|

시장보고서

상품코드

2063737

남미의 판유리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Flat Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

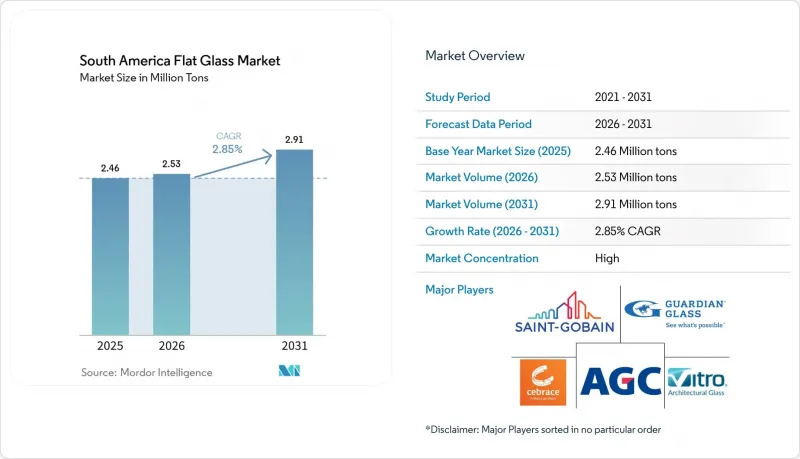

Mordor Intelligence에 의하면, 남미 판유리 시장 규모는 2025년 246만 톤에서 2026년에는 253만 톤으로 확대되어 2031년까지 291만 톤에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 2.85%로 성장할 전망입니다.

본 보고서는 제품 유형(어닐링 유리, 코팅 유리, 가공 유리, 거울 유리, 무늬 유리), 최종 사용자 산업(건축 및 건설, 자동차, 태양광 유리, 기타 최종 사용자 산업) 및 지역(브라질, 아르헨티나, 콜롬비아, 칠레, 페루 및 기타 남미)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제공됩니다.

남미 판유리 시장 동향과 인사이트

브라질 2급 도시의 건설 붐

상파울루나 리우데자네이루를 제외한 2급 도시권에서는 포화 상태에 이른 주요 시장과 비교해 공공 인프라에 대한 투자와 민간 부동산 자금의 유입이 가속화되고 있습니다. 쿠리치바, 벨루오리존치, 헤시피에서 발급된 건축 허가 건수는 2025년에 9%에서 14% 증가할 것으로 예상되며, 이는 약 18만 제곱미터의 파사드 면적 증가로 이어질 것으로 전망됩니다. 이 도시들의 개발업체들은 다른 지역에서 고급 Low-E 코팅이 인기를 끌고 있음에도 불구하고, 비용 효율이 뛰어난 어닐링 유리나 열강화 유리를 계속 우선시하고 있어 플로트 라인의 가동률을 안정적으로 유지하고 있습니다. 수요가 지리적으로 확대됨에 따라 생산자들은 지역 서비스 센터 설립을 서둘러야 하며, 운영 자금 수요는 증가하지만, 아시아 수출업체들이 적시 납품에 어려움을 겪고 있는 지역에서 고객 유지율을 높이는 데 기여합니다. 이러한 건설 수요 증가는 표준 기판에 대한 안정적인 수요를 뒷받침하는 한편, 가공 업체들이 마그네트론 스퍼터링 및 라미네이트 가공 능력을 확대할 수 있게 해줍니다.

지역 내 자동차 생산의 급속한 확대

스텔란티스는 2030년까지 총 62억 2,000만 달러 규모의 남미 제조 로드맵의 일환으로 아르헨티나 코르도바 공장에 3억 8,500만 달러를 투자했습니다. 이번 설비 현대화를 통해 연간 생산 능력이 5만 대 증가하여, 브라질, 파라과이, 우루과이와의 메르코수르(남미 공동시장) 무관세 무역을 뒷받침할 것입니다. 에탄올 연료 대응 기능과 전기 모터를 통합한 브라질의 하이브리드 플렉스 차량이 도입됨에 따라 방음 요구 사항이 높아지고 있으며, 이에 따라 더 크고 다층 구조의 전면 유리 및 측면 유리가 필요해지고 있습니다. 차량 1대당 유리 사용량은 8-12% 증가할 것으로 예상되며, 이에 따라 판유리 수요는 10-12%에 달하는 시장 점유율을 넘어 더욱 확대될 전망입니다. 그 결과, 자동차 시장의 성장에 힘입어 제조 투자가 강화 처리, 접합 유리 및 방음 중간막 분야로 집중되면서, 건설 수요가 둔화되는 시기에도 남미의 판유리 시장을 견고하게 뒷받침하고 있습니다.

소다회 및 LNG 가격 변동

2025년 4분기, 튀르키예의 카잔 소다 일렉트릭(Kazan Soda Electric)사의 수출 제한 조치로 인해 산토스의 소다회 가격은 전년 동기 대비 18% 상승했습니다. 한편, 페트로브라스는 2026년 1월, 유럽의 기준에 맞추어 액화천연가스(LNG) 요금을 22% 인상했습니다. 이러한 비용 상승으로 인해 플로트라인의 영업이익률은 200-300 베이시스 포인트 하락했습니다. 각 개발사는 이러한 비용을 감당하거나 알루미늄이나 폴리카보네이트 등의 대체 소재로 전환해야 하는 선택의 기로에 놓였고, 그 결과 유리 수요가 감소했습니다. 헤지 수단이 없는 소규모 용해로는 개조를 연기했고, 장기 소다회 계약이나 LNG 스왑 계약을 맺고 있는 다국적 기업들에 의한 소유권 통합이 가속화되었습니다.

부문별 분석

2025년 남미 판유리 시장에서 어닐드 유리 시장 규모는 총 생산량의 79.32%를 차지했습니다. 여전히 지배적인 위치를 차지하고 있는 가공 유리는 2031년까지 연평균 성장률(CAGR) 3.65%를 나타낼 것으로 예측에 따라, 그 시장 점유율은 감소할 것으로 전망됩니다. 복합유리와 강화유리는 브라질 북동부의 허리케인 내성 기준을 충족하며, 한편 Low-E 코팅은 칠레의 열 성능 기준인 Decreto N05를 준수합니다. 가디언 글라스(Guardian Glass)나 산고반(Saint-Gobain)과 같은 제조업체들은 일사열 획득률이 0.35 미만이어야 하는 ‘Minha Casa Minha Vida(마이 카사 마이 비다)’ 프로젝트에 대응하기 위해 트리플 실버 스퍼터링 라인을 도입하고 있습니다. 가공 유리는 이익률이 높아 원자재 가격 변동을 상쇄하며, 판매량이 점차 증가하고 있음에도 불구하고 가격 결정력을 유지하고 있습니다.

세브라세(Cebrace)의 ‘아토모스(Atmos)’ 저탄소 시리즈는 내재된 탄소 배출량을 50% 줄여, 1제곱미터당 약 5kg의 CO2로 억제하고 있습니다. 이는 콜롬비아의 ‘에너지 및 환경 설계 리더십(LEED)’ 및 ‘고효율 설계 우수성(EDGE)’ 인증 기준을 준수하며, 해당 국가에서는 법률 1715/2014에 따라 에너지 절약 투자에 대해 50%의 세액 공제가 인정되고 있습니다. 거울 유리나 무늬가 들어간 유리는 여전히 틈새 시장으로, 장식용이나 자동차 백미러용으로 공급되고 있습니다. 가공 제품 수요가 증가함에 따라, 어닐링 처리된 유리의 가격은 하락세를 보이고 있습니다. 이는 산고반의 2025년 결산 실적에서도 드러나는데, 라틴아메리카의 매출액은 13.5% 증가한 반면, 판매량은 8% 증가에 그쳐 제품 구성의 대폭적인 변화를 보여주고 있습니다. 이러한 추세에 따라, 가공 기판은 남미 판유리 시장에서 주요 성장 동력으로서의 입지를 확고히 다져가고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the south america flat glass market size is expected to increase from 2.46 Million tons in 2025 to 2.53 Million tons in 2026 and reach 2.91 Million tons by 2031, growing at a CAGR of 2.85% over 2026-2031.

This report is Segmented by Product Type (Annealed Glass, Coated Glass, Processed Glass, Mirror Glass, and Patterned Glass), End-User Industry (Building and Construction, Automotive, Solar Glass, and Other End-User Industries), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons).

South America Flat Glass Market Trends and Insights

Construction Boom in Tier-2 Brazilian Cities

Secondary metropolitan areas outside Sao Paulo and Rio de Janeiro are receiving public infrastructure investments and private real estate funding at a faster pace compared to the saturated primary markets. Building permits issued in Curitiba, Belo Horizonte, and Recife increased by 9% to 14% in 2025, contributing an estimated 180,000 square meters of facade area. Developers in these cities continue to prioritize cost-effective annealed and heat-strengthened glass, ensuring consistent float-line utilization, even as premium low-E coatings gain popularity in other regions. The geographic spread of demand requires producers to establish regional service centers, increasing working capital needs but enhancing customer retention in areas where Asian exporters face challenges in providing just-in-time deliveries. This construction growth supports stable demand for standard substrates while allowing processors to expand magnetron-sputtering and laminating capabilities.

Rapid Scale-Up of Regional Automotive Output

Stellantis has allocated USD 385 million for its Cordoba, Argentina facility as part of its USD 6.22 billion South America manufacturing roadmap through 2030. This upgrade will boost capacity by 50,000 units annually, supporting Mercosur duty-free trade into Brazil, Paraguay, and Uruguay. Brazil's hybrid-flex vehicle rollout, which integrates ethanol capability with electric motors, is increasing acoustic requirements, necessitating larger, multi-layer windshields and side glazing. Glass content per vehicle is expected to grow by 8-12%, further driving flat-glass demand beyond its 10-12% volume share. Consequently, automotive growth is directing fabrication investments toward tempering, lamination, and acoustic interlayers, strengthening the South America flat glass market even during construction slowdowns.

Volatile Soda-Ash and LNG Prices

Soda-ash prices at Santos increased by 18% year-on-year in Q4 2025 due to export restrictions from Turkey's Kazan Soda Elektrik, while Petrobras raised liquefied natural gas tariffs by 22% in January 2026, aligning with European benchmarks. These cost increases reduced float-line operating margins by 200-300 basis points. Developers were forced to either absorb these costs or switch to alternative materials like aluminum and polycarbonate, reducing glass demand. Smaller furnaces without hedging mechanisms delayed rebuilds, accelerating ownership consolidation among multinationals with long-term soda-ash contracts and LNG swaps.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Utility-Scale Solar Farms

- Government Green-Building Tax Incentives

- Rising Low-Cost Imports from Asia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The South America flat glass market size for annealed glass accounted for 79.32% of the total volume in 2025. Although still dominant, its share is expected to decline as processed glass is projected to grow at a 3.65% CAGR through 2031. Laminated and tempered glass meet hurricane code requirements in Brazil's Northeast, while low-E coatings comply with Chile's Decreto N05 thermal-performance standards. Producers like Guardian Glass and Saint-Gobain have installed triple-silver sputtering lines to cater to Minha Casa Minha Vida projects, which require solar heat-gain coefficients below 0.35. Processed glass offers higher margins, offsetting feedstock volatility and providing pricing power despite gradual volume increases.

Cebrace's Atmos low-carbon series reduces embedded emissions by 50% to approximately 5 kg CO2 per square meter, aligning with Leadership in Energy and Environmental Design (LEED) and Excellence in Design for Greater Efficiencies (EDGE) certifications in Colombia, where Law 1715/2014 allows 50% tax deductions for efficiency investments. Mirror and patterned glass remain niche, catering to decor and automotive rear-view mirrors. As processed products gain traction, annealed glass pricing softens, as seen in Saint-Gobain's 2025 results, where Latin America revenue increased by 13.5% against an 8% volume rise, indicating a significant product mix shift. This trend positions processed substrates as the primary growth driver for the South America flat glass market.

List of Companies Covered in this Report:

- AGC Inc.

- AGP sGlass

- Cebrace Cristal Plano Ltda.

- Guardian Industries, LLC

- Nippon Sheet Glass Co. Ltd

- Saint-Gobain

- SCHOTT AG

- Sisecam

- Vitro

- VIVIX

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction boom in Tier-2 Brazilian cities

- 4.2.2 Rapid scale-up of regional automotive output

- 4.2.3 Expansion of utility-scale solar farms

- 4.2.4 Government green-building tax incentives

- 4.2.5 On-shoring of ultra-thin display glass lines

- 4.3 Market Restraints

- 4.3.1 Volatile soda-ash and LNG prices

- 4.3.2 Rising low-cost imports from Asia

- 4.3.3 Stricter furnace-emission regulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Annealed Glass

- 5.1.2 Coater Glass

- 5.1.3 Processed Glass

- 5.1.4 Mirror Glass

- 5.1.5 Patterned Glass

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Solar Glass

- 5.2.4 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Chile

- 5.3.5 Peru

- 5.3.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 AGP sGlass

- 6.4.3 Cebrace Cristal Plano Ltda.

- 6.4.4 Guardian Industries, LLC

- 6.4.5 Nippon Sheet Glass Co. Ltd

- 6.4.6 Saint-Gobain

- 6.4.7 SCHOTT AG

- 6.4.8 Sisecam

- 6.4.9 Vitro

- 6.4.10 VIVIX

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment