|

시장보고서

상품코드

2063690

생명과학 및 화학 계측기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Life Science And Chemical Instrumentation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

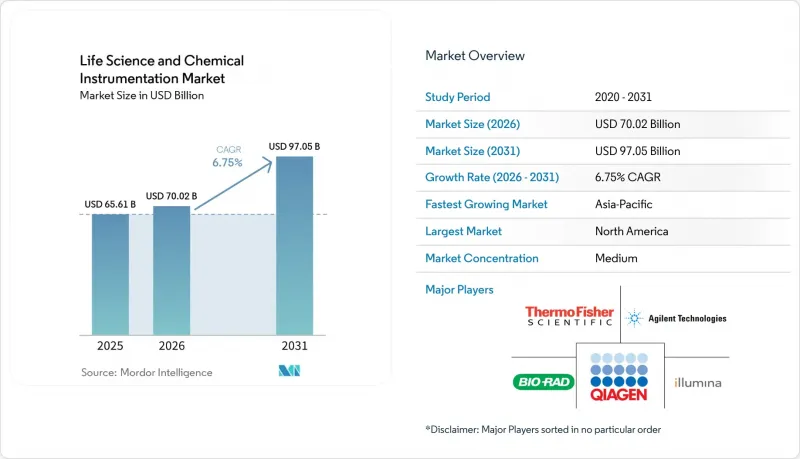

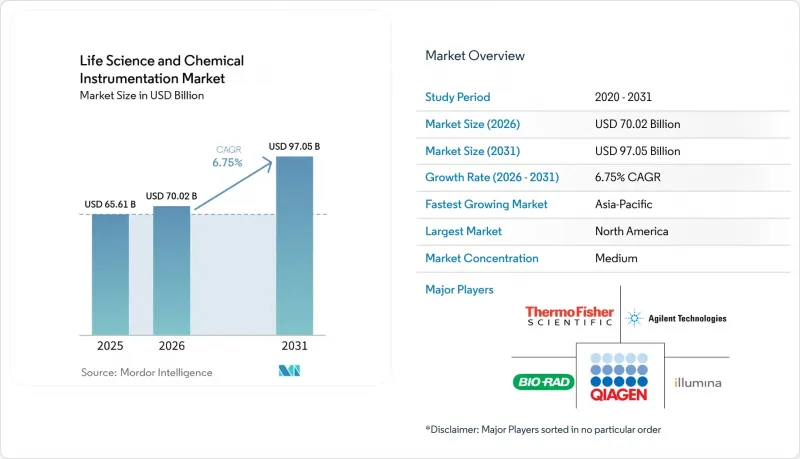

Mordor Intelligence에 의하면, 생명과학 및 화학 계측기 시장 규모는 2025년에 656억 1,000만 달러로 평가되었습니다. 2026년에 700억 2,000만 달러에서 2031년까지 970억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.75%를 나타낼 전망입니다.

본 보고서는 제품(장비, 소모품, 소프트웨어), 기술(분광법, 크로마토그래피, PCR, NGS 등), 최종 사용자(제약·바이오기술 기업, 병원 및 진단센터 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 생명과학 및 화학 계측기 시장 동향 및 인사이트

급증하는 제약·생명공학 연구개발 예산

2025년, 전 세계 연구개발비는 고르지 않은 회복세를 보였습니다. 비만 치료제 및 GLP-1 관련 제품을 주력 제품으로 하는 기업은 예산을 두 자릿수 비율로 증액하고, 항체-약물 복합체(ADC) 및 CAR-T 제품의 특성 평가를 위한 초고속 액체 크로마토그래피와 고매개변수 유세포분석기에 추가 자금을 투입했습니다. 현재 종양학 분야는 신약 개발 아웃소싱 시장의 31.5%를 차지했으며, 각 CRO 기업들은 혈장 내 저빈도 종양 돌연변이를 정량화하는 디지털 PCR 및 차세대 염기서열 분석 역량을 강화해야 하는 상황에 직면해 있습니다. 2023년 바이오의약품 거래 상위 10건 중 9건에 정밀의학 관련 자산이 포함되어 있으며, 이는 단일 세포의 이질성이나 멀티오믹스 시그니처를 규명하는 분석 플랫폼에 대한 지속적인 수요를 보여줍니다. 이러한 추세에 따라, 스폰서와 서비스 제공업체 양쪽 생태계 모두에서 크로마토그래피, 질량 분석, 시퀀싱 시스템의 구매 주기가 지속될 것으로 확실시되고 있습니다. 베이지안 알고리즘을 도입해 법 개발을 자동화하는 벤더는 이용률을 한층 더 높여, 인력 부족으로 어려움을 겪는 연구소에 최적의 선택지가 되고 있습니다.

세계 각국의 엄격한 규제 및 품질 관리 요건

FDA의 2024년판 ‘신규 조사 기법’ 지침은 오르가노-온-칩 및 하이컨텐츠 이미징을 명시적으로 권장하고 있으며, 마이크로플루이딕스 장치와 자동 현미경 장치의 즉각적인 도입을 촉진하는 한편, 많은 구형 벤치탑형 분광기를 구식으로 만들고 있습니다. 유럽의 유해사건 관리 시스템은 실시간 데이터 업로드를 의무화하고 있어, CRO는 크로마토그래피 및 질량 분석기에 전자 서명과 감사 추적을 추가하는 클라우드 커넥터를 사후에 장착해야만 합니다. 규정 준수 대응을 위한 개조 비용은 1대당 5만-15만 달러에 달하고, 소규모 연구소에게는 부담이 크기 때문에 21 CFR Part 11 및 GDPR(EU 개인정보보호규정) 모듈이 기본으로 탑재된 통합 플랫폼에 대한 수요가 증가하고 있습니다. 감사 기관이 사이버 보안을 엄격하게 심사하게 되면서 ISO 17025 인증에 소요되는 기간이 2배인 1년으로 늘어났으며, 이로 인해 업그레이드 주기가 가속화되어 안전한 펌웨어와 원격 모니터링 기능을 갖춘 공급업체가 유리한 입장에 서게 되었습니다. 이러한 규제들이 복합적으로 작용함에 따라, 구매 기준은 분석 성능뿐만 아니라 추적성, 데이터 무결성, 그리고 사이버 보안 성숙도로 전환되고 있습니다.

첨단 실험실용 분석 장비에 드는 높은 설비 투자 비용 및 운영 비용

일루미나(Illumina)사의 NovaSeq X Plus 가격은 100만 달러를 초과하며, 연간 소모품 비용으로 20만-30만 달러가 필요하기 때문에 많은 학술 연구 기관의 전체 장비 예산을 상회하고 있습니다. 디지털 PCR 카트리지는 검체당 8-12달러로, 실시간 PCR 비용의 약 3배이며, 그 도입은 보험 적용 대상인 종양 진단으로 제한되어 있습니다. 분광 분석 장치의 리스료는 정가의월1.8-3.3%입니다. 따라서, 20만 달러짜리 FTIR 장비의 경우 월 3,600-6,600달러의 비용이 발생하며, 가동률이 60% 미만으로 떨어지면 큰 부담이 됩니다. 질량 분석기의 서비스 계약 비용은 연간 구매 가격의 평균 12-15%를 차지하며, 공급업체가 소프트웨어 구독을 세트로 요구하는 사례가 늘어나면서 LC-MS 1대당 연간 총 지출을 5만 달러 이상으로 끌어올리고 있습니다. 이러한 경제적 이유로 인한 교체 주기의 장기화는 보조금이나 벤처 자금이 부족한 신흥 시장에서 특히 두드러집니다.

부문별 분석

2025년 매출액 중 기기가 여전히 63.66%를 차지했지만, 소모품은 연평균 성장률(CAGR) 7.23%라는 가장 높은 성장세를 보였으며, 이는 현대 벤더 전략의 근간을 이루는 ‘면도날’ 경제 모델을 반영했습니다. 크로마토그래피 컬럼은 500-2,000회 주입마다 교체해야 하지만, Bio-Rad사의 액적 생성 카트리지는 기존 PCR 시약 가격의 3-5배에 달하는 가격으로 안정적인 수익원을 확보하고 있습니다.

금액 기준으로는 가장 작은 규모인 소프트웨어 부문이지만, 벤더들이 클라우드 데이터 스토리지, 예측 유지보수, 규정 준수 보고에 대해 기기 1대당 연간 5,000-1만 5,000달러를 청구하고 있기 때문에 비중 면에서는 가장 빠르게 성장할 것으로 예측됩니다. 매출총이익률은 80%를 초과하며, 기업들은 99%의 가동률을 보장하는 장비 구독 계약에 소프트웨어를 묶어 판매하도록 권장받고 있어, 이를 통해 충성도 높고 수익성이 뛰어난 고객 관계를 구축하고 있습니다.

지역별 분석

북미는 2025년에 42.20%의 점유율을 유지했습니다. 이는 엄격한 규제를 받는 의약품 제조, NIH(미국 국립보건원)가 자금을 지원하는 연구 인프라, 그리고 신속한 서비스 대응을 뒷받침하는 집중된 공급업체 기반에 힘입은 결과입니다. 이 지역의 성장세는 신흥 시장에 비해 둔화되고 있지만, FDA(미국 식품의약국)의 지침에 따라 연구소들이 ‘장기 온 칩(organ-on-a-chip)’ 및 하이컨텐츠 이미징 솔루션으로 전환해야 하는 상황에서 방대한 도입 기반이 꾸준한 교체 수요를 보장하고 있습니다. 캐나다의 바이오 제조 인센티브와 멕시코의 니어쇼어링 확대에 힘입어, 크로마토그래피 및 분광 분석 플랫폼에 대한 수요가 더욱 증가하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.45%를 나타낼 것으로 전망됩니다. 인도의 생산 연계형 인센티브 제도 덕분에 191종의 원료의약품 중간체에 대해 260억 달러의 투자가 유치되었으며, 이들 모두 품질 관리를 위해 크로마토그래피와 질량 분석이 필요합니다. 카르나타카주의 산업 정책에 따라 25%의 자본 보조금이 제공되고 있으며, 이를 통해 생명과학 및 화학 계측기 시장의 총 소유 비용이 최대 20% 절감되어, 애지런트, 워터스, 서모피셔 각사가 방갈로르와 하이데라바드에 용도 연구소를 개설하는 계기가 되었습니다. 중국 내 국내 장비 제조업체에 대한 보조금은 희토류 수출 규제에 따른 지정학적 위험에도 불구하고, 현지에서 두 자릿수 성장을 뒷받침하고 있습니다. 일본, 한국, 호주는 의약품 생산 및 학술 연구와 관련하여 규모는 작지만 안정적인 수요를 이끌고 있습니다.

유럽은 금액 기준으로 3위입니다. 독일의 공정 분석 기술에 대한 수요, 영국의 공유 핵심 시설 모델, 그리고 프랑스의 종양학 연구가 수요를 뒷받침하고 있습니다. EMA(유럽의약품청)의 데이터 무결성 관련 규정에 따라, 감사 추적이 내장된 클라우드 연동형 크로마토그래피 및 질량 분석 장치의 도입이 확대되고 있습니다. 남미 및 중동 및 아프리카는 여전히 개발도상국 단계에 있지만, GCC 국가들의 병원 확장 및 브라질의 생명공학 클러스터가, 특히 리스나 ‘장비 서비스(IaaS)’ 모델이 자금 면의 제약을 해소해 주는 지역에서 해당 지역 전체의 수주 실적을 끌어올리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the life science and chemical instrumentation market size is projected to be USD 65.61 billion in 2025, USD 70.02 billion in 2026, and reach USD 97.05 billion by 2031, growing at a CAGR of 6.75% from 2026 to 2031.

This report is Segmented by Product (Instruments, Consumables, Software), Technology (Spectroscopy, Chromatography, PCR, NGS, and More), End-User (Pharmaceutical & Biotechnology Companies, Hospitals & Diagnostic Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Life Science And Chemical Instrumentation Market Trends and Insights

Surging Pharmaceutical & Biotech R&D Budgets

Global R&D spending rebounded unevenly in 2025; companies with obesity and GLP-1 franchises raised budgets by double digits, channeling extra capital toward ultra-high-performance liquid chromatography and high-parameter flow cytometry that characterize antibody-drug conjugates and CAR-T products. Oncology now captures 31.5% of outsourced discovery, compelling CROs to expand digital PCR and next-generation sequencing capacity that quantifies low-frequency tumor mutations in plasma. Nine of the top 10 biopharma deals in 2023 included precision-medicine assets, signaling a durable preference for analytical platforms that resolve single-cell heterogeneity and multi-omic signatures. These dynamics ensure sustained purchase cycles for chromatography, mass spectrometry, and sequencing systems across both sponsor and service-provider ecosystems. Vendors that embed Bayesian algorithms to automate method development further improve utilization, making them preferred choices for labs battling labor shortages.

Stringent Global Regulatory & Quality-Control Requirements

The FDA's 2024 New Approach Methodologies guidance explicitly endorses organ-on-chip and high-content imaging, driving immediate procurement of microfluidic and automated microscopy instruments and rendering many legacy bench spectrometers obsolete. Europe's Adverse Event Management System mandates real-time data uploads, compelling CROs to retrofit chromatography and mass spectrometry units with cloud connectors that add electronic signatures and audit trails. Compliance retrofits cost USD 50,000-150,000 per unit, a burden smaller labs struggle to shoulder, which steers demand toward integrated platforms that ship with 21 CFR Part 11 and GDPR modules out-of-the-box. ISO 17025 accreditation timelines have doubled to one year as auditors scrutinize cybersecurity, intensifying upgrade cycles that favor vendors with secure firmware and remote-monitoring capabilities. Collectively, these rules move purchasing criteria beyond analytical performance toward traceability, data integrity, and cybersecurity maturity.

High Capital & Operating Costs of Advanced Laboratory Analytical Instruments

Illumina's NovaSeq X Plus lists above USD 1 million with annual consumable obligations of USD 200,000-300,000, exceeding entire instrumentation budgets for many academic cores. Digital PCR cartridges cost USD 8-12 per sample, about triple the real-time PCR costs, limiting uptake to reimbursable oncology diagnostics. Spectroscopy leases run 1.8-3.3% of list price monthly; a USD 200,000 FTIR, therefore, costs USD 3,600-6,600 per month, a strain when utilization dips under 60%. Mass-spec service contracts average 12-15% of purchase price per year, and vendors increasingly require bundled software subscriptions that push total annual spend above USD 50,000 per LC-MS unit. These economic slow refresh cycles are especially prevalent in emerging markets that lack grant or venture funding.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Automation & Miniaturization in Laboratory Analytical Instruments

- Expansion of Precision-Medicine & Multi-Omics Workflows

- Shortage of Skilled Analytical Scientists & Service Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments still generated 63.66% of 2025 revenue, but consumables posted the highest trajectory at a 7.23% CAGR, reflecting the razor-blade economics underpinning modern vendor strategies. Chromatography columns require replacement every 500-2,000 injections, while Bio-Rad's droplet-generation cartridges secure an annuity stream priced three to five times conventional PCR reagents.

Software, the smallest category by dollars, is expected to rise fastest in percentage terms as vendors charge USD 5,000-15,000 annually per instrument for cloud data storage, predictive maintenance, and compliance reporting. Gross margins surpass 80%, encouraging firms to bundle software into instrument subscription contracts that promise 99% uptime, creating sticky, high-margin relationships.

Geography Analysis

North America retained 42.20% share in 2025, driven by tightly regulated pharmaceutical manufacturing, NIH-funded research infrastructure, and a concentrated vendor base that supports rapid service response. Although the region's growth decelerates relative to emerging markets, a vast installed base ensures steady replacement as FDA guidance pushes labs toward organ-on-chip and high-content imaging solutions. Canada's biomanufacturing incentives and Mexico's nearshoring gains add incremental demand for chromatography and spectroscopy platforms.

Asia-Pacific is projected to record an 8.45% CAGR through 2031. India's Production Linked Incentive scheme unlocked USD 26 billion in investment across 191 bulk-drug intermediates, each requiring chromatography and mass spectrometry for quality control. Karnataka's Industrial Policy offers 25% capital subsidies, slicing the life science and chemical instrumentation market's total cost of ownership by up to 20% and enticing Agilent, Waters, and Thermo Fisher to open application labs in Bengaluru and Hyderabad. China's subsidies for domestic instrument builders spur double-digit local growth despite geopolitical risks tied to rare-earth export controls. Japan, South Korea, and Australia contribute stable but smaller volumes linked to pharmaceutical production and academic research.

Europe sits third by value. Germany's process-analytical-technology requirements, the UK's shared core-facility model, and France's oncology research underpin demand. EMA data-integrity mandates push adoption of cloud-connected chromatography and mass spectrometry with embedded audit trails. South America and Middle East & Africa remain nascent, yet GCC hospital expansions and Brazil's biotech clusters lift regional orders, especially where leasing and instrument-as-a-service models bridge capital constraints.

- Agilent Technologies

- Beckton Dickinson

- Bio-Rad Laboratories

- Bruker

- Danaher

- Eppendorf

- GE HealthCare (Cytiva)

- Hitachi High-Tech Corp.

- HORIBA

- Illumina

- JEOL Ltd.

- Merck

- Mettler Toledo

- Oxford Instruments

- PerkinElmer Inc. (Revvity)

- QIAGEN

- Sartorius

- Shimadzu

- Thermo Fisher Scientific

- Waters Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Pharmaceutical & Biotech R&D Budgets

- 4.2.2 Stringent Global Regulatory & Quality-Control Requirements

- 4.2.3 Rapid Adoption of Automation & Miniaturization in Laboratories

- 4.2.4 Expansion of Precision-Medicine & Multi-Omics Workflows

- 4.2.5 Government Incentives for Domestic Instrument Manufacturing

- 4.2.6 Subscription-Based "Instrument-As-A-Service" Models Gaining Traction

- 4.3 Market Restraints

- 4.3.1 High Capital & Operating Costs of Advanced Instruments

- 4.3.2 Shortage of Skilled Analytical Scientists & Service Engineers

- 4.3.3 Supply-Chain Vulnerability for Semiconductor/Rare-Earth Components

- 4.3.4 Cyber-Security & Data-Integrity Compliance Burden for Cloud-Connected Devices

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Instruments

- 5.1.2 Consumables

- 5.1.3 Software

- 5.2 By Technology

- 5.2.1 Spectroscopy

- 5.2.2 Chromatography

- 5.2.3 Polymerase Chain Reaction (PCR)

- 5.2.4 Next-Generation Sequencing (NGS)

- 5.2.5 Flow Cytometry

- 5.2.6 Microscopy

- 5.2.7 Electrophoresis

- 5.2.8 Centrifuges

- 5.3 By End-User

- 5.3.1 Pharmaceutical & Biotechnology Companies

- 5.3.2 Hospitals & Diagnostic Centers

- 5.3.3 Contract Research Organizations (CROs)

- 5.3.4 Academia & Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agilent Technologies Inc.

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Bio-Rad Laboratories Inc.

- 6.3.4 Bruker Corporation

- 6.3.5 Danaher Corporation

- 6.3.6 Eppendorf AG

- 6.3.7 GE HealthCare (Cytiva)

- 6.3.8 Hitachi High-Tech Corp.

- 6.3.9 Horiba Ltd.

- 6.3.10 Illumina Inc.

- 6.3.11 JEOL Ltd.

- 6.3.12 Merck KGaA

- 6.3.13 Mettler-Toledo International Inc.

- 6.3.14 Oxford Instruments plc

- 6.3.15 PerkinElmer Inc. (Revvity)

- 6.3.16 QIAGEN N.V.

- 6.3.17 Sartorius AG

- 6.3.18 Shimadzu Corporation

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Waters Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment