|

시장보고서

상품코드

2063875

디지털 콜드체인 관리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Digital Cold Chain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

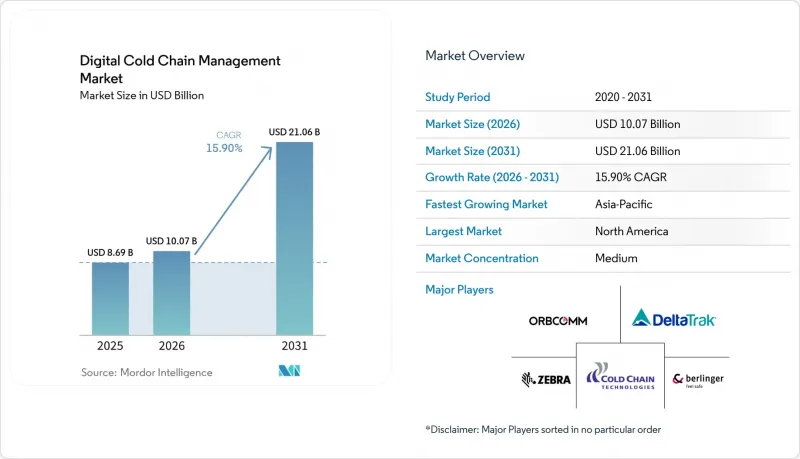

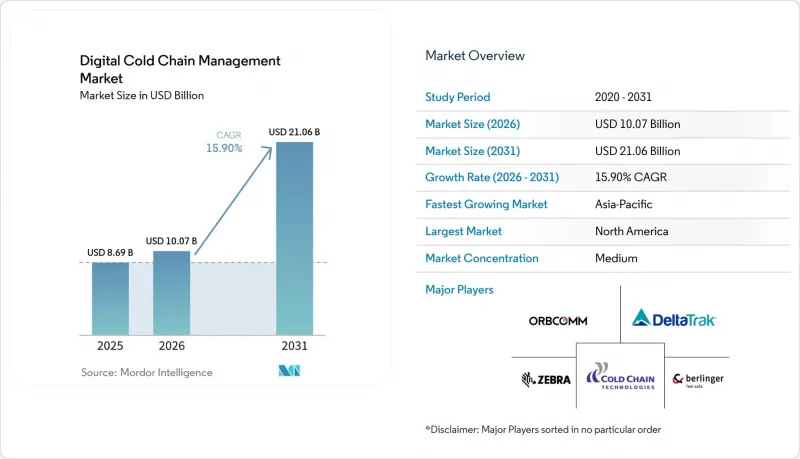

Mordor Intelligence에 의하면, 디지털 콜드체인 관리 시장 규모는 2025년 86억 9,000만 달러에서 2026년에는 100억 7,000만 달러로 확대되어 2031년까지 210억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 15.90%로 성장할 전망입니다.

본 보고서는 구성 요소(하드웨어, 소프트웨어, 서비스), 온도 범위(냉장, 냉동, 기타), 물류 단계(시설 내, 운송 중, 기타), 최종 사용자(식품 및 음료, 의약품 및 헬스케어, 기타) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 디지털 콜드체인 관리 시장 동향 및 인사이트

규정 준수를 중심으로 한 추적성의 디지털화

규제 일정에 따라, 추적성은 모범 사례에서 법적 요건으로 전환되었습니다. 미국의 ‘의약품 공급망 보안법’은 2025년부터 전자 데이터 단계를 시행하며, 일련번호가 부여된 기록이 누락될 경우 최대 50만 달러의 벌금을 부과하게 되었습니다. 이러한 움직임에 따라 기업들은 클라우드 연동형 온도 센서의 도입을 가속화했습니다. 이와 동시에, 2026년 1월부터 ‘사유에 따른’ 검사가 시행될 FDA의 식품안전 현대화법에서는 대상 식품에 대해 24시간 이내에 주요 데이터를 제공해야 할 의무가 부과되어 있어, 실시간 데이터 수집이 법적으로 필수적입니다. 유럽연합(EU) 역시 이와 같은 시급성을 느끼고 있으며, 일반 식품법 및 개정된 폐기물 기본지침에서 검증을 위한 디지털 기록 관리가 권장되고 있습니다. 이러한 규제들의 시너지 효과로 인해 규정 준수 리스크가 높아지면서, 디지털 콜드체인 관리 시장에 대한 투자가 촉진되고 있습니다.

생물학적 제제, 백신, 세포 및 유전자 치료의 모니터링 분야에서의 성장

첨단 치료법의 등장으로 초저온 및 정밀 온도 관리가 필요한 물류의 범위가 확대되고 있습니다. 2025년에는 4,000건 이상의 세포 및 유전자 치료 후보가 임상 개발 단계에 있을 것으로 예상되며, 자가 CAR-T 치료의 경우 운송 중 135°C 이하의 온도 관리가 필요합니다. 1회 투여량이 50만 달러를 초과하는 경우도 있으므로, 후원사는 ‘체인 오브 아이덴티티(제품 식별 관리)’ 및 ‘체인 오브 카스투디(보관 이력 관리)’에 대한 문서화를 요구하고 있으며, 이는 기존의 데이터 로거로는 해결할 수 없는 과제입니다. 이러한 엄격한 요건은 2-8℃ 범위에서 운송되는 mRNA 백신과 단일클론 항체에도 적용됩니다. 그 결과, 제약 기업의 운송업체들은 24시간 365일 가동되는 관제 센터로 데이터를 전송하는 멀티 센서 장치로 전환하고 있습니다. 제품의 높은 가격, 엄격한 안정성 요건, 그리고 전 세계적인 임상시험 확대가 맞물려 디지털 콜드체인 관리 시장의 성장세를 뒷받침하고 있습니다.

높은 통합 및 검증 비용

엔터프라이즈급 시스템을 도입하려면 하드웨어만으로도 물류 센터 1곳당 5만 달러 이상의 설비 투자가 필요하며, 여기에 21 CFR Part 11이나 EU GMP Annex 11 등에 따른 소프트웨어 검증에 드는 추가 비용도 발생합니다. 중소규모 유통업체들은 부분적인 규정 위반에 따른 제재를 피하기 위해 전면적인 도입을 미루는 경우가 많으며, 이러한 경향은 IT 예산이 세계 수준에 미치지 못하는 신흥 시장에서 특히 두드러집니다. 2025년 유럽사법재판소의 판결에서 온도 기록 미비로 인해 포워더에게 104만 2,000달러의 벌금이 부과된 사례에서 알 수 있듯이, 법적 위험은 매우 큽니다. 이러한 위험이 있음에도 불구하고, 검증 과정의 복잡성이 계속해서 도입을 가로막고 있습니다. 따라서 초기 비용이, 본래라면 높은 성장 잠재력을 지닌 디지털 콜드체인 관리 시장의 성장을 저해하는 요인이 되고 있습니다.

부문별 분석

2025년, 사업자들이 창고, 차량, 라스트 마일 자산에 센서, RFID 태그, GPS 추적기를 도입한 결과, 하드웨어는 디지털 콜드체인 관리 시장 점유율의 54.13%를 차지했습니다. 센서의 평균 가격이 연평균 7% 하락함에 따라, 비용에 민감한 식품 운송업체들 사이에서도 센서의 광범위한 도입이 촉진되었습니다. 19×19×3.5mm 크기의 초소형 무선 센서는 15년의 배터리 수명을 갖추고 있어 총 소유 비용을 절감했습니다. 하드웨어의 규모에도 불구하고, 수익 성장세는 소프트웨어 쪽으로 이동하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 16.6%로 확대되고 있습니다. 구독형 플랫폼은 원시 데이터를 온도 이탈 예측으로 변환하여 GDP(적정 보관 증명) 및 FSMA(식품 안전 현대화법) 인증서를 자동으로 생성하는 동시에, 연료비를 최대 8% 절감하는 경로 최적화 모듈을 통합하고 있습니다. 구매자들이 보다 상세한 분석을 요구하는 가운데, 소프트웨어 공급업체들은 고객 유지율을 높이기 위해 검증 서비스, 사이버 보안 감사 및 탄소 배출량 대시보드를 패키지로 제공합니다.

2025년에는 냉동 부문이 디지털 콜드체인 관리 시장의 61.55%를 차지하며 시장을 주도했습니다. 이는 냉동 단백질, 아이스크림, 즉석식품 분야의 출하량 증가에 힘입은 결과입니다. 해운 업계는 신선 화물의 총 톤수의 절반 이상을 취급하며, ‘Move-to-15°C’와 같은 이니셔티브를 통해 새로운 설정 온도를 철저히 모니터링함으로써 5%의 에너지 절감을 목표로 하고 있습니다. 냉장 부문은 2℃에서 8℃ 사이의 보관이 필요한 바이오의약품과, 신선식품을 1시간 이내에 배송하는 래피드 커머스(Rapid Commerce) 방식의 식료품점이 주도하면서 연평균 성장률(CAGR) 16.15%로 성장할 것으로 전망됩니다. 냉장 화물은 열용량이 낮기 때문에 위험이 높고, 허용 오차가 작아집니다. 그 결과, 제약 회사의 화주들은 실시간 클라우드 연결 기능을 갖춘 이중화된 멀티프로브 장치를 점점 더 많이 활용하게 되었으며, 이는 수요를 견인하고 있습니다.

지역별 분석

2025년, 북미는 디지털 콜드체인 관리 시장에서 38.40%라는 압도적인 점유율을 차지했습니다. DSCSA 및 FSMA와 같은 엄격한 규제로 인해 제조업체부터 판매업체에 이르기까지 일련번호 부여 및 온도 검증 기록이 의무화되었으며, 이는 의약품 및 고위험 식품 분야에서 센서의 급속한 도입을 촉진하고 있습니다. 주요 냉장 창고 운영업체들은 도크에 있는 팔레트가 정해진 사양 범위 내에 있음을 보장하기 위해 AI를 활용한 야드 관리 시스템에 대한 투자를 확대되고 있습니다. 2위를 차지한 유럽에서는 추적 가능성과 지속가능성이 통합되어 있습니다. 2025년 현지 GDP(적정 유통 기준) 검사의 재개에 더해, 각국의 식품 폐기물 관련 법률에 따라 유통업체들은 국경을 초월한 규정 준수를 효율화할 수 있는 통합 모니터링 플랫폼의 도입을 요구받고 있습니다. 2025년 1월, 영국은 EU 기준에 부합하기 위해 윈저 프레임워크에 기반한 GDP 지침을 갱신함으로써, 범유럽 물류 사업자들의 사업 연속성을 확보했습니다.

아시아태평양은 대규모 인프라 프로젝트와 지원 정책에 힘입어 2026년부터 2031년까지 연평균 성장률(CAGR) 17.25%라는 견실한 성장세를 보일 것으로 전망됩니다. 2025년까지 중국의 냉장 창고 용량은 2억 7,700만 m³를 넘어설 전망이며, 냉장 트럭 보유 대수는 전년 대비 19% 증가한 58만 7,900대에 달할 것으로 예상되어, 차량용 텔레매틱스에 대한 수요가 증가하고 있음을 반영하고 있습니다. 인도에서는 ‘프라단 만트리 키산 삼파다 요자나(Pradhan Mantri Kisan SAMPADA Yojana)’를 통한 정부 자금 지원으로 농촌 지역의 냉장 시설이 현대화되고 있습니다. 동남아시아의 전자상거래 식품 소매업체들은 상품의 신선도를 보장하기 위해 라스트 마일 센서 네트워크에 투자하고 있습니다. 라틴아메리카의 수출업체, 특히 아보카도, 베리류, 수산물 수출업체들은 미국 FSMA(식품안전현대화법)의 요건, 특히 수출 경로에 관한 요건을 준수하기 위한 대책을 점점 더 많이 도입하고 있습니다. 중동에서는 항만 자유무역지구 인근에 위치한 IoT 기반 냉동 컨테이너 보관 시설이 아프리카로 수출되는 신선식품을 보호하고 있으며, 이는 디지털 콜드체인 관리 시장의 기회가 전 세계적으로 확대되고 있음을 여실히 보여주고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the digital cold chain management market size is expected to increase from USD 8.69 billion in 2025 to USD 10.07 billion in 2026 and reach USD 21.06 billion by 2031, growing at a CAGR of 15.90% over 2026-2031.

This report is Segmented by Component (Hardware, Software, Services), Temperature Range (Chilled, Frozen, and More), Logistics Stage (In-Facility, In-Transit, and More), End User (Food and Beverage, Pharmaceuticals and Healthcare, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Cold Chain Management Market Trends and Insights

Compliance-Led Traceability Digitization

Regulatory timelines have shifted traceability from a best practice to a statutory requirement. The United States Drug Supply Chain Security Act enforced its electronic-data phase in 2025, penalizing up to USD 500,000 for missing serialized records. This move spurred enterprises to adopt cloud-connected temperature sensors. Concurrently, the FDA's Food Safety Modernization Act, under "for-cause" inspections since January 2026, mandates that covered foods provide key data within 24 hours, making real-time data acquisition legally essential. The European Union mirrors this urgency, with the General Food Law and the revised Waste Framework Directive endorsing digital record-keeping for verification. These collective mandates amplify compliance risks, bolstering investments in the digital cold chain management market.

Growth in Biologics, Vaccines, and Cell & Gene Therapy Monitoring

Advanced therapeutics are broadening the scope for ultralow and precision-temperature logistics. In 2025, over 4,000 cell and gene therapy candidates were in clinical development, with autologous CAR-T treatments needing temperatures below 135 °C during transit. Given that single doses can surpass USD 500,000, sponsors demand chain-of-identity and chain-of-custody documentation, a feat beyond legacy data loggers. This rigor extends to mRNA vaccines and monoclonal antibodies, which are transported in the 2-8 °C range. Consequently, pharmaceutical shippers are gravitating towards multi-sensor devices that relay data to 24/7 command centers. The combination of high product value, strict stability requirements, and a global trial presence fuels the momentum of the digital cold chain management market.

High Integration and Validation Costs

Enterprise-grade deployments require capital investments exceeding USD 50,000 per distribution center for hardware alone, with additional costs for software validation, such as 21 CFR Part 11 or EU GMP Annex 11. Small and mid-sized distributors often delay full rollouts to avoid penalties for partial compliance, a trend particularly evident in emerging markets where IT budgets fall short of global standards. Legal risks are significant, as demonstrated by a 2025 European court ruling that fined a freight forwarder USD 1.042 million for inadequate temperature records. Despite these risks, the complexity of validation continues to deter adoption. Up-front costs, therefore, moderate the otherwise strong growth potential of the digital cold chain management market.

Other drivers and restraints analyzed in the detailed report include:

- Food Waste and Spoilage Reduction Mandates

- Cloud Analytics and Exception Automation

- Legacy-System Interoperability Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, hardware accounted for 54.13% of the digital cold chain management market share as operators equipped warehouses, vehicles, and last-mile assets with sensors, RFID tags, and GPS trackers. A 7% annual decline in average sensor prices encouraged widespread adoption, even among cost-sensitive food shippers. Ultra-compact wireless sensors, measuring 19 X 19 X 3.5 mm with 15-year battery lives, reduced total ownership costs. Despite hardware's scale, revenue growth is shifting toward software, expanding at a 16.6% CAGR from 2026 to 2031. Subscription platforms transform raw data into excursion forecasts, auto-generate GDP or FSMA certificates, and integrate route optimization modules that cut fuel costs by up to 8%. As buyers demand deeper analytics, software providers bundle validation services, cybersecurity audits, and carbon-emission dashboards to enhance client retention.

In 2025, the Frozen segment dominated the digital cold chain management market with a 61.55% share, driven by global shipments of frozen proteins, ice cream, and ready meals. Sea freight handled over half of perishable cargo tonnage, and initiatives like Move-to-15 °C aim to save 5% energy by monitoring and enforcing new set-points. The Chilled segment is projected to grow at a 16.15% CAGR, driven by biologics requiring 2 °C to 8 °C storage and rapid-commerce grocers offering one-hour delivery of fresh produce. Chilled loads are riskier due to lower thermal mass, leaving less margin for error. Consequently, pharmaceutical shippers increasingly use redundant multi-probe devices with real-time cloud connectivity, driving demand.

Geography Analysis

In 2025, North America commanded a dominant 38.40% share of the digital cold chain management market. Strict regulations, such as DSCSA and FSMA, require serialized and temperature-verified records from manufacturers to dispensers, driving rapid sensor adoption in pharmaceuticals and high-risk food sectors. Leading cold-storage operators are investing in AI-driven yard management systems to ensure pallets on docks remain within required specifications. Europe, holding the second position, integrates traceability with sustainability. The resumption of on-site GDP inspections in 2025, coupled with national food waste laws, is pushing distributors toward unified monitoring platforms that streamline cross-border compliance. In January 2025, the United Kingdom updated its GDP guidance under the Windsor Framework to align with EU standards, ensuring continuity for pan-European logistics providers.

Asia-Pacific is set to surge at a robust 17.25% CAGR from 2026 to 2031, driven by large-scale infrastructure projects and supportive policies. By 2025, China's cold storage capacity exceeded 277 million m3, and its refrigerated truck fleet grew 19% year-on-year to 587,900 units, reflecting rising demand for in-vehicle telematics. In India, government funding through the Pradhan Mantri Kisan SAMPADA Yojana is modernizing rural cold storage facilities. Southeast Asian e-commerce grocers are investing in last-mile sensor networks to ensure product freshness. Latin American exporters, particularly in avocados, berries, and seafood, are increasingly adopting measures to comply with U.S. FSMA requirements, especially for export lanes. In the Middle East, IoT-enabled reefer parks near port free zones are safeguarding perishables destined for Africa, highlighting the global scope of opportunities in the digital cold chain management market.

- ORBCOMM

- Berlinger & Co. AG

- Cold Chain Technologies

- Controlant

- Cryoport Systems

- DeltaTrak

- Dickson

- ELPRO

- Freshliance

- Haier Biomedical

- Infratab

- LogTag Recorders

- Monnit

- Roambee / Decklar

- Sensitech

- TagBox Solutions

- TempSen Electronics

- Testo

- Tive

- Zebra Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Compliance-Led Traceability Digitization

- 4.2.2 Growth in Biologics, Vaccines, and CGT Monitoring

- 4.2.3 Food Waste and Spoilage Reduction Mandates

- 4.2.4 Cloud Analytics and Exception Automation

- 4.2.5 Insurer Demand for Defensible Excursion Records

- 4.2.6 Detached-Asset Visibility Across Handoffs and Yard Dwell

- 4.3 Market Restraints

- 4.3.1 High Integration and Validation Costs

- 4.3.2 Legacy-System Interoperability Gaps

- 4.3.3 Airline Tracker Approval and In-Flight Data Blind Spots

- 4.3.4 Reusable-Device Return Friction

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Temperature Range

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.2.3 Ultra-low and Cryogenic

- 5.2.4 Controlled Ambient

- 5.3 By Logistics Stage

- 5.3.1 In-facility Monitoring

- 5.3.2 In-transit Monitoring

- 5.3.3 Last-mile Monitoring

- 5.3.4 Returnable Asset and Packaging Monitoring

- 5.4 By End User

- 5.4.1 Food and Beverage

- 5.4.2 Pharmaceuticals and Healthcare

- 5.4.3 Chemicals and Specialty Materials

- 5.4.4 Third-party Logistics and Cold Storage Operators

- 5.4.5 Retail, E-grocery, and Quick Commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ORBCOMM

- 6.3.2 Berlinger & Co. AG

- 6.3.3 Cold Chain Technologies

- 6.3.4 Controlant

- 6.3.5 Cryoport Systems

- 6.3.6 DeltaTrak

- 6.3.7 Dickson

- 6.3.8 ELPRO

- 6.3.9 Freshliance

- 6.3.10 Haier Biomedical

- 6.3.11 Infratab

- 6.3.12 LogTag Recorders

- 6.3.13 Monnit

- 6.3.14 Roambee / Decklar

- 6.3.15 Sensitech

- 6.3.16 TagBox Solutions

- 6.3.17 TempSen Electronics

- 6.3.18 Testo SE & Co. KGaA

- 6.3.19 Tive

- 6.3.20 Zebra Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space and unmet-need assessment