|

시장보고서

상품코드

2063817

Wi-fi 6E 라우터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Wi-fi 6E Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

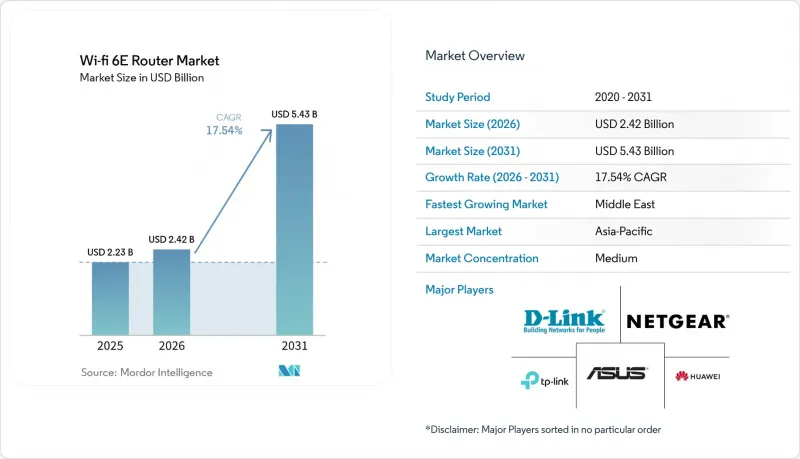

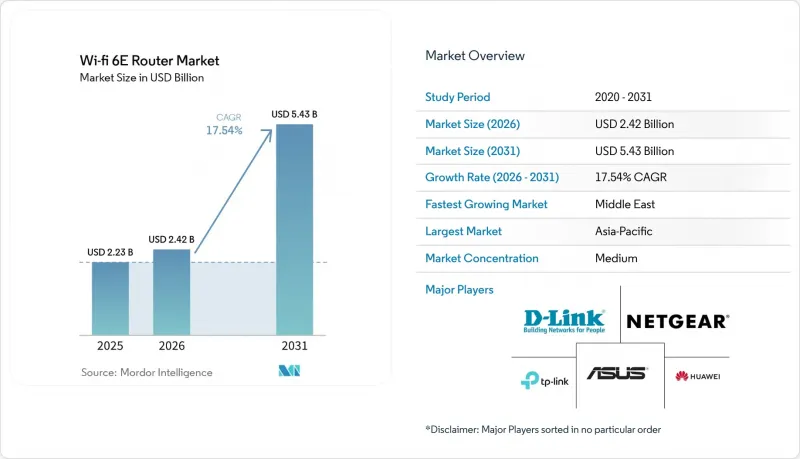

Mordor Intelligence에 의하면, Wi-Fi 6E 라우터 시장 규모는 2025년에 22억 3,000만 달러로 평가되었고 2026년 24억 2,000만 달러에서 2031년까지 54억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 17.54%를 나타낼 전망입니다.

본 보고서는 대역(트라이밴드, 듀얼밴드, 쿼드밴드 이상), 제품 유형(소비자용, 엔터프라이즈용, 캐리어 등급 및 ISP 게이트웨이), 최종 사용자(가정, 중소기업, 엔터프라이즈 및 캠퍼스, 공공 핫스팟 및 스마트 시티), 판매 채널(온라인 소매, 매장, 리셀러, 직접 OEM), 지역(북미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 Wi-Fi 6E 라우터 시장 동향 및 인사이트

기가비트 광대역 가입자 수의 급증

2025년, FTTH(Fiber-to-the-Home) 보급률이 중요한 임계치를 넘어섰고, 북미, 유럽, 아시아태평양의 통신 사업자들이 대칭형 멀티 기가비트 서비스를 출시함에 따라 기존의 Wi-Fi 5 라우터가 병목 현상을 일으키고 있습니다. 2025년 Wi-Fi 6E 기기 출하량이 6억 2,690만 대에 달할 것이라는 예측은 소비자들이 기가비트 회선을 포화시킬 수 있는 성능의 하드웨어로 업그레이드함에 따라 수요 측면에서의 견인력이 강해지고 있음을 보여줍니다. 전략적으로 중요한 것은 ISP의 비즈니스 모델 전환입니다. 통신 사업자들은 라우터를 일반화된 가정용 기기로 취급하는 대신, 프리미엄급 Wi-Fi 6E 게이트웨이를 광회선 계약과 함께 제공함으로써 서비스 계층의 차별화를 꾀하고, 해지율 감소를 목표로 하고 있습니다. 이를 통해 선순환이 만들어집니다. 광대역 속도의 향상은 라우터 업그레이드의 필요성을 뒷받침하며, 이는 부모를 위한 관리 기능이나 네트워크 보안 구독 서비스와 같은 부가가치 서비스를 통한 매출 증대로 이어집니다. 공급업체에게 주는 시사점은 분명합니다. Tier 1 ISP와의 제휴는 확실한 판매량을 가져다주지만, 사업자가 현장에 직접 방문하지 않고 원격으로 성능 최적화 및 문제 해결을 수행할 수 있도록 소프트웨어 정의 네트워크(SDN) 기능을 통해 차별화를 꾀하지 않는 한, 이익률은 압박을 받게 될 것입니다.

기업들의 하이브리드 근무 모델로의 전환

하이브리드 근무 체계는 지식 근로자들에게 표준적인 업무 모델로 자리 잡았으며, 기업들은 지금까지 기업 캠퍼스에서만 적용되던 것과 동일한 엄격함을 바탕으로 재택 근무 환경의 연결성을 구축해야만 하는 상황에 놓여 있습니다. 2025년에 출하될 Wi-Fi 6E 액세스 포인트가 8,160만 대에 달할 것이라는 보고는 저지연 화상 회의와 안전한 VPN 터널링이 필요한 분산형 근로자들로부터의 강력한 수요를 보여주고 있습니다. 두 번째 인사이트은 기업의 조달 동향의 양극화에 관한 것입니다. 대기업은 중앙 관리 콘솔을 갖춘 캐리어급 라우터를 표준화하고 있는 반면, 중소기업은 프로슈머용 가격대에서 엔터프라이즈급 보안을 제공하는 소비자용 하드웨어로 눈을 돌리고 있습니다. 이러한 양극화는 제로 터치 프로비저닝 및 역할 기반 접근 제어를 갖춘 클라우드 관리형 플랫폼을 제공하면서도, SMB(중소기업)의 프로젝트를 수주할 수 있을 만큼 경쟁력 있는 가격 정책을 통해 그 격차를 메울 수 있는 벤더에게 비즈니스 기회를 창출하고 있습니다. GDPR(EU 개인정보보호규정) 및 새로운 데이터 현지화 의무와 같은 규제 체계는 특히 규정 위반 시 부과되는 벌칙이 심각한 유럽 및 아시아태평양 시장에서 암호화 기능과 감사 로그 기능을 내장한 라우터에 대한 수요를 더욱 높이고 있습니다.

고성능 칩셋공급망 제약

Wi-Fi 6E 라우터는 브로드컴, 퀄컴, 미디어텍 등 소수의 주요 공급업체가 제공하는 첨단 반도체에 의존하고 있으며, 이들의 생산 일정은 TSMC(대만 반도체 제조 회사)의 생산 능력 제약이나 동아시아의 지정학적 긴장의 영향을 받기 쉬운 상황에 놓여 있습니다. 분석에 따르면, 연결용 집적회로(IC)는 연평균 성장률(CAGR) 11.6%를 나타낼 것으로 예측되지만, 이 성장률은 데이터센터 및 자동차용 반도체 수요에는 미치지 못하며, 파운드리 할당 결정에 따라 WLAN 시장으로공급이 주기적으로 제한될 가능성이 있음을 시사합니다. 전략적 위험 요인으로는 칩셋 부족으로 인해 공급업체의 이익률이 압박을 받을 수 있다는 점을 들 수 있습니다. 라우터 제조업체는 리드타임의 장기화를 수용하고, 보다 견고한 공급 계약을 맺고 있는 경쟁사에게 시장 점유율을 빼앗길 위험을 감수할지, 아니면 현물 시장 가격을 지불할지 중 하나를 선택할 수밖에 없습니다.

부문별 분석

2025년 현재, 트라이밴드 기기는 Wi-Fi 6E 라우터 시장의 46.78% 점유율을 차지하고 있으며, 대다수의 가정이 수용할 수 있는 가격대에서 메쉬 백홀의 기본 선택지로 자리매김하고 있습니다. 밀집된 도시 지역의 아파트에서는 트라이밴드 노드 1대만으로도 기가비트 광회선을 완전히 포화시킬 수 있으므로, 추가 무선 모듈에 대한 투자로 얻을 수 있는 이점은 거의 없습니다. 쿼드밴드 이상의 모델은 기업, 게이머, 컨텐츠 크리에이터들이 두 개의 독립적인 6GHz 또는 5GHz 무선 연결이 제공하는 이중화 기능을 중요하게 여기기 때문에 연평균 성장률(CAGR) 18.43%로 성장할 것으로 전망됩니다. 인도처럼 하위 6GHz 대역만 허가하고 있는 시장에서는 쿼드밴드 하드웨어의 실질적인 이점이 줄어들고 보급 속도가 둔화되지만, 수요가 사라지는 것은 아닙니다.

강력한 기기 지원도 중요합니다. 스마트폰과 노트북에 멀티 무선 칩셋이 탑재됨에 따라, 10대 이상의 활성 클라이언트를 보유한 가정에서는 추가적인 6GHz 채널을 통한 부하 분산 효과를 체감하기 시작하고 있습니다. 트라이밴드 라우터는 소매업체와 ISP의 재고 관리를 간소화해 주지만, 쿼드밴드 모델은 AR, VR, 8K 스트리밍을 대비한 미래 지향적인 용량을 필요로 하는 파워 유저들에게 어필합니다. 따라서 각 벤더사는 SKU 라인을 병행하여 유지하면서, 트라이밴드 모델은 대규모 업그레이드 주기에 맞추어 가격을 책정하고, 쿼드밴드 모델은 수십 대의 클라이언트가 동시에 연결되어도 성능을 보장하는 프리미엄 제품군으로 포지셔닝하고 있습니다. 이러한 양극화 전략은 WiFi 6E 라우터 시장을 확대하고, 가성비 제품군과 하이엔드 제품군 모두에서 시장 규모를 끌어올리며, 반도체 원가 하락 속에서도 제조업체들이 이익률을 유지하는 데 도움이 됩니다. 또한, 이 접근 방식은 지역의 주파수 정책에 맞추어 칩셋 할당을 트라이밴드 모델과 쿼드밴드 모델 사이에서 조정할 수 있으므로, 공급망 리스크를 완화합니다. 예측 기간 동안 주파수 대역의 자유화가 진행됨에 따라 시장 점유율은 점차 쿼드밴드로 이동할 것으로 보이지만, 2031년까지는 트라이밴드가 판매량 1위를 유지할 것으로 예측됩니다.

2025년 매출액 중 소비자용 하드웨어가 54.32%를 차지했습니다. 이는 호황을 누리고 있는 전자상거래와 WiFi 5에서 업그레이드하려는 수요가 큰 기반이 되어 이 같은 성장을 이끈 결과입니다. 그러나 통신 사업자들이 멀티기가 서비스를 차별화하기 위해 Wi-Fi 6E를 번들로 제공하고 있는 만큼, 캐리어급 게이트웨이가 연평균 성장률(CAGR) 17.98%를 기록하며 가장 빠르게 성장하는 분야로 부상하고 있습니다. 엔터프라이즈급 라우터는 여전히 캠퍼스용으로 제공되고 있지만, 교체 주기가 길기 때문에 단기적인 성장은 제한되고 있습니다.

자녀 보호 기능, 보안 오버레이, 원격 진단 등을 포함하는 통신사용 게이트웨이에 수반되는 지속적인 소프트웨어 수익 덕분에, 수익원은 일회성 하드웨어 판매에서 수년에 걸친 서비스 계약으로 전환되고 있습니다. ISP 설계 수주를 따낸 벤더는 사실상 판매 물량을 확보하게 되며, 하드웨어 이익률 하락을 연금과 같은 여러 수입원으로 보충하면서 WiFi 6E 라우터 시장의 성장 궤도를 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 중국, 인도, 동남아시아에서의 FTTH(Fiber-to-the-Home) 확대에 힘입어 2025년에는 매출의 37.44%를 차지했습니다. 인도에서는 2026년 1월에 6GHz 대역의 하위 주파수 대역에 대한 라이선스 규제가 해제되어, 방대한 주택 및 캠퍼스 시장이 열리게 됩니다. 한편, 중국은 자국의 ODM 기반을 활용하여 국내 및 ‘일대일로’ 연선 시장을 대상으로 경쟁력 있는 가격의 하드웨어를 제공합니다. 지역적 위험 요인으로는 공급망이나 인증 제도를 단절시킬 가능성이 있는 무역 마찰을 들 수 있습니다.

북미는 여전히 교체 수요가 주를 이루는 시장이지만, FCC가 2026년에 승인한 표준 출력의 혜택을 받고 있습니다. 이를 통해 지자체 Wi-Fi나 경기장 내 야외 Wi-Fi 6E가 가능해지며, 적용 가능한 이용 사례가 확대될 것입니다. 한편, 유럽에서는 위성과의 공존에 관한 논의가 보급 속도를 늦추고 있습니다. Ofcom의 지속적인 협의로 인해 2027년까지 6GHz 대역 상단의 이용 현황이 불투명한 상태이기 때문에 공급업체들은 여러 SKU를 출시할 수밖에 없게 되었고, 이로 인해 공공 부문에서의 도입이 주춤하고 있습니다.

중동은 연평균 성장률(CAGR) 20.11%의 성장이 예상되며, 사우디아라비아와 아랍에미리트(UAE)의 ‘비전 2030’ 계획이 스마트시티의 연결성을 의무화하고 있는 점을 활용하고 있습니다. 남미와 아프리카는 광대역 보급률 면에서 뒤처져 있지만, 주요 도시에서는 중가대 트라이밴드 모델에 대한 초기 수요가 나타나고 있습니다. 지역별 맞춤형 제품 라인업, 걸프 연안 국가들을 위한 프리미엄 캐리어 게이트웨이, 남미 시장을 겨냥한 가성비 뛰어난 트라이밴드 키트를 통해, 다양한 경제 상황 하에서 Wi-Fi 6E 라우터 시장의 보급이 최적화됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the wi-Fi 6E router market size was valued at USD 2.23 billion in 2025 and estimated to grow from USD 2.42 billion in 2026 to reach USD 5.43 billion by 2031, at a CAGR of 17.54% during the forecast period (2026-2031).

This report is Segmented by Band (Tri-Band, Dual-Band, and Quad-Band and Above), Product Type (Consumer, Enterprise, and Carrier-Grade and Isp Gateways), End User (Residential, SMB, Enterprise and Campuses, and Public Hotspots and Smart Cities), Sales Channel (Online Retail, Stores, Resellers, and Direct OEM), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Wi-fi 6E Router Market Trends and Insights

Explosion Of Gigabit Broadband Subscriptions

Fiber-to-the-home penetration crossed critical thresholds in 2025, with operators in North America, Europe, and Asia-Pacific deploying symmetrical multi-gigabit services that render legacy Wi-Fi 5 routers a bottleneck. The projection of 626.9 million Wi-Fi 6E devices shipped in 2025 underscores the demand-side pull as consumers upgrade to hardware capable of saturating gigabit links. What matters strategically is the shift in ISP business models: rather than treating routers as commoditized customer-premises equipment, telcos now bundle premium Wi-Fi 6E gateways with fiber subscriptions to differentiate service tiers and reduce churn. This creates a flywheel effect: higher broadband speeds justify router upgrades, which in turn drive incremental revenue from value-added services such as parental controls and network security subscriptions. The implication for vendors is clear: partnerships with tier-1 ISPs unlock predictable volume, but also compress margins unless differentiated through software-defined networking features that enable operators to remotely optimize performance and troubleshoot issues without truck rolls.

Enterprise Migration Toward Hybrid Work Models

Hybrid work arrangements have entrenched themselves as the default operating model for knowledge workers, compelling enterprises to architect home-office connectivity with the same rigor previously reserved for corporate campuses. The reported 81.6 million Wi-Fi 6E access points shipped in 2025 indicate strong demand from distributed workforces requiring low-latency video conferencing and secure VPN tunneling. The second-order insight involves the bifurcation of enterprise procurement: large corporations are standardizing on carrier-grade routers with centralized management consoles, while small and medium-sized businesses are gravitating toward consumer-grade hardware that offers enterprise-class security at prosumer price points. This bifurcation creates whitespace for vendors that can bridge the gap by offering cloud-managed platforms with zero-touch provisioning and role-based access controls, yet priced competitively enough to win SMB deals. Regulatory frameworks such as GDPR and emerging data-localization mandates further amplify demand for routers with built-in encryption and audit-logging capabilities, particularly in Europe and Asia-Pacific markets where compliance penalties are material.

Supply Chain Constraints of High-end Chipsets

Wi-Fi 6E routers depend on advanced silicon from a concentrated supplier base, Broadcom, Qualcomm, and MediaTek, whose production schedules remain vulnerable to capacity constraints at Taiwan Semiconductor Manufacturing Company and geopolitical tensions in East Asia. Analysis indicates that connectivity integrated circuits are forecast to grow at an 11.6% CAGR, yet this growth lags data-center and automotive semiconductor demand, suggesting that foundry allocation decisions could periodically constrain supply to the WLAN market. The strategic risk is that chipset shortages compress vendor margins. Router manufacturers must either accept longer lead times, thereby risking market-share loss to competitors with stronger supply agreements, or pay spot-market prices.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Wi-Fi 6E Certified End-Devices

- Spectrum Liberalisation in 6 GHz Band by Regulators

- High Average Selling Price Versus Wi-Fi 5 Routers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tri-band devices held 46.78% WiFi 6E router market share in 2025, validating their position as the default choice for mesh backhaul at a price point most households accept. In dense urban apartments, one tri-band node can fully saturate a gigabit fiber link, so incremental spending on additional radios brings little extra benefit. Quad-band and above models are forecast to expand at an 18.43% CAGR because enterprises, gamers, and content creators value the redundancy that two independent 6 GHz or 5 GHz radios provide. Markets that authorize only the lower 6 GHz block, such as India, narrow the real-world advantage of quad-band hardware, slowing adoption but not eliminating demand.

Strong device support also matters: as smartphones and laptops ship with multi-radio chipsets, households with ten or more active clients begin to notice the load-balancing advantage of an extra 6 GHz channel. Tri-band routers simplify inventory for retailers and ISPs, while quad-band units appeal to power users seeking future-proof capacity for AR, VR, and 8K streaming. Vendors, therefore, keep parallel SKU lines, price tri-band for mass upgrade cycles, and position quad-band as a premium tier that safeguards performance when dozens of clients connect simultaneously. This bifurcated strategy expands the WiFi 6E router market, boosting market size across both value and high-end price bands, helping manufacturers defend margins even as silicon costs fall. The approach also cushions supply-chain risk because chipset allocations can be shifted between tri- and quad-band models to match regional spectrum policies. Over the forecast window, continued spectrum liberalization will gradually tilt share toward quad-band, but tri-band is expected to remain the volume leader through 2031.

Consumer hardware accounted for 54.32% of 2025 revenue, driven by thriving e-commerce and a large base of WiFi 5 replacements. Carrier-grade gateways, however, are the fastest-growing slice at a 17.98% CAGR, as telcos bundle WiFi 6E to differentiate multi-gig services. Enterprise-class routers continue to serve campuses but face longer refresh cycles that temper near-term growth.

Recurring software revenues attached to carrier gateways, including parental controls, security overlays, and remote diagnostics, shift profit pools from one-time hardware sales to multi-year service contracts. Vendors that secure ISP design wins effectively lock in volume, underpinning the trajectory of the WiFi 6E router market while balancing thinner hardware margins with annuity income streams.

Geography Analysis

Asia-Pacific commanded 37.44% revenue in 2025, propelled by fiber-to-the-home expansion in China, India, and Southeast Asia. India's January 2026 de-licensing of the lower 6 GHz band unlocks a vast residential and campus market, while China leverages its ODM base to deliver competitively priced hardware for domestic and Belt-and-Road destinations. Regional risk lies in potential trade friction that may split supply chains and certification regimes.

North America remains a replacement market but benefits from the FCC's 2026 standard-power approval, which enables outdoor WiFi 6E for municipal WiFi and stadiums, broadening the addressable use cases. Satellite coexistence debates temper Europe's adoption; Ofcom's ongoing consultation keeps upper-6 GHz clarity in limbo through 2027, compelling vendors to ship multiple SKUs and slowing public-sector rollouts.

The Middle East, forecast to grow at 20.11% CAGR, leverages Vision 2030 agendas in Saudi Arabia and the United Arab Emirates that mandate smart-city connectivity. South America and Africa trail in broadband penetration, yet tier-1 cities show early demand for mid-priced tri-band models. Tailored regional portfolios, premium carrier gateways in the Gulf, value tri-band kits in South America, optimize the WiFi 6E router market penetration across diverse economic profiles.

- ASUSTeK Computer Inc.

- TP-Link Technologies Co., Ltd.

- Netgear, Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Linksys Holdings, Inc.

- Zyxel Communications Corporation

- Ubiquiti Inc.

- EnGenius Technologies, Inc.

- Cambium Networks Corporation

- MikroTikls SIA

- Edimax Technology Co., Ltd.

- Buffalo Inc.

- Cisco Systems, Inc.

- CommScope Holding Company, Inc. (ARRIS)

- Actiontec Electronics, Inc.

- Comtrend Corporation

- NetComm Wireless Pty Ltd.

- Juniper Networks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of Gigabit Broadband Subscriptions

- 4.2.2 Enterprise Migration Toward Hybrid Work Models

- 4.2.3 Rapid Growth of Wi-Fi 6E Certified End-Devices

- 4.2.4 Spectrum Liberalisation in 6 GHz Band by Regulators

- 4.2.5 Energy-Efficient Target Wake Time (TWT) Adoption in IoT

- 4.2.6 Increasing Support for WPA3 Security Standard

- 4.3 Market Restraints

- 4.3.1 Supply Chain Constraints of High-end Chipsets

- 4.3.2 High Average Selling Price Versus Wi-Fi 5 Routers

- 4.3.3 Interference with Fixed Satellite Services in 6 GHz

- 4.3.4 Limited Consumer Awareness Outside Tier-1 Economies

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalary

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Band

- 5.1.1 Tri-Band (2.4 GHz, 5 GHz, 6 GHz)

- 5.1.2 Dual-Band (2.4 GHz and 6 GHz)

- 5.1.3 Quad-Band and Above

- 5.2 By Product Type

- 5.2.1 Consumer-Grade Routers

- 5.2.2 Enterprise-Class Routers

- 5.2.3 Carrier-Grade and ISP Gateways

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Small and Medium-Sized Businesses

- 5.3.3 Large Enterprises and Campuses

- 5.3.4 Public Hotspots and Smart Cities

- 5.4 By Sales Channel

- 5.4.1 Online Retail

- 5.4.2 Consumer Electronics Stores

- 5.4.3 Value-Added Resellers

- 5.4.4 Direct OEM / ODM Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASUSTeK Computer Inc.

- 6.4.2 TP-Link Technologies Co., Ltd.

- 6.4.3 Netgear, Inc.

- 6.4.4 D-Link Corporation

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Xiaomi Corporation

- 6.4.7 Linksys Holdings, Inc.

- 6.4.8 Zyxel Communications Corporation

- 6.4.9 Ubiquiti Inc.

- 6.4.10 EnGenius Technologies, Inc.

- 6.4.11 Cambium Networks Corporation

- 6.4.12 MikroTikls SIA

- 6.4.13 Edimax Technology Co., Ltd.

- 6.4.14 Buffalo Inc.

- 6.4.15 Cisco Systems, Inc.

- 6.4.16 CommScope Holding Company, Inc. (ARRIS)

- 6.4.17 Actiontec Electronics, Inc.

- 6.4.18 Comtrend Corporation

- 6.4.19 NetComm Wireless Pty Ltd.

- 6.4.20 Juniper Networks, Inc.