.2 Scarcity of skilled nuclear-medicine technologists

- 4.3.3 Mo-99 import supply-chain disruptions

- 4.3.4 AERB licensing delays for new cyclotrons

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Equipment

- 5.1.2 Radioisotopes

- 5.1.2.1 SPECT Radioisotopes

- 5.1.2.1.1 Technetium-99m (Tc-99m)

- 5.1.2.1.2 Thallium-201 (Tl-201)

- 5.1.2.1.3 Gallium-67 (Ga-67)

- 5.1.2.1.4 Iodine-123 (I-123)

- 5.1.2.1.5 Other SPECT Isotopes

- 5.1.2.2 PET Radioisotopes

- 5.1.2.2.1 Fluorine-18 (F-18)

- 5.1.2.2.2 Rubidium-82 (Rb-82)

- 5.1.2.2.3 Other PET Isotopes

- 5.1.2.1 SPECT Radioisotopes

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Neurology

- 5.2.3 Thyroid

- 5.2.4 Oncology

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Imaging Centres

- 5.3.3 Academic & Research Institutes

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Advanced Accelerator Applications S.A. (Novartis)

- 6.3.2 Alliance Medical (Life Healthcare Group)

- 6.3.3 Board of Radiation & Isotope Technology (BRIT)

- 6.3.4 Bracco Imaging S.p.A.

- 6.3.5 Canon Medical Systems Corporation

- 6.3.6 Cardinal Health Inc.

- 6.3.7 Curium Pharma

- 6.3.8 GE HealthCare

- 6.3.9 Koninklijke Philips N.V.

- 6.3.10 Positron Corporation

- 6.3.11 Shenzen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.12 Siemens Healthineers

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment