|

시장보고서

상품코드

2063938

AI 단백질 공학 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)AI Protein Engineering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

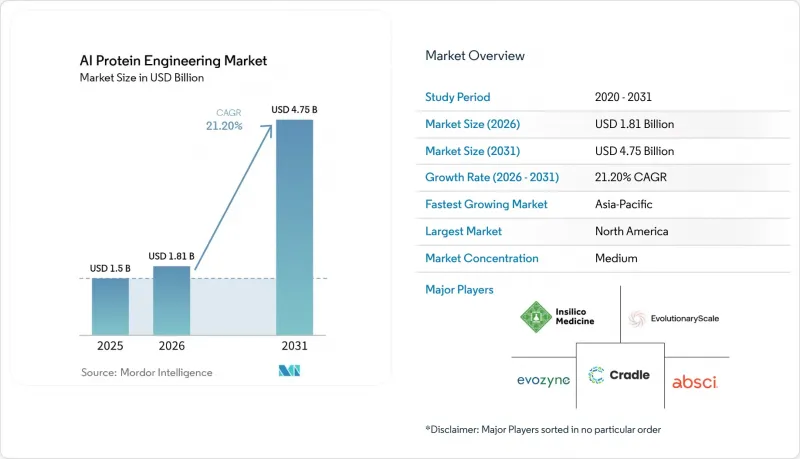

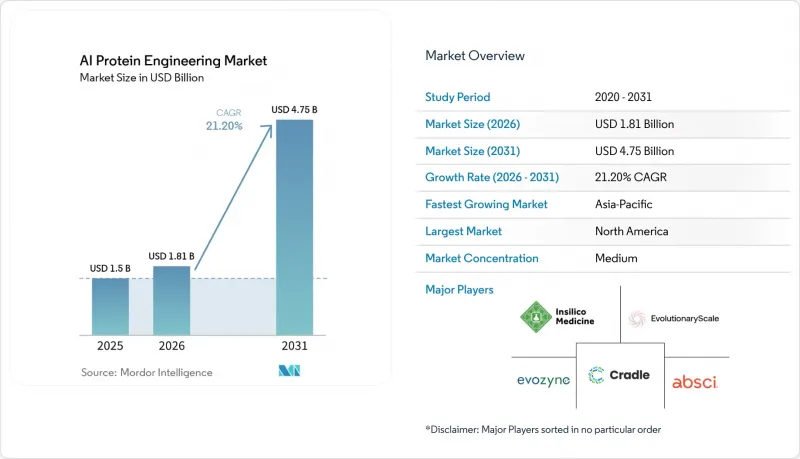

Mordor Intelligence에 의하면, AI 단백질 공학 시장 규모는 2025년 15억 달러, 2026년 18억 1,000만 달러에서 2031년까지 47억 5,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 21.20%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 등), 단백질 유형(단일클론 항체 등), 기술적 접근 방식(합리적 설계 등), 용도(신약 개발, 농업용 단백질 등), 최종 사용자(제약 업계 등), 도입 형태(클라우드, On-Premise, 하이브리드), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액 기준(달러)으로 표시되어 있습니다.

세계 AI 단백질 공학 시장 동향 및 인사이트

바이오의약품 분야에서 바이오의약품 개발 가속화에 대한 수요

의약품 개발 기업들이 바이오의약품의 신속한 신약 개발, 반복 작업의 부담 경감, 그리고 접근이 어려운 표적에 대한 접근을 우선시함에 따라, 단백질 공학 분야의 AI 시장은 확대되고 있습니다. Absci사는 자사의 플랫폼이 ABS-201을 전임상 단계의 개념에서 2년 만에 3개의 투여군을 포함하는 1상 임상시험 단계로 발전시킨 능력을 입증함으로써, 개발 주기 단축에 있어 AI의 역할을 보여주었습니다. 또한, 이 플랫폼은 표적당 100건 미만의 설계만으로 제로 우선순위 에피토프 후보를 생성할 수 있음을 보여줌으로써, 대규모 스크리닝에 대한 의존도를 낮췄습니다. 대형 제약 기업과의 제휴 및 막대한 자금 조달은 이러한 수요가 연구 개발 전략에 필수적임을 보여줍니다. 모델 출력, 실험을 통한 후속 조치, 그리고 성과 제공을 통합한 플랫폼은 독립형 소프트웨어를 제공하는 플랫폼보다 더 많은 지지를 얻고 있습니다.

신규 히트 물질 창출을 촉진하는 단백질 기반 모델

배열, 구조, 기능을 통합한 기반 모델의 발전이 단백질 공학 분야의 AI 시장을 주도하고 있습니다. EvolutionaryScale사의 ESM3는 28억 개의 단백질 서열과 1.1×10^24 FLOPS를 활용해 학습되었으며, 5억 년에 해당하는 자연 진화에 필적하는 새로운 형광 단백질을 창출해 냈습니다. 이는 데 노보 설계 분야에서 획기적인 진전을 보여줍니다. 이러한 발전으로 인해 AI를 통해 설계된 단백질과 기존에 발견된 단백질 간의 격차가 좁혀지면서, 치료 및 산업 분야에서의 AI 신뢰도가 높아지고 있습니다. 업계 전반에 걸쳐 모델의 품질이 향상됨에 따라, 독자적인 실험적 피드백이 중요한 차별화 요소로 부상하고 있습니다. 견고한 내부 검증 프로세스를 갖춘 기업은 경쟁 우위를 유지하는 데 있어 유리한 입장에 있습니다.

실험적 검증의 병목 현상과 습식 실험실의 비용 효율성

단백질 공학 분야의 AI 시장은 인실리코(in silico)를 통한 서열 생성이 실험실에서의 검증을 능가하고 있기 때문에 병목 현상에 직면해 있습니다. 96가지 변이에 대한 ‘설계·구축·시험·학습’의 각 주기에는 여전히 59시간의 실험실 작업이 필요하기 때문에 로봇 기술을 활용하더라도 이 공정은 자본 집약적입니다. 이로 인해 자동화 인프라나 반복 실험을 위한 자금이 부족한 중소 바이오기술 기업이나 학술 연구팀은 제약을 받게 됩니다. 그 결과, 활동은 클라우드 컴퓨팅이나 자동화와 같은 첨단 자원을 갖춘, 자금력이 풍부한 거점에 집중되고 있습니다. 비용 대비 효과가 높은 검증 모델이 이용 가능해질 때까지는 이 시장의 지역별 성장세가 여전히 고르지 않을 것입니다.

부문별 분석

2025년, 소프트웨어 솔루션 부문은 단백질 공학 분야의 AI 시장에서 38.20%의 점유율을 차지하며, 조기 도입 추세를 반영했습니다. 바이오의약품 기업의 사용자들은 프로그램 전체를 외부에 위탁하기보다는 단백질 언어 모델을 통합하기 위한 소프트웨어에 접근하는 것을 선호했습니다. 슈뢰딩거사는 1억 9,950만 달러의 소프트웨어 매출을 기록했으며, 상위 20개 제약사와의 계약액은 15.3% 증가한 8,080만 달러에 달했습니다. 이 단계에서 기업은 기존 워크플로우 내에서 AI를 시범적으로 도입하여 사내 조달 체계와 조화를 이룰 수 있었습니다. 임상 적용이 임박한 AI 설계 프로그램에 대한 종단간 지원을 요구하는 구매자가 증가함에 따라, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 21.05%를 기록하며 성장할 것으로 전망됩니다.

2025년에는 단일클론 항체가 매출의 39.78%를 차지하며, 확립된 개발 및 규제 절차를 바탕으로 주도적인 위치를 차지했습니다. AI는 이 성숙한 단백질 군을 재구성함으로써 워크플로우 내 실험 부담을 줄이고 있습니다. 백신 및 항원은 SKYCovione과 같은 규제 당국의 승인을 발판으로 2031년까지 연평균 성장률(CAGR) 21.76%를 기록하며 성장할 것으로 예측됩니다. 이러한 성장에 힘입어 시장은 치료용 항체에서 예방용 및 항원 설계 프로그램으로 확대되며, 백신 관련 업무가 단백질 설계의 자연스러운 연장선상에 자리 잡게 될 것입니다.

지역별 분석

2025년, 북미는 단백질 공학 분야의 AI 시장에서 44.32%의 점유율을 차지하며, 매출, 기업 집중도 및 상용화 준비 측면에서 최대 지역 클러스터로서의 위상을 유지했습니다. 이러한 선도적 지위는 강력한 바이오의약품 생태계, 막대한 벤처 캐피털 투자, 그리고 의약품 개발 기업 및 중개 연구소와 협력하는 기초 모델 기반 스타트업의 밀집된 존재에 의해 뒷받침되고 있습니다. 이 지역은 플랫폼 기업, ?랩 인프라, 자본 제공업체 간의 효율적인 협력의 혜택을 누리고 있으며, 이는 신약 개발 단계에서 자금 지원을 받는 개발 프로그램으로의 전환을 가속화하고 있습니다. 대규모 자금 조달 라운드는 이 지역이 전 세계의 자본을 유치하는 능력을 더욱 부각시키고 있습니다.

유럽은 단백질 공학 분야의 AI 시장 점유율은 작지만, 공공 연구 자금, 단백질 공학 분야의 학술적 전문 지식, 그리고 상업화 파이프라인에 기여하는 활발한 중개 연구 프로젝트 덕분에 기술적으로는 여전히 중요한 위치를 차지하고 있습니다. 범용 단백질 공학 및 자율적 바이오프로세스 개발에 대한 지원을 목표로 하는 자금 지원 이니셔티브는 스타트업과 산업계의 공동 프로그램을 뒷받침하는 과학적 기반을 강화하고 있습니다. 이 연구 그룹은 중개 연구 용도의 도구와 시스템 개발을 추진하고 있으며, 기초 과학에서 상용화에 이르는 과정에서 유럽의 역할을 확대되고 있습니다. 규모는 작지만, 유럽은 방법론 개발, 인재 양성, 스핀아웃 기회 창출에 기여하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 24.25%를 기록하며 성장할 것으로 예상되며, 단백질 공학 분야의 AI 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 정책 지원, 바이오 합성 기술의 역량 확대, 그리고 중국, 일본, 한국, 호주 등 주요 국가에서의 현지 데이터셋 및 플랫폼 기업 개발에 힘입어 이루어지고 있습니다. AI와 바이오 제조의 통합을 지시하는 지침이나 단백질 서열 데이터베이스의 발전과 같은 지역 차원의 노력이 진전을 가속화하고 있습니다. 중동 및 아프리카와 남미는 여전히 초기 단계에 있지만, 세계 임상시험 네트워크에 참여함으로써 AI 설계에 기반한 생물학적 제제에 대한 이해를 심화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the aI protein engineering market size is projected to expand from USD 1.5 billion in 2025 and USD 1.81 billion in 2026 to USD 4.75 billion by 2031, registering a CAGR of 21.20% between 2026 to 2031.

This report is Segmented by Component (Software and Mores), Protein Type (Monoclonal Antibodies, Eand More), Technology Approach (Rational Design, and More), Application (Drug Discovery, Agricultural Proteins, and More), End User (Pharmaceutical, and More), Deployment Mode (Cloud, On-Premises, Hybrid), and Geography (North America, Europe, and More). Market Forecasts in Value (USD).

Global AI Protein Engineering Market Trends and Insights

Biopharma Demand for Faster Biologics Discovery

The AI in protein engineering market is growing as drug developers prioritize faster biologics discovery, reduced iteration burdens, and access to challenging targets. Absci demonstrated its platform's ability to advance ABS-201 from a preclinical concept to three dosed Phase 1 cohorts in two years, showcasing AI's role in shortening development cycles. The platform also showed that fewer than 100 designs per target could generate candidates for zero-prior epitopes, reducing reliance on large-scale screening. Partnerships with major pharmaceutical companies and significant funding indicate that this demand is integral to R&D strategies. Platforms integrating model output, experimental follow-up, and delivery are gaining traction over those offering standalone software.

Protein Foundation Models Improving De Novo Hit Generation

Advancements in foundation models that integrate sequence, structure, and function are driving the AI in protein engineering market. EvolutionaryScale's ESM3, trained on 2.8 billion protein sequences with 1.1 x 10^24 FLOPS, created novel fluorescent proteins equivalent to 500 million years of natural evolution, marking a leap in de novo design. This progress narrows the gap between AI-designed and traditionally discovered proteins, increasing AI's credibility for therapeutic and industrial applications. As model quality improves across the industry, proprietary experimental feedback is becoming a key differentiator. Companies with robust internal validation processes are better positioned to maintain competitive advantages.

Experimental Validation Bottlenecks and Wet-lab Cost Intensity

The AI in protein engineering market faces bottlenecks as in silico sequence generation outpaces laboratory validation. Each design-build-test-learn cycle of 96 variants still requires 59 hours of wet-lab processing, making the process capital-intensive even with robotics. This limits smaller biotech firms and academic teams that lack funding for automated infrastructure or repeated experimental rounds. Consequently, activity is concentrated in well-funded hubs with advanced resources like cloud computing and automation. Until cost-effective validation models are accessible, regional growth in this market will remain uneven.

Other drivers and restraints analyzed in the detailed report include:

- Wet-lab Automation Closing the Design-build-test Loop

- Multispecific Antibody Complexity Favoring AI-native Design Stacks

- Biosecurity and Regulatory Scrutiny for Novel Proteins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Software & Solutions held a 38.20% share of the AI in protein engineering market, reflecting early adoption trends. Biopharma users preferred software access to integrate protein language models rather than outsourcing entire programs. Schrodinger reported USD 199.5 million in software revenue, with top 20 pharma contract value rising 15.3% to USD 80.8 million. This phase allowed companies to test AI within existing workflows, aligning with internal procurement structures. Services are projected to grow at a 21.05% CAGR through 2031, as buyers increasingly seek end-to-end support for AI-designed programs nearing clinical use.

Monoclonal antibodies accounted for 39.78% of revenue in 2025, leading due to their established development and regulatory pathways. AI is reshaping this mature protein class, reducing experimental burdens in workflows. Vaccines & Antigens are expected to grow at a 21.76% CAGR through 2031, driven by regulatory approvals like SKYCovione. This growth expands the market from therapeutic antibodies to include prophylactic and antigen design programs, making vaccine-related work a credible extension of protein design.

Geography Analysis

In 2025, North America held a 44.32% share of the AI in protein engineering market, maintaining its position as the largest regional cluster by revenue, company concentration, and commercial readiness. This leadership is driven by strong biopharma ecosystems, significant venture capital investments, and a high density of foundational model start-ups collaborating with drug developers and translational labs. The region benefits from efficient integration between platform companies, wet-lab infrastructure, and capital providers, which accelerates the transition from discovery to funded development programs. Large-scale funding rounds further highlight the region's ability to attract global capital.

Europe holds a smaller share of the AI in protein engineering market but remains technically significant due to public research funding, academic expertise in protein engineering, and active translational projects feeding commercial pipelines. Funding initiatives, such as support for general-purpose protein engineering and autonomous bioprocess development, strengthen the scientific base that supports start-ups and collaborative industry programs. Research groups are advancing tools and systems for translational use, extending Europe's role from basic science to commercialization pathways. While smaller in scale, Europe contributes to method development, talent creation, and spin-out opportunities.

Asia-Pacific is forecast to grow at a 24.25% CAGR through 2031, making it the fastest-growing region in the AI in protein engineering market. Growth is driven by policy support, expanding biosynthetics capabilities, and the development of local datasets and platform companies in key countries like China, Japan, South Korea, and Australia. Regional initiatives, such as directives to integrate AI and biomanufacturing and advancements in protein sequence databases, are accelerating progress. While still in early stages, the Middle East, Africa, and South America are building familiarity with AI-designed biologics through participation in global clinical trial networks.

- Absci

- AI Proteins

- Arzeda

- Biomatter

- Cradle

- DenovAI Biotech

- Diffuse Bio

- EvolutionaryScale

- Evozyne

- Generate:Biomedicines

- Ginkgo Bioworks

- Insilico Medicine

- Isomorphic Labs

- Latent Labs

- Nabla Bio

- Profluent

- ProteinQure

- Recursion Pharmaceuticals

- Schrodinger

- XtalPi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Biopharma Demand for Faster Biologics Discovery

- 4.2.2 Protein Foundation Models Improving De Novo Hit Generation

- 4.2.3 Wet-Lab Automation Closing the Design-Build-Test Loop

- 4.2.4 Expansion of Enzyme Engineering in Industrial Biotech and Food Systems

- 4.2.5 Multispecific Antibody Complexity Favoring AI-Native Design Stacks

- 4.2.6 Proprietary Assay-Data Network Effects Strengthening Platform Economics

- 4.3 Market Restraints

- 4.3.1 Experimental Validation Bottlenecks and Wet-Lab Cost Intensity

- 4.3.2 Biosecurity and Regulatory Scrutiny for Novel Proteins

- 4.3.3 Training-Data Provenance and IP Ambiguity

- 4.3.4 GPU Access and Sovereign-Compute Constraints

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software & Solutions

- 5.1.2 Services

- 5.2 By Protein Type

- 5.2.1 Monoclonal Antibodies

- 5.2.2 Enzymes

- 5.2.3 Peptides & Miniproteins

- 5.2.4 Vaccines & Antigens

- 5.2.5 Cytokines & Growth Factors

- 5.3 By Technology Approach

- 5.3.1 Rational Design

- 5.3.2 Directed Evolution

- 5.3.3 De Novo Design

- 5.3.4 Hybrid / Semi-rational Design

- 5.3.5 Physics-informed Simulation

- 5.4 By Application

- 5.4.1 Drug Discovery & Biologics

- 5.4.2 Enzyme Engineering & Industrial Biotechnology

- 5.4.3 Agricultural & Food Proteins

- 5.4.4 Vaccines & Immunotherapy Design

- 5.4.5 Synthetic Biology & Research Tools

- 5.4.6 Diagnostics & Biosensors

- 5.5 By End User

- 5.5.1 Pharmaceutical Companies

- 5.5.2 Biotechnology Companies

- 5.5.3 Contract Research Organizations

- 5.5.4 Academic & Research Institutes

- 5.5.5 Agri-food & Industrial Biotechnology Companies

- 5.6 By Deployment Mode

- 5.6.1 Cloud

- 5.6.2 On-premises

- 5.6.3 Hybrid

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Absci

- 6.3.2 AI Proteins

- 6.3.3 Arzeda

- 6.3.4 Biomatter

- 6.3.5 Cradle

- 6.3.6 DenovAI Biotech

- 6.3.7 Diffuse Bio

- 6.3.8 EvolutionaryScale

- 6.3.9 Evozyne

- 6.3.10 Generate:Biomedicines

- 6.3.11 Ginkgo Bioworks

- 6.3.12 Insilico Medicine

- 6.3.13 Isomorphic Labs

- 6.3.14 Latent Labs

- 6.3.15 Nabla Bio

- 6.3.16 Profluent

- 6.3.17 ProteinQure

- 6.3.18 Recursion Pharmaceuticals

- 6.3.19 Schrodinger

- 6.3.20 XtalPi

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment