|

시장보고서

상품코드

2063940

수술실용 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Operating Room - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

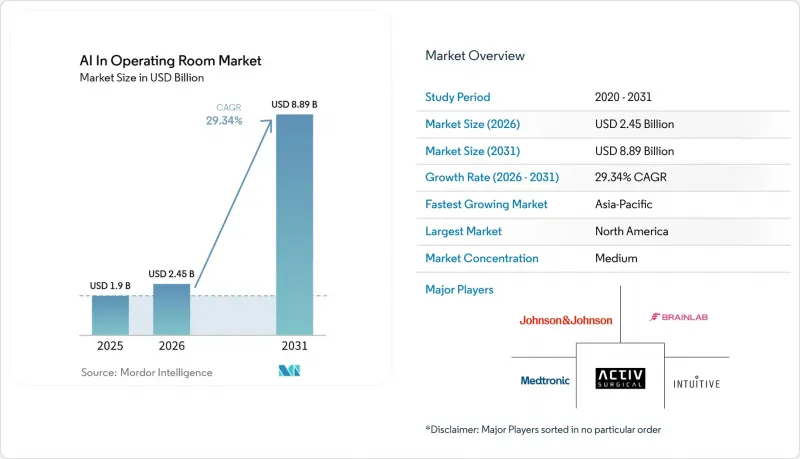

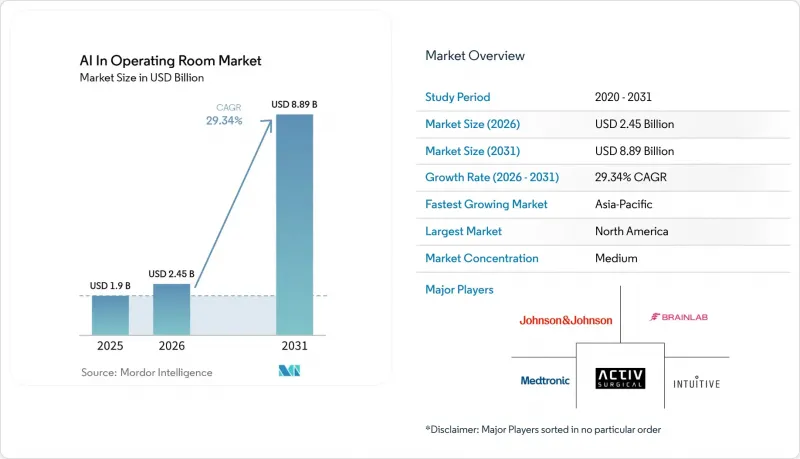

Mordor Intelligence에 의하면, 수술실용 AI 시장 규모는 2025년 19억 달러로 평가되었고, 2026년에는 24억 5,000만 달러로 추정되고, 2031년까지 88억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 29.34%로 성장할 전망입니다.

본 보고서는 제공 형태별(소프트웨어, 하드웨어, 서비스), 기술별(머신러닝 및 딥러닝, 기타), 용도별(수술 중 안내 및 내비게이션, 기타), 외과 전문 분야별(일반외과, 기타), 도입 형태별(클라우드 기반, 기타), 최종 사용자별(병원, ASC, 클리닉, 기타), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 수술실용 AI 시장 동향 및 인사이트

저침습 수술 및 로봇 보조 수술에 대한 수요 증가

저침습 수술에 대한 수요가 증가함에 따라 수술실용 AI 시장이 성장하고 있습니다. 이러한 수술은 영상, 정밀도, 워크플로우의 일관성에 의존하기 때문입니다. 2025년 연구에 따르면, AI 로봇 시스템은 기존 방식에 비해 수술 시간을 25% 단축하고, 수술 중 합병증을 30% 감소시키며, 수술 정확도를 40% 향상시켰습니다. 2024년, 영국에서는 3만 6,209건의 로봇 수술이 시행되었으며, 이는 시범 프로그램 단계에서 본격적인 보급 단계로 넘어가고 있음을 보여줍니다. 수술 건수가 증가함에 따라, 주석이 달린 외과 데이터가 AI 모델을 강화하고, 로봇 시스템의 사용을 간소화하며, 보급을 확대하는 피드백 루프가 형성되고 있습니다.

AI를 활용한 수술 중 의사결정 지원과 실시간 영상 기술의 발전

실시간 AI 의사결정 지원은 수술실용 AI 시장의 주요 성장 동력으로 부상하고 있습니다. 복강경 간 수술용으로 검증된 AI 시스템은 초당 19.2 프레임의 속도로 동영상을 처리하여, 상 인식 정확도 89%, 상 분류 정확도 91%를 달성했습니다. 연구에 따르면, 대장 수술 중 관류를 13초 이내에 0.98의 재현율로 예측하는 AI의 능력이 입증되었습니다. 두경부 종양 수술에서 딥러닝을 활용한 초분광 영상을 통해 10분 이내에 0.98의 분류 정확도를 달성했습니다. 이러한 발전 덕분에 영상 진단이 표준화되고 신속한 의사 결정이 가능해짐에 따라, 응급 상황에서 기존의 저속한 기법에 대한 의존도가 낮아집니다.

설비 투자 및 시스템 총 소유 비용 증가

도입 비용은 특히 소규모 시설의 경우, 수술실에 AI를 도입하는 데 있어 큰 걸림돌이 되고 있습니다. 로봇 수술 플랫폼은 건당 비용이 복강경 수술에 비해 1.5배에서 2배 더 비싸며, 다빈치 시스템의 하드웨어는 1대당 50만 달러에서 250만 달러의 비용이 듭니다. 투자 회수에는 수술 건수가 많은 의료기관에서도 3-5년, 소규모 병원에서는 7년 이상이 소요되는 경우가 있습니다. 소프트웨어 라이선스, 시스템 통합, 검증, 교육 등의 비용이 추가됨에 따라 지역 병원에서의 도입이 지연되고 있습니다. 수술 건수가 많고 여러 진료과에서 활용되는 대규모 의료 시스템은 이러한 비용을 흡수하기 쉬운 입장에 있어 시장의 성장을 가속화하고 있습니다.

부문별 분석

2025년, 하드웨어는 부문 매출의 45.25%를 차지했으며 수술실용 AI 시장의 주요 제품으로서의 입지를 유지했습니다. 이는 수술 중 AI 기능에 필수적인 로봇 수술 콘솔, 영상 시스템, 엣지 컴퓨팅 유닛에 대한 투자에 힘입어 이루어졌습니다. 많은 소프트웨어 도구가 이미 도입된 하드웨어에 의존하고 있기 때문에 병원들은 디지털 수술 프로그램의 기반으로서 이러한 하드웨어 구매를 우선시하고 있습니다. 소프트웨어 도입은 확대되고 있지만, 통합 워크플로우 솔루션을 구현하는 역할을 담당하는 하드웨어는 여전히 필수적입니다.

소프트웨어 시장은 2031년까지 연평균 성장률(CAGR) 32.45%를 나타낼 것으로 예측되며, 이는 가치 창출의 변화를 시사합니다. 벤더에 구애받지 않는 소프트웨어 계층이 점차 보급되면서, 다양한 기기 간의 통합을 가능하게 하고 초기 비용을 절감하고 있습니다. 또한, 소프트웨어를 통해 공급업체는 모델 업데이트, 워크플로 모듈 추가, 지속적인 학습을 통한 성능 향상을 실현할 수 있습니다. 병원들이 도입 지원을 요청하는 가운데, 통합 및 교육 등의 서비스가 확대되면서 정기적인 소프트웨어 및 서비스 계약으로의 전환이 촉진되고 있습니다.

2025년 기준으로, 머신러닝과 딥러닝은 기술 부문의 48.56%를 차지했으며, 수술실용 AI 시장을 주도했습니다. 이러한 우위는 수술 단계의 인식, 해부학적 분할, 수술 중 위험 예측 분야의 발전을 반영하고 있습니다. 이러한 기술들은 수술실 업무에 매우 적합하며, 측정 가능한 임상적 및 운영상의 이점을 입증하고 있어 병원의 조달 과정에서 도입이 촉진되고 있습니다.

파운데이션 모델은 이 분야의 역량을 재정의하고 있으며, 수술 전용으로 구축된 데이터를 통해 그 성능이 향상되고 있습니다. 증강현실(AR)과 가상현실(VR)은 내비게이션 오버레이 및 시뮬레이션 도구의 성장에 힘입어 2031년까지 연평균 성장률(CAGR) 33.24%를 기록하며 성장할 것으로 전망됩니다. 시장은 진화하고 있으며, 현재 머신러닝이 수익을 주도하는 한편, 파운데이션 모델과 AR/VR 도구가 미래의 차별화 요소로 부상하고 있어, 경쟁은 하드웨어의 범위를 넘어 확대되고 있습니다.

지역별 분석

2025년, 북미는 수술실용 AI 시장의 42.17%라는 압도적인 점유율을 차지했으며 주요 지역 부문으로서의 입지를 확고히 다졌습니다. 이러한 선도적 지위는 로봇 시스템 도입 대수가 많고, 병원의 기술 예산이 충실하며, 상용화를 가능하게 하는 규제 당국의 일관된 승인이 있었기 때문입니다. 미국은 특수 수술을 막론하고 로봇 수술의 도입이 확대되고 있으며, 병원이 연결형 수술 플랫폼을 통합할 수 있는 역량을 갖추고 있다는 점에서 성장을 주도하고 있습니다. 캐나다와 멕시코는 시장 규모는 작지만, 현대화 노력과 국경을 초월한 임상 협력 확대라는 혜택을 누리고 있습니다.

아시아태평양은 2031년까지의 예상 연평균 성장률(CAGR)이 34.50%에 달할 전망이며, 모든 지역을 앞지르는 성장이 예상됩니다. 이러한 성장은 병원의 현대화, 전문의 부족 문제의 심화, 수술 생산성 향상에 대한 압박에 의해 주도되고 있습니다. 중국은 높은 수술 건수와 국내 플랫폼 개발을 지원하는 정책을 바탕으로 성장을 이루고 있습니다. 인도에서는 도시 지역의 병원에서 수술용 로봇과 AI 도구의 도입이 급속히 진행되고 있는 반면, 일본과 한국은 고도화된 디지털화와 정밀 기술에 대한 투자를 통해 기여하고 있습니다.

유럽은 수술실용 AI 시장에서 전략적으로 중요한 위치를 차지하고 있지만, 도입에는 엄격한 규제 요건으로 인한 과제가 있습니다. EU AI법 및 의료기기 규제로 인해 문서화 기준이 강화되면서, 시장 출시까지의 기간에 영향을 미치고 있습니다. 그럼에도 불구하고 독일, 프랑스, 영국, 이탈리아, 스페인은 수술의 디지털화와 높은 임상적 관심을 바탕으로 지역 내 수요를 주도하고 있습니다. 중동 및 아프리카와 남미는 아직 초기 단계에 있지만, 의료 시스템이 접근성 향상, 연수 기회 확대, 수술실 효율 증대를 목표로 하고 있어 성장 잠재력을 지니고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aI in operating room market size is expected to increase from USD 1.9 billion in 2025 to USD 2.45 billion in 2026 and reach USD 8.89 billion by 2031, growing at a CAGR of 29.34% over 2026-2031.

This report is Segmented by Offering (Software, Hardware, Services), Technology (ML and Deep Learning, and More), Application (Guidance and Navigation, and More), Surgical Specialty (General Surgery, and More), Deployment Mode (Cloud-Based, and More), End User (Hospitals, Ascs, Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Operating Room Market Trends and Insights

Rising Demand for Minimally Invasive and Robotic-Assisted Surgeries

The growing demand for minimally invasive surgeries is driving the AI in operating room market, as these procedures rely on imaging, precision, and workflow consistency. A 2025 study revealed that AI-robotic systems reduced operative times by 25%, intraoperative complications by 30%, and improved procedural precision by 40% compared to traditional methods. In 2024, the UK performed 36,209 robotic surgeries, indicating a shift from pilot programs to widespread adoption. As more procedures are conducted, annotated surgical data enhances AI models, creating a feedback loop that simplifies robotic system use and expands adoption.

AI-Driven Intraoperative Decision Support and Real-Time Imaging Advancements

Real-time AI decision support is emerging as a key growth driver for the AI in operating room market. A validated AI system for laparoscopic liver surgery processed video at 19.2 frames per second with 89% phase recognition accuracy and 91% phase classification. Another study demonstrated AI's ability to predict perfusion during colorectal surgery with 0.98 recall within 13 seconds. In head and neck tumor surgeries, hyperspectral imaging with deep learning achieved 0.98 classification accuracy in under 10 minutes. These advancements enable standardized image interpretation and faster decision-making, reducing reliance on slower methods in critical cases.

Elevated Capital Expenditures and Overall System Ownership Costs

Acquisition costs remain a significant barrier to AI adoption in operating rooms, particularly in smaller facilities. Robotic surgery platforms are 1.5 to 2 times more expensive per procedure than laparoscopic alternatives, with da Vinci system hardware costing between USD 0.5 million and USD 2.5 million per installation. Return on investment can take 3 to 5 years for high-volume centers and over 7 years for smaller hospitals. These costs, including software licensing, integration, validation, and training, slow adoption in community hospitals. Larger health systems with higher case volumes and multi-department usage are better positioned to absorb these expenses, driving faster market growth.

Other drivers and restraints analyzed in the detailed report include:

- Global Surge in Surgical Volume Amidst Specialist Surgeon Shortages

- Imperatives for Optimizing OR Workflow and Enhancing Operational Efficiency

- Challenges in Data Privacy, Cybersecurity, and System Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, hardware contributed 45.25% of segment revenue, maintaining its position as the leading offering in the AI-driven operating room market. This was driven by investments in robotic surgical consoles, imaging systems, and edge computing units essential for intraoperative AI functions. Hospitals prioritize these purchases as foundational for digital surgery programs, with many software tools relying on installed hardware. While software adoption is growing, hardware remains critical due to its role in enabling integrated workflow solutions.

Software is projected to grow at a 32.45% CAGR through 2031, signaling a shift in value creation. Vendor-neutral software layers are gaining traction, enabling integration across diverse equipment fleets and reducing upfront costs. Software also allows vendors to update models, add workflow modules, and enhance performance through continuous learning. As hospitals demand implementation support, services like integration and training are expanding, driving a transition toward recurring software and service contracts.

Machine learning and deep learning held 48.56% of the technology segment in 2025, leading the AI-driven operating room market. Their dominance reflects advancements in surgical phase recognition, anatomy segmentation, and intraoperative risk prediction. These technologies are well-suited for operating room tasks and have demonstrated measurable clinical and operational benefits, supporting their adoption in hospital procurement.

Foundation models are redefining capabilities in this segment, with purpose-built surgical data enhancing performance. Augmented reality and virtual reality are forecast to grow at a 33.24% CAGR through 2031, driven by navigation overlays and simulation tools. The market is evolving, with machine learning driving current revenues while foundation models and AR/VR tools shape future differentiation, expanding competition beyond hardware.

Geography Analysis

In 2025, North America commanded a dominant 42.17% share of the AI in operating room market, solidifying its position as the leading regional segment. This leadership stems from a large installed base of robotic systems, strong hospital technology budgets, and consistent regulatory approvals enabling commercial rollouts. The U.S. drives growth with expanding robotic procedure adoption across specialties and hospitals' ability to integrate connected surgical platforms. Canada and Mexico, though smaller markets, benefit from modernization efforts and growing cross-border clinical collaborations.

Asia-Pacific is set to outpace all regions, boasting a projected CAGR of 34.50% through 2031. Growth is driven by hospital modernization, a widening specialist shortage, and pressure to enhance surgical productivity. China leverages high procedural volumes and supportive policies for local platform development. India sees rapid adoption of surgical robotics and AI tools in urban hospitals, while Japan and South Korea contribute with advanced digitalization and investments in precision technologies.

Europe holds strategic importance in the AI in operating room market, but adoption faces challenges from stringent regulatory requirements. The EU AI Act and medical device rules increase documentation standards, affecting time to market. Despite this, Germany, France, the U.K., Italy, and Spain lead regional demand through surgical digitization and strong clinical interest. The Middle East, Africa, and South America, though in early stages, offer growth potential as health systems aim to improve access, training, and operating room efficiency.

- Activ Surgical, Inc.

- Asensus Surgical, Inc.

- Augmedics Ltd.

- Brain Lab

- Caresyntax GmbH

- CMR Surgical Ltd.

- DeepOR S.A.S.

- ExplORer Surgical Corp.

- GE Healthcare

- Holo Surgical Inc.

- Hypervision Surgical

- Intuitive Surgical, Inc.

- Johnson & Johnson (Ethicon / Auris Health)

- Karl Storz

- LeanTaaS, Inc.

- Medtronic

- Moon Surgical

- Noah Medical

- Oath Surgical

- Proximie Ltd.

- See All AI

- Siemens Healthineers

- Stryker

- Theator, Inc.

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Minimally Invasive & Robotic-Assisted Surgeries

- 4.2.2 AI-Driven Intraoperative Decision Support & Real-Time Imaging Advancements

- 4.2.3 Global Surge in Surgical Volume Amidst Surgeon Shortages

- 4.2.4 Imperatives for Optimizing OR Workflow & Enhancing Operational Efficiency

- 4.2.5 Broadened Reimbursement Policies for AI-Enhanced Medical Procedures

- 4.3 Market Restraints

- 4.3.1 Elevated Capital Expenditures and Overall Ownership Costs

- 4.3.2 Challenges in Data Privacy, Cybersecurity & System Interoperability

- 4.3.3 Navigating Regulatory Complexities & Validating AI Devices (EU AI Act, FDA SaMD)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Machine Learning and Deep Learning

- 5.2.2 Generative AI and Foundation Models

- 5.2.3 Natural Language Processing and Knowledge Graphs

- 5.2.4 Computer Vision and Image Recognition

- 5.2.5 Utilization of Augmented Reality (AR) / Virtual Reality (VR)

- 5.2.6 Surgery's Edge AI & IoT Integration

- 5.2.7 Robotic Process Automation (RPA) in Medical Settings

- 5.3 By Application

- 5.3.1 Guidance & Navigation During Surgery

- 5.3.2 Planning & Risk Assessment Before Surgery

- 5.3.3 Monitoring Outcomes Post-Surgery

- 5.3.4 Enhancing Surgical Workflow & Efficiency

- 5.3.5 Training & Simulation for Surgeons

- 5.4 By Surgical Speciality

- 5.4.1 General Surgical Practices

- 5.4.2 Orthopedic & Spine Procedures

- 5.4.3 Urological Surgeries

- 5.4.4 Cardiac & Cardiothoracic Operations

- 5.4.5 Neurosurgical Interventions

- 5.4.6 Gastrointestinal & Colorectal Procedures

- 5.4.7 Gynecological Surgeries

- 5.4.8 ENT & Eye Operations

- 5.4.9 Others

- 5.5 By Deployment Mode

- 5.5.1 Cloud-Based

- 5.5.2 Hybrid

- 5.5.3 On-Premises

- 5.6 By End User

- 5.6.1 Hospitals & Surgical Facilities

- 5.6.2 Centers for Ambulatory Surgery (ASCs)

- 5.6.3 Specialized Medical Clinics

- 5.6.4 Academic Institutions & Research Bodies

- 5.6.5 Facilities for Surgical Training & AI Health Technology Centers

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Activ Surgical, Inc.

- 6.4.2 Asensus Surgical, Inc.

- 6.4.3 Augmedics Ltd.

- 6.4.4 Brainlab AG

- 6.4.5 Caresyntax GmbH

- 6.4.6 CMR Surgical Ltd.

- 6.4.7 DeepOR S.A.S.

- 6.4.8 ExplORer Surgical Corp.

- 6.4.9 GE HealthCare

- 6.4.10 Holo Surgical Inc.

- 6.4.11 Hypervision Surgical

- 6.4.12 Intuitive Surgical, Inc.

- 6.4.13 Johnson & Johnson (Ethicon / Auris Health)

- 6.4.14 Karl Storz SE & Co. KG

- 6.4.15 LeanTaaS, Inc.

- 6.4.16 Medtronic plc

- 6.4.17 Moon Surgical

- 6.4.18 Noah Medical

- 6.4.19 Oath Surgical

- 6.4.20 Proximie Ltd.

- 6.4.21 See All AI

- 6.4.22 Siemens Healthineers AG

- 6.4.23 Stryker Corporation

- 6.4.24 Theator, Inc.

- 6.4.25 Zimmer Biomet Holdings, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space and unmet-need assessment