|

시장보고서

상품코드

2063820

서비스 제공업체 라우터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Service Provider Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

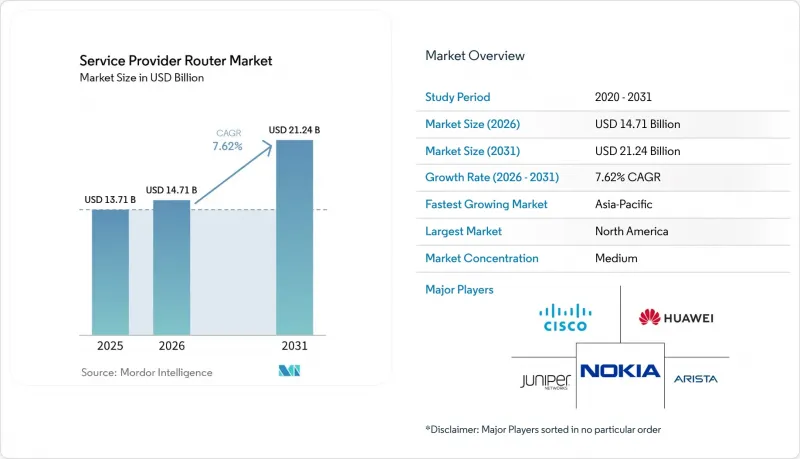

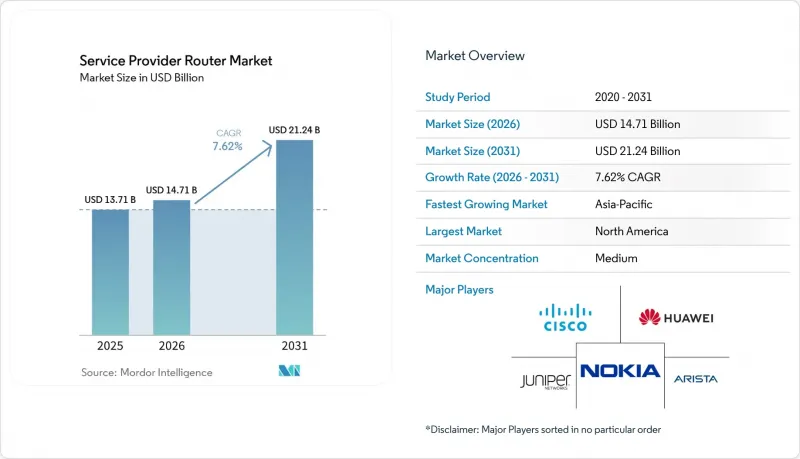

Mordor Intelligence에 의하면, 서비스 제공업체 라우터 시장 규모는 2025년에 137억 달러로 평가되었습니다. 2026년 147억 달러에서 2031년까지 212억 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.6%를 나타낼 전망입니다.

본 보고서는 라우터의 유형(코어 라우터, 에지 라우터, 어그리게이션 라우터 등), 대역폭/포트 속도(최대 40 Gbps, 40-100 Gbps, 100-400 Gbps 등), 용도(통신 서비스 제공업체, 클라우드 서비스 제공업체, 인터넷 익스체인지 제공업체 등), 기술(하드웨어 기반 라우터 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 서비스 제공업체 라우터 시장 동향 및 인사이트

5G 및 5G-Advanced의 백홀 요구 사항

모바일 통신 사업자들은 초기 5G 서비스에서 네트워크 슬라이싱 및 통합형 액세스 백홀과 같은 5G-Advanced 기능으로 전환하고 있습니다. 중국은 2025년 말까지 350만 기의 기지국을 구축했으며, 각 기지국에는 최소 10G의 백홀 용량이 필요하기 때문에 전국적으로 35Tbit/s를 초과하는 라우터에 대한 추가 수요가 발생했습니다. 한국의 3대 통신사는 2025년에 백홀 업그레이드에 8조 7,000억 원(65억 달러)을 투자했습니다. 화웨이의 FlexE 2.0 하드 슬라이싱 및 SRv6 세분화을 통해 엔터프라이즈 SLA 티어에서 1밀리초 미만의 지연을 실현합니다. 노키아는 10G E-밴드 링크를 지원하는 AirScale 마이크로파 무선 장비를 100만 대 이상 출하하여, 도시 지역의 광케이블 비용을 30% 절감했습니다. 이러한 도입 사례에서는 분산 안테나 전체에서 위상 일관성을 유지하기 위해 IEEE 1588v2와 같은 타이밍 프로토콜이 우선적으로 채택되고 있습니다.

400G/800G 라우팅 기술의 보급

고비트레이트 코히런트 플러그어블 모듈 덕분에 2024년 이후 전송 비트당 비용이 약 60% 감소했습니다. Lumen은 2025년, 미국 내 도시 간 백본 전체에 800G 인터페이스를 도입하여 경로당 필요한 파장 수를 75% 줄였습니다. Colt와 Nokia가 실시한 현장 시험에서 증폭 장치를 사용하지 않고 표준 광섬유를 통해 800G QSFP-DD 모듈을 120km까지 전송하는 데 성공했습니다. Arista의 R4 라우터는 단일 HyperPort에서 3.2T를 집계할 수 있어, 하이퍼스케일러의 스파인 패브릭에 최적입니다. Ciena의 WaveLogic 6 Extreme 광 모듈은 500km 거리에서 1.6T를 달성하며, 테라비트급 장거리 링크 시대의 도래를 알렸습니다. OIF 800ZR 사양을 기반으로 한 다중 벤더 간의 상호 운용성 덕분에 벤더 종속성이 완화되어 대규모 도입이 가속화되고 있습니다.

반도체 공급망의 변동

2025년 초에는 7nm 및 5nm 라우팅 ASIC의 리드타임이 40주를 초과함에 따라, 18개월 후의 생산 능력을 확보할 수밖에 없는 상황에 처해 운전 자금에 여유가 없어졌습니다. DDR4/DDR5 가격은 80-90% 급등하여 중견 업체들의 이익률을 5-7포인트 끌어내렸습니다. AI 가속기에 따른 전 세계적인 HBM3 공급 부족으로 인해, 여러 라우터 제조업체들은 전력 소모가 많은 GDDR6 버퍼로 전환할 수밖에 없었습니다. TSMC의 N3 노드는 2025년 중반까지 할당량이 모두 소진되어, 중소규모의 팹리스 기업들은 구형 공정을 계속 사용해야 하게 되었습니다. 미국 CHIPS법에 따른 국내 파운드리 지원금은 2027년까지는 병목 현상을 완화하지 못할 것으로 보이며, 단기적으로는 변동이 지속될 것으로 전망됩니다.

부문별 분석

엣지 플랫폼 시장은 연평균 성장률(CAGR) 8.94%로 확대될 것으로 예상되며, 서비스 제공업체 라우터 시장 전체를 상회하는 성장세를 보일 것으로 전망됩니다. 코어 섀시는 2025년 매출의 35.4%를 차지하며, 장거리 및 메트로 백본을 뒷받침했습니다. 엣지의 성장은 최종 사용자당에서 1밀리초 미만의 지연 시간을 필요로 하는 프라이빗 5G 네트워크와 멀티액세스 엣지 컴퓨팅(MAEC)에 기인합니다. 시스코의 Catalyst 8200은 2025년에 5만 대 이상을 출하했으며, SD-WAN, IPsec, 용도 인식 라우팅을 통합함으로써 기존의 지점용 어플라이언스를 대체했습니다. 주니퍼의 Session Smart Router를 시범 도입한 결과, 포춘 500대 기업의 사업장에서 WAN 대역폭을 30% 절감했습니다. 애그리게이션 라우터는 DOCSIS 4.0 업링크에 10G 및 25G 백홀이 필요한 성숙한 케이블 시스템에서 여전히 안정적인 수요를 유지하고 있습니다. 가입자 에지 기능은 uCPE에서 가상화가 진행되고 있습니다. 스위스콤은 1만 대의 OneOS6 어플라이언스를 도입하여 현장 출장 대응을 60% 줄였습니다. 이러한 전환으로 인해 설비 투자가 전용 하드웨어에서 x86 기반 화이트박스로 이동하면서, 기존 벤더들의 이익률이 압박받고 있습니다. 그렇긴 하지만, 10만 라우트 킬로미터가 넘는 네트워크를 관리하는 Tier 1 통신사에게 있어 코어 라우터는 여전히 중요한 역할을 수행하고 있으며, 이중화된 패브릭 모듈이 99.999%의 가동률을 보장하고 있습니다.

이 부문의 분화는 서비스 제공업체 라우터 시장 규모 확대가 분산형 노드에 집중되는 반면, 코어 장비의 교체 수요는 정체 상태를 보이고 있음을 보여줍니다. 엣지 라우팅, 컴퓨팅, 보안을 소프트웨어 정의 번들로 통합할 수 있는 벤더가 추가 지출을 확보하는 데 있어 가장 유리한 입장에 있습니다. 한편, 핵심 분야에 주력하는 공급업체들은 코히런트 광 기술과 전력 효율이 뛰어난 실리콘을 통합함으로써 랙 유닛당 처리량을 향상시키고, 전면적인 교체를 미루는 방식으로 시장 점유율을 지키고 있습니다.

400G를 초과하는 인터페이스는 연평균 성장률(CAGR) 12.42%로 증가할 것으로 예상되며, 이는 서비스 제공업체 라우터 시장의 모든 속도 대역 중에서 가장 높은 성장률입니다. 2025년에도 100G-400G 포트는 여전히 매출의 34.82%를 차지하고 있으며, 이는 메트로 집약 및 데이터센터 스파인에서의 확고한 활용 현황을 반영하고 있습니다. 버라이즌이 2025년 메트로 지역 네트워크 개편에서 100G를 완전히 건너뛴 사례에서 볼 수 있듯이, 통신 사업자들은 100G를 건너뛰고 400G나 800G로 직접 전환하는 경향이 강해지고 있습니다. ZTE의 ZXCTN 6120H-SE는 콤팩트한 기지국 라우터로 400G를 구현하여, 캐비닛을 업그레이드하지 않고도 테라비트급 백홀을 가능하게 했습니다.

Arista의 XPO 수냉식 플러그인 얼라이언스는 30W 이상의 열을 방출하는 1.6T 및 3.2T 모듈을 대상으로 하며, 능동형 열 루프와 표준 QSFP-DD 소켓을 결합하고 있습니다. Ciena의 WaveLogic 6 광모듈은 1.6T 파장을 500km 이상 전송하여 재생 비용과 비트당 에너지 소비를 줄여줍니다. 코히런트 플러그어블 기술을 통해 트랜스폰더 셸프가 라우터의 라인 카드에 통합됨에 따라, 400G를 초과하는 플랫폼에서 서비스 제공업체 라우터 시장 점유율이 확대되고 있으며, 광통신 및 IP 예산이 통합된 지출 풀로 집약되고 있습니다.

지역별 분석

북미는 버지니아주, 오리건주, 텍사스주에서 이루어진 800억 달러 규모의 하이퍼스케일러 투자에 힘입어 2025년 매출의 41.28%를 차지했습니다. '광대역 형평성, 접근성 및 확장(BEAD)' 프로그램은 지방 광섬유 네트워크에 424억 5,000만 달러를 투자함으로써 견고한 집계 라우터에 대한 수요를 끌어올리고 있습니다. 에너지 효율 목표와 중국 공급업체에 대한 금지 조치로 인해 국내 조달이 확대되고 있으며, 이는 현지 제조업체에 유리하게 작용하고 있습니다.

아시아태평양은 중국의 ‘5G-Advanced’ 계획이 350만 기의 기지국으로 확대되고, 각 기지국에 10G 백홀이 필요해짐에 따라 2031년까지 연평균 성장률(CAGR) 8.14%를 나타낼 것으로 전망됩니다. 인도의 ‘BharatNet’은 광섬유 백본 프로젝트에 13만 9,000 카롤 루피(167억 달러)를 배정했습니다. 일본의 통신 사업자들은 2025년도에 5G 관련 비용으로 1조 8,000억 엔(120억 달러)을 지출했습니다. 동남아시아에서 일어나고 있는 해저 케이블 건설 붐은 섬나라들의 라우터 수요를 더욱 부추기고 있습니다.

유럽에서는 고성능 기기의 대기 전력을 8W로 제한하는 EU 규정 2023/826으로 인해 자본 지출이 억제되고 있음에도 불구하고, 통신 사업자들은 2025년 네트워크에 450억 유로(509억 달러)를 투자했습니다. 에너지 규제에 대응하기 위한 비용으로 인해 수냉식 광학 부품 및 첨단 열 설계가 촉진되고 있으며, 이는 연구개발 예산이 풍부한 공급업체에 유리하게 작용하고 있습니다.

남미에서는 브라질이 주파수 경매 수익을 활용해 핵심 백본망의 현대화를 추진하고 있는 반면, 아르헨티나에서는 FTTH 도입이 가속화되고 있습니다. 중동에서는 ‘사우디 비전 2030’과 UAE의 스마트시티 구상에 따라 5G 독립형 코어가 구축되고 있으며, UPF 지원 라우터가 필요로 하고 있습니다. 아프리카 각국은 모잠비크의 ‘디지털 가속화 프로그램’ 등 세계은행의 보조금을 활용해 국내 광섬유망을 확장하고 있으며, 주변 온도 50℃에서도 작동 가능한 실외용 라우터 시장에 비즈니스 기회가 생겨나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the service provider router market size was valued at USD 13.7 billion in 2025 and is estimated to grow from USD 14.7 billion in 2026 to reach USD 21.2 billion by 2031, at a CAGR of 7.6% during the forecast period (2026-2031).

This report is Segmented by Router Type (Core Routers, Edge Routers, Aggregation Routers, and More), Bandwidth/Port Speed (Up To 40 Gbps, 40-100 Gbps, 100-400 Gbps, and More), Application (Telecom Service Providers, Cloud Service Providers, Internet Exchange Providers and More), Technology (Hardware-Based Routers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Service Provider Router Market Trends and Insights

5G And 5G-Advanced Backhaul Requirements

Mobile operators are moving from early 5G releases toward 5G-Advanced features such as network slicing and integrated access backhaul. China targeted 3.5 million base stations by year-end 2025, each requiring at least 10 G of backhaul capacity, creating incremental router demand exceeding 35 Tbit/s nationwide. South Korea's three carriers invested KRW 8.7 trillion (USD 6.5 billion) in backhaul upgrades in 2025. Huawei's FlexE 2.0 hard slicing and SRv6 segmentation enable sub-millisecond latency for enterprise SLA tiers. Nokia shipped more than one million AirScale microwave radios supporting 10 G E-band links, cutting urban fiber costs by 30%. These deployments prioritize timing protocols such as IEEE 1588v2 to maintain phase coherence across distributed antennas.

Proliferation Of 400 G / 800 G Routing Technology

The cost per transported bit has fallen roughly 60% since 2024, thanks to high-baud-rate coherent pluggables. Lumen activated 800G interfaces across its U.S. intercity backbone in 2025, reducing the required wavelengths per route by 75%. A Colt-Nokia field trial pushed 800 G QSFP-DD modules 120 km over standard fiber with no amplification. Arista's R4 routers aggregate 3.2 T on a single HyperPort, ideal for hyperscaler spine fabrics. Ciena's WaveLogic 6 Extreme optics achieved 1.6 T over 500 km, heralding terabit-class long-haul links. Multi-vendor interoperability under the OIF 800ZR spec is reducing lock-in and expediting volume deployments.

Semiconductor Supply-Chain Volatility

Lead times for 7 nm and 5 nm routing ASICs surpassed 40 weeks in early 2025, forcing 18-month capacity reservations and straining working capital. DDR4/DDR5 prices surged 80-90%, slicing mid-tier vendor margins by 5-7 points. A global HBM3 shortage, driven by AI accelerators, pushed several router makers toward higher-power GDDR6 buffers. TSMC's N3 node reached full allocation by mid-2025, leaving smaller fabless firms on older processes. Domestic foundry subsidies under the U.S. CHIPS Act will not soften bottlenecks before 2027, extending volatility through the near term.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Cloud Data Centers And DCI Traffic

- Rise Of AI Overlay Networks Requiring Lossless Ethernet

- Regulatory Restrictions On Chinese Vendors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge platforms are forecast to expand at an 8.94% CAGR, outstripping the overall service provider router market. Core chassis captured 35.4% of 2025 revenue, anchoring long-haul and metro backbones. Edge growth stems from private 5G networks and multi-access edge computing that require sub-millisecond latency near end users. Cisco's Catalyst 8200 shipped more than 50,000 units in 2025, bundling SD-WAN, IPsec, and application-aware routing to displace legacy branch appliances. Juniper's Session Smart Router pilot reduced WAN bandwidth by 30% at Fortune 500 sites. Aggregation routers remain steady in mature cable systems where DOCSIS 4.0 uplinks need 10 G and 25 G backhaul. Subscriber edge functions are virtualizing onto uCPE: Swisscom rolled out 10,000 OneOS6 appliances, cutting truck rolls by 60%. This shift directs capex from proprietary hardware toward x86-based white boxes, tightening margins for incumbents. Nevertheless, core routers retain relevance for tier-1 carriers managing networks beyond 100,000 route-km, where redundant fabric modules ensure five-nines uptime.

The segment's divergence illustrates how service provider router market size growth concentrates in distributed nodes while core refreshes flatten. Vendors that can package edge routing, compute, and security into a software-defined bundle are best positioned to capture incremental spend. Meanwhile, core-focused suppliers defend their share by integrating coherent optics and power-optimized silicon to squeeze more throughput per rack unit, delaying forklift upgrades.

Interfaces above 400 G are forecast to rise at a 12.42% CAGR, the fastest of any speed tier in the service provider router market. In 2025, 100 G-to-400 G ports still accounted for a commanding 34.82% of revenue, reflecting entrenched use in metro aggregation and data-center spines. Operators increasingly skip 100 G and move straight to 400 G or 800 G, as seen in Verizon's 2025 metro refresh that bypassed 100 G entirely. ZTE's ZXCTN 6120H-SE delivered 400 G in a compact base-station router, enabling terabit backhaul without cabinet upgrades.

Arista's XPO liquid-cooled pluggable alliance targets 1.6 T and 3.2 T modules dissipating 30 W+, pairing active thermal loops with standard QSFP-DD sockets. Ciena's WaveLogic 6 optics extend 1.6T wavelengths over 500 km, lowering regeneration costs and energy consumption per bit. As coherent pluggables collapse transponder shelves into router line cards, the service provider router market share for platforms above 400 G widens, pulling optical and IP budgets into a converged spend pool.

Geography Analysis

North America captured 41.28% of 2025 revenue, buoyed by USD 80 billion hyperscaler investment across Virginia, Oregon, and Texas. The Broadband Equity, Access, and Deployment program injects USD 42.45 billion into rural fiber networks, boosting demand for rugged aggregation routers. Energy-efficiency targets and Chinese vendor bans are accelerating domestic sourcing, advantaging local manufacturers.

Asia-Pacific is set for an 8.14% CAGR through 2031 as China's 5G-Advanced plan scales to 3.5 million base stations, each requiring 10 G backhaul. India's BharatNet allocated INR 139,000 crore (USD 16.7 billion) for fiber backbone projects. Japan's carriers spent JPY 1.8 trillion (USD 12 billion) on 5G in fiscal 2025. Southeast Asia's submarine-cable boom further props router demand in archipelagic states.

In Europe, operators invested EUR 45 billion (USD 50.9 billion) in 2025 networks despite tight capital outlays under EU Regulation 2023/826 that caps standby power at 8 W for high-performance appliances. Energy compliance costs encourage liquid-cooled optics and advanced thermal design, which favor vendors with deep R&D budgets.

South America leverages Brazil's spectrum auction proceeds to modernize core backbones, while Argentina accelerates FTTH adoption. The Middle East is deploying 5G standalone cores under Saudi Vision 2030 and UAE smart-city initiatives, requiring UPF-enabled routers. African nations tap World Bank grants, such as Mozambique's Digital Acceleration Program, to extend national fiber rings, creating opportunities for outdoor-rated routers capable of operating at 50 °C ambient temperatures.

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Juniper Networks, Inc.

- Nokia Corporation

- Hewlett Packard Enterprise Company

- ZTE Corporation

- Arista Networks, Inc.

- Ciena Corporation

- Extreme Networks, Inc.

- Dell Technologies Inc.

- NEC Corporation

- Fujitsu Limited

- Ribbon Communications Inc.

- Adtran Holdings, Inc.

- Edgecore Networks Corporation

- Telefonaktiebolaget LM Ericsson

- Allied Telesis Holdings Corporation

- Radisys Corporation

- D-Link Corporation

- Infinera Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G and 5G-Advanced Backhaul Requirements

- 4.2.2 Proliferation of 400G/800G Routing Technology

- 4.2.3 Expansion of Cloud Data Centers and DCI Traffic

- 4.2.4 Rise of AI Overlay Networks Requiring Lossless High-Bandwidth Backbone

- 4.2.5 Emerging Quantum-Safe Routing Protocol Adoption

- 4.2.6 Government Subsidies for Rural Fiber Backbone in Developing Countries

- 4.3 Market Restraints

- 4.3.1 Semiconductor Supply Chain Volatility

- 4.3.2 Regulatory Restrictions on Chinese Vendors

- 4.3.3 Transition to Virtualized Routing Compressing Hardware Margins

- 4.3.4 Increasing Energy Efficiency Mandates Raising Design Costs

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Router Type

- 5.1.1 Core Routers

- 5.1.2 Edge Routers

- 5.1.3 Aggregation Routers

- 5.1.4 Subscriber Edge Routers

- 5.2 By Bandwidth/Port Speed

- 5.2.1 Up to 40 Gbps

- 5.2.2 40-100 Gbps

- 5.2.3 100-400 Gbps

- 5.2.4 Above 400 Gbps

- 5.3 By Application

- 5.3.1 Telecom Service Providers

- 5.3.2 Cloud Service Providers

- 5.3.3 Internet Exchange Providers

- 5.3.4 Enterprises and Public Sector

- 5.4 By Technology

- 5.4.1 Hardware-Based Routers

- 5.4.2 Software-Defined/Virtual Routers (VNF/uCPE)

- 5.4.3 Disaggregated/White-Box Routers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Huawei Technologies Co., Ltd.

- 6.4.3 Juniper Networks, Inc.

- 6.4.4 Nokia Corporation

- 6.4.5 Hewlett Packard Enterprise Company

- 6.4.6 ZTE Corporation

- 6.4.7 Arista Networks, Inc.

- 6.4.8 Ciena Corporation

- 6.4.9 Extreme Networks, Inc.

- 6.4.10 Dell Technologies Inc.

- 6.4.11 NEC Corporation

- 6.4.12 Fujitsu Limited

- 6.4.13 Ribbon Communications Inc.

- 6.4.14 Adtran Holdings, Inc.

- 6.4.15 Edgecore Networks Corporation

- 6.4.16 Telefonaktiebolaget LM Ericsson

- 6.4.17 Allied Telesis Holdings Corporation

- 6.4.18 Radisys Corporation

- 6.4.19 D-Link Corporation

- 6.4.20 Infinera Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment