|

시장보고서

상품코드

2063742

남미의 저밀도 폴리에틸렌(LDPE) 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Low-Density Polyethylene (LDPE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

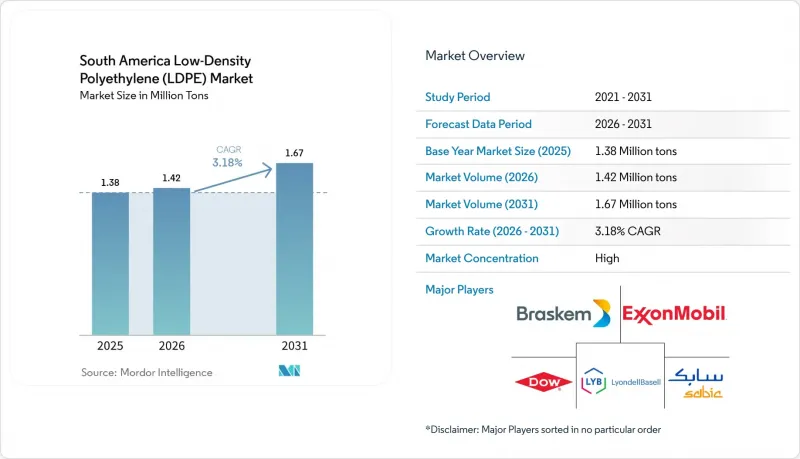

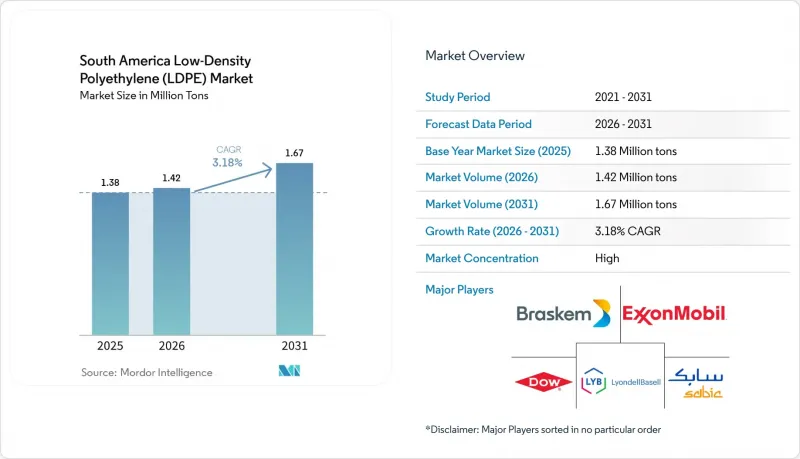

Mordor Intelligence에 의하면, 남미 저밀도 폴리에틸렌(LDPE) 시장 규모는 2025년 138만 톤, 2026년 142만 톤으로부터, 2031년까지 167만 톤으로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 3.18%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(시트·필름, 블로우 성형, 사출 성형, 압출 코팅, 기타), 최종 사용자 산업(포장, 농업, 자동차, 전기 및 전자, 기타) 및 지역(브라질, 아르헨티나, 콜롬비아, 칠레, 페루 및 기타 남미)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

남미 저밀도 폴리에틸렌(LDPE) 시장 동향 및 인사이트

자동차 분야에서 경량 플라스틱 채택을 위한 정부의 인센티브 시행

브라질의 ‘Programa Mover’는 차량 중량을 줄이는 기술에 매년 35억-41억 레알을 투자하고 있으며, 재활용 가능성 기준을 의무화하고, 해당 기준을 충족하는 모델에 대해 차별화된 과세를 실시했습니다. 자동차 제조업체들은 금속과 유리를 LDPE 기반 인테리어 필름으로 대체함으로써 차량 중량을 5%-8% 줄이고, 연비를 최대 5% 향상시키고 있습니다. 라디치 그룹은 2025년 3월, Tier 1 공급업체를 대상으로 한 폴리머 컴파운드 공급을 현지화하기 위해 1만 7,000제곱미터 규모의 공장을 설립했습니다. 아르헨티나의 OEM(주문자 상표 제조) 플랫폼은 2027년까지 동등한 기준을 준수할 준비를 진행 중이며, 수요는 브라질 국외로도 확대되고 있습니다. 향후 2-4년간의 전망은 차량 플랫폼의 재설계 주기와 검증 프로토콜을 반영한 것입니다.

브라질 내 연포장 변환 업체의 확대

브라질의 각 변환기 제조업체들은 급성장하는 전자상거래 및 식품 배달 시장 수요에 선제적으로 대응하기 위해 고생산성 생산 라인을 도입하고 있습니다. 봄플라스틱(Bomplastic)의 Comexi F2 MB 압출기는월350톤의 고차단 필름을 생산하고 있으며, 한편 COEXPAN-EMSUR의 준디아이 공장은 2024년에 가동을 시작하여 남동 회랑 지역공급 체제를 강화했습니다. 오벤 그룹의 비토펠 인수는 강력한 BOPP 제품군을 추가함으로써 밀봉층 사업을 둘러싼 경쟁을 심화시키고 있습니다. 시트 및 필름은 이미 남미 LDPE 생산량의 거의 절반을 차지하고 있으며, 생산 라인의 급속한 증산은 일반적으로 12-18개월 내에 정격 생산 능력에 도달하기 때문에 남미의 저밀도 폴리에틸렌(LDPE) 시장에 단기적인 호재가 될 것으로 보입니다.

LLDPE 대체재 및 신흥 생분해성 필름

필름 가공업체들은 내천자성과 두께를 얇게 만들 수 있다는 점을 이유로 선형 저밀도 폴리에틸렌(LLDPE)을 선호하여 사용하고 있습니다. 브라질 창고에 자동 팔레트 래퍼를 도입함으로써, 스트레치 후드 필름에 사용되는 LDPE의 사용량은 이미 약 15% 감소했습니다. 생분해성 폴리젖산(PLA) 및 폴리하이드록시알카노에이트(PHA) 소재는 고급 일회용 식품 포장, 특히 칠레의 소매 시범 사업에서 주목을 받고 있지만, 수지 가격의 급등과 퇴비화 인프라의 부족으로 인해 그 사용량은 여전히 극히 미미한 수준입니다. 변환기 설비 교체에는 보통 2년이 소요되므로, 이것이 남미의 저밀도 폴리에틸렌(LDPE) 시장에 대한 중기적인 제약 요인으로 작용하고 있습니다.

부문별 분석

시트 및 필름은 2025년에 해당 지역의 LDPE 생산량의 48.37%를 차지해, 2031년까지 연평균 성장률(CAGR) 3.46%로 증가할 것으로 전망됩니다. Bomplastic사의월350톤 생산 라인과 COEXPAN-EMSUR사의 생산 확대에 힘입어, 풀필먼트 센터를 통해 고투명 오버랩 필름 수요를 주도하는 브라질 남동부 지역으로공급이 강화되고 있습니다. 브라질의 세라두 지역과 아르헨티나의 팜파 지역에서 사용되는 농업용 멀칭 필름 역시 이 부문의 남미 저밀도 폴리에틸렌(LDPE) 시장 규모에 기여하고 있습니다. 블로우 성형 병은 브랜드 소유주들이 비용 측면에서 압출 성형이 가능한 형태로(고밀도 폴리에틸렌) 전환하고 있기 때문에 시장 점유율 증가세가 주춤하고 있습니다. 한편, 접을 수 있는 화장품용 튜브는 LDPE의 유연성과 부드러운 촉감 덕분에 여전히 확고한 입지를 유지하고 있습니다.

오벤 그룹의 비토펠 인수를 계기로, 이축연신 폴리프로필렌(BOPP)(BOPP) 제조업체들이 LDPE의 타의 추종을 불허하는 핫택 범위를 이유로 LDPE 밀봉층 시장에 진출함에 따라 경쟁이 치열해지고 있습니다. 전체 수요의 불과 7%를 차지하는 사출 성형용 등급은 최종 사용자의 비용 절감 기조로 인해 폴리프로필렌으로의 대체가 진행되고 있지만, 확실한 부정 개봉 방지 기능이 필요한 고급 캡 분야에서는 여전히 호조를 보이고 있습니다. 액체용 카톤 분야에서는 압출 코팅이 견조한 실적을 유지하고 있지만, 상온 보관이 가능한 유제품 분야에서는 폴리에틸렌 테레프탈레이트(PET) 기반 라미네이트가 성장하고 있습니다. 이러한 추세들이 복합적으로 작용함에 따라, 2031년까지 남미의 저밀도 폴리에틸렌(LDPE) 시트 및 필름 시장 점유율은 계속해서 확고한 우위를 유지할 것으로 전망됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the south america low-Density polyethylene market size is projected to expand from 1.38 Million tons in 2025 and 1.42 Million tons in 2026 to 1.67 Million tons by 2031, registering a CAGR of 3.18% between 2026 to 2031.

This report is Segmented by Product Type (Sheets and Films, Blow-Molded, Injection-Molded, Extrusion Coating, and Other Product Types), End-User Industry (Packaging, Agriculture, Automotive, Electrical and Electronics, and More), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons).

South America Low-Density Polyethylene (LDPE) Market Trends and Insights

Implementation of Government Incentives for Lightweight Plastic Adoption in Automotive

Brazil's Programa Mover injects BRL 3.5-4.1 billion each year into technologies that cut vehicle weight, mandating recyclability thresholds and differentiated taxation for compliant models. Automakers are substituting metal and glass with LDPE-based interior films, reducing curb weight by 5%-8% and improving fuel economy by as much as 5%. RadiciGroup's 17,000 m2 plant opened in March 2025 to localize polymer-compound supply for tier-one suppliers. Argentine original equipment manufacturer (OEM) platforms are preparing to align with comparable standards by 2027, extending demand beyond Brazil. The 2-to-4-year horizon reflects vehicle-platform redesign cycles and validation protocols.

Expansion of Flexible-Packaging Converters in Brazil

Brazilian converters are installing high-output lines to preempt demand from rapid e-commerce and food-delivery growth. Bomplastic's Comexi F2 MB press contributes 350 tons per month of high-barrier film, while COEXPAN-EMSUR's Jundiai plant went on-stream in 2024, strengthening supply in the southeast corridor. Oben Group's purchase of Vitopel intensifies contest for sealant-layer business by adding a strong BOPP portfolio. Sheets and films already claim nearly half of South American LDPE volume, and rapid line ramp-ups usually reach nameplate in 12-18 months, underscoring the short-term boost to the South America Low-Density Polyethylene (LDPE) market.

Substitution by LLDPE and Emerging Biodegradable Films

Film processors prefer Linear Low-Density Polyethylene (LLDPE) for puncture resistance and downgauging; automated pallet-wrappers in Brazil's warehouses have already cut LDPE usage in stretch-hood films by about 15%. Biodegradable polylactic acid (PLA) and polyhydroxyalkanoate (PHA) structures are gaining traction in premium single-use food packaging, especially in Chilean retail pilots, but high resin premiums and scarce composting infrastructure keep volumes marginal. Converter re-tooling typically takes two years, explaining the medium-term drag on the South America Low-Density Polyethylene (LDPE) market.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Upgrades Opening New Pipe-Coating Demand Corridors

- E-Commerce Boom Accelerating Stretch-Film Consumption

- Feedstock (Ethylene) Price Volatility Linked to Regional Naphtha Differentials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sheets and films captured 48.37% of regional LDPE volume in 2025 and are forecast to rise at a 3.46% CAGR through 2031. Bomplastic's 350 tons per month line and COEXPAN-EMSUR's ramp-up feed Brazil's southeast, where fulfillment centers dictate demand for high-clarity overwraps. Agricultural mulch films in Brazil's Cerrado and Argentina's Pampas also contribute to the South America Low-Density Polyethylene (LDPE) market size for this segment. Blow-molded bottles trail because brand owners shift squeezable formats to (High-Density Polyethylene) for cost reasons, while collapsible cosmetic tubes keep a foothold for LDPE's flexibility and soft-touch feel.

Oben Group's Vitopel takeover escalates competition as Biaxially Oriented Polypropylene (BOPP) producers pursue LDPE sealant layers given the latter's unmatched hot-tack range. Injection-molding grades, only 7% of demand, face polypropylene substitution amid end-user cost discipline, but still thrive in premium closures that need secure tamper evidence. Extrusion-coating remains steady in liquid cartons, though Polyethylene Terephthalate (PET)-based laminates grow in shelf-stable dairy. Together these dynamics keep the South America Low-Density Polyethylene (LDPE) market share for sheets and films firmly ahead through 2031.

List of Companies Covered in this Report:

- ALPA Group

- Borealis AG

- Braskem SA

- Chevron Phillips Chemical Company

- Dow

- Exxon Mobil Corporation

- INEOS

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals Inc.

- Osterman Company

- SABIC

- Sasol

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of government incentives for lightweight plastic adoption in automotive

- 4.2.2 Expansion of flexible-packaging converters in Brazil

- 4.2.3 Infrastructure upgrades opening new pipe-coating demand corridors

- 4.2.4 E-commerce boom accelerating stretch-film consumption

- 4.2.5 Bio-LDPE capacity build-out at Braskem's Triunfo complex

- 4.3 Market Restraints

- 4.3.1 Substitution by LLDPE and emerging biodegradable films

- 4.3.2 Feed-stock (ethylene) price volatility linked to regional naphtha differentials

- 4.3.3 PCR-content limits above 20% degrading mechanical properties

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Sheets and Films

- 5.1.2 Blow-Molded

- 5.1.3 Injection-Molded

- 5.1.4 Extrusion Coating

- 5.1.5 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Packaging

- 5.2.2 Agriculture

- 5.2.3 Automotive

- 5.2.4 Electrical and Electronics

- 5.2.5 Construction

- 5.2.6 Healthcare

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Chile

- 5.3.5 Peru

- 5.3.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ALPA Group

- 6.4.2 Borealis AG

- 6.4.3 Braskem SA

- 6.4.4 Chevron Phillips Chemical Company

- 6.4.5 Dow

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 INEOS

- 6.4.8 LyondellBasell Industries Holdings B.V.

- 6.4.9 Mitsui Chemicals Inc.

- 6.4.10 Osterman Company

- 6.4.11 SABIC

- 6.4.12 Sasol

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment