|

시장보고서

상품코드

2063846

GPU 콜드 플레이트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)GPU Cold Plate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

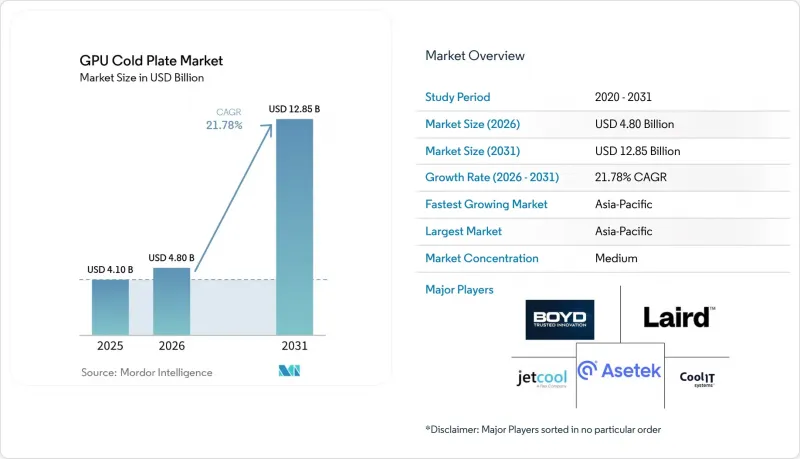

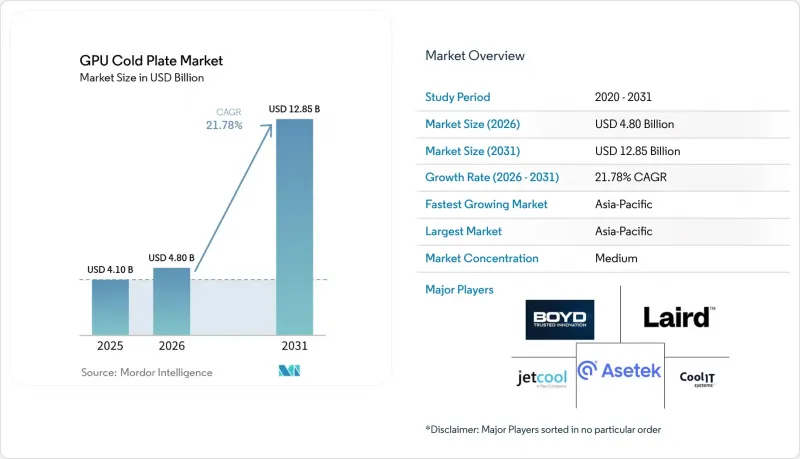

Mordor Intelligence에 의하면, GPU 콜드 플레이트 시장 규모는 2025년 41억 달러로 평가되었습니다. 2026년에는 48억 달러로 확대되어 2031년까지 128억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 21.78%로 성장할 전망입니다.

본 보고서는 냉각 방식(단상 및 2상), 설계 유형(마이크로채널, 제트 임팩트, 하이브리드/어드밴스드), 도입 환경(하이퍼스케일/클라우드, 엔터프라이즈, 정부·연구용 HPC, 엣지 AI), GPU 전력 밀도(300W 미만, 300W-700W, 700W 초과), 지역(북미, 아시아태평양, 기타)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 GPU 콜드 플레이트 시장 동향 및 인사이트

하이퍼스케일 데이터센터에서의 액체 냉각 도입 가속화

하이퍼스케일 제공업체는 2025년에 200메가와트 이상의 수냉식 GPU 용량을 추가했습니다. 이는 2023년 도입량에 비해 5배 증가한 수치입니다. 이는 랙 부하가 80kW를 초과하면 공랭식 냉각을 경제적으로 유지하기 어려워졌기 때문입니다. 마이크로소프트의 페어워터 캠퍼스에서는 40%의 에너지 절감 효과가 입증되었으며, 설비 투자가 즉시 영업이익으로 전환되었습니다. 메타가 향후 도입될 모든 AI 클러스터에 수냉식 시스템을 의무적으로 탑재하도록 함에 따라, 사실상 업계 표준이 확립되었고, 공급업체들은 생산 규모를 확대해야만 했습니다. 수냉식 가속기는 부스트 클럭을 장시간 유지할 수 있어 트레이닝 처리량이 직접적으로 향상되며, GPU 활용도 증대를 통해 비즈니스 타당성이 더욱 강화됩니다. 이러한 요인들이 복합적으로 작용하여 수주량이 급증했고, 그 결과 콜드 플레이트의 단가가 하락하고 있습니다.

증가하는 GPU의 전력 밀도가 공랭식의 한계를 넘어선다.

NVIDIA H200 및 AMD MI300A 칩은 2025년에 760와트에 도달하며, 귀를 찢을 듯한 팬 회전수에 의존하지 않고도 공랭식의 실질적인 한계를 뛰어넘었습니다. 공기의 열전도율이 낮기 때문에 열유속 제거 능력은 0.5 W cm?² 정도로 제한되지만, 수냉 플레이트는 5 W cm?² 이상을 실현하여 주변 온도 25°C 환경에서도 성능 저하를 해소합니다. 실제 데이터에 따르면, 기온이 27℃를 초과하면 공랭식 클러스터의 18%에서 훈련 에포크 중에 스로틀링이 발생했습니다. 콜드 플레이트는 이러한 변동을 해소하여, 특히 싱가포르와 같은 열대 지역의 데이터센터 허브에서 운영자가 자본 집약적인 가속기의 성능을 최대한 끌어낼 수 있도록 합니다.

액체 냉각 시스템 도입에 따른 높은 초기 비용

단상 콜드 플레이트를 사후 장착한 10랙 규모의 GPU 클러스터에는 약 40만 달러의 초기 투자가 필요하며, 이는 동등한 수준의 공랭식 설비 설치 비용의 3배에 달할 전망입니다. 2상 시스템은 냉매 펌프, 열교환기, 인증 배관이 추가되기 때문에 비용이 더욱 높아집니다. 코로케이션 환경에서는 고객별 분리 및 계측 하드웨어가 필요하며, 이로 인해 랙당 비용이 1만 5,000-2만 5,000달러 더 증가합니다. 투자 회수 기간이 3년 미만이 되는 경우는 전기 요금이 1kWh당 0.10달러를 초과하는 지역으로 한정되기 때문에 많은 저요금 지역에서는 도입이 진전되지 않습니다. 또한, 기업의 IT 예산에는 대개 포함되지 않는 직원 교육 비용이 벤더와의 필수 서비스 계약을 통해 라이프사이클 비용을 더욱 높입니다.

부문별 분석

단상 시스템은 냉수 루프와의 플러그 앤 플레이 방식의 호환성과 비교적 적은 운영 기술이 필요하다는 점 덕분에 2025년 매출의 74.69%를 차지했습니다. 핵심인 300와트에서 700와트 대역에서는 단상 플레이트가 2-4 L/min의 유량으로 열 부하를 충족시키면서, 펌프의 소비 전력을 관리 가능한 범위로 억제하고 있습니다. 2상 시스템은 시장 점유율이 25.31%에 그치지만, 200 W/cm²를 초과하는 방열 능력을 바탕으로 1,000와트를 넘는 차세대 GPU의 성능 한계를 해소하기 위해 21.98%의 성장률을 보이고 있습니다. 이러한 설계를 시범 도입하고 있는 하이퍼스케일 사업자들은 냉각 에너지 사용량을 60% 절감할 수 있었습니다고 보고하고 있으며, 열을 드라이 쿨러로 직접 배출할 수 있기 때문에 칠러 설비가 필요 없어져, 수익을 창출하는 랙을 설치할 공간을 확보할 수 있게 됩니다.

단상 프라이머리 루프와 2상 핫스팟 모듈을 결합한 하이브리드 아키텍처가 실용적인 가교 역할로 부상하고 있습니다. 파커 하니핀의 ‘HyperCool’과 같은 제품은 대량의 열을 제거하기 위한 물·글리콜 회로와, 국소적인 피크에서 냉매를 기화시키는 내장형 히트파이프를 결합하여, 현장 전체에서 냉매 처리가 필요 없이 150 W cm-²의 냉각 성능을 실현하고 있습니다. 2상 기술의 보급과 저GWP 냉매의 성숙에 따라, GPU 콜드플레이트 시장에서는 특히 기존 수냉 루프의 유량 한계에 도달하는 100kW를 초과하는 랙의 경우, 완전 2상 플레이트로 시장 점유율 전환이 점차 진행될 것으로 예측됩니다.

마이크로채널 플레이트는 CNC 가공 기술이 성숙되어 있고, 비용 효율성이 뛰어나며, 10년에 걸친 서버 OEM을 통한 검증 실적이 뒷받침되고 있기 때문에 2025년에도 63.56%의 시장 점유율을 유지했습니다. 그러나 물리적 제약으로 인해 채널 폭이 좁아질수록 압력 손실이 4제곱에 비례하여 증가하기 때문에 800와트급 GPU로의 확장성에는 한계가 있습니다. 제트 임팩트 설계는 고속 냉각제 제트를 다이에 수직으로 분사함으로써 이 문제를 해결하며, 동등한 마이크로채널 솔루션에 비해 30% 적은 펌프 동력으로 300 W/cm²를 초과하는 냉각 밀도를 실현하고 있습니다.

제조상의 제약으로 인해 제트 임팩트 기술은 여전히 비용이 높았으나, 자동화된 레이저 천공 및 3D 프린팅을 활용한 노즐 어레이 기술이 그 비용 격차를 점차 좁혀가고 있습니다. 2028년까지 각 공급업체들이 비용 면에서 대등한 수준에 도달함에 따라, Boyu Liquid Cooling은 700와트 이상의 틈새 시장에서 제트 임팩트 기술이 주류가 되는 것을 목표로 하고 있습니다. 한편, 마이크로채널 베이스 레이어와 베퍼 챔버 또는 노즐 인서트를 결합한 하이브리드 플레이트는 신뢰성과 극한의 과도 성능을 모두 요구하는 금융 거래 클러스터 등, 비용 효율성과 핫스팟 강도가 공존하는 워크로드에 대응합니다.

지역별 분석

아시아태평양은 2025년에 매출의 68.53%를 차지하며 GPU 콜드플레이트 시장을 주도했으며, 2031년까지 연평균 22.78%의 성장률이 예상됩니다. 중국 공업정보화부는 액체 냉각 방식의 AI 인프라에 500억 위안(70억 달러)을 배정하며, 알리바바 클라우드의 10만 GPU 규모 우란차브 캠퍼스와 같은 대규모 수주를 주도하고 있습니다. 싱가포르는 PUE 상한선을 1.3으로 설정하고 있는데, 이는 사실상 액체 냉각을 의무화하는 조치입니다. 디지털 리얼티의 12억 6,000만 달러 규모 주롱 캠퍼스에서는 칠러 부하를 피하기 위해 해수를 이용한 열 방출 방식이 채택되었습니다. 인도는 하이퍼스케일 시설 건설을 빠른 속도로 추진하고 있으며, 슈나이더 일렉트릭의 방갈로르 공장 등 현지 제조업체들은 2026년 말까지 연간 5만 장의 플레이트를 생산하여 수입 의존도를 낮출 계획입니다.

북미는 2025년 매출의 약 18%를 차지하며, 위스콘신주, 오리건주, 버지니아주의 하이퍼스케일 캠퍼스가 그 핵심을 이루었습니다. 미국 연방정부 및 주정부의 인센티브 덕분에 기업의 투자 회수 기간이 단축되고 있습니다. 또한, 한랭 지역에서는 여름철 피크 시간대에 700와트 칩을 주변의 자연 냉각만으로는 처리할 수 없기 때문에 GPU 랙에는 여전히 액체 냉각 방식이 채택되고 있습니다. 캐나다의 사업자들은 액체 냉각을 통해 서버를 집약할 수 있게 되고, 연중 높은 연산 밀도를 실현함으로써 수개월에 걸친 자연 대류 냉각의 이점을 상쇄할 수 있다고 인식하고 있습니다.

유럽은 매출의 약 10%를 차지하며, 에너지 효율 지침이 사업자들에게 규제상의 압박을 가하고 있습니다. 독일의 헤츠너사는 팔켄슈타인에서 PUE 1.25를 달성하여 가속 상각을 확보했습니다. 한편, 영국은 기본적으로 액체 냉각 방식을 채택하는 대학 클러스터를 위해 2억 파운드(2억 5,500만 달러)를 배정했습니다. 남미, 중동 및 아프리카의 합계는 4% 미만에 그치고 있지만, 전략적으로 중요한 지역입니다. 브라질 상파울루 캠퍼스는 저탄소 이미지를 강조하기 위해 수력 발전망을 활용하고 있으며, 아랍에미리트의 AI71 프로젝트는 여름철 기온 45℃에 대응하기 위해 2상 침지 냉각 장치를 건설하고 있습니다. 물 부족 문제가 완화되면, 2031년까지 세계 시장 점유율 5%를 확보하는 것을 목표로 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the gPU cold plate market size is expected to increase from USD 4.1 billion in 2025 to USD 4.8 billion in 2026 and reach USD 12.85 billion by 2031, growing at a CAGR of 21.78% over 2026-2031.

This report is Segmented by Cooling Type (Single-Phase, and Two-Phase), Design Type (Microchannel, Jet Impingement, and Hybrid/Advanced), Deployment Environment (Hyperscale/Cloud, Enterprise, Government and Research HPC, and Edge AI), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography (North America, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global GPU Cold Plate Market Trends and Insights

Accelerating Adoption of Liquid Cooling in Hyperscale Data Centers

Hyperscale providers added more than 200 megawatts of liquid-cooled GPU capacity during 2025, a fivefold jump from 2023 deployments, as air cooling became economically untenable once rack loads exceeded 80 kilowatts. Microsoft's Fairwater campus validated a 40% energy-savings metric, turning capital expenditure into immediate operating profit. Meta's mandate that every forthcoming AI cluster ship with liquid cooling set a de facto industry baseline that pushed suppliers to scale production. Higher GPU utilization reinforces the business case because liquid-cooled accelerators sustain boost clocks for longer duty cycles, directly raising training throughput. These factors combine to accelerate order volumes that, in turn, compress per-unit costs for cold plates.

Rising GPU Power Densities Surpassing Air Cooling Limits

NVIDIA H200 and AMD MI300A chips hit 760 watts in 2025, surpassing air cooling's practical ceiling without resorting to deafening fan speeds. Air's poor thermal conductivity caps heat-flux removal near 0.5 W cm-2, while water-based plates deliver 5 W cm-2 or higher, eliminating performance throttling even in 25 °C ambient conditions. Field data show that air-cooled clusters throttled during 18% of training epochs when temperatures rose past 27 °C. Cold plates remove that variability, ensuring operators extract the full value from capital-intensive accelerators, especially in tropical data center hubs such as Singapore.

High Upfront Cost of Liquid Cooling Deployment

A 10-rack GPU cluster retrofitted with single-phase cold plates requires roughly USD 400,000 in capital, triple the outlay for a comparable air-cooled install. Two-phase systems cost even more because they add refrigerant pumps, heat exchangers, and certified piping. Colocation environments add customer isolation and metering hardware, which inflates rack costs by an additional USD 15,000-25,000. Payback drops below three years only where electricity rates top USD 0.10 kWh-1, leaving many low-tariff regions unmoved. Staff training, often absent in enterprise IT budgets, further inflates life-cycle expense through mandatory vendor service contracts.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Energy-Efficient Infrastructure

- Increasing AI Model Complexity Requiring Higher Thermal Performance

- Compatibility Challenges with Existing Rack Infrastructures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase systems accounted for 74.69% of 2025 revenue, driven by their plug-and-play fit with chilled-water loops and the modest operational skills required. In the core 300-watt-to-700-watt band, single-phase plates satisfy thermal loads at 2-4 L min-1 flow while keeping pump power manageable. Two-phase systems, although at only 25.31% share, are scaling at 21.98% because they dissipate over 200 W cm-2, unlocking next-generation GPU envelopes above 1,000 watts. Hyperscale operators piloting these designs report 60% reductions in cooling energy use and the ability to dump heat directly into dry coolers, eliminating chiller plants and freeing real estate for revenue-generating racks.

Hybrid architectures that blend single-phase primary loops with two-phase hotspot modules are emerging as a pragmatic bridge. Products such as Parker-Hannifin's HyperCool pair water-glycol circuits for bulk removal with embedded heat pipes that vaporize refrigerant at localized peaks, delivering 150 W cm-2 without site-wide refrigerant handling. As two-phase expertise diffuses and low-GWP fluids mature, the GPU cold plate market is likely to witness gradual share transfer toward full two-phase plates, especially for racks exceeding 100 kilowatts, where traditional water loops hit flow-rate ceilings.

Microchannel plates retained 63.56% share in 2025 because CNC machining is mature, cost-effective, and backed by a decade of server OEM validation. However, physics impose a fourth-power rise in pressure drop as channel width narrows, capping scalability for 800-watt GPUs. Jet impingement designs circumvent this by firing high-velocity coolant jets perpendicularly onto the die, achieving above 300 W cm-2 while using 30% less pumping power than equivalent microchannel solutions.

Manufacturing constraints kept jet impingement costly, yet automated laser drilling and 3D-printed nozzle arrays are closing the gap. As vendors reach cost parity by 2028, Boyu Liquid Cooling targets jet impingement to dominate the above-700-watt niche. Meanwhile, hybrid plates combining microchannel base layers with vapor chambers or nozzle inserts address workloads where cost sensitivity and hotspot intensity coexist, such as financial trading clusters demanding both reliability and extreme transient performance.

Geography Analysis

Asia-Pacific led the GPU cold plate market with 68.53% revenue in 2025 and is forecast to grow at 22.78% through 2031. China's Ministry of Industry and Information Technology earmarked CNY 50 billion (USD 7 billion) for liquid-ready AI infrastructure, driving massive orders such as Alibaba Cloud's 100,000-GPU Ulanqab campus. Singapore enforces a 1.3 PUE ceiling that virtually mandates liquid cooling; Digital Realty's USD 1.26 billion Jurong campus showcased seawater heat rejection to sidestep chiller loads. India is fast-tracking hyperscale builds, and local manufacturers like Schneider Electric's Bangalore plant will produce 50,000 plates annually by year-end 2026, cutting import dependence.

North America contributed roughly 18% of 2025 revenue, anchored by hyperscale campuses in Wisconsin, Oregon, and Virginia. U.S. federal and state incentives shorten enterprise payback periods, and in cold-climate regions, liquid cooling is still adopted for GPU racks because ambient free cooling alone cannot handle 700-watt chips during summer peaks. Canada's operators find that liquid cooling lets them consolidate servers, offsetting months of free-air advantage with higher annual compute density.

Europe clocked about 10% of revenue, with the Energy Efficiency Directive placing a regulatory gun to operators' heads. Germany's Hetzner achieved 1.25 PUE in Falkenstein and secured accelerated depreciation, while the United Kingdom earmarked GBP 200 million (USD 255 million) for university clusters that default to liquid cooling. South America and the Middle East and Africa together contributed under 4% yet display strategic importance. Brazil's Sao Paulo campus leverages hydroelectric grids for low-carbon marketing, and the Emirates' AI71 project builds two-phase immersion rigs to cope with 45 °C summers, aiming to claim a 5% global share by 2031 if water-scarcity challenges are mitigated

- CoolIT Systems Inc.

- Asetek A/S

- BOYD Corporation

- JetCool Technologies Inc.

- Laird Thermal Systems Inc.

- Nidec Corp.

- Danfoss A/S

- Schneider Electric SE

- Rittal GmbH and Co. KG

- LiquidStack Inc.

- Alfa Laval AB

- Fujikura Ltd.

- Advanced Cooling Technologies Inc.

- Lytron LLC

- TE Connectivity Ltd.

- Parker-Hannifin Corporation

- AMAX Information Technologies Inc.

- Cool-IT Science Ltd.

- Midas Cooling Solutions LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Adoption of Liquid Cooling in Hyperscale Data Centers

- 4.2.2 Rising GPU Power Densities Surpassing Air Cooling Limits

- 4.2.3 Government Incentives for Energy-Efficient Data Center Infrastructure

- 4.2.4 Increasing AI Model Complexity Demanding Higher Thermal Management Performance

- 4.2.5 Emergence of Open-Hardware Cold Plate Standards Reducing Vendor Lock-In

- 4.2.6 Advancements in Low-Fluorinated Dielectric Fluids Enabling Two-Phase Cold Plates

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Liquid Cooling Deployment

- 4.3.2 Compatibility Challenges with Existing Rack Infrastructures

- 4.3.3 Limited Field Expertise for Operational Maintenance of Two-Phase Systems

- 4.3.4 Supply Chain Constraints for High-Precision Microchannel Machining

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Type

- 5.1.1 Single-Phase Cold Plates

- 5.1.2 Two-Phase Cold Plates

- 5.2 By Design Type

- 5.2.1 Microchannel Cold Plates

- 5.2.2 Jet Impingement Cold Plates

- 5.2.3 Hybrid / Advanced Designs

- 5.3 By Deployment Environment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge AI

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W-700W

- 5.4.3 Above 700W

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CoolIT Systems Inc.

- 6.4.2 Asetek A/S

- 6.4.3 BOYD Corporation

- 6.4.4 JetCool Technologies Inc.

- 6.4.5 Laird Thermal Systems Inc.

- 6.4.6 Nidec Corp.

- 6.4.7 Danfoss A/S

- 6.4.8 Schneider Electric SE

- 6.4.9 Rittal GmbH and Co. KG

- 6.4.10 LiquidStack Inc.

- 6.4.11 Alfa Laval AB

- 6.4.12 Fujikura Ltd.

- 6.4.13 Advanced Cooling Technologies Inc.

- 6.4.14 Lytron LLC

- 6.4.15 TE Connectivity Ltd.

- 6.4.16 Parker-Hannifin Corporation

- 6.4.17 AMAX Information Technologies Inc.

- 6.4.18 Cool-IT Science Ltd.

- 6.4.19 Midas Cooling Solutions LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment