|

시장보고서

상품코드

2063914

아이스크림 냉동고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Ice-Cream Freezers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

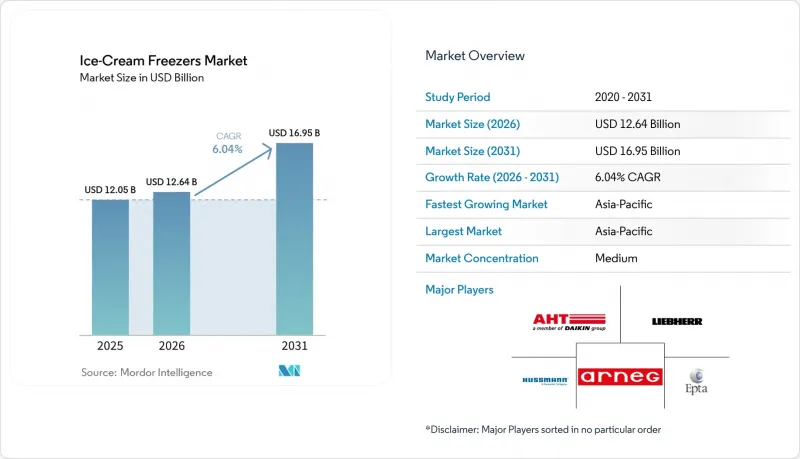

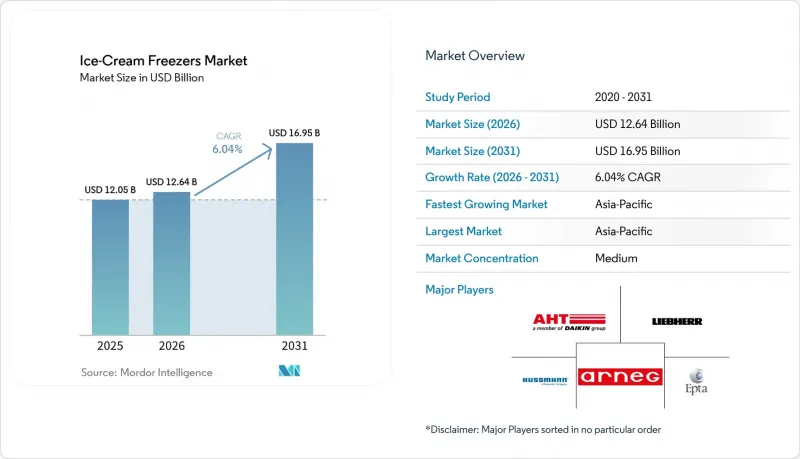

Mordor Intelligence에 의하면, 아이스크림 냉동고 시장 규모는 2025년 120억 5,000만 달러로 평가되었고, 2026년에는 126억 4,000만 달러로 추정되고, 2031년까지 169억 5,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 6.04%로 성장할 전망입니다.

본 보고서는 제품 유형별(서랍형, 직립형, 디핑형, 카운터탑형, 아일랜드/멀티덱형), 냉각 기술별(정지식, 통기식, 하이브리드식, 글리콜/워터 루프식), 용량별(300L 이하, 301-600L, 600L 초과), 최종 사용자별(슈퍼마켓, 편의점, 아이스크림 가게, 호레카(Horeca), 바), 유통 채널별(유통업체 및 OEM 직접 판매), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준입니다.

세계릐 아이스크림 냉동고 시장 동향 및 인사이트

HFC의 단계적 감축과 효율성 규제가 구조적인 교체 수요를 창출하고 있습니다.

유럽연합(EU)의 불소계 가스 규제(EU) 2024/573에 따라 2025년 1월 1일부터 GWP가 150 이상인 불소계 가스의 신규 독립형 상업용 냉동 기기 사용이 금지됨에 따라, 아이스크림 냉동고 시장은 구조적인 교체 단계에 접어들었습니다. 이는 기존 R134a 및 R404A를 사용하는 냉동고 군에 직접적인 영향을 미치고 있습니다. 미국에서는 AIM법에 따라, 같은 날부로 신규 독립형 상업용 냉동 장치에 대해 GWP가 150 이하인 냉매로의 전환이 의무화되었으며, 2024-2028년 HFC 할당 상한은 기준치의 60%로 하향 조정되었습니다. 2024년 유럽연합(EU)의 HFC 소비량은 이미 몬트리올 의정서의 목표치보다 60% 낮은 수준이며, 이는 기존 시스템 소유자들에게 사용 가능한 냉매공급이 얼마나 급속히 부족해지고 있는지를 보여줍니다. 이러한 변화는 아이스크림 냉동고 시장에 있어 중요한 의미를 지닙니다. 왜냐하면, 구형 장비를 계속 사용하고 있는 사업자는 신규 HFC 공급 계약으로 인해 유지보수 비용 부담이 커지기 때문입니다. 그 결과, 장비 교체 여부는 단순히 사용 연한 만료 시점이 아니라 총 소유 비용이나 규정 준수 위험을 바탕으로 결정되는 경우가 늘고 있습니다.

아시아태평양 지역의 소매점망 확대 및 현대화

아시아태평양은 현재 가장 큰 시장 규모와 가장 빠른 성장세를 동시에 보이고 있으며, 이로 인해 아이스크림 냉동고 시장은 성장세가 교체 수요에 의존하는 다른 지역보다 더욱 견고한 구조적 수요 기반을 갖추고 있습니다. 인도의 아이스크림 시장은 2023년에 3,000억 루피(35억 달러)로 평가되며, 조직형 소매업의 확대와 1인당 소비량 증가에 힘입어 해당 부문은 13%-15%의 성장률을 보일 것으로 전망됩니다. 이러한 소매망의 확대는 대형 하이퍼마켓에만 국한된 것이 아닙니다. 중국, 인도, 동남아시아에서는 인근 식료품점이나 편의점도 냉동식품 취급 능력을 확대하고 있기 때문입니다. 이러한 소규모 점포에서는 일반적으로 중앙 관리 시스템이 아닌 플러그인식 냉동고가 필요하기 때문에 아이스크림 냉동고 시장 수요는 300L 이하와 301-600L 용량대에 집중되어 있습니다. 실질적인 영향으로 볼 때, 온난한 기후의 도시 지역에서 점포 수가 증가함에 따라, 특히 냉동 디저트 매출이 여전히 충동 구매에 의존하고 있는 지역에서는 새로운 냉동 진열장에 대한 수요로 직결되고 있습니다.

HC/CO2 관련 기술자의 역량 부족과 안전 기준 준수

아이스크림 냉동고 시장은 R290 및 CO2 시스템으로의 전환이, 새로운 안전 및 취급 요건에 아직 적응하지 못한 기술자층에 의존하고 있기 때문에 전환 과정에서 병목 현상을 겪고 있습니다. 유럽연합(EU)의 플론 가스 규제(2024/573)는 회원국들에게 자연 냉매 기술자 인증 프로그램을 마련할 것을 의무화하고 있으며, 시행 규칙은 2025년에 걸쳐 순차적으로 마련되기 시작하고 있습니다. 인증 일정의 지연과 인력 부족으로 인한 격차로 인해, 구매자가 지출 준비를 마쳤더라도 설치나 장비 교체에 차질이 생길 수 있습니다. 특히 소규모 사업자들은 더욱 신중을 기하고 있습니다. 왜냐하면, 탄화수소 시스템의 부적절한 취급은 보험상의 문제를 야기하거나 건축기준법 위반으로 이어질 우려가 있기 때문입니다. 그 결과, 아이스크림 냉동고 시장에서는 수요가 견조한 추세를 보일 것으로 예상되지만, 실제 설치 속도는 인력 확보 상황이나 규정 준수 위험에 따라 제약을 받을 가능성이 있습니다.

부문별 분석

2025년 기준으로, 서랍형 및 대형 냉동고는 아이스크림 냉동고 시장 점유율의 34.23%를 차지했으며, 이는 아시아태평양, 아프리카, 남미 전역에서 브랜드 냉동고 프로그램에 깊이 정착되어 있음을 반영합니다. 다국적 아이스크림 브랜드가 독점적이거나 준독점적인 판매 계약에 따라 독립 소매업체에 계속해서 냉동고를 설치하고 있기 때문에 그 입지는 여전히 견고합니다. 이러한 설치 기반은 상품 진열의 노후화보다는 냉매 규제를 준수하기 위해 형성된 주기에 따라 갱신되고 있습니다. 아이스크림 냉동고 시장은 시각적인 진열보다는 저렴한 비용, 내구성, 간편한 유지보수가 중시되는 충동 구매가 많은 장소에서 여전히 상자형 냉동고에 의존하고 있습니다. 이에 따라 냉동 디저트의 회전율은 안정적이지만, 매장 면적이 제한된 도로변 소매점, 키오스크, 인근 점포에서는 여전히 냉동고형 유닛에 대한 수요가 높게 유지되고 있습니다.

조직형 소매업이 세로형 가시성과 상품 비교의 명확화로 전환됨에 따라, 세로형/유리문식 냉동고는 2031년까지 연평균 성장률(CAGR) 6.18%를 나타낼 것으로 예측되며, 이는 제품 유형 중 가장 높은 성장률입니다. 유럽연합(EU)의 에너지 규제가 이러한 추세를 뒷받침하고 있으며, 2023년 9월 1일 이후 아이스크림 냉동고는 에너지 효율 지수(EEI)가 50% 이하라는 기준을 충족해야 하기 때문에 규제 시장에서는 새로운 세로형 디자인이 선호되고 있습니다. 디핑 캐비닛과 스쿠핑 냉동고는 그동안 공식적인 진출이 거의 없었던 시장으로 젤라토와 프리미엄 디저트가 확대됨에 따라, 해당 수요를 늘리고 있습니다. 아일랜드형/멀티데크형 냉동고는 여전히 대형 슈퍼마켓의 매장 진열대에 자리 잡고 있으며, 매장 설비의 현대화에 따라 GWP(지구온난화지수)가 낮은 플랫폼으로의 교체가 진행되고 있습니다. 카운터탑형 아이스크림 냉동고는 여전히 가장 작은 하위 부문이지만, 카페, QSR(퀵서비스 레스토랑), 디저트 메뉴 확대의 혜택을 받고 있으며, 이로 인해 아이스크림 냉동고 산업은 일반 소매 시장을 넘어 전문적인 제품층을 확보하고 있습니다.

2025년 매출액 중 정적 냉각 시스템이 44.92%를 차지했으며, 이는 아이스크림 냉동고 시장이 여전히 브랜드 매장이나 소규모 소매점에서 사용되는 저비용 플러그인형 캐비닛에 얼마나 의존하고 있는지를 여실히 보여주고 있습니다. 이러한 꾸준한 인기는 단순함, 낮은 도입 비용, 충동 구매를 유도하는 유통 채널에서의 오랜 설치 실적에 기인합니다. 또한, 규제 대응에 따른 압박으로 인해 제조업체들이 기존 플랫폼을 포기하기보다는 최적화를 도모한 점도 정적 시스템이 여전히 유효한 이유 중 하나입니다. 실제로 많은 사업자들은 유지보수 및 설치가 용이한 개량형 정적 유닛을 선호합니다. 이러한 추세는 첨단 기술이 주목을 받는 상황에서도 아이스크림 냉동고 시장의 기반이 여전히 광범위한 이유를 설명하는 한 가지 요인이 되고 있습니다.

원격 글리콜/물 루프(SPI) 시스템은 냉매 규제를 준수하면서도 매장 레이아웃의 유연성을 모두 충족시키기 위해 2031년까지 연평균 6.88%의 성장률을 보일 전망이며, 이는 냉각 기술 분야 중 가장 빠른 성장 속도입니다. AHT Cooling Systems는 2025년에 태국에서 자사의 VENTO SPI 워터 루프 시스템을 도입했습니다. 이 회사는 R404A 랙 시스템과 비교해 연간 에너지 사용량을 12% 절감하고, 냉매 충전량을 97% 줄였습니다고 보고했습니다. 또한, 독일에서 하이브리드 R290 플러그인 워터 루프를 도입함으로써 슈퍼마켓의 총 에너지 사용량을 8.8% 절감했으며, 따뜻한 계절에는 냉난방 부하를 최대 40%까지 줄였습니다. EN IEC 60335-2-89:2022에 따른 충전량 제한 규정에 따라, 단일 대형 집중 충전 방식 대신 냉매를 보다 소규모의 밀폐 회로에 분산시키는 방식으로, 분산형 아키텍처의 도입이 더욱 가속화되고 있습니다. 아이스크림 냉동고 시장에서는 설치 기준으로는 여전히 고정식 유닛이 주류를 이루고 있지만, 워터 루프 시스템이 기술의 미래를 주도하고 있다고 할 수 있습니다.

지역별 분석

아시아태평양은 2025년에 아이스크림 냉동고 시장 점유율의 37.13%를 차지한 것으로 평가되었으며, 2031년까지 지역별 가장 높은 연평균 성장률(CAGR)인 7.23%를 나타낼 것으로 전망됩니다. 이러한 이례적인 조합은 일시적인 교체 수요의 급증이 아니라 구조적인 수요의 존재를 시사하고 있습니다. 이 지역은 냉동 디저트 소비 증가, 소매업의 급속한 정상화, 그리고 일년내내 눈에 잘 띄는 곳에 설치된 상업용 냉동고에 대한 수요를 뒷받침하는 기후 조건의 혜택을 누리고 있습니다. 인도는 조직형 소매업의 확대로 콜드체인의 보급이 진전되고 있으며, 1인당 소비량이 낮은 수준에서 지속적으로 증가하고 있어 강력한 장기 성장 요인으로 작용하고 있습니다. 또한, 이 지역은 기온이 높기 때문에 온대 지역의 많은 시장에 비해 매장 차원의 배열 문제가 더욱 시급한 과제로 대두되고 있으며, 워터 루프 시스템이나 세미 플러그인 시스템의 조기 상용화 사례가 기대됩니다.

유럽은 2031년까지 연평균 3.50%의 성장이 예상되며, 이는 아시아태평양보다 완만하지만 규제 준수를 배경으로 한 명확한 교체 주기에 의해 여전히 뒷받침되고 있습니다. 해당 지역의 설치 대수가 많고 시장이 성숙기에 접어들었기 때문에 장비 교체는 신규 매장 개설보다는 규제, 효율성, 기술 업그레이드에 크게 좌우됩니다. 유럽연합(EU)의 에코디자인 규정과 EPREL 규정에 따라 제품 비교의 투명성이 높아지고 있으며, EU 프레온 가스 규정(EU) 2024/573에 따라 구형 HFC 기기군에 대한 규제가 가속화되고 있습니다. 북미 시장은 AIM법과 프리미엄 아티산 계열 냉동 디저트에 대한 수요에 힘입어 2031년까지 연평균 4.50%의 성장률을 보일 것으로 전망됩니다. 두 지역 모두에서 아이스크림 냉동고 시장은 단순히 판매 대수 증가만을 목표로 하는 것이 아니라, 더 높은 성능을 갖추고 GWP(지구온난화지수)가 낮으며 데이터 가시성이 뛰어난 기기로 전환되고 있습니다.

남미는 2031년까지 연평균 5.00%의 성장률이 예상되는 반면, 서아시아는 5%-6% 범위에서 아프리카는 4% 정도 범위에서 더 낮은 수준에서 성장할 것으로 전망됩니다. 이 지역들은 발전의 초기 단계에 있기 때문에 단기적으로는 규제에 따른 개편보다 소매업의 현대화 및 콜드체인에 대한 투자가 더 중요합니다. 키갈리 체제는 개발도상국을 HFC 단계적 감축 과정에 임베디드시키고, 기존 냉매로부터의 단계적 전환을 지원하는 측면에서 여전히 중요합니다. 매장 네트워크와 푸드서비스 산업의 형태가 현대화됨에 따라, 해당 지역의 아이스크림 냉동고 시장은 단순히 대규모 장비 교체에 그치지 않고, 신규 설치와 선택적 업그레이드가 결합되어 확대될 것으로 전망됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the ice-cream freezers market size is expected to increase from USD 12.05 billion in 2025 to USD 12.64 billion in 2026 and reach USD 16.95 billion by 2031, growing at a CAGR of 6.04% over 2026-2031.

This report is Segmented by Product Type (Chest, Upright, Dipping, Countertop, and Island/Multideck), Cooling Technology (Static, Ventilated, Hybrid, and Glycol/Waterloop), Capacity (≤300L, 301-600L, and >600L), End User (Supermarkets, C-Stores, Ice-Cream Parlors, Horeca, and Bars), Sales Channel (Distributors and Direct OEM), and Geography. Market Forecasts in Value (USD).

Global Ice-Cream Freezers Market Trends and Insights

HFC Phase-Down and Efficiency Mandates Creating Structural Replacement Demand

The ice-cream freezer market is entering a structural replacement phase because the European Union F-Gas Regulation (EU) 2024/573 banned fluorinated gases with a GWP of 150 or more in new self-contained commercial refrigeration equipment from January 1, 2025, directly affecting legacy R134a and R404A freezer fleets. In the United States, the AIM Act requires new stand-alone commercial refrigeration units to shift to refrigerants with a GWP below 150 on the same date, while the HFC allowance cap for 2024-2028 fell to 60% of baseline . European Union HFC consumption in 2024 was already 60% below Montreal Protocol targets, which shows how quickly the available refrigerant pool has tightened for owners of legacy systems. That change matters for the ice-cream freezers market because operators who keep older equipment in service face higher servicing exposure due to virgin HFC supply contracts. The result is that replacement decisions are increasingly being justified by total ownership cost and compliance risk rather than by simple end-of-life timing.

Retail Footprint Expansion and Modernization in Asia-Pacific

Asia-Pacific combines the largest current base with the fastest growth path, giving the ice-cream freezers market a stronger structural demand base than in regions where growth depends on replacement. India's ice-cream business was valued at INR 30,000 crore (USD 3.5 billion) in 2023, and the category is expected to grow at 13%-15% as organized retail expands and per-capita consumption rises. That retail build-out is not limited to large-format hypermarkets, because neighborhood grocery and convenience formats are also widening frozen-food capacity across China, India, and Southeast Asia. Those smaller stores usually need plug-in cabinets rather than centralized systems, so demand tilts toward the ≤300L and 301-600L bands in the ice-cream freezers market. The practical effect is that store-count growth in warm-climate urban corridors converts directly into new cabinet demand, especially where impulse purchases still dominate frozen dessert sales.

Technician Skill Gaps and Safety Code Compliance for HC/CO2

The ice-cream freezers market faces a conversion bottleneck because the move to R290 and CO2 systems depends on a technician base that is still catching up with new safety and handling requirements. European Union F-Gas Regulation (EU) 2024/573 requires member states to establish certification programs for natural-refrigerant technicians, and implementing rules began to appear through 2025. The gap between certification timelines and workforce capacity can cause installation and fleet conversion to lag even when buyers are ready to spend. Smaller operators are particularly cautious because improper handling of hydrocarbon systems can raise insurance concerns and trigger building code violations. As a result, the ice-cream freezers market may see demand remain healthy while actual installation velocity is constrained by labor availability and compliance risk.

Other drivers and restraints analyzed in the detailed report include:

- Natural Refrigerant Adoption Enabling Higher-Efficiency Plug-in Units

- Growth of Supermarkets, Convenience Formats, and Premium Gelato Outlets

- High Upfront Costs Amid Energy Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chest/Deep Freezers held 34.23% of the ice-cream freezer market share in 2025, reflecting their deep entrenchment in branded freezer programs across Asia-Pacific, Africa, and South America. Their position remains strong because multinational ice-cream brands continue to place chest units with independent retailers under exclusive or semi-exclusive distribution arrangements. That installed base is replaced on a cycle shaped more by refrigerant compliance than by merchandising obsolescence. The ice-cream freezers market still relies on chest formats in impulse-heavy locations where low cost, durability, and simple maintenance matter more than visual presentation. This keeps chest units highly relevant in roadside retail, kiosks, and neighborhood outlets where frozen dessert turnover is steady, but floor area is limited.

Upright/Glass-Door Freezers are projected to grow at a 6.18% CAGR through 2031, the fastest rate among product types, as organized retail shifts toward vertical visibility and clearer product comparisons. European Union energy rules have reinforced that shift, as ice-cream freezers had to meet an EEI threshold of 50% or less from September 1, 2023, favoring newer vertical designs in regulated markets . Dipping Cabinets and Scooping Freezers are gaining more addressable demand as gelato and premium dessert formats expand into markets where they previously had little formal presence. Island/Multideck Freezers remain tied to larger supermarket floor displays and are being refreshed on lower-GWP platforms as store fleets modernize. Countertop Ice-Cream Freezers remain the smallest sub-segment, yet they benefit from cafe, QSR, and dessert menu expansion, which gives the ice-cream freezers industry a specialist product layer beyond mainstream retail.

Static cooling systems accounted for 44.92% of 2025 revenues, underscoring how much the ice-cream freezers market still relies on low-cost plug-in cabinets used in branded fleets and small-format retail. Their staying power is linked to simplicity, lower acquisition costs, and a long history of installation in impulse channels. Static systems have also remained viable because compliance pressure has pushed manufacturers to optimize familiar platforms rather than abandon them. In practice, many operators prefer an improved static unit that is easy to service and install. That dynamic helps explain why the base of the ice-cream freezers market remains broad even as advanced technologies gain attention.

Remote Glycol/Waterloop (SPI) systems are growing at 6.88% through 2031, the fastest pace among cooling technologies, because they address both refrigerant compliance and store-layout flexibility. AHT Cooling Systems deployed its VENTO SPI waterloop system in Thailand in 2025. They reported a 12% reduction in annual energy use against an R404A rack system, along with a 97% reduction in refrigerant charge. A hybrid R290 plug-in water-loop installation in Germany also cut total supermarket energy use by 8.8% and reduced air-conditioning load by up to 40% in warmer months. Charge-limit rules under EN IEC 60335-2-89:2022 have further strengthened the case for distributed architectures by spreading refrigerant across smaller sealed circuits rather than a single large, centralized charge. In the ice-cream freezers market, which means waterloop systems are shaping the future of technology, even as static units continue to dominate the installed base.

Geography Analysis

Asia-Pacific held 37.13% of the ice-cream freezer market share in 2025 and is also forecast to post the fastest regional CAGR of 7.23% through 2031. That rare combination points to structural demand rather than a short replacement spike. The region benefits from rising frozen dessert consumption, rapid retail formalization, and climate conditions that sustain year-round demand for visible commercial freezer placement. India adds a strong long-term layer because organized retail expansion is improving cold-chain reach while per-capita consumption continues to rise from a low base. The region also offers an early commercial case for waterloop and semi plug-in systems because high ambient temperatures make heat rejection a more immediate store-level issue than in many temperate markets.

Europe is projected to grow at 3.50% through 2031, which is slower than Asia-Pacific but still supported by a clear compliance-led replacement cycle. The region's installed base is large and mature, so equipment refresh depends more on regulations, efficiency, and technology upgrades than on the creation of new outlets. European Union Ecodesign and EPREL rules have made product comparison more transparent, and the European Union F-Gas Regulation (EU) 2024/573 has accelerated pressure on legacy HFC fleets. North America is forecast to grow at 4.50% through 2031, supported by the AIM Act and by demand for premium and artisan frozen dessert formats. In both regions, the ice-cream freezers market is moving toward better-specified, lower-GWP, and more data-visible equipment rather than simply toward higher unit volumes.

South America is projected to grow at 5.00% through 2031, while Western Asia is expected to expand in the 5%-6% range and Africa in the 4% range, from lower bases. These regions are at an earlier stage of development, so retail modernization and cold-chain investment matter more than regulation-driven replacement in the near term. The Kigali framework remains important because it pulls developing economies onto the HFC phase-down path and supports a gradual shift away from legacy refrigerants. As store networks and foodservice formats modernize, the ice-cream freezers market in these geographies should expand through a mix of first-time installations and selective upgrades, rather than solely through broad fleet conversion.

- AHT Cooling Systems (Daikin)

- Epta Group (IARP/Eurocryor)

- Arneg Group

- ISA S.p.A.

- Liebherr Professional

- Hussmann (Panasonic)

- Carrier Commercial Refrigeration

- Beverage-Air (Ali Group)

- Turbo Air

- Master-Bilt

- Nor-Lake

- Sanden Intercool

- Blue Star (India)

- Western Refrigeration (India)

- Rockwell Industries

- Vestfrost Solutions

- TEFCOLD

- Jordao

- Maxx Cold

- Avantco

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 HFC phase-down and efficiency mandates driving replacement cycles

- 4.2.2 Retail footprint expansion and modernization in Asia-Pacific

- 4.2.3 Natural refrigerants (R290/CO2) adoption enabling higher-efficiency plug-ins

- 4.2.4 Growth of supermarkets/convenience formats and premium gelato outlets

- 4.2.5 Energy labeling and procurement transparency (EU) accelerating upgrades

- 4.2.6 Waterloop/semi plug-in architectures enabling heat recovery and flexible layouts

- 4.3 Market Restraints

- 4.3.1 Technician skill gaps and safety code compliance for HC/CO2

- 4.3.2 High upfront costs amid energy price volatility

- 4.3.3 Hydrocarbon charge/room-size limits restricting some sites

- 4.3.4 EU market surveillance and conformity burdens elongating purchase cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Competitive Rivalry

- 4.5.2 Supplier Power

- 4.5.3 Buyer Power

- 4.5.4 Threat of Substitutes

- 4.5.5 Threat of New Entrants

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights into the Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.) in the Industry

- 4.8 Insights into Commercial End Users' Buying Behavior and Key Selection Criteria for Icecream Freezers

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Chest/Deep Freezers

- 5.1.2 Upright/Glass-Door Freezers

- 5.1.3 Dipping Cabinets/Scooping Freezers

- 5.1.4 Countertop Ice-Cream Freezers

- 5.1.5 Island/Multideck Freezers for Ice-Cream

- 5.2 By Cooling Technology

- 5.2.1 Static

- 5.2.2 Ventilated/Forced-Air

- 5.2.3 Hybrid

- 5.2.4 Remote Glycol/Waterloop (SPI)

- 5.3 By Capacity (Liters)

- 5.3.1 <=300 L

- 5.3.2 301-600 L

- 5.3.3 >600 L

- 5.4 By End User

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience Stores/Gas Stations

- 5.4.3 Ice-Cream Parlors & Gelaterias

- 5.4.4 HoReCa (Restaurants, Cafes, QSRs)

- 5.4.5 Bars & Clubs

- 5.5 By Sales Channel

- 5.5.1 Distributors/Dealers

- 5.5.2 Direct OEM/Key Accounts

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East And Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 AHT Cooling Systems (Daikin)

- 6.4.2 Epta Group (IARP/Eurocryor)

- 6.4.3 Arneg Group

- 6.4.4 ISA S.p.A.

- 6.4.5 Liebherr Professional

- 6.4.6 Hussmann (Panasonic)

- 6.4.7 Carrier Commercial Refrigeration

- 6.4.8 Beverage-Air (Ali Group)

- 6.4.9 Turbo Air

- 6.4.10 Master-Bilt

- 6.4.11 Nor-Lake

- 6.4.12 Sanden Intercool

- 6.4.13 Blue Star (India)

- 6.4.14 Western Refrigeration (India)

- 6.4.15 Rockwell Industries

- 6.4.16 Vestfrost Solutions

- 6.4.17 TEFCOLD

- 6.4.18 Jordao

- 6.4.19 Maxx Cold

- 6.4.20 Avantco

7 Market Opportunities & Future Outlook

- 7.1 Digital energy-and-compliance procurement (EPREL + API telemetry) bundles for ice-cream fleets

- 7.2 Tropicalized hydrocarbon semi plug-in (waterloop) retrofits with heat recovery for small-format stores