|

시장보고서

상품코드

2063881

인도의 라스트 마일 배송 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)India Last Mile Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

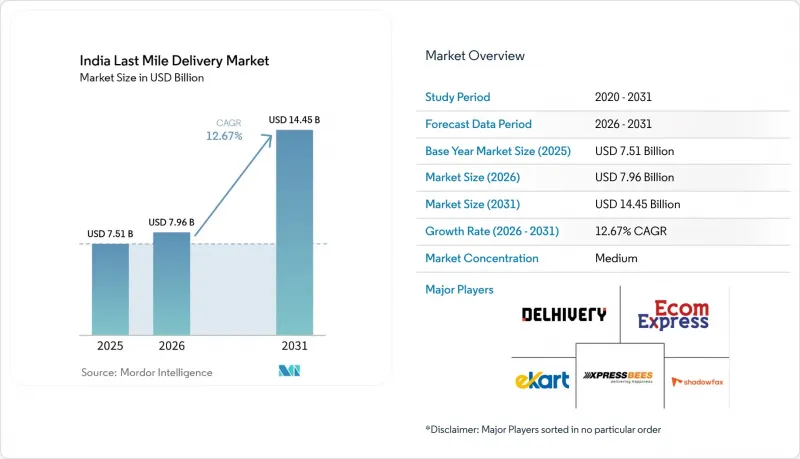

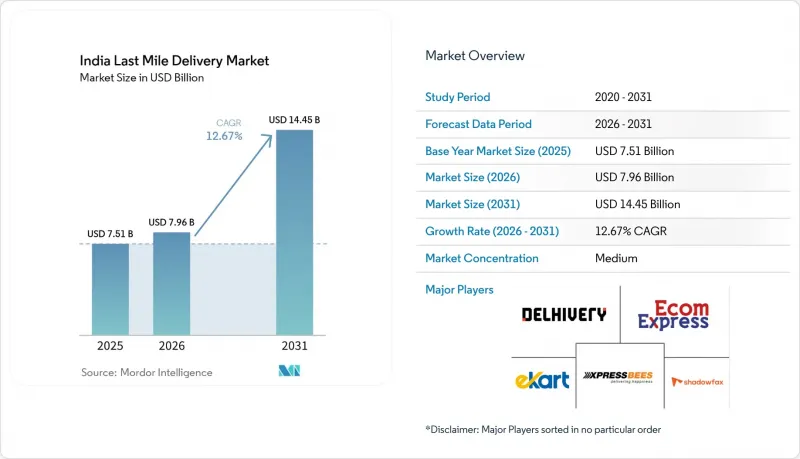

Mordor Intelligence에 의하면, 인도 라스트 마일 배송 시장 규모는 2025년 75억 1,000만 달러, 2026년 79억 6,000만 달러에서 2031년까지 144억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 12.67%를 나타낼 것으로 예측됩니다.

본 보고서는 서비스별(당일 배송, 특급 배송, 일반 배송), 비즈니스 모델별(B2B, B2C, C2C), 최종 사용자 산업별(전자상거래 소매, 패션·라이프스타일, 미용·웰니스·퍼스널케어, 홈·가구, 가전·가전제품 등), 지역별(북부, 중부, 서부, 동부, 남부)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도 라스트 마일 배송 시장 동향과 인사이트

2·3급 도시에서 전자상거래 GMV의 폭발적인 증가

지방 도시(Tier-2 및 Tier-3)의 GMV는 2025년에 42% 증가하여 대도시권의 성장률을 크게 상회했습니다. 이는 지방 지역의 스마트폰 보급률이 61%를 넘어섰고, 현지 언어를 지원하는 앱이 첫 구매자들의 진입 장벽을 낮춘 데 기인합니다. Flipkart의 Ekart는 우편번호 서비스 범위를 19,000개에서 23,500개로 확대하는 한편, 자이푸르, 라크나우, 비샤카파트남 전역에서 2일 배송 서비스 범위를 축소했습니다. 동시에, ElasticRun의 킬라나 네트워크 모델 덕분에 우타르프라데시 주와 비하르 주에서 라스트 마일 비용이 30% 절감되었습니다. 현재 소포의 집적도가 높아짐에 따라 허브 앤 스포크 방식에 대한 의존도를 줄이고, 트럭을 이용한 직행 노선을 도입할 수 있게 되었습니다. 다만, 여전히 40%의 주소에는 표준화된 건물 번호가 없어, 정차할 때마다 8-12분의 지연이 발생하고 있습니다. 따라서 인도의 라스트 마일 배송 시장은 첫 배송 성공률을 높이기 위해 지능형 엔진 도입으로 초점을 옮기고 있습니다. 지방의 지오코딩 문제를 해결한 운송업체는 수요가 가장 빠르게 증가하고 있는 지역에서 고객의 충성도를 확보할 수 있을 것입니다.

퀵 커머스와 다크 스토어의 급속한 확대

Blinkit, Zepto, Swiggy Instamart가 10-15분 이내 배송을 약속하기 위해 경쟁한 결과, 다크 스토어의 수는 2026년 3월까지 1,489개 점포에 달했으며, 15개월 동안 67% 증가했습니다. 2025년 Zepto에 대한 10억 달러 규모의 자금 조달과 Blinkit의 Zomato 통합은 주문 빈도가 높다는 점이 소규모 장바구니 규모를 상쇄한다는 투자자들의 확신을 뒷받침하고 있습니다. 안델리와 콜라망가라에서 나타난 35%의 부동산 프리미엄은 초지역 거점의 전략적 가치를 여실히 보여주고 있습니다. 가전제품으로의 카테고리 확장에 따라 평균 주문 금액은 485루피(5.13달러)로 상승했으며, 일부 마이크로마켓에서는 기여 이익률이 플러스로 전환되었습니다. 신선식품의 온도 기록과 관련된 FSSAI(식품표준안전청)의 초안은 규정 준수 측면에서 장애물이 될 가능성이 높으며, 콜드체인 대응 체계가 잘 갖춰진 플랫폼에 유리하게 작용할 것입니다.

대도시권 내 퀵커머스의 포화와 가격 경쟁

2026년 3월 기준, 뭄바이, 델리 수도권(NCR), 벵갈루루의 온라인 식료품 구매자 보급률은 38%를 넘어 한국과 유사한 성숙 단계에 근접한 수준에 도달했으며, 고객 확보 비용은 전년 대비 62% 상승했습니다. 2025-26 회계연도의 총 현금 소모액은 320억 루피(33억 8,600만 달러)에 달했으며, 매출총이익률은 전년도의 18%에서 11%로 하락했습니다. 소비자들이 할인 상품만을 엄선해 구매하는 경향이 강해지면서, 평균 주문 금액은 440루피(4.66달러)까지 하락해 카테고리 확장 전략을 저해했습니다. 경쟁위원회는 부당한 가격 책정 의혹에 대해 조사를 시작했으며, 이로 인해 불확실성이 커지고 있습니다. 각 플랫폼은 인구 밀도가 낮고 배송 시간을 20-30분으로 단축할 수 있는 1급 도시로 사업을 전환하고 있지만, 그 수익성은 여전히 불투명합니다.

부문별 분석

2025년, 인도의 라스트 마일 배송 시장 점유율에서 일반 배송이 58.19%를 차지하며 1위를 기록했으나, 2031년까지 가장 높은 연평균 성장률(CAGR) 14.32%를 나타낼 것으로 예측되는 것은 당일 배송입니다. 2025년 표준 배송의 경쟁력은 3-5일의 배송 기간을 수용할 수 있는 비신선 식품 카테고리에 적합하다는 점에 기반을 두고 있습니다. 익스프레스 배송은 익일 배송이 중요한 상품의 경우, 높은 수수료로 인해 당일 배송 이용이 어려워지는 패션 상품 주문 시 발생하는 격차를 해소하고 있습니다. 각 운송사는 하루 120만 개의 소포를 처리하는 Delhivery의 방갈로르 게이트웨이와 같은 AI 분류 라인에 설비 투자를 하고 있습니다. 이러한 변화로 인해, 비용 효율이 높은 표준 부문이 배제되지 않는 가운데, 인도의 라스트마일 배송 시장은 점차 고속 서비스 부문으로 전환될 것입니다.

현재 네트워크의 차별화는 다크 스토어의 밀도와 데이터 기반의 배송 슬롯 배정에 달려 있습니다. 아마존의 '프라임 나우(Prime Now)'는 2025년에 4,200만 건의 배송을 처리했으며, 품절 사태를 피하기 위해 인도 소비자들이 기꺼이 지불하는 35%의 가격 프리미엄을 유지했습니다. 2025년 연휴 시즌 동안 블루 다트(Blue Dart)의 2급 도시에서 특급 배송이 급증한 것은 지방 지역에서 예측 가능한 익일 배송 서비스에 대한 수요가 높다는 점을 여실히 보여주고 있습니다. AI를 활용한 동적 경로 설정이 보급됨에 따라, 비용과 속도의 균형을 적절히 맞출 수 있는 운송업체들이 인도의 라스트마일 배송 시장에서 점유율을 확대해 나갈 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 2026-2031년)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the india last mile delivery market size is projected to expand from USD 7.51 billion in 2025 and USD 7.96 billion in 2026 to USD 14.45 billion by 2031, registering a CAGR of 12.67% between 2026 to 2031.

This report is Segmented by Service (Same-Day Delivery, Express Delivery, Standard Delivery), by Business Model (B2B, B2C, C2C), by End User Industry (E-Commerce Retail, Fashion and Lifestyle, Beauty, Wellness and Personal Care, Home and Furniture, Consumer Electronics and Appliances, and More), and by Region (North, Central, West, East, South). Market Forecasts are Provided in Terms of Value (USD).

India Last Mile Delivery Market Trends and Insights

Explosive E-Commerce GMV Surge in Tier-2/3 Cities

Tier-2 and Tier-3 GMV expanded by 42% in 2025, far outstripping metro growth, as smartphone penetration crossed 61% in rural areas and vernacular apps lowered entry barriers for first-time buyers. Flipkart's Ekart expanded its pin-code coverage from 19,000 to 23,500, compressing the two-day delivery coverage across Jaipur, Lucknow, and Visakhapatnam. At the same time, ElasticRun's kirana network model has reduced last-mile costs by 30% in Uttar Pradesh and Bihar. Parcel density now justifies direct truck routes, reducing reliance on hubs and spokes, though 40% of addresses still lack standardized building numbers, adding 8-12 minutes per stop. The Indian last-mile delivery market is therefore pivoting to adopt intelligent engines to improve first-attempt success rates. Carriers that crack rural geocoding will secure loyalty in the fastest-growing demand pockets.

Rapid Expansion of Quick-Commerce and Dark Stores

Dark-store count hit 1,489 by March 2026, up 67% in fifteen months as Blinkit, Zepto, and Swiggy Instamart raced to maintain 10-15-minute delivery promises. Funding inflows Zepto's USD 1 billion in 2025 and Blinkit's integration within Zomato underscore investor confidence that high order frequency offsets smaller baskets. Real estate premiums of 35% in Andheri and Koramangala highlight the strategic value of hyperlocal nodes. Category expansion into electronics lifted average order values to INR 485 (USD 5.13), pushing contribution margins positive in select micro-markets. Draft FSSAI norms on temperature logs for perishables are likely to create compliance hurdles, favoring platforms with cold-chain readiness.

Metro Quick-Commerce Saturation and Discount Wars

Penetration among online grocery shoppers crossed 38% in Mumbai, Delhi-NCR, and Bengaluru by March 2026, near maturity levels seen in South Korea, driving customer-acquisition costs up 62% year on year. The collective cash burn of INR 3,200 (USD 33.86) crore in FY 2025-26 slashed gross margins to 11%, down from 18% a year earlier. Average order values fell to INR 440 (USD 4.66) as consumers cherry-picked discount SKUs, undermining category-expansion strategies. The Competition Commission has opened a probe into alleged predatory pricing, stoking uncertainty. Platforms are pivoting toward Tier-1 cities where density is lower and delivery promises can stretch to 20-30 minutes, but the economics remain unproven.

Other drivers and restraints analyzed in the detailed report include:

- National Logistics Policy and Corridor Build-Out

- AI-Driven Routing and Fulfillment Optimization

- High RTO Rates from Tier-2/3 Address Quality Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard delivery led with 58.19% of the Indian last-mile delivery market share in 2025, while same-day delivery is projected to post the highest 14.32% CAGR through 2031. Standard delivery's 2025 lead rests on its suitability for non-perishable categories that tolerate 3-5-day windows. Express delivery bridges the gap for fashion orders where next-day delivery matters but premium fees deter same-day uptake. Carriers are channeling capex into AI sortation lines, such as Delhivery's Bengaluru gateway, which handles 1.2 million parcels daily. These shifts will gradually shift the India last-mile delivery market toward faster tiers without erasing the cost-efficient standard segment.

Network differentiation now hinges on dark-store density and data-driven slot-allocation. Amazon's Prime Now processed 42 million shipments in 2025, sustaining a 35% price premium that Indian consumers are willing to pay to avoid stockouts. Blue Dart's Tier-2 express surge during the 2025 festive season underscores the hinterland's appetite for a predictable next-day service. As AI-enabled dynamic routing proliferates, carriers that balance cost and speed will capture incremental market share in India's last-mile delivery market.

List of Companies Covered in this Report:

- Delhivery

- Ecom Express

- Xpressbees

- Shadowfax

- Ekart Logistics

- Loadshare Networks

- ElasticRun

- Dunzo

- Borzo

- Porter

- Blue Dart Express

- DTDC Express

- Allcargo Gati

- Safexpress

- Mahindra Logistics

- TCI Express

- FedEx India

- DHL eCommerce

- Aramex India

- Amazon Transportation Services

- Reliance Retail Logistics

- India Post

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive E-Commerce GMV Surge in Tier-2/3 Cities

- 4.2.2 Rapid Expansion of Quick-Commerce and Dark Stores

- 4.2.3 National Logistics Policy and Corridor Build-Out

- 4.2.4 AI-Driven Routing and Fulfilment Optimization

- 4.2.5 Electric 2-Wheeler-as-a-Service Unlocking Gig Capacity

- 4.2.6 ULIP Open-API Data Platform Streamlining Compliance

- 4.3 Market Restraints

- 4.3.1 Metro Quick-Commerce Saturation and Discount Wars

- 4.3.2 High RTO Rates from Tier-2/3 Address Quality Gaps

- 4.3.3 Urban Congestion & Parking Shortages Inflating Costs

- 4.3.4 Sparse EV-Charging/Financing Slowing Green Fleets

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Insights on Warehousing & Distribution Centers

- 4.9 Insights on Refrigerated Last-Mile Delivery

- 4.10 Reverse / Return Logistics Insights

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service

- 5.1.1 Same-day Delivery

- 5.1.2 Express Delivery

- 5.1.3 Standard Delivery

- 5.2 By Business Model

- 5.2.1 Business-to-Business (B2B)

- 5.2.2 Business-to-Consumer (B2C)

- 5.2.3 Customer-to-Consumer (C2C)

- 5.3 By End User Industry

- 5.3.1 E-commerce Retail

- 5.3.2 Fashion and Lifestyle

- 5.3.3 Beauty, Wellness and Personal Care

- 5.3.4 Home and Furniture

- 5.3.5 Consumer Electronics and Appliances

- 5.3.6 Healthcare and Medical Supplies

- 5.3.7 Others

- 5.4 By Region

- 5.4.1 North

- 5.4.2 Central

- 5.4.3 West

- 5.4.4 East

- 5.4.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Delhivery

- 6.4.2 Ecom Express

- 6.4.3 Xpressbees

- 6.4.4 Shadowfax

- 6.4.5 Ekart Logistics

- 6.4.6 Loadshare Networks

- 6.4.7 ElasticRun

- 6.4.8 Dunzo

- 6.4.9 Borzo

- 6.4.10 Porter

- 6.4.11 Blue Dart Express

- 6.4.12 DTDC Express

- 6.4.13 Allcargo Gati

- 6.4.14 Safexpress

- 6.4.15 Mahindra Logistics

- 6.4.16 TCI Express

- 6.4.17 FedEx India

- 6.4.18 DHL eCommerce

- 6.4.19 Aramex India

- 6.4.20 Amazon Transportation Services

- 6.4.21 Reliance Retail Logistics

- 6.4.22 India Post

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment