|

시장보고서

상품코드

2063731

아미노산 대사장애 치료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Amino Acid Disorders Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

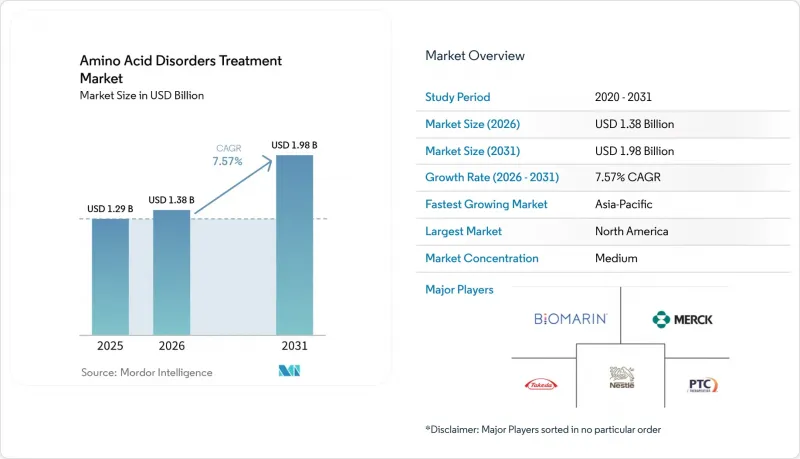

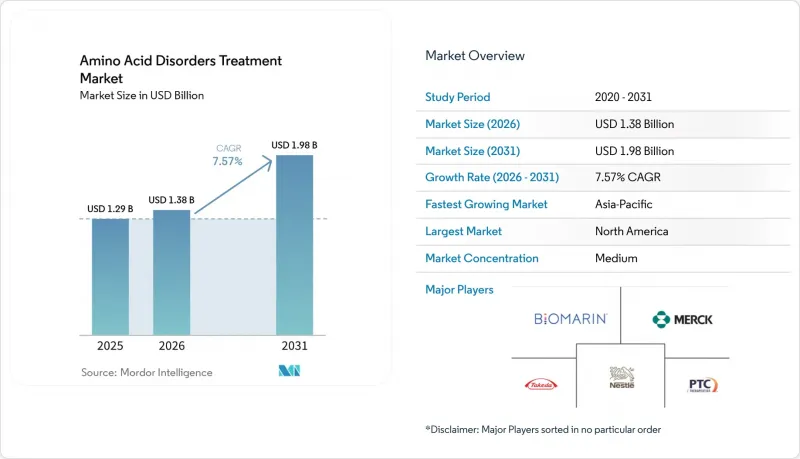

Mordor Intelligence에 의하면, 아미노산 대사장애 치료 시장 규모는 2025년 12억 9,000만 달러로 평가되었습니다. 2026년에는 13억 8,000만 달러로 확대되어 2031년까지 19억 8,000만 달러에 이르고 2026-2031년 CAGR은 7.57%를 나타낼 전망입니다.

본 보고서는 질환 유형(페닐케톤뇨증, MSUD, 호모시스테인뇨증, 티로신혈증, ARG1-D), 치료법(의료영양요법, 약물요법, 임상시험 요법), 투여 경로(경구, 비경구), 유통 채널(병원, 소매, 온라인 약국), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준입니다.

세계의 아미노산 대사장애 치료 시장 동향 및 인사이트

희귀질환 치료제의 승인 확대에 따라 치료 대상이 되는 환자층이 확대됨

적응증 확대 및 신규 승인으로 인해 치료 대상이 되는 환자 수가 증가하고 있으며, 이에 따라 단기적인 치료 시작 건수가 늘어나고, 복약 순응도 지원이 지속되고 있습니다. 2026년 2월, FDA는 12-17세 청소년을 대상으로 한 효소 요법을 승인함으로써, 성인에 대한 사용에 이어 더 어린 연령층으로의 접근성을 확대하고, 지속적인 매출 성장을 뒷받침하고 있습니다. 2025년 7월, 테트라하이드로비오프테린 전구체가 영유아부터 성인에 이르는 광범위한 적응증에 대해 미국에서 승인을 획득했으며, 이 치료법은 유럽연합 집행위원회의 승인도 획득했습니다. 이를 통해 주요 시장 전반에 걸쳐 시기적으로 조율된 출시 계획이 마련되었습니다. 유럽 규제 당국은 호모시스테인뇨증 치료용 후보 약물인 하이드록시코발라민 아세테이트에 희귀질환 치료제 지정을 부여함으로써, 페닐알라닌 수산화효소 결핍증을 넘어선 파이프라인의 확장을 시사했습니다. 2025년 6월, FDA는 알카프톤뇨증 치료제인 니치시논 정을 승인했습니다. 이는 이 극히 드문 질환에 대한 최초의 승인된 치료법이며, 제조업체는 환자들의 접근성을 높이기 위해 동반 지원 프로그램을 시작했습니다. 효소 요법에 대해 의무화된 REMS(위험 평가 및 완화 전략)에는 모든 환자와 보호자를 대상으로 한 아나필락시스 교육 및 에피네프린 자동 주사기 비치가 포함되어 있어, 승인 후 위험 관리 요건이 계속해서 주목받고 있습니다.

전 세계적으로 신생아 선별검사가 확대됨에 따라 진단 건수가 증가

신생아 선별검사에 대한 정책의 갱신과 기술의 발전으로 인해 유전성 대사 질환의 검출률이 높아지고 있으며, 보다 조기 치료 체계가 확립되고 있습니다. 호주의 전국 신생아 혈액 선별검사는 새로운 적응증의 추가로 확대되고 있으며, 정부 부처의 승인 절차를 통해 리소좀 축적증이 검사 대상에 포함되도록 추진되고 있습니다. 이에 따라 가까운 시일 내에 연간 진단 건수가 점진적으로 증가할 것으로 예측됩니다. 중국에서 2018년부터 2024년까지 신생아 16만 1,966명을 대상으로 한 지역 등록 자료를 분석한 결과, 살아난 신생아 1,000명당 2,842명 중 1명의 비율로 유전성 대사 질환이 확인되었습니다. 이는 과거의 여러 코호트와 비교했을 때 유의미하게 높은 검출률이며, 탠덤 질량 분석법의 도입 확대가 미친 영향을 뒷받침하는 것입니다. 뉴질랜드에서는 2024년에 국가 지원 대상이 14유형의 페닐케톤뇨증용 보충제로 확대됨에 따라, 규모는 작지만 증가 추세에 있는 이용자층에 대한 지속적인 관리가 개선되었습니다. 온타리오주는 2025년 3월에 지원 대상 목록을 갱신하여, 48종의 페닐케톤뇨증 전용 의료용 식품을 추가하는 한편, 의약품 승인 절차를 변경했습니다. 이로 인해 1차 치료법의 선정 및 예산에 미치는 영향이 결정되고 있습니다. 2025년 신생아 유전체 선별 검사 프로그램에 관한 다국적 분석 결과, 주요 유전자 집합에서 뚜렷한 수렴 현상이 관찰되었으며, 검사 대상 선정에 영향을 미치는 예측 인자가 정량화되었습니다. 이는 지역을 초월한 향후 검사 범위 확대에 있어 조화와 우선순위 설정에 도움이 될 수 있습니다.

고액의 치료비와 의료용 식품비가 접근을 가로막고 있습니다.

치료 총비용은 여전히 고액이며, 특정 보험 가입자층의 경우 이용 가능한 지원액을 초과하는 경우가 있어, 이로 인해 치료 시작이 지연되거나 처방전 갱신이 중단되는 경우가 있습니다. 많은 환자들이 제약사의 본인부담금 지원과 재단의 보조금을 병행하여 이용하고 있지만, 연간 보조금 상한액이 1년 치 치료비에 반드시 부합하는 것은 아니기 때문에 여러 지원처를 병행하거나 지원 창구로 안내해 줄 필요가 있는 경우가 종종 있습니다. 제약 회사의 프로그램을 이용하면, 해당 민간 보험 가입 환자의 본인 부담금을 매우 낮은 수준으로 낮출 수 있지만, 공적 보험 수급자는 추가적인 지원이 없으면 비용 부족에 직면할 가능성이 있습니다. 일부 주나 국가에서는 공적 보험 기관이 유전성 대사 질환에 대한 의료용 식품의 적용 대상 목록을 확대하여 식이 관리를 지원하고 있지만, 정책의 차이로 인해 여전히 적용 범위에 차이가 발생할 수 있습니다. 극히 드문 질환의 적응증에 대해서는 저·중소득 국가에서 발생하는 경제적 부담의 격차를 해소하기 위해 ‘컴패셔네이트 유스(특별 사용 허가)’나 무상 제공 등의 방안이 도입되고 있습니다. 이러한 조치가 있더라도, 급여 내용 확인, 사전 승인 및 이의 제기 절차로 인해 소요 기간이 길어지고, 약국 허브의 지원이 통합되지 않은 경우, 치료 공백이 발생할 위험이 높아질 수 있습니다.

부문별 분석

페닐케톤뇨증은 2025년에 44.08%를 차지했으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.10%를 나타낼 것으로 전망됩니다. 이는 대상 연령의 확대와 생후 1개월 이상의 환자를 대상으로 승인된 BH4 전구체의 등장을 반영한 것입니다. PKU의 점유율은 대규모 의료 시스템 전반에 걸쳐 조기 진단과 체계적인 치료를 보장하는 신생아 선별 검사의 보급에 힘입고 있습니다. 한편, 임상시험 및 등록 연구 데이터를 통해 보면, 승인된 약물 요법을 통해 페닐알라닌 수치가 임상적으로 유의미한 수준까지 감소한다는 사실이 밝혀졌습니다. PKU 이외에도 메이플 시럽 요증, 호모시스테인뇨증, 티로신혈증이 많은 지역에서 치료 대상 환자군의 상당 부분을 차지하고 있으며, 선별검사의 적용 범위 확대로 인한 혜택을 받고 있습니다. 2025년에 승인된 알카프톤뇨증의 새로운 치료법은 그동안 관리되지 않았던 초희귀질환에 대한 최초의 치료 경로를 개척했습니다. 이는 특정 국가에서의 이용 확대를 지원하는 ‘컴패니언 액세스 프로그램’에 의해 뒷받침되고 있습니다. 정책의 업데이트와 기술의 발전으로 인해 아시아태평양의 특정 지역에서는 검출률이 향상되고 있으며, 이에 따라 예측 기간 동안 식이 요법과 약물 요법 모두에 대한 환자 유입이 확대될 것으로 전망됩니다.

페닐케톤뇨증(PKU) 분야에서 선도적인 위상은 식이요법, BH4 경로 억제제, 효소 보충 요법을 아우르는 생태계를 반영하며, 이 모든 요소가 하나로 어우러져 전문의의 감독 하에 결과 중심의 치료 경로의 기반을 형성하고 있습니다. 효소 요법에 관한 미국 및 EU의 위험 관리 체계에는 아나필락시스 관리를 위한 교육 및 대비 조치가 포함되어 있으며, 이에 따라 투여는 훈련을 받은 센터나 거점에 집중되어 있습니다. 호모시스틴뇨증의 경우, 효소 보충 요법 및 경구용 효소 후보 약물에 대해 임상적 진전과 규제상 지정이 보고되었으며, 제조 규모 확대를 위해 3상 임상시험 프로그램이 일시 중단된 반면, 경구용 효소 요법에 대해서는 IND 신청 전 준비 작업이 계속되고 있습니다. 동일한 경로를 표적으로 하는 mRNA 치료 연구도 희귀 소아 질환 및 희귀질환으로 지정되어 있어, 장기적인 관리를 위한 치료 선택지의 확대 가능성을 시사하고 있습니다. 이러한 동향을 종합해 보면, PKU는 아미노산 대사장애 치료 시장의 최전선에 계속 자리 잡고 있는 동시에, 해당 질환군에 포함된 다른 적응증에도 점차적으로 대응하고 있으며, 안전성, 유효성 및 실제 임상 현장에서의 복약 순응도 간의 균형을 유지하면서 수년에 걸친 치료법 혁신을 뒷받침하고 있습니다. 2025년에는 신생아 선별검사 대상 집단에서의 보급이 보다 광범위한 접근성과 지원 중심의 치료 모델에 힘입어 확대된 결과, PKU가 아미노산 대사장애 치료 시장 점유율의 44.08%를 차지했습니다.

2025년에는 의료용 영양 식품이 매출의 55.32%를 차지했으며, GMP 기준에 따른 제제 및 유리 아미노산 제제가 소아 및 성인 집단의 일일 섭취 목표의 기반이 되었습니다. 각 공급업체들은 비타민 D 함량이 높고 단백질 상당량당 부피가 작은 즉석 음용형 제품을 출시하여 섭취의 부담을 줄이는 동시에, 일상생활이나 업무 리듬에의 적합성을 높였습니다. 이 혁신은 PKU에 그치지 않고, 이눌린과 DHA를 함유한 호모시스테인뇨증 및 메이플 시럽뇨증 치료제 분야로 확대되었으며, 한편 원료 플랫폼의 개선을 통해 페닐알라닌 함량이 감소되어 민감한 환자들의 위장 편안함이 향상되었습니다. 유럽에서의 생산 투자를 통해 분말 제품의 포장 및 보관 시스템이 현대화되었으며, 이를 통해 병원 및 소매점의 업무 흐름이 개선되었을 뿐만 아니라, 소포장 형태로 인한 폐기물도 감소했습니다. 예측 기간 동안, 효소 보충 요법, 경구용 효소 제제, mRNA 및 BH4 전구체 접근법이 규제 및 제조 측면에서의 준비를 진행 중이므로, 임상시험 단계 및 첨단 카테고리는 아미노산 대사장애 치료 시장 전체보다 빠른 성장이 예상됩니다.

미국 및 EU에서 광범위한 적응증이 승인된 BH4 전구체가 치료 옵션을 확대하고, REMS 체계 내에서 적절한 대상 환자에 대한 효소 요법을 통해 페닐알라닌 수치의 정상화를 지속적으로 도모하는 가운데, 많은 환자에게 있어 약물 요법은 식이 제한을 완화하는 데 여전히 핵심적인 역할을 하고 있습니다. 2025년부터 2026년에 걸쳐 유전자 편집 분야의 포트폴리오 재평가 및 프로그램 중단은 간 표적 전달 방식에서 면역 장벽이 제기하는 과제를 부각시켰으며, 이로 인해 보다 단기적인 확장성이 기대되는 치료법으로의 투자 전환이 가속화되고 있습니다. 의료용 영양제는 선진적인 선택지가 확대되는 가운데, 폭넓은 환자층의 일상적인 관리를 지속적으로 뒷받침할 것입니다. 또한, 기호성, 영양 밀도 및 제형의 개선을 통해 의료용 식품은 장기 관리에 있어 필수적인 존재로 남을 것입니다. 아미노산 대사장애 치료 시장 규모는 임상시험 단계 및 첨단 치료법과 관련하여, 비경구 및 경구 투여 프로그램의 제조·유통 체계가 정비됨에 따라 확대될 것으로 전망됩니다.

지역별 분석

북미는 2025년에 매출의 52.11%를 차지했으며, 2031년까지 꾸준한 성장이 예상됩니다. 이는 효소 요법의 적응증 확대와 지역 의료의 관리 경로를 넓히는 데 기여한, 이미 승인된 BH4 전구체 제제의 선택지가 늘어난 데 힘입은 것입니다. 이 지역은 강력한 전문의 네트워크, 통합된 환자 지원 허브, 그리고 대다수의 피보험자를 등록하고 민간 보험 가입자 대다수의 본인 부담금을 경감시켜 주는 제약사의 프로그램의 혜택을 받고 있습니다. 포트폴리오의 최신 동향에 따르면, 제네릭 의약품과의 경쟁에 직면한 제품의 경우 매출이 압박을 받고 있는 반면, 효소 요법 및 희귀질환 포트폴리오 내의 성장 자산은 계속해서 증가하고 있습니다. 캐나다의 주 차원 정책 조정을 통해 의료용 식품 및 특정 약물 요법에 대한 보험 적용 범위가 세분화되었으며, 1차 선택 약물 및 예외적인 접근 경로로 환자를 의뢰하는 패턴이 형성되고 있습니다. 미국에서는 REMS(위험 평가 및 완화 전략)에 기반한 교육 및 모니터링 요건으로 인해 효소 요법의 사용이 훈련을 받은 시설로 집중되어 있으며, 이는 제한적인 유통망 및 조제를 위한 통합 허브와 일치합니다.

유럽에서는 주요 시장의 신생아 보편적 선별검사와, 영유아부터 성인에 이르기까지를 대상으로 하는 효소 보충 요법 및 BH4 전구체 약물의 지역 전체에 걸친 승인으로 인해 대규모 환자 기반이 유지되고 있습니다. 규제 문서에는 저페닐알라닌혈증과 관련된 안전상의 고려 사항, 교육 요건, 모니터링 사항이 명시되어 있으며, 이러한 내용들은 각국의 위험 관리 계획 및 환자 교육 프로그램에 반영되어 있습니다. 유럽의 제조업체들은 의료용 영양 식품의 생산 능력과 포장 시스템을 강화하고 있으며, 이를 통해 병원 및 소매 약국의 물류 효율이 향상되고 안정적인 재고 확보가 뒷받침되고 있습니다. 2025년에 승인된 아르카프토누리아 치료제는 저소득 국가를 대상으로 한 다자간 무상 제공 프로그램을 포함하여, 전 세계 희귀질환 치료제 포트폴리오 및 동반 접근 전략에서 유럽이 수행하는 역할을 보여주고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 5.24%를 나타낼 것으로 예측되며, 그 가장 큰 요인은 중국 및 탠덤 질량 분석법을 도입한 기타 몇몇 국가에서 신생아 선별 검사가 확대되고 유전성 대사 질환의 검출률이 향상되고 있기 때문입니다. 호주의 국가 프로그램에는 여러 질환이 추가되었으며, 장관 결정 절차를 통해 리소좀 축적증에 대한 추가적인 치료가 진행되고 있습니다. 이에 따라 연간 진단 건수가 증가하고, 의료용 영양제 및 약물 요법에 대한 수요가 확대될 것으로 전망됩니다. 뉴질랜드는 2024년에 14유형의 페닐케톤뇨증 치료용 보충제에 대한 지원 기간을 연장하여, 소수의 환자 집단에서 치료의 지속성과 순응도를 지원하고 있습니다. 남미에서는 제약사들의 접근성 향상 이니셔티브 덕분에 특정 국가에서 치료제의 접근성이 확대되고 있으며, 중동 및 아프리카의 일부 지역에서도 보험 적용이 여전히 제한적인 지역에서 환자를 지원하기 위한 유사한 프로그램이 운영되고 있습니다. 이 지역 전체에서 신생아 유전체 선별검사에 사용되는 주요 유전자 목록의 통합이 진행됨에 따라, 향후 프로토콜의 조화가 이루어질 것으로 전망됩니다. 이를 통해 증례 발견의 표준화가 진전되고, 아미노산 대사장애 치료법의 보급이 가속화될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the amino acid disorders treatment market size is expected to increase from USD 1.29 billion in 2025 to USD 1.38 billion in 2026 and reach USD 1.98 billion by 2031, growing at a CAGR of 7.57% over 2026-2031.

This report is Segmented by Disorder Type (Phenylketonuria, MSUD, Homocystinuria, Tyrosinemia, ARG1-D), Treatment Modality (Medical Nutrition, Pharmacotherapy, Investigational Therapies), Route (Oral, Parenteral), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography (North America, Europe, APAC, MEA, South America). Market Forecasts are in Value (USD)

Global Amino Acid Disorders Treatment Market Trends and Insights

Orphan-Drug Approvals Expanding Treatable Patient Pool

Broadened labels and new approvals are increasing the number of patients eligible for therapy, which lifts near-term initiations and sustains adherence support. In February 2026, the FDA cleared an enzyme therapy for adolescents aged 12-17, expanding access to a younger cohort following adult use and supporting ongoing revenue growth. A tetrahydrobiopterin precursor received United States approval in July 2025 with a broad label that spans infants through adults, and the therapy also secured European Commission authorization, together setting up a synchronized launch trajectory across major markets. The European regulator granted an orphan designation to a hydroxocobalamin acetate candidate for homocystinuria, signaling pipeline breadth beyond phenylalanine hydroxylase deficiency. In June 2025, the FDA approved nitisinone tablets for alkaptonuria, the first approved therapy for this ultra-rare indication, and the manufacturer launched a companion support program to facilitate patient access. Post-approval risk management requirements remain in focus, since a mandated REMS for enzyme therapy includes anaphylaxis education and epinephrine auto-injector readiness for all patients and caregivers.

Global Newborn Screening Expansion Increasing Diagnosed Base

Policy updates and technology upgrades in newborn screening are increasing the detection of inherited metabolic diseases and aligning treatment pathways earlier in life. Australia's national newborn bloodspot screening is expanding with new indications and is progressing additional lysosomal storage disorders through its ministerial pathway, which will translate into incremental annual diagnoses in the near term. In China, a regional registry covering 161,966 newborns from 2018 to 2024 documented an inherited metabolic disease incidence of 1 in 2,842 live births, a significantly higher detection rate than several prior cohorts, which underscores the impact of tandem mass spectrometry scale-up. New Zealand's national funding expanded to include 14 phenylketonuria supplements in 2024, improving continuity of care for a small but growing cohort of users. Ontario updated its covered list in March 2025 to include 48 phenylketonuria-specific medical foods while changing how pharmacologic agents are approved, which shapes first-line therapy choice and budget impact. A 2025 multi-country analysis of genomic newborn screening programs showed strong convergence on a core set of genes, and it quantified the predictors that drive inclusion decisions, which can help harmonize and prioritize future expansions across geographies.

High Therapy and Medical Food Costs Constraining Access

Total cost of care remains high and can exceed available assistance in certain payer segments, which delays starts and interrupts refills. Many patients rely on a combination of manufacturer copay support and foundation grants, yet annual grant caps do not always match full-year therapy costs, so layering of resources and hub navigation is often required. Access to programs from manufacturers can reduce out-of-pocket costs to very low levels for eligible commercially insured patients, but public program beneficiaries may experience shortfalls without supplemental aid. Public payers in some provinces and countries have expanded lists of covered medical foods for inherited metabolic diseases, which supports dietary management, though policy differences can still create uneven coverage. For ultra-rare indications, compassionate-use and free-goods initiatives have emerged to bridge affordability gaps across low- and middle-income countries. Even with these measures, benefit verification, prior authorization, and appeal cycles can extend timelines and heighten the risk of treatment gaps where pharmacy hub support is not integrated.

Other drivers and restraints analyzed in the detailed report include:

- Medical Nutrition Innovation (GMP-Based, Ready-to-Drink) Improving Adherence

- Specialty Pharmacy and Patient-Support Hubs Improving Access

- Lifelong Diet Adherence Challenges: Reducing Real-World Effectiveness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Phenylketonuria accounted for 44.08% in 2025 and is projected to grow at 8.10% CAGR from 2026 to 2031, reflecting broadened age access and the arrival of a BH4 precursor approved for patients one month and older. PKU's share is supported by newborn screening penetration, which ensures early diagnosis and structured care across large health systems, while trial and registry evidence has demonstrated clinically meaningful reductions in phenylalanine with approved pharmacologic options. Outside PKU, maple syrup urine disease, homocystinuria, and tyrosinemia comprise a sizable minority of cases in treated populations in many regions and benefit from growing screening coverage . A new therapy for alkaptonuria, approved in 2025, has opened a first treatment path for a previously unmanaged ultra-rare condition, supported by a companion access program to extend availability in select countries . Policy updates and technology improvements are raising detection rates across certain Asia Pacific geographies, which will expand the patient funnel for both dietary and pharmacologic interventions through the forecast period.

PKU's leadership reflects an ecosystem that covers dietary management, BH4-pathway agents, and enzyme substitution, which together anchor outcomes-focused care pathways under specialist oversight. The enzyme therapy's United States and EU risk management frameworks include education and readiness measures for anaphylaxis management, which concentrate administration within trained centers and hubs. For homocystinuria, enzyme replacement and oral enzyme candidates have reported clinical progress and regulatory designations, with a Phase 3 program paused for manufacturing scale-up and pre-IND work continuing for an oral enzyme therapy. mRNA efforts targeting the same pathway have also received rare pediatric and orphan designations, indicating a broadening toolkit for long-term control. Taken together, these dynamics keep PKU at the forefront of the amino acid disorders treatment market while gradually addressing other indications in the disorder mix, and they support multi-year therapeutic innovation that balances safety, efficacy, and real-world adherence. PKU captured 44.08% of amino acid disorders treatment market share in 2025 as broader access and supportive care models reinforced uptake in newborn-screened cohorts.

Medical nutrition held 55.32% of revenue in 2025, with GMP-based and free amino acid formulations anchoring daily intake targets in pediatric and adult populations. Suppliers rolled out ready-to-drink formats with high vitamin D levels and lower volume per gram of protein equivalent, which reduced consumption burden and improved suitability for life and work routines. Innovation extended beyond PKU to include homocystinuria and maple syrup urine disease formulas with inulin and DHA, while ingredient platforms reduced phenylalanine content and improved gastrointestinal comfort for sensitive patients. European production investments modernized packaging and storage for powders, which supports hospital and retail workflows and reduces waste from sachet formats. Over the forecast period, the investigational and advanced category is projected to grow faster than the overall amino acid disorders treatment market as enzyme-replacement, oral enzyme, mRNA, and BH4-precursor approaches advance regulatory and manufacturing readiness.

Pharmacotherapy remains central to diet liberalization for many patients as a BH4 precursor with a broad United States and EU label expands options, and enzyme therapy continues to normalize phenylalanine for appropriate candidates within REMS frameworks. From 2025 to 2026, portfolio reassessments and program discontinuations in gene-editing underscore immune-barrier challenges in liver-directed delivery, which is encouraging a shift of investment toward modalities with nearer-term scalability . Medical nutrition will continue to anchor daily control in a wide patient base as advanced options expand, and improvements to palatability, density, and formats will keep medical foods essential to long-term management. The amino acid disorders treatment market size tied to investigational and advanced modalities is projected to expand alongside improved manufacturing and distribution readiness for parenteral and oral programs.

Geography Analysis

North America held 52.11% of revenue in 2025 and is expected to grow at a steady rate through 2031, supported by label expansions for enzyme therapy and approved BH4-precursor options that broaden community management pathways. The region benefits from strong specialist networks, integrated patient-support hubs, and manufacturer programs that enroll the vast majority of insured patients and reduce out-of-pocket costs for many commercially covered beneficiaries. Portfolio updates show that products facing generic competition have seen revenue pressure, while enzyme therapies and growth assets in rare-disease portfolios continue to climb. Provincial policy adjustments in Canada have refined coverage for medical foods and certain pharmacologic therapies, shaping first-line choices and referral patterns to exceptional access pathways. In the United States, education and monitoring requirements under REMS concentrate enzyme therapy use within trained centers, which aligns with limited distribution networks and integrated hubs for dispensing.

Europe maintains a large, treated base with universal newborn screening in key markets and region-wide approvals for both enzyme therapy and a BH4-precursor agent that covers infants through adults. Regulatory documents outline safety considerations, education requirements, and monitoring for hypophenylalaninemia, which are embedded into national risk management plans and patient education programs. European manufacturers have upgraded medical nutrition production capacity and packaging, which streamlines hospital and retail pharmacy logistics and supports consistent shelf availability. A therapy for alkaptonuria approved in 2025 demonstrates Europe's role in global orphan portfolios and companion access strategies that include multi-country free-goods programs in lower-income settings.

Asia Pacific is projected to post a 5.24% CAGR through 2031, with the largest boost from newborn screening expansion and higher inherited metabolic disease detection rates in China and several other countries that have scaled tandem mass spectrometry. Australia's national program is adding multiple conditions and has advanced additional lysosomal storage diseases through the ministerial decision pathway, which will produce incremental annual diagnoses and add to medical nutrition and pharmacotherapy demand. New Zealand extended funding for 14 phenylketonuria supplements in 2024, which supports adherence and continuity of care in a small patient population. In South America, access initiatives from manufacturers expand the availability of therapy in select countries, and similar programs in parts of the Middle East and Africa help patients where reimbursement remains limited. Across these regions, convergence on core gene lists in genomic newborn screening is likely to harmonize future protocols, which can standardize case finding and accelerate therapy uptake in the treatment of amino acid disorders.

- Abbott Laboratories

- Ajinomoto

- Arla Foods Ingredients

- Biomarin Pharmaceutical

- Cycle Pharmaceuticals

- Danone

- Dr. Schar

- Homology Medicines

- Mead Johnson / Reckitt

- Merck

- Nestle

- PTC Therapeutics

- Sobi

- Synlogic

- Takeda Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Orphan-drug approvals expanding treatable patient pool

- 4.2.2 Global newborn screening expansion increasing diagnosed base

- 4.2.3 Medical nutrition innovation (GMP-based, ready-to-drink) improving adherence

- 4.2.4 Specialty pharmacy and patient-support hubs improving access

- 4.2.5 Gut-targeted synthetic biotics enabling diet liberalization

- 4.2.6 Pipeline progress in BH4 precursors and multi-modal PKU therapies

- 4.3 Market Restraints

- 4.3.1 High therapy and medical food costs constraining access

- 4.3.2 Lifelong diet adherence challenges reducing real-world effectiveness

- 4.3.3 REMS/anaphylaxis risks limiting enzyme therapy uptake

- 4.3.4 Pipeline uncertainty (gene therapy/editing durability, program terminations)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Disorder Type

- 5.1.1 Phenylketonuria (PKU)

- 5.1.2 Maple Syrup Urine Disease (MSUD)

- 5.1.3 Homocystinuria (HCU)

- 5.1.4 Tyrosinemia

- 5.1.5 Arginase 1 Deficiency (ARG1-D)

- 5.2 By Treatment Modality

- 5.2.1 Medical Nutrition

- 5.2.2 Pharmacotherapy

- 5.2.3 Investigational/Advanced Modalities

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Parenteral/Subcutaneous

- 5.4 By Distribution Channel

- 5.4.1 Hospitals Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Abbott Nutrition

- 6.3.2 Ajinomoto

- 6.3.3 Arla Foods Ingredients

- 6.3.4 BioMarin Pharmaceutical Inc.

- 6.3.5 Cycle Pharmaceuticals

- 6.3.6 Danone Nutricia

- 6.3.7 Dr. Schar

- 6.3.8 Homology Medicines

- 6.3.9 Mead Johnson / Reckitt

- 6.3.10 Merck & Co., Inc.

- 6.3.11 Nestle Health Science

- 6.3.12 PTC Therapeutics

- 6.3.13 Sobi

- 6.3.14 Synlogic

- 6.3.15 Takeda Pharmaceutical

7 Market Opportunities & Future Outlook

- 7.1 White?space & unmet?need assessment