|

시장보고서

상품코드

2063751

알레르기성 비염 치료제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Allergic Rhinitis Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

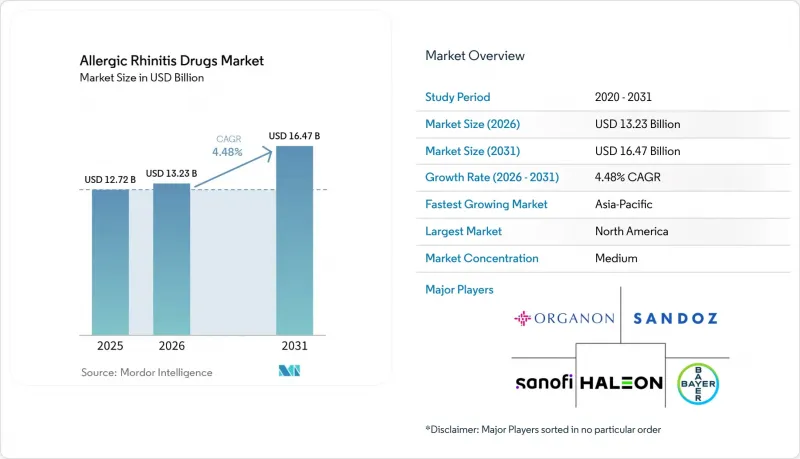

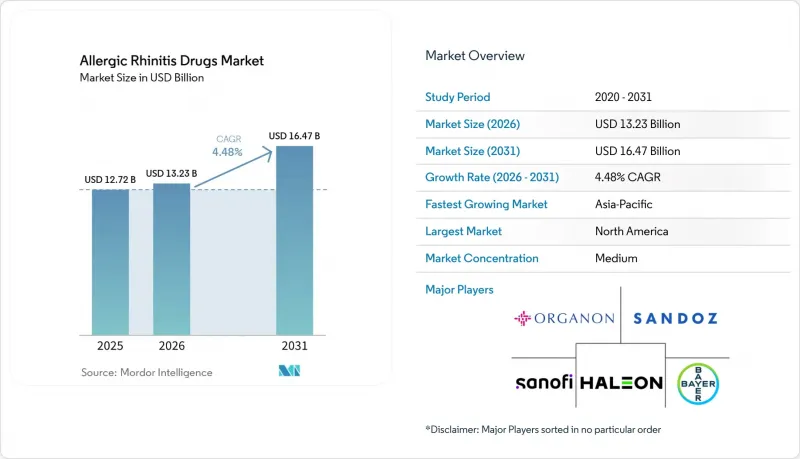

Mordor Intelligence에 의하면, 알레르기성 비염 치료제 시장 규모는 2025년에 127억 2,000만 달러로 평가되었고 2026년 132억 3,000만 달러에서 2031년까지 164억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.48%를 나타낼 전망입니다.

본 보고서는 약물 분류별(항히스타민제, 면역요법, 코르티코스테로이드 등), 제형별(정제 및 캡슐, 액제·시럽, 비강 스프레이, 비강 점적제 등), 처방 현황(일반의약품, 처방약), 유통 채널(드럭스토어 및 소매 약국, 병원 약국 등), 지역(북미 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 알레르기성 비염 치료제 시장 동향 및 인사이트

꽃가루 시즌의 장기화로 증상 부담이 커지고 있습니다.

1990년 이후, 미국의 꽃가루 시즌은 약 3주 정도 길어졌으며, 봄이 더 일찍 찾아오고 가을 첫 서리가 내리는 시기가 늦어지고 있습니다. 유럽에서도 비슷한 추세가 나타나고 있으며, 꽃가루 비산 시기는 20년 전보다 1-2주 정도 빨라졌습니다. 꽃가루에 노출되는 기간이 길어짐에 따라, 많은 계절성 알레르기 환자들이 1년 중 더 긴 기간 동안 약을 복용하게 되었습니다. 또한, 산업안전보건규정에 따라 고용주는 졸음을 유발하는 구식 약제 대신, 진정 작용이 없는 항히스타민제나 즉효성이 있는 비강 스프레이를 권장하도록 권고받고 있습니다. 이러한 요인들이 복합적으로 작용하여, 환자들은 하루 한 번 복용하는 류코트리엔 정제나 심지어 수년에 걸친 설하 면역요법을 받게 되며, 그 결과 환자 1인당 연간 지출이 증가하고 있습니다.

대기 오염은 증상의 심각도와 지속 기간을 악화시킵니다.

미세 입자상 물질과 이산화질소는 꽃가루 입자의 부착성을 높이고 자극성을 강화하기 때문에 알레르기성 비염 증상을 악화시킵니다. 싱가포르에서는 주민의 85%에서 90%가 집먼지진드기에 과민반응을 보이며, 습도가 높은 중국의 연안 도시에서도 절반 이상의 사람들이 양성 반응을 보이고 있습니다. 잡초 꽃가루, 특히 쑥과 돼지풀의 경우, 중국 북부에서 실시한 피부 검사에서 최대 50%의 양성률을 보였습니다. 인도에서는 알레르기성 비염의 유병률이 20%에서 30%에 달하며, 일부 지역에서는 파르테니움 꽃가루가 환자의 최대 3분의 1에게 영향을 미치고 있습니다. 대기 오염의 악화는 코 점막을 자극하여 증상이 급격히 악화되거나 회복 기간이 길어지게 하므로, 아시아·태평양 지역이 다른 어느 지역보다 빠르게 성장할 것으로 예측되는 이유 중 하나입니다.

경구용 페닐레프린에 대한 FDA의 조치가 충혈 완화제 시장을 위축시키고 있습니다.

2024년 하반기, FDA는 자문위원회가 표준 용량인 10mg이 효과가 없다고 판단한 데 따라, 경구용 페닐에프린을 OTC(일반의약품) 목록에서 제외할 것을 제안했습니다. 이 결정은 수백 가지에 달하는 다양한 증상에 대응하는 감기·알레르기용 정제 시장에 타격을 줄 것이며, 각 제약사들로 하여금 처방 변경이나 시장 철수를 강요하게 될 것입니다. 프소이도에페드린은 여전히 효과가 있지만, 메탄페타민 규제로 인해 매장 판매가 제한되어 있어 충동 구매가 억제되고 있습니다. 일부 기업들은 옥시메타졸린 등의 비강 스프레이에 주목하고 있지만, 사용을 시작한 지 불과 며칠 만에 반동성 코막힘이 발생할 위험이 있어 장기적인 수요는 제한되고 있습니다. Haleon과 같은 다각화 기업은 항히스타민제와 스테로이드의 복합제로 사업을 전환할 수 있지만, 페닐레프린에 의존하던 소규모 브랜드는 진열 공간 축소와 이익률 압박에 직면하게 될 것입니다.

부문별 분석

항히스타민제는 2025년 알레르기성 비염 치료제 시장 규모의 39.52%를 차지하며 최대 점유율을 기록했으나, 류코트리엔 수용체 길항제와 바이오의약품은 2031년까지 연평균 성장률(CAGR) 5.87%로 더 빠르게 성장하고 있습니다. 2세대 경구용 약물은 여전히 일상적인 주력 제품이지만, 박스 경고 및 새로운 IL-4/IL-13 억제제의 등장으로 인해 임상의들의 치료 알고리즘이 재구성되고 있습니다. 듀필마브의 새로운 부비동염 적응증은 생물학적 제제가 높은 보험 급여율을 바탕으로 틈새 시장을 개척할 수 있음을 보여줍니다. 경쟁 압력으로 인해 혁신적인 제약 기업들은 이중 작용형 스프레이 및 새로운 작용기전에 대한 개발을 추진하는 한편, 제네릭 의약품은 대량으로 판매되는 항히스타민제의 가격 경쟁력을 유지하고 있어, 알레르기성 비염 치료제 시장은 ‘접근성’과 ‘혁신성’의 균형을 유지하고 있습니다.

기존의 충혈 완화제는 불투명한 상황에 직면해 있으며, 신속한 증상 완화와 항염증 효과를 겸비한 복합 비강 스프레이로의 전환이 가속화되고 있습니다. 설하 면역요법은 소아 대상 데이터와 간소화된 EU 임상시험 지침을 통해 신뢰성을 높여가고 있으며, 비록 낮은 수준이긴 하지만 질환 수정 치료제 시장에서 알레르기성 비염 치료제 점유율 확대를 위한 입지를 점차 확립해 나가고 있습니다.

정제나 캡슐 등의 경구 제형은 2025년 매출의 약 46.87%를 차지하고 있으며, 이는 1일 1회 투여하는 정제에 대한 소비자들의 편의성 평가를 반영한 것입니다. 그러나 코 스프레이와 설하정이 혁신의 주역으로 부상하며, 즉각적인 효과와 주사 없이 진행되는 질환 수정 치료를 원하는 환자들의 요구에 부응함으로써 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 알레르기성 비염 치료제 시장에서 스프레이 제제 시장 점유율은 OTC(일반의약품)로의 전환에 힘입어 확대되고 있는 반면, 설하 면역요법(SLIT) 정제는 새로운 소아 적응증 승인으로 인해 수혜를 보고 있습니다.

주사제(SCIT)는 치료가 필요한 틈새 시장을 유지하고 있지만, 시간적 부담이 보급을 저해하고 있습니다. 한편, 캐나다 보건부의 비강용 에피네프린 스프레이 승인은 환자들이 필요에 따라 기구 없이 투여할 수 있는 방법에 큰 관심을 보이고 있음을 보여줍니다. 이러한 동향은 알레르기성 비염 치료제 시장에서 제형의 다양화가 앞으로도 계속될 것임을 시사합니다.

지역별 분석

북미는 여전히 최대의 지역 거점이며, 생물학적 제제의 보험 적용 및 정착된 OTC 문화에 힘입어 2025년 매출의 38.95%를 차지하지만, CMS(미국 의료보험서비스센터)에 의한 보상 체계 축소 및 페닐레프린의 보험 적용 제외가 단기적인 상승 여력을 억제하고 있습니다. 꽃가루 시즌이 길어짐에 따라 치료 기간이 연장되면서, 알레르기성 비염 치료제 시장은 기존의 봄철 성수기를 넘어 확대되고 있습니다. 캐나다에서 바늘 없는 에피네프린 및 소아용 SLIT의 승인은 새로운 투여 방식에 대한 규제 당국의 수용성을 보여주는 반면, 멕시코에서는 도시화가 진행되고 민간 보험의 보급을 배경으로 수요가 확대되고 있습니다.

유럽에서는 비강 스테로이드제나 면역요법이 보험 적용 범위에 널리 포함되어 있어 긍정적인 요인으로 작용하고 있지만, 각국의 처방약 목록이 다르기 때문에 도입 현황에 차이가 나타나고 있습니다. 독일에서 SLIT에 대한 전액 보험 적용은 영국의 NHS가 시행하는 선택적 보험 적용과 대조를 이루며, 알레르기성 비염 치료제 시장의 상황에 불균일한 양상을 초래하고 있습니다. EMA의 적은 표본 수에 대한 지침은 중소 제조업체 시장 진입을 용이하게 했으며, 알레르기 시즌을 앞두고 OTC용 듀얼 액션 제품을 출시한 것은 신속한 상품화를 보여주고 있습니다.

아시아태평양은 많은 연안 도시에서 집먼지진드기에 대한 감작률이 85%를 초과하고, 중국 북부에서는 잡초 꽃가루 양성률이 상승하고 있는 점으로 미루어 볼 때, 연평균 성장률(CAGR) 5.21%로 가장 빠르게 성장하고 있는 시장입니다. 글렌마크사의 ‘라이알트리스’가 중국에서 승인을 받았고, SLIT와 관련하여 다국적 기업들간의 제휴가 이루어진 것은 고가 스프레이와 면역요법의 추가적인 확산을 예고하지만, 합리적인 가격이라는 제약으로 인해 제네릭 의약품이 여전히 중요한 역할을 하고 있습니다. 중국, 일본, 한국의 규제 당국은 소아용 제제의 심사를 신속히 진행하고 있으며, 이에 따라 알레르기성 비염 치료제 시장은 더욱 확대되고 있습니다. 중동 및 아프리카와 남미는 뒤처져 있지만, 가처분 소득 증가에 따라 도시 지역을 중심으로 성장이 가속화되는 지역이 나타나고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the allergic rhinitis drugs market size was valued at USD 12.72 billion in 2025 and is estimated to grow from USD 13.23 billion in 2026 to reach USD 16.47 billion by 2031, at a CAGR of 4.48% during the forecast period (2026-2031).

This report is Segmented by Drug Class (Antihistamines, Immunotherapy, Corticosteroids, and More), Dosage Form (Tablets & Capsules, Liquids & Syrups, Nasal Sprays, Nasal Drops, and More), Prescription Status (OTC, Rx), Distribution Channel (Drugstores & Retail Pharmacies, Hospital Pharmacies, and More), and Geography (North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Allergic Rhinitis Drugs Market Trends and Insights

Longer Pollen Seasons Intensify Symptom Burden

Since 1990, the U.S. pollen season has lengthened by roughly three weeks, with spring arriving earlier and the first fall frost coming later. Europe shows a similar trend, with pollen counts now starting one to two weeks sooner than they did twenty years ago. A longer exposure window pushes many seasonal sufferers to take medicine for a larger part of the year. Work-safety rules also nudge employers to recommend non-sedating antihistamines and fast-acting nasal sprays instead of older, drowsiness-inducing drugs. Together, these forces steer patients toward once-daily leukotriene tablets or even multi-year sublingual immunotherapy, which lifts annual spending per patient.

Air Pollution Exacerbates Symptom Severity and Duration

Fine particles and nitrogen dioxide make pollen grains stickier and more irritating, which worsens allergic rhinitis symptoms. In Singapore, house-dust-mite sensitization touches 85% to 90% of residents, and more than half of people in humid Chinese coastal cities test positive as well. Weed pollen, particularly mugwort and ragweed, reaches up to 50% positivity in northern China skin tests. India shows a 20% to 30% allergic-rhinitis rate, with Parthenium pollen affecting up to one-third of patients in some regions. Elevated air pollution primes the nasal lining for quicker flare-ups and longer recovery, helping to explain why Asia-Pacific is projected to grow faster than any other region.

FDA Move Against Oral Phenylephrine Undercuts Decongestants

In late 2024, the FDA proposed pulling oral phenylephrine from the OTC monograph after advisors ruled the standard 10 mg dose ineffective. This ruling threatens hundreds of multi-symptom cold-and-allergy tablets and forces drugmakers to reformulate or exit the aisle. Pseudoephedrine still works but stays behind the counter because of methamphetamine controls, limiting spontaneous buys. Some companies are eyeing topical sprays such as oxymetazoline, yet the risk of rebound congestion after just a few days of use tempers long-term demand. Diversified firms like Haleon can pivot to antihistamine-steroid blends, while smaller brands that leaned on phenylephrine face shelf cuts and tighter margins.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce and Online Pharmacies Expand OTC Access

- Rx-to-OTC Switches and Dual-Action Combination Sprays

- Montelukast Boxed Warning Cools Prescriber Enthusiasm

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Antihistamines generated the largest allergic rhinitis drugs market size with 39.52% contribution in 2025, yet leukotriene receptor antagonists and biologics are escalating faster with 5.87% CAGR through 2031. Second-generation oral agents remain everyday staples, but boxed warnings and emerging IL-4/IL-13 inhibitors reshape clinician algorithms. Dupilumab's new rhinosinusitis label shows biologics can carve specialized niches with high reimbursement acceptance. Competitive pressure pushes innovators toward dual-action sprays and novel pathways, while generics sustain affordability for volume-driven antihistamines, keeping the allergic rhinitis drugs market balanced between accessibility and innovation.

Legacy decongestants face uncertainty, accelerating the pivot to combination nasal sprays that merge rapid relief with anti-inflammatory efficacy. Sublingual immunotherapy gains credibility through pediatric data and streamlined EU trial guidance, positioning the class to lift the allergic rhinitis drugs market share of disease-modifying treatments albeit from a low base.

Oral dosage forms such as tablets & capsules commanded nearly 46.87% share of 2025 revenue, reflecting the convenience premium consumers place on once-daily tablets. Yet nasal sprays and sublingual tablets headline innovation, posting the highest CAGRs as they align with patient desires for rapid onset or needle-free disease modification. The allergic rhinitis drugs market share for sprays is fortified by OTC switches, while SLIT tablets benefit from new pediatric indications.

Injectable SCIT retains a procedural niche but carries time burdens that hinder uptake; conversely, Health Canada's approval of a nasal epinephrine spray highlights patient enthusiasm for on-demand, device-free delivery modalities. These dynamics signal continued diversification of formats inside the allergic rhinitis drugs market.

Geography Analysis

North America remains the largest regional node, responsible for 38.95% of 2025 revenue, buoyed by insurance coverage for biologics and entrenched OTC culture, but CMS fee-schedule cuts and phenylephrine delisting temper near-term upside. Longer pollen seasons extend treatment windows, enlarging the allergic rhinitis drugs market beyond traditional spring peaks. Canada's approval of needle-free epinephrine and pediatric SLIT underscores regulatory openness to novel delivery, while Mexico's urbanization enlarges demand against a backdrop of rising private insurance.

Europe benefits from broadly reimbursed intranasal steroids and immunotherapy, yet national formularies vary, influencing uptake heterogeneity. Germany's full SLIT reimbursement contrasts with selective NHS coverage in the UK, shaping an uneven allergic rhinitis drugs market landscape. The EMA's low-sample guideline eases smaller-manufacturer entry, and OTC dual-action launches ahead of allergy seasons illustrate agile commercialization.

Asia-Pacific is the fastest-growing arena at 5.21% CAGR as house-dust-mite sensitization surpasses 85% in many coastal cities and weed-pollen positivity rises in northern China. Glenmark's China approval for Ryaltris and multinational alliances on SLIT herald deeper penetration of premium sprays and immunotherapies, yet affordability constraints keep generics pivotal. Regulatory agencies in China, Japan, and South Korea quicken reviews for pediatric formulations, further enlarging the allergic rhinitis drugs market. Middle East, Africa, and South America trail but show urban-center pockets of accelerated growth as disposable incomes climb.

- ALK-Abello

- Allergy Therapeutics

- Bayer

- Boehringer Ingelheim

- Cipla

- Dr. Reddy's Laboratories

- Glenmark Pharmaceuticals

- HAL Allergy Group

- Haleon plc

- Hikma Pharmaceuticals

- HollisterStier Allergy

- Kenvue

- Organon

- Perrigo Company

- Sandoz Group

- Sanofi

- Stallergenes Greer

- Teva Pharmaceutical Industries

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Longer Pollen Seasons Intensify Symptom Burden

- 4.2.2 Air Pollution Exacerbates AR Symptom Severity and Duration

- 4.2.3 E-Commerce and Online Pharmacies Expand Access to OTC Therapies

- 4.2.4 Rx-To-OTC Switches and Adoption of Dual-Action Combination Sprays

- 4.2.5 Non-Sedating Daytime Regimens Prioritized by Employers and Safety Bodies

- 4.2.6 SLIT Tablet Launches and Pediatric Label Expansions Accelerate AIT Uptake

- 4.3 Market Restraints

- 4.3.1 FDA Move Against Oral Phenylephrine Undercuts Decongestant Subsegment

- 4.3.2 Montelukast Boxed Warning Limits AR Usage and Prescriber Willingness

- 4.3.3 Adherence Gaps for Intranasal Steroids; Rebound Congestion Limits Decongestant Use

- 4.3.4 Reimbursement and Logistical Burdens Slow AIT Adoption

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 Antihistamines

- 5.1.2 Immunotherapy

- 5.1.3 Corticosteroids

- 5.1.4 Decongestants

- 5.1.5 Leukotriene Receptor Antagonists

- 5.1.6 Others (Combination Therapy, Anticholinergics, etc.)

- 5.2 By Dosage Form

- 5.2.1 Tablets & Capsules

- 5.2.2 Liquids & Syrups

- 5.2.3 Nasal Sprays

- 5.2.4 Nasal Drops

- 5.2.5 Sublingual Tablets/Drops (AIT)

- 5.2.6 Injectables (SCIT)

- 5.3 By Prescription Status

- 5.3.1 Over-the-Counter (OTC)

- 5.3.2 Prescription (Rx)

- 5.4 By Distribution Channel

- 5.4.1 Drugstores & Retail Pharmacies

- 5.4.2 Hospital Pharmacies

- 5.4.3 Online Pharmacies / E-commerce

- 5.4.4 Supermarkets/Hypermarkets

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 ALK-Abello

- 6.3.2 Allergy Therapeutics

- 6.3.3 Bayer AG

- 6.3.4 Boehringer Ingelheim

- 6.3.5 Cipla

- 6.3.6 Dr. Reddy's Laboratories Ltd.

- 6.3.7 Glenmark Pharmaceuticals Limited

- 6.3.8 HAL Allergy Group

- 6.3.9 Haleon plc

- 6.3.10 Hikma Pharmaceuticals

- 6.3.11 HollisterStier Allergy

- 6.3.12 Kenvue

- 6.3.13 Organon

- 6.3.14 Perrigo Company plc

- 6.3.15 Sandoz

- 6.3.16 Sanofi SA

- 6.3.17 Stallergenes Greer

- 6.3.18 Teva Pharmaceuticals

- 6.3.19 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment