|

시장보고서

상품코드

2063765

Wi-Fi 6 라우터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Wi-Fi 6 Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

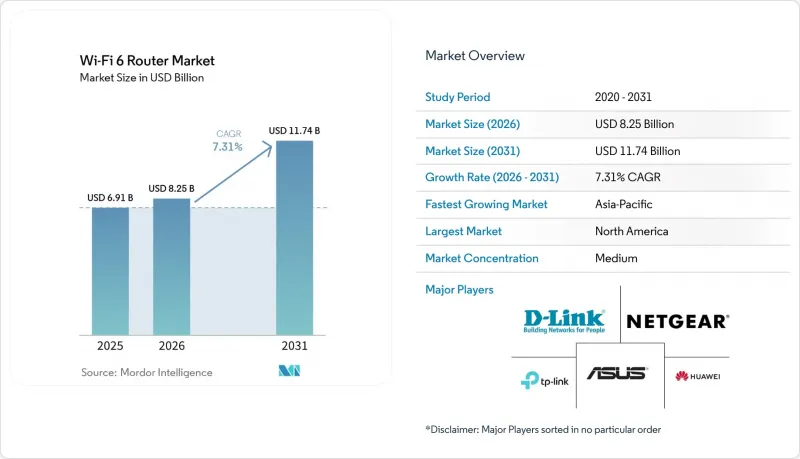

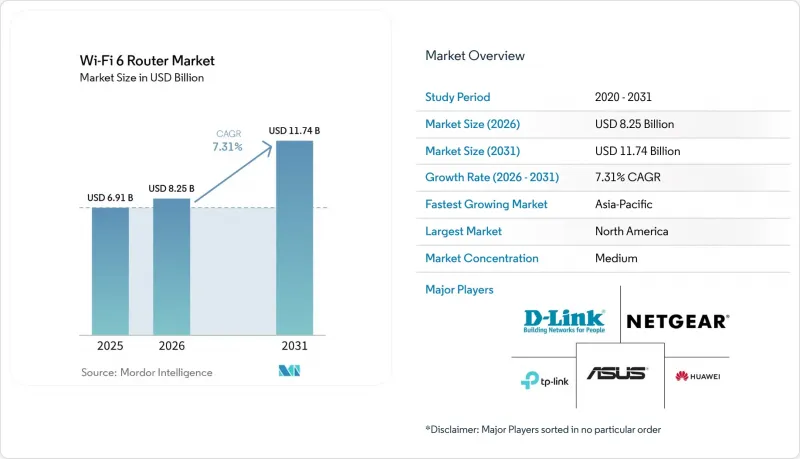

Mordor Intelligence에 의하면, Wi-Fi 6 라우터 시장 규모는 2025년에 69억 1,000만 달러로 평가되었습니다. 2026년 82억 5,000만 달러에서 2031년까지 117억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.31%를 나타낼 전망입니다.

본 보고서는 제품 유형(듀얼 밴드 라우터, 트라이 밴드 라우터, 쿼드 밴드 라우터), 주파수 대역(2.4GHz, 5GHz, 6GHz), 최종 사용자(가정용, 상업용, 산업용), 유통 채널(온라인 스토어, 오프라인 소매, 기업 직접 조달) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 Wi-Fi 6 라우터 시장 동향 및 인사이트

기가비트급 서비스로의 광대역 업그레이드 급증

Ofcom에 따르면, 2025년 기준 영국 가구의 광섬유 보급률은 89.58%에 달했으며, 기가비트 수준 이하의 처리 속도에 제약을 받는 구형 VDSL 게이트웨이를 통신 사업자가 주도하여 교체하는 움직임이 가속화되고 있습니다. 차터 커뮤니케이션즈는 2024년 하반기, 미국 내 가입자 120만 명에게 멀티 기가비트 게이트웨이를 도입함으로써 이러한 전환을 뒷받침했으며, 이는 케이블 업계의 기존 사업자들이 차세대 Wi-Fi 하드웨어를 활용해 광섬유와의 경쟁에서 선제적으로 대응하고 있음을 보여주었습니다. 번들형 리스 가격 책정 방식에 따라 라우터 업그레이드가 서비스 요금에 포함되므로 초기 비용이 들지 않고, 교체 주기가 단축됩니다. 동시에, DOCSIS와 Wi-Fi를 통합한 플랫폼을 제공하는 업체들은 수년에 걸친 공급 계약을 체결함으로써 수요에 대한 가시성을 높이고 있습니다. 대칭형 기가비트 요금제가 유럽과 동아시아에서 확대됨에 따라, Wi-Fi 6 라우터 시장은 지속적인 판매 성장세와 견조한 가격 수준을 보이고 있습니다.

2025년 주파수 재할당 이후 ISP의 Wi-Fi 6 게이트웨이로의 전환 의무화

2026년 1월, 연방통신위원회(FCC)가 6GHz 대역의 1,200 MHz 전체 대역을 개방하기로 결정함에 따라, 통신 사업자들은 이 채널을 이용할 수 없는 Wi-Fi 5 하드웨어를 단계적으로 단종할 수밖에 없게 되었습니다. 이와 동시에, 유럽전기통신표준화기구(ETSI)가 저대역 규정을 조율함에 따라, 공급업체들은 주요 EU 시장 전반에 걸쳐 트라이밴드 플랫폼의 표준화가 가능해졌습니다. 통신 사업자들은 2026년도 결산에서 구형 재고와 관련된 단기적인 감손 처리를 반영하고 있지만, 6GHz 백홀을 기반으로 하는 프리미엄 속도 요금제를 통해 ARPU(1명당 평균 매출)가 증가할 것으로 전망하고 있습니다. 인도 및 한국에서 시행된 유사한 규제 조치로 인해 제품 개발 주기가 12-18개월로 단축되었으며, 칩셋 공급업체들의 수익 창출이 가속화되고 있습니다.

Wi-Fi 6E 트라이밴드 모델의 프리미엄 가격대는 400달러 이상입니다.

NETGEAR의 Orbi 870 3대 세트는 1,499.99달러에 출시되어, 200달러 미만의 듀얼 밴드 시스템과의 가격 차이가 뚜렷합니다. 한편, TP-Link는 중급 트라이밴드 모델을 333.99달러 전후로 책정하고 있는데, 이 가격대는 일반적으로 광대역 속도가 500 Mbps를 초과하는 경우에만 타당합니다. 부품 비용의 급등은 추가적인 RF 체인, 대형 방열 어셈블리, 그리고 2.4GHz, 5GHz, 6GHz 대역을 아우르는 보다 복잡한 밴드 스티어링 펌웨어를 반영한 것입니다. 칩셋 통합이 진행됨에 따라 2027년 말까지 엔트리급 트라이밴드 제품의 가격이 250달러 아래로 떨어질 것으로 예상되지만, 현재의 가격 프리미엄은 가격에 민감한 시장, 특히 신흥국 시장에서 판매 대수를 억제하고 있습니다.

부문별 분석

트리밴드 하드웨어는 메쉬 트래픽을 클라이언트 스트림에서 분리하고 처리량의 결정성을 향상시키는 전용 6GHz 백홀에 대해 기업들이 기꺼이 비용을 지불하려는 태도에 힘입어, 2031년까지 연평균 성장률(CAGR) 9.62%로 성장할 것으로 전망됩니다. 시스코 시스템즈는 2026년도 결산에서 캠퍼스 설비 갱신 추세를 언급하며, 원활한 로밍과 안정적인 영상 품질을 필요로 하는 하이브리드 업무 환경이 수요의 요인이라고 지적했습니다. 그럼에도 불구하고, 2025년에는 듀얼 밴드 제품이 40.43%의 점유율을 유지했습니다. 이는 주택 구매자들이 커버리지를 우선시하여, 기가비트 광회선의 보급이 확대될 때까지 6GHz 도입을 미루었기 때문입니다. 쿼드밴드 기기는 여전히 틈새 시장 제품이며, 생태계 지원이 제한적이기 때문에 주로 게임 용도로만 사용되고 있습니다.

각 벤더사들은 Wi-Fi 8의 조기 개발을 추진하고 있으며, ASUSTeK Computer Inc.는 IEEE 802.11bn 초안 규격을 준수하고 최고 속도가 30 Gbps에 육박하는 라우터 프로토타입을 발표했습니다. 지역별 취향에는 여전히 차이가 나타납니다. 북미 가정에서는 구독형 보안 기능이 포함된 일체형 기기를 선호하는 반면, 유럽 소비자들은 구조적인 간섭 제약을 해결하기 위해 라우팅 기능과 무선 기능을 분리된 모듈식 시스템을 선택하는 경향이 있습니다. Wi-Fi Alliance의 자동 주파수 조정 인증은 6GHz 대역 내에서의 공존을 보장함으로써 소비자의 신뢰를 높이고, 트라이밴드 아키텍처의 지속적인 보급을 뒷받침하고 있습니다.

6GHz 대역 시장은 2031년까지 연평균 성장률(CAGR) 9.83%로 확대되고 있으며, 2025년에 47.32%의 점유율을 기록한 5GHz 대역을 능가하는 속도로 성장하고 있습니다. 연방통신위원회(FCC)는 5.925GHz에서 6.875GHz에 이르는 연속된 1,200 MHz 대역을 개방함으로써 이러한 전환을 가능하게 했으며, 멀티 기가비트 처리량을 유지할 수 있는 간섭 없는 160 MHz 채널 7개를 마련했습니다. 통신부는 2024년 12월에 500 MHz 대역의 면허를 해제함으로써 전 세계적인 경제성을 강화하고, 공급업체들이 주요 시장 전반에 걸쳐 설계를 표준화할 수 있도록 했습니다. 자동 주파수 조정 프레임워크 덕분에 기존 마이크로파 시스템에 지장을 주지 않으면서도 물류 야드나 기업 캠퍼스 등의 실외 환경에서도 6GHz 대역의 활용 범위가 더욱 확대되고 있습니다.

Wi-Fi 6 라우터 시장은 저전력·장거리 IoT 용도에서 여전히 2.4GHz 대역에 의존하고 있지만, 최대 처리량인 600 Mbps라는 한계로 인해 높은 대역폭이 필요한 이용 사례에는 제약이 있습니다. 5GHz 대역은 레이더 감지로 인해 발생하는 동적 주파수 선택에 의한 간섭이 있음에도 불구하고, 용량과 벽 투과성 간의 균형이 잘 잡혀 있어, 밀집된 주거 환경에서 실용적인 중간 대역으로 여전히 자리 잡고 있습니다. 반면, 6GHz 대역은 지연에 민감한 기업 및 산업용 워크로드를 위해 점점 더 많이 확보되고 있으며, 결정론적 네트워크를 지원하기 위해서는 지터를 3밀리초 미만으로 억제해야 합니다. 이러한 세분화는 각 대역이 서로 다른 성능 및 도입 요건에 맞추어 최적화되어 있다는 점을 통해 명확한 기능적 계층 구조를 부각시키고 있습니다.

지역별 분석

북미는 2025년에 전 세계 매출의 35.43%를 차지했으며, 광섬유를 통한 인프라 확장 경쟁에 대응하기 위해 게이트웨이를 임대하는 케이블 사업자들의 지지를 받고 있습니다. 이 모델 덕분에 Wi-Fi 6 라우터 시장 진입 방식이 소매 채널에서 통신 사업자 제공 방식으로 전환되면서, 평균 판매 가격이 높은 수준을 유지하고 업그레이드 주기가 단축되는 현상이 지속되고 있습니다. 차터 커뮤니케이션즈와 컴캐스트 코퍼레이션은 고가치 가입자를 유지하기 위해 Wi-Fi 7의 조기 도입을 포함한 서비스 플랜에 첨단 게이트웨이를 묶어 제공하는 방식으로 이러한 접근 방식을 실천하고 있습니다. 또한, 이 지역은 광대역 보급률이 높고, 성능에 따라 기꺼이 비용을 지불하려는 경향이 있어 프리미엄 부문의 성장이 촉진되고 있으며, 세계 다른 지역보다 앞서 차세대 규격의 도입이 가속화되고 있습니다.

아시아태평양은 규제 조화와 비용 효율적인 제조 생태계에 힘입어, 2026년부터 2031년까지 12.43%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측됩니다. 통신부는 6GHz 대역에 대한 면허 요건을 폐지함으로써, 주파수 정책을 미국 및 유럽과 조화시키고, 공급업체의 규정 준수 부담을 줄였습니다. 중국의 제조업체, 특히 선전에 본사를 둔 기업들은 50달러 미만의 듀얼 밴드 제품 수출 시장을 주도하고 있는 반면, 대만과 한국공급업체들은 수익성이 높은 트라이밴드 시스템에 주력하고 있습니다. 동시에, 인도네시아와 베트남에서 정부 주도로 광섬유망이 구축됨에 따라 광대역 접속이 확대되고 있으며, 가격 민감도로 인해 단가 수익 증가세는 둔화되고 있지만, 라우터 출하 대수는 증가하고 있습니다.

남미와 아프리카는 신흥 성장 지역으로, 공공 자금을 통해 연결성에 대한 의지가 구체적인 인프라 구축으로 이어지고 있습니다. ANATEL은 농촌 지역의 연결성 향상을 위해 32억 레알(6억 4,000만 달러)을 투자하고 있으며, 아프리카개발은행이 지원하는 나이지리아의 ‘프로젝트 브리지’와 남부아프리카개발은행이 주도하는 남아프리카공화국의 광대역 확장 사업 등을 통해 라스트 마일 접근성이 확대되고 있습니다. 절대적인 수익은 성숙한 시장보다 낮은 수준에 머물러 있지만, 출하 대수가 두 자릿수 성장세를 유지하고 있는 만큼, 각 벤더들은 다양한 환경 조건에 적합하고 견고하며 온도 변화에 강한 설계를 우선시하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the wi-Fi 6 router market size was valued at USD 6.91 billion in 2025 and is estimated to grow from USD 8.25 billion in 2026 to reach USD 11.74 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

This report is Segmented by Product Type (Dual-Band Routers, Tri-Band Routers, and Quad-Band Routers), Frequency Band (2. 4 GHz, 5 GHz, and 6 GHz), End User (Residential, Commercial, and Industrial), Distribution Channel (Online Stores, Offline Retail, and Direct Enterprise Procurement), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Wi-Fi 6 Router Market Trends and Insights

Surging Broadband Upgrades To Gigabit-Class Service

Fiber penetration reached 89.58% of United Kingdom premises in 2025, according to Ofcom, accelerating operator-led replacement of legacy VDSL gateways that constrain throughput below gigabit levels. Charter Communications reinforced this shift by deploying multi-gigabit gateways to 1.2 million United States subscribers in late 2024, indicating cable incumbents are pre-empting fiber competition with next-generation Wi-Fi hardware. Bundled lease pricing embeds router upgrades within service fees, eliminating upfront costs and compressing replacement cycles. Concurrently, vendors delivering integrated DOCSIS and Wi-Fi platforms lock in multi-year supply contracts, improving demand visibility. As symmetrical gigabit plans expand across Europe and East Asia, the Wi-Fi 6 router market gains sustained volume momentum and pricing resilience.

Mandatory Transition Of ISPs To Wi-Fi 6 Gateways After 2025 Spectrum Re-allocation

The January 2026 decision by the Federal Communications Commission to release the full 1,200 MHz of 6 GHz spectrum forces operators to phase out Wi-Fi 5 hardware that cannot utilize these channels. In parallel, the European Telecommunications Standards Institute aligned lower-band rules, enabling vendors to standardize tri-band platforms across major EU markets. Operators are absorbing near-term write-offs on legacy inventory in 2026 financials but expect higher ARPU from premium speed tiers supported by 6 GHz backhaul. Similar regulatory actions in India and South Korea are compressing product-development cycles to 12-18 months, accelerating revenue conversion for chipset vendors.

Premium Pricing Of Wi-Fi 6E Tri-Band Models Above USD 400

NETGEAR's Orbi 870 three-pack launched at USD 1,499.99, highlighting a substantial price delta versus sub-USD 200 dual-band systems, while TP-Link positions mid-tier tri-band units around USD 333.99, a threshold typically justified only when broadband speeds exceed 500 Mbps. The elevated bill of materials reflects an additional RF chain, larger thermal assemblies, and more complex band-steering firmware spanning 2.4, 5, and 6 GHz. Although ongoing chipset integration is expected to compress entry-level tri-band pricing below USD 250 by late 2027, the current premium suppresses unit volumes in price-sensitive markets, particularly across emerging economies.

Other drivers and restraints analyzed in the detailed report include:

- Explosive Growth Of Smart-Home IoT Node Density

- Government-Backed Rural Fiber Roll-outs In South America And Africa

- Fragmented 6 GHz Rules Forcing Multi-SKU Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tri-band hardware is projected to expand at a 9.62% CAGR through 2031, driven by enterprise willingness to pay for dedicated 6 GHz backhaul that segregates mesh traffic from client streams and improves throughput determinism. Cisco Systems referenced campus-refresh momentum in its FY 2026 earnings, linking demand to hybrid work environments that require seamless roaming and stable video quality. Despite this, dual-band units retained 40.43% share in 2025 as residential buyers prioritized coverage and delayed 6 GHz adoption until gigabit fiber availability improved. Quad-band devices remain niche, largely confined to gaming use cases with limited ecosystem support.

Vendors are advancing early Wi-Fi 8 development, with ASUSTeK Computer Inc. introducing a prototype router aligned with draft IEEE 802.11bn specifications and peak speeds approaching 30 Gbps. Regional preferences remain differentiated: North American households favor integrated units bundled with subscription-based security, while European consumers opt for modular systems that separate routing and wireless functions to address structural interference constraints. Certification by the Wi-Fi Alliance for automatic frequency coordination strengthens buyer confidence by ensuring coexistence within the 6 GHz band, supporting sustained uptake of tri-band architectures.

The 6 GHz segment is expanding at a 9.83% CAGR through 2031, outpacing the 5 GHz band, which held a 47.32% share in 2025. The Federal Communications Commission enabled this shift by opening a contiguous 1,200 MHz block from 5.925 to 6.875 GHz, creating seven interference-free 160 MHz channels capable of sustaining multi-gigabit throughput. The Department of Telecommunications reinforced global-scale economics by delicensing 500 MHz in December 2024, allowing vendors to standardize designs across key markets. Automated frequency coordination frameworks further extend 6 GHz usability to outdoor environments, including logistics yards and enterprise campuses, without disrupting incumbent microwave systems.

The Wi-Fi 6 router market still depends on 2.4 GHz for low-power, long-range IoT applications, although its throughput ceiling of 600 Mbps limits high-bandwidth use cases. The 5 GHz band remains the practical midpoint in dense residential settings, balancing capacity and wall penetration, despite interruptions from dynamic frequency selection triggered by radar detection. In contrast, 6 GHz is increasingly reserved for latency-sensitive enterprise and industrial workloads, where jitter must remain below 3 milliseconds to support deterministic networking. This segmentation highlights a clear functional stratification, with each band optimized for distinct performance and deployment requirements.

Geography Analysis

North America generated 35.43% of global revenue in 2025, supported by cable operators that lease gateways to defend against fiber overbuild competition. This model shifts entry into the Wi-Fi 6 router market from retail to carrier provisioning, sustaining higher average selling prices and faster upgrade cycles. Charter Communications and Comcast Corporation exemplify this approach by bundling advanced gateways within service plans, including early Wi-Fi 7 deployments to retain high-value subscribers. The region also benefits from higher broadband penetration and willingness to pay for performance tiers, reinforcing premium segment growth and accelerating adoption of next-generation standards ahead of global peers.

Asia-Pacific is expected to record the fastest CAGR of 12.43% between 2026 and 2031, driven by regulatory alignment and cost-efficient manufacturing ecosystems. The Department of Telecommunications enabled 6 GHz delicensing, aligned spectrum policy with the United States and Europe, and reduced compliance complexity for vendors. Chinese manufacturers, particularly those based in Shenzhen, dominate sub-USD 50 dual-band exports, while suppliers in Taiwan and South Korea focus on higher-margin tri-band systems. Concurrently, government-backed fiber rollouts in Indonesia and Vietnam expand broadband access, increasing router volumes even as price sensitivity moderates per-unit revenue growth.

South America and Africa represent emerging growth corridors, where public funding is translating connectivity ambitions into tangible infrastructure deployment. ANATEL is channeling BRL 3.2 billion (USD 640 million) into rural connectivity, while initiatives such as Nigeria's Project BRIDGE, supported by the African Development Bank, and South Africa's broadband expansion led by the Development Bank of Southern Africa are scaling last-mile access. Although absolute revenues remain lower than mature markets, sustained double-digit shipment growth is prompting vendors to pprioritize ruggedized, temperature-resilient designs suited to diverse environmental conditions.

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Belkin International, Inc.

- Cisco Systems, Inc.

- Xiaomi Corporation

- Ubiquiti Inc.

- Zyxel Communications Corporation

- MikroTikls SIA

- Shenzhen Tenda Technology Co., Ltd.

- Shenzhen Mercury Communication Technologies Co., Ltd.

- Zioncom Holdings Limited (TOTOLINK)

- Edimax Technology Co., Ltd.

- TRENDnet, Inc.

- GL Technologies Inc.

- Buffalo Inc.

- AVM Computersysteme Vertriebs GmbH

- DrayTek Corp.

- Synology Inc.

- Cambium Networks Corporation

- Ruijie Networks Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Broadband Upgrades to Gigabit-Class Services

- 4.2.2 Mandatory Transition of ISPs to Wi-Fi 6 Gateways After 2025 Spectrum Re-allocation

- 4.2.3 Explosive Growth of Smart-Home IoT Node Density

- 4.2.4 Government-Backed Rural Fiber Roll-outs in South America and Africa

- 4.2.5 Enterprise Network Refresh Cycles Driven by Hybrid Work Policies

- 4.2.6 Regulatory Approvals for 6 GHz Band Unleashing Wi-Fi 6E Capacity

- 4.3 Market Restraints

- 4.3.1 Premium Pricing of Wi-Fi 6E Tri-Band Models Above USD 400

- 4.3.2 Fragmented 6 GHz Rules Forcing Multi-SKU Compliance Costs

- 4.3.3 Semiconductor Lead-Times Exceeding 30 Weeks for Key Chipsets

- 4.3.4 Limited Consumer Awareness of Standard Benefits Slowing Adoption

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Dual-Band Routers

- 5.1.2 Tri-Band Routers

- 5.1.3 Quad-Band Routers

- 5.2 By Frequency Band

- 5.2.1 2.4 GHz

- 5.2.2 5 GHz

- 5.2.3 6 GHz (Wi-Fi 6E)

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Distribution Channel

- 5.4.1 Online Stores

- 5.4.2 Offline Retail

- 5.4.3 Direct Enterprise Procurement

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TP-Link Technologies Co., Ltd.

- 6.4.2 NETGEAR, Inc.

- 6.4.3 ASUSTeK Computer Inc.

- 6.4.4 D-Link Corporation

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Belkin International, Inc.

- 6.4.7 Cisco Systems, Inc.

- 6.4.8 Xiaomi Corporation

- 6.4.9 Ubiquiti Inc.

- 6.4.10 Zyxel Communications Corporation

- 6.4.11 MikroTikls SIA

- 6.4.12 Shenzhen Tenda Technology Co., Ltd.

- 6.4.13 Shenzhen Mercury Communication Technologies Co., Ltd.

- 6.4.14 Zioncom Holdings Limited (TOTOLINK)

- 6.4.15 Edimax Technology Co., Ltd.

- 6.4.16 TRENDnet, Inc.

- 6.4.17 GL Technologies Inc.

- 6.4.18 Buffalo Inc.

- 6.4.19 AVM Computersysteme Vertriebs GmbH

- 6.4.20 DrayTek Corp.

- 6.4.21 Synology Inc.

- 6.4.22 Cambium Networks Corporation

- 6.4.23 Ruijie Networks Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment