|

시장보고서

상품코드

2063854

유럽의 자동차용 LED 패키지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Automotive LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

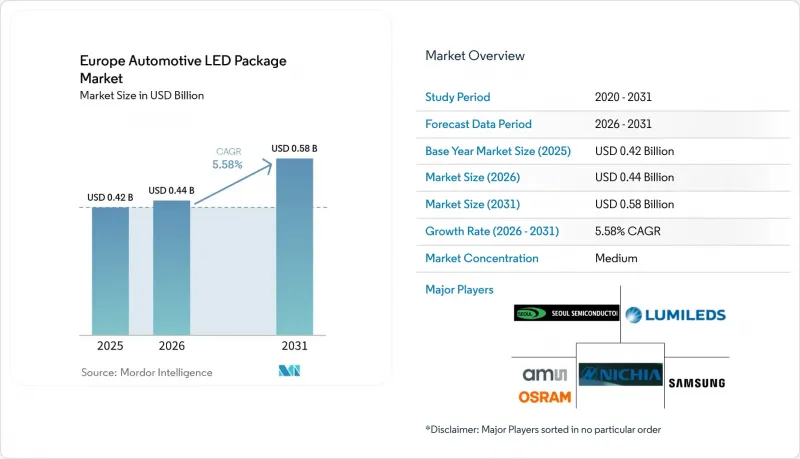

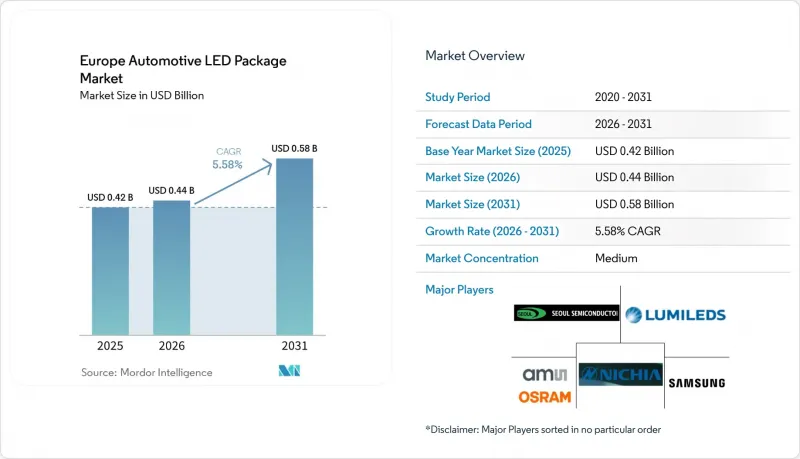

Mordor Intelligence에 의하면, 자동차용 LED 패키지 시장 규모는 2025년 4억 2,000만 달러로 평가되었습니다. 2026년에는 4억 4,000만 달러로 확대되어 2031년까지 5억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 5.58%를 나타낼 전망입니다.

본 보고서는 패키지 구조(SMD, CSP, 플립칩 LED 패키지, COB), 출력 등급(0.5W 미만의 저출력, 0.5-1W의 중출력, 1W 초과의 고출력), 용도(외장 조명, 내장 조명 등), 차종(승용차, 상용차), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 자동차용 LED 패키지 시장 동향 및 분석

할로겐에서 LED 헤드램프로의 급속한 전환

2022년 유엔 규정 제37호의 개정에 따라, 할로겐 램프 장착 위치에 인증된 LED 교체용 전구를 도입하기 위한 법적 기반이 마련되었습니다. 2025년 5월, ams OSRAM은 최초의 ECE 인증 H11 LED 교체용 전구를 출하하며, 에너지 소비량을 5분의 1로 줄이고 수명을 6배 연장하겠다고 약속했습니다. 할로겐 전구 전체 라인업을 지원하기 위한 단계적 로드맵은 2028년까지 이어지며, 유럽의 2억 5,200만 대에 달하는 승용차 시장에서 향후 수년에 걸쳐 사후 교체 시장을 개척할 것입니다. 동시에, 스텔란티스 등 각 OEM 업체들은 더 낮은 비용과 낮은 전력 소비로 할로겐 램프의 광도 특성을 충족하는 소형 Bi-LED 모듈을 발표하고 있으며, 이는 신형 엔트리 모델 차량에서 비용 최적화된 LED에 대한 병행 수요를 시사하고 있습니다. 따라서 패키지 공급업체는 열적으로 견고한 개조용 형식과 초소형 OEM 솔루션으로 제품 포트폴리오를 구분해야 하며, 각각에 따라 서로 다른 임피던스 및 드라이버 IC 전략이 요구됩니다.

어댑티브 프론트 라이팅 시스템(AFLS)에 대한 수요 증가

유엔 규정 제123호의 조화를 통해 어댑티브 드라이빙 빔(ADB)의 형식 인증 장벽이 낮아졌으며, 이 기능은 고급차에서 일반 시장용 모델로 확대되었습니다. 아우디의 2026년형 Q3는 2만 5,600픽셀의 마이크로 LED 매트릭스를 최초로 탑재했으며, 한편, 닛야 화학공업의 3단계 구성으로 이루어진 ‘Pixelated Light Source’ 제품군을 통해 OEM 각사는 새로운 하우징을 준비하지 않고도 엔트리 모델부터 프리미엄 모델에 이르기까지 ADB를 확장할 수 있게 되었습니다. 인피니언의 통합형 LITIX 드라이버는 도심 주행 사이클에서 대기 전력을 50% 절감하여 BEV의 효율 목표를 달성합니다. 이러한 아키텍처는 LED 에피택시와 ASIC의 공동 설계를 결합하는 공급업체에 유리한 조건을 제공함으로써, 고화소 모듈 시장에서 ‘승자 독식’ 추세를 가속화하고 있습니다.

2025년 이후 자동차 생산 대수의 변동

유럽의 생산 대수는 팬데믹 이전 최고치보다 300만 대 낮은 수준을 유지하고 있으며, 2024년 이후 공급업체에서 10만 명 이상의 일자리가 사라졌습니다. 영국에서는 사이버 공격과 관세 문제의 영향으로 2025년 생산량이 15.5% 감소했습니다. 또한, 밴과 트럭의 등록 대수는 각각 8.8%와 6.2% 감소했습니다. 에너지 가격 급등, 인력 부족, 저스트-인-타임(JIT) 방식의 혼란으로 인해 LED 제조업체의 운전 자금 비용이 증가하고 있으며, 최종 시장의 다각화가 진전되지 않은 기업들은 가동률이 낮은 클린룸을 가동할 수밖에 없어 이익률이 압박받고 있습니다.

부문별 분석

2025년에는 칩 스케일 패키지(CSP)가 자동차용 LED 패키지 시장 규모에서 차지하는 비중이 확대되어, 2031년에 이르러 기존의 표면 실장 소자(SMD)를 능가하는 성장을 이룰 것으로 전망됩니다. CSP는 칩을 기판에 직접 접합하기 때문에 열 저항을 낮추고, 적응형 빔에 적합한 픽셀 피치를 실현합니다. 이 공급업체는 각 다이 크기가 100µm 미만인 마이크로 LED 어레이에 CSP를 활용하고 있으며, 크로스 토크를 억제하면서 2만 5,000픽셀을 초과하는 매트릭스를 지원합니다. 플립칩 방식은 1만 칸델라를 초과하는 헤드램프 빔에 대해 뛰어난 전류 분산 성능을 제공하지만, 공극이 없는 본딩이 요구되므로 보다 엄격한 공정 관리가 필요합니다. 비용 효율을 중시하는 주간 주행등 시장에서는 여전히 기존의 SMD 패키지가 주류를 이루고 있지만, 각 OEM 업체들이 LED와 드라이버를 단일 기판 위에 통합한 시스템 통합형 솔루션으로 전환함에 따라 그 시장 점유율은 줄어들고 있습니다. 칩 온 보드는 엔트리 레벨 반사판용으로는 여전히 저비용 옵션이지만, 교체할 수 없습니다는 점이 EU의 순환 경제에 관한 논의와 상충되어, 이것이 보급을 저해할 수 있는 잠재적 요인으로 작용하고 있습니다.

2025년 자동차용 LED 패키지 시장 점유율 1위는 여전히 SMD가 차지했지만, CSP의 연평균 성장률(CAGR) 6.01%는 가장 급격한 성장세를 보이고 있습니다. 고화소 어댑티브 라이팅, 디지털 사이니지, 그릴 조명은 모두 CSP의 낮은 Z축 높이와 열전도 경로의 장점을 활용하여, 공기역학적 성능을 향상시키는 슬림형 램프 프로파일을 구현하고 있습니다. CSP 칩을 인피니온이나 NXP의 드라이버 ASIC과 함께 묶어 공급하는 업체는 시스템의 정착도를 높이는 반면, 범용 SMD로만 한정된 공급업체는 가격 압박의 위험에 직면하게 됩니다. 교체 가능한 LED 광원을 둘러싼 EU 내 논의는 수요를 모듈 형식으로 되돌릴 가능성도 있어, SMD, CSP, 그리고 새롭게 등장한 플러그인 LED 엔진 규격 간의 경쟁이 벌어질 것입니다.

2025년에는 1W를 초과하는 고출력 패키지가 자동차용 LED 패키지 시장 매출의 60% 가까이 차지했습니다. 이는 유엔 규정 112호의 광속 임계값에 따라 헤드램프가 고휘도 시스템으로 고정되었기 때문입니다. 프리미엄 ADB 모듈은 일반적으로 2,000루멘을 초과하기 때문에 세척 및 레벨링이 필요하지만, 다수의 중출력 칩 대신 단일 고출력 다이를 사용함으로써 이를 최적으로 구현할 수 있으며, 광학 시스템과 배선을 간소화할 수 있습니다. 중출력 LED는 밝기 요구 사항이 중간 수준인 코너링 라이트나 신호등과 같은 틈새 시장을 채우고 있지만, 그 판매량만으로는 가격 하락을 상쇄할 수 없습니다. 저출력 LED는 여전히 차량 내 간접 조명이나 계기판 백라이트에 없어서는 안 될 요소이지만, ISELED의 스마트 RGB 장치는 드라이버를 내장함으로써 그 경계를 모호하게 만들고, 가치를 개별 패키지에서 반도체 집적형 조명으로 전환시키고 있습니다.

고출력 LED의 우위는 프로젝션 헤드램프와 마이크로 LED 어레이에 힘입어 연평균 성장률(CAGR) 5.94%로 지속될 전망이지만, 열 설계상의 한계는 현실적인 과제입니다. 각 공급업체는 접합부의 온도를 125℃ 미만으로 유지하기 위해 증기실이나 흑연 시트를 적용하고 있으며, 이는 2만 5,000시간을 초과하는 L70 수명을 달성하기 위한 필수 요건입니다. 제곱센티미터당 10W를 초과하는 열 관리를 할 수 없는 공급업체는 차세대 헤드램프 시장에서 배제될 위험이 있습니다. 한편, 저전력 인테리어용 LED는 맞춤형 차량 실내 공간과 에너지 절약을 추구하는 BEV(배터리 전기자동차) 수요를 배경으로 성장하고 있으며, 제어 가능한 RGB 스트립을 통해 인포테인먼트와 동기화된 테마를 무선으로 전송할 수 있게 됩니다.

기타 장점 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the automotive lED package market size is expected to increase from USD 0.42 billion in 2025 to USD 0.44 billion in 2026 and reach USD 0.58 billion by 2031, growing at a CAGR of 5.58% over 2026-2031.

This report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, and COB), Power Class (Low Power Less Than 0. 5 W, Mid Power 0. 5-1 W, and High Power Greater Than1 W), Application (Exterior Lighting, Interior Lighting, and More), Vehicle Type (Passenger Vehicles, and Commercial Vehicles), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Automotive LED Package Market Trends and Insights

Rapid Shift From Halogen to LED Headlamps

UN Regulation 37 amendments in 2022 cleared the legal path for certified LED retrofit bulbs in halogen positions. In May 2025, ams OSRAM shipped the first ECE-approved H11 LED replacements, promising fivefold energy savings and six times longer life. A phased roadmap runs through 2028 to address the full halogen bulb family, opening a multiyear retrofit opportunity across Europe's 252 million-unit passenger fleet. Concurrently, OEMs like Stellantis have showcased compact Bi-LED modules that meet halogen photometry at lower cost and power, signaling parallel demand for cost-optimized LEDs in new entry vehicles. Package suppliers must therefore split portfolios between thermally robust retrofit formats and ultra-compact OEM solutions, each requiring different impedance and driver-IC strategies.

Growing Demand for Adaptive Front-Lighting Systems

UN Regulation 123 harmonization lowered homologation barriers for adaptive driving beam (ADB), shifting the feature from luxury to mass-market trims. Audi's 2026 Q3 debuts a micro-LED matrix with 25,600 pixels, while Nichia's three-tier Pixelated Light Source family lets OEMs scale from entry to premium ADB without new housings. Integrated Infineon LITIX drivers cut idle power by 50% during city cycles, meeting BEV efficiency targets. These architectures favor suppliers that combine LED epitaxy with ASIC co-design, accelerating a "winner-take-most" dynamic in high-pixel modules.

Volatility in Automotive Production Volumes Post-2025

European builds remain 3 million units below pre-pandemic peaks, with 100,000+ supplier jobs lost since 2024. UK output fell 15.5% in 2025 amid cyberattacks and tariff woes, and van plus truck registrations slid 8.8% and 6.2% respectively. Energy inflation, labor shortages, and just-in-time disruptions raise working-capital costs for LED makers, forcing those without diversified end markets to operate under-utilized cleanrooms that erode margins.

Other drivers and restraints analyzed in the detailed report include:

- Stringent EU CO2 Regulations Driving Energy-Efficient Lighting

- Mini-LED and Micro-LED Integration in Premium Models

- Thermal Management Challenges at Power Classes Above 1 W

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale packages accounted for a rising slice of the Automotive LED package market size in 2025 and will out-grow legacy surface-mount devices through 2031. CSP attaches the die directly to the substrate, cutting thermal resistance and enabling pixel pitches fit for adaptive beams. Suppliers leverage CSP in micro-LED arrays where each die is <100 µm, limiting crosstalk while supporting >25,000-pixel matrices. Flip-chip variants offer superior current spreading for >10,000-candela headlamp beams yet demand void-free bonding, driving tighter process controls. Traditional SMD packages still dominate cost-sensitive daytime running lamps, but their share erodes as OEMs pivot to system-integrated solutions that combine LEDs and drivers on a single board. Chip-on-board remains the low-cost choice for entry reflectors, though its non-replaceability conflicts with EU circularity debates, a potential headwind to wide adoption.

The Automotive LED package market share leader in 2025 remained SMD, yet CSP's 6.01% CAGR gives it the steepest trajectory. High-pixel adaptive lighting, digital signage, and grille illumination all benefit from CSP's lower Z-height and thermal path, allowing thinner lamp profiles that improve aerodynamics. Suppliers that bundle CSP dies with Infineon or NXP driver ASICs gain system stickiness, while those limited to commodity SMD risk compression. EU discussions around replaceable LED sources may even tilt volume back to modular formats, creating a three-way contest among SMD, CSP, and emerging plug-in LED engine standards.

High-power packages above 1 W contributed nearly 60% of Automotive LED package market revenue in 2025 as UN Regulation 112 flux thresholds lock headlamps into high-luminous systems. Premium ADB modules routinely exceed 2,000 lumens and thus require cleaning and leveling, activities best met by single high-power dies rather than many mid-power chips, simplifying optics and wiring. Mid-power LEDs fill cornering and signal niches where intensity demands are moderate, but their unit volumes cannot offset falling prices. Low-power LEDs remain vital for ambient interiors and cluster backlighting; however, ISELED smart RGB devices blur the line by embedding drivers, which shifts value from discrete packages to semiconductor-integrated lights.

High-power dominance will persist, with a 5.94% CAGR driven by projection headlamps and micro-LED arrays, yet thermal ceilings are real. Suppliers integrate vapor chambers or graphite sheets to keep junctions under 125 °C, a requirement for L70 lifetime beyond 25,000 hours. Vendors unable to manage >10 W per square centimeter risk exclusion from next-gen headlamps. Conversely, low-power interior LEDs thrive on BEV demand for customizable cabins and energy savings, with addressable RGB strips enabling over-the-air themes that synchronize with infotainment.

List of Companies Covered in this Report:

- ams OSRAM AG

- Nichia Corporation

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED

- Lite-On Technology Corporation

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- EVERLIGHT Electronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- ROHM Co., Ltd.

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- Hella GmbH & Co. KGaA

- Valeo S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Shift From Halogen to LED Headlamps

- 4.2.2 Growing Demand for Adaptive Front-Lighting Systems

- 4.2.3 Stringent EU CO2 Regulations Driving Energy-Efficient Lighting

- 4.2.4 Mini-LED and Micro-LED Integration in Premium Models

- 4.2.5 Supply Chain Localization Incentives in Eastern Europe

- 4.2.6 Automotive Cyber-Security Standards Requiring IR LEDs

- 4.3 Market Restraints

- 4.3.1 Volatility in Automotive Production Volumes Post-2025

- 4.3.2 Thermal Management Challenges at >1 W Power Class

- 4.3.3 Patent Cliffs and Ongoing LED IP Litigations in Europe

- 4.3.4 Rising Import Duties on Asian LED Packages After CBAM Roll-out

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 CSP (Chip Scale Package)

- 5.1.3 Flip-Chip LED Packages

- 5.1.4 COB (Chip-on-Board)

- 5.2 By Power Class

- 5.2.1 Low Power (<0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (>1 W)

- 5.3 By Application

- 5.3.1 Exterior Lighting

- 5.3.2 Interior Lighting

- 5.3.3 Sensing / IR Applications

- 5.3.4 Other Applications (Signaling, minor)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Vehicles

- 5.4.2 Commercial Vehicles

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Nichia Corporation

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Cree LED

- 6.4.8 Lite-On Technology Corporation

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 EVERLIGHT Electronics Co., Ltd.

- 6.4.12 Dominant Opto Technologies Sdn. Bhd.

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 Lextar Electronics Corporation

- 6.4.15 NationStar Optoelectronics Co., Ltd.

- 6.4.16 Sanan Optoelectronics Co., Ltd.

- 6.4.17 Refond Optoelectronics Co., Ltd.

- 6.4.18 Hella GmbH & Co. KGaA

- 6.4.19 Valeo S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment