|

시장보고서

상품코드

2063951

추적 및 조회 솔루션용 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Track And Trace Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

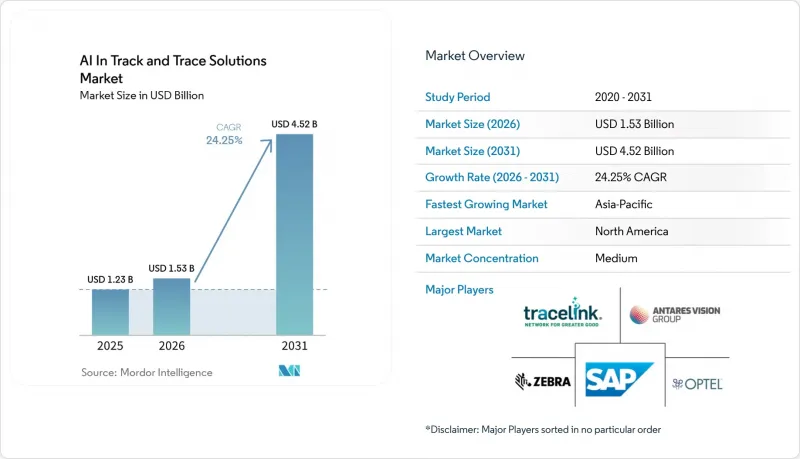

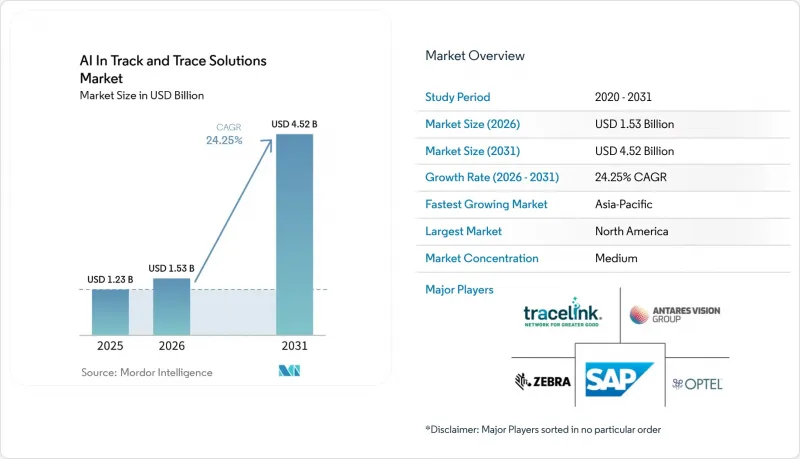

Mordor Intelligence에 의하면, 추적 및 조회 솔루션용 AI 시장 규모는 2025년 12억 3,000만 달러로 평가되었고, 2026년 15억 3,000만 달러로 추정되고, 2031년까지 45억 2,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 24.25%를 나타낼 것으로 예측됩니다.

본 보고서는 컴포넌트별(AI 소프트웨어 플랫폼, 하드웨어, 서비스), 기술별(2차원 바코드, RFID, AI 컴퓨터 비전, IoT 센서, EPCIS), 용도별(일련번호 부여, 집계, 검증, 규정 준수, 공급망 가시화), 최종 용도별(의약품, 의료기기, 소비재, 기타), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

세계의 추적 및 조회 솔루션용 AI 시장 동향과 인사이트

전 세계적인 시리얼라이제이션 및 추적성 의무화

추적 및 조회 솔루션용 AI 시장은 우선 법적 규제에 의해 주도되고 있습니다. 이는 연방 및 지역의 시리얼화 규칙이 조달 주기를 직접 유발하기 때문입니다. DSCSA(의약품 안전 추적법)의 시행 일정은 2025년 5월 제조업체, 2025년 8월 도매업체, 2025년 11월 대규모 조제업체를 대상으로 하고 있으며, 이에 따라 연간 내내 공급망 전반에 걸쳐 지출이 활발하게 유지되었습니다. 추적 및 조회 솔루션용 AI 시장에서 제조업체와 유통업체 간의 데이터 교환 성공률은 2025년 중반까지 90%-95%에 달했으나, 예외 처리 및 마스터 데이터 문제가 여전히 나머지 실패 사례의 상당 부분을 차지하고 있습니다. 이는 규정 준수를 강제했을 때와 동일한 규제상 부담이, 이상 감지나 더 정밀한 리콜에 필요한 대규모 이벤트 데이터 세트도 생성하고 있음을 의미합니다. 2025 회계연도에도 FDA의 모니터링 활동은 여전히 활발하게 진행되었으며, CGMP 감사와 병행하여 50건 이상의 DSCSA 검사가 실시되었습니다. 이를 통해 2026년 11월 소형 디스펜서 도입 기한까지 지출이 지속될 것임이 입증되었습니다.

GS1 Sunrise 2027과 2차원 바코드로의 전환

소매 산업 및 포장 상품 전반에 걸쳐 1차원 바코드에서 2차원 바코드로의 전환 역시 시장을 형성하고 있습니다. GS1 Sunrise 2027에 따르면, 2027년 12월 31일까지 해당 규격을 준수하는 소매 POS 시스템이 2차원 바코드를 판독할 수 있어야 하며, 이 요건은 이미 2026년 포장 계획에 영향을 미치고 있습니다. 추적 및 조회 솔루션용 AI 시장에서 듀얼 마킹 단계에 있는 각 브랜드 기업들은 2차원 코드가 하나의 매체에 일련번호, 로트 데이터, 유효기간을 저장할 수 있다는 점을 인식하고 있습니다. 이로 인해 스캔할 때마다 추적 가능성 이벤트가 발생합니다. 이러한 풍부한 데이터 구조는 생산 라인의 속도로 작동하는 AI를 활용한 인쇄 검증 및 머신 비전 검사에 대한 직접적인 수요를 창출하고 있습니다. 이러한 단일 매체에 정보를 집약하는 방식은 2027년 2월부터 시행될 EU의 배터리 패스포트 요건에도 부합하므로, 포장 투자만으로도 여러 규제 요건을 동시에 충족할 수 있게 됩니다.

높은 도입 및 검증 비용

추적 및 조회 솔루션용 AI 시장은 여전히 포장 라인에서 높은 비용 장벽에 직면해 있습니다. 라인당 개조 비용은 15만-40만 달러에 달하며, 여러 라인을 동시에 업그레이드해야 하는 중소 제조업체에게는 여전히 큰 부담이 되고 있습니다. 추적 및 추적 가능성 솔루션에 AI를 도입할 경우, 규제 하에서 진행되는 IQ, OQ, PQ 및 컴퓨터 시스템 검증 작업으로 인해 프로젝트 총비용이 30%-50% 증가할 가능성이 있으므로, 부담은 더욱 커집니다. 또한, 2024년에는 RFID 칩셋 가격도 40%-60% 상승하고, 새로운 규제 요건으로 인해 대상 시장이 확대되는 바로 그 시점에 하드웨어 계획 수립이 더욱 어려워졌습니다. 구매 기업들은 공급업체의 지역 분포와 니어쇼어링 대안을 재검토함으로써 이에 대응하고 있지만, 이러한 선택 과정에는 여전히 인증에 시간이 소요되어 도입을 지연시키는 요인이 되고 있습니다.

부문별 분석

2025년 시장은 소프트웨어로 명확하게 전환되었으며, AI 소프트웨어 플랫폼이 45.2%의 점유율을 차지했습니다. 추적 및 조회 솔루션용 AI 시장에서 이러한 구성 비율은 기업의 구매 행태 변화를 반영하고 있습니다. 이는 하드웨어 도입이 완전히 완료되기 전에 오케스트레이션 계층이 도입되는 사례가 늘어나고 있기 때문입니다. 구매자들은 개별 라인 장비보다 여러 기업 간의 상호 연결성, 워크플로우 제어, 데이터 재사용을 더 중요하게 여깁니다. 이에 따라 추적 및 추적 가능성 솔루션 산업의 AI 부문은 사이트 단위의 개발을 반복할 필요 없이, 파트너 간에 확장 가능한 소프트웨어 계층에 지속적으로 주력하고 있습니다.

또한, 클라우드 서비스가 기존의 온프레미스 모델을 대체함에 따라 서비스 부문은 2031년까지 연평균 성장률(CAGR) 26.9%를 기록하며 가장 빠르게 성장할 것으로 전망됩니다. 많은 사용자가 일회성 도입이 아닌 지속적인 규정 준수 지원을 원하고 있기 때문에 소프트웨어, 검증 지원, 파트너 온보딩을 묶은 관리형 구독 서비스가 점차 확산되고 있습니다. 하드웨어와 엣지 캡처 시스템은 인쇄, 검사, 스캔과 같은 생산 라인 현장에서 여전히 중요하지만, 하류 소프트웨어가 이벤트 스트림에서 더 많은 가치를 추출함에 따라 그 비중은 줄어들고 있습니다. TraceLink의 OPUS 플랫폼은 5가지 비즈니스 오케스트레이션에 걸쳐 16가지 유형의 트랜잭션을 지원하며, 2025년에는 182건의 실시간 트랜잭션을 실현함으로써 그 가치가 시리얼라이제이션을 넘어 확장될 수 있음을 보여주었습니다. 따라서 추적 및 추적 가능성 솔루션 산업에서 AI는 규정 준수 관련 사건이 기록된 후의 네트워크 활동을 수익화할 수 있는 공급업체에 이점을 제공합니다.

시장은 여전히 2차원 바코드와 데이터 매트릭스가 주를 이루고 있으며, 2025년에는 35.2%의 점유율을 차지했습니다. 이러한 입지는 소매업체와 브랜드를 대상으로 전 세계 공급망 전반에 걸쳐 포장 및 스캔 인프라의 업데이트를 촉진하고 있는 ‘GS1 Sunrise 2027’을 통해 더욱 공고해지고 있습니다. 추적·トレ-서빌리티 솔루션 분야의 AI 시장에서 2차원 바코드가 중요하게 여겨지는 이유는 포장 형태를 전면적으로 변경하지 않고도 하나의 라벨에 많은 식별 데이터, 유통기한 데이터, 이벤트 데이터를 기재할 수 있기 때문입니다. 이는 또한 단 한 번의 스캔으로 규정 준수, 제품 정보, 인증을 모두 처리할 수 있어, 소비자용 추적성 시스템으로의 전환을 촉진하고 있습니다.

시장에서 가장 빠르게 성장하고 있는 분야는 IoT 센서 및 환경 모니터링 부문으로, 2031년까지 연평균 성장률(CAGR) 28.1%를 나타낼 것으로 전망됩니다. 이러한 성장은 바이오의약품, 백신, 온도에 민감한 소비재 분야의 콜드체인 관리와 밀접한 관련이 있으며, 이러한 부문에서는 식별 정보 확보와 마찬가지로 상태 모니터링도 중요하게 여겨지고 있습니다. 2025년 4월에 시작된 Identiv와 Tag-N-Trac의 제휴를 통해 BLE 스마트 라벨과 RELATIVITY SaaS 플랫폼을 결합하여 실시간 콜드체인 추적을 실현했으며, 이후 2025년 IoT 플랫폼 상을 수상했습니다. RFID와 NFC 역시 규제 대상 이용 사례에서 진전을 보이고 있으며, 2025년 6월에는 미시간주에서 진행된 시범 프로젝트를 통해 GS1 상호운용성 표준을 활용한 모의 의약품 공급망 전체에 걸친 완벽한 추적 가능성이 보고되었습니다. AI 컴퓨터 비전 기술도 이러한 기술들과 함께 확대되고 있으며, 코그넥스는 규제 대상 제조 분야에서 코드 검사 및 감사 추적에 대한 요구를 충족하기 위해 In-Sight 8900 시리즈를 선보이고 있습니다.

지역별 분석

2025년 시장은 북미가 주도했으며, 매출 점유율은 38.2%를 차지했습니다. 이 지역의 경쟁력은 가장 성숙한 의약품 일련번호 관리 제도에 기인하며, DSCSA(의약품 안전 추적법)에 따라 제조업체, 유통업체, 조제업체에 이르는 장기적인 조달 사이클이 형성되었습니다. 추적 및 조회 솔루션용 AI 시장에서 북미의 구매자들은 현재 기본적인 규정 준수 대응을 넘어 예측 분석, 에이전트 기반 오케스트레이션, 보다 광범위한 전사적 가시성 확보와 같은 최적화 용도로 전환하고 있습니다. FDA의 규정 준수국은 2025 회계연도에 50건 이상의 DSCSA 모니터링 검사를 완료하며 법 집행에 대한 압박을 분명히 유지하고 있으며, 이는 시스템 가동 이후 지속적인 지출을 뒷받침하고 있습니다.

2031년까지 연평균 성장률(CAGR) 26.4%를 기록할 전망이며, 아시아태평양이 가장 빠르게 시장을 확대되고 있습니다. 이 지역은 중국, 인도, 일본, 한국, 태국, 인도네시아에서 정책 성숙도가 단계적으로 발전함에 따른 혜택을 누리고 있습니다. 컴플라이언스 사이클이 겹치면서, 일회성 파동이 아닌 반복되는 구매 기회가 발생하고 있기 때문입니다. 2025년 2월, 인도가 CDSCO 산하에서 의약품 수출 추적 시스템을 통합한 조치는 규정 준수 절차를 간소화하고 GS1 표준 준수 플랫폼에 대한 수요를 강화했습니다. 중국의 NMPA 의약품 추적성 시스템 역시 대규모 제조 거점에서 예외 관리 및 EPCIS 호환성 도입에 대한 수요를 뒷받침하고 있습니다. 추적 및 조회 솔루션용 AI 시장에서 동남아시아 제약 부문의 신규 투자는 일부 공급업체에게 기존 시장에서 볼 수 있는 레거시 시스템 개조 부담 없이 새로운 출발점을 제공합니다.

또한, 이 시장은 유럽 내에서도 중요한 위치를 차지하고 있으며, EU의 의약품 제조 관리(FMD) 성숙도는 여전히 높은 수준을 유지하고 있어, 2025년에는 주요 시장에서 규정 준수율이 95%를 넘어섰습니다. 보다 중요한 다음 단계는 ESPR(유럽 지속가능성 규정)에 따른 ‘디지털 제품 여권’으로, 이는 2027년 2월 배터리 부문에서 시작되어, 이후 2026년과 2027년에 예정된 위임 법령을 통해 다른 범주로 확대될 예정입니다. 이로 인해, 그동안 완전한 직렬화 스택이 필요하지 않았던 소비재, 전자기기, 산업용 기기 제조업체들 사이에서 새로운 구매 주기가 형성될 것입니다. 또한, 2026년 2월 OPTEL이 이집트 의약품청의 규제 준수를 목적으로 Techno Service와 제휴한 사례는 중동 및 아프리카이 국가 차원의 추적성 시스템을 구축하고 있음을 보여줍니다. 한편, 브라질과 사우디아라비아는 유럽의 주요 시장 이외의 지역에서 여전히 활기찬 신흥 시장으로서 존재감을 드러내고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the aI in track and trace solutions market size is projected to expand from USD 1.23 billion in 2025 and USD 1.53 billion in 2026 to USD 4.52 billion by 2031, registering a CAGR of 24.25% between 2026 to 2031.

This report is Segmented by Component (AI Software Platforms, Hardware, Services), Technology (2D Barcodes, RFID, AI Vision, Iot Sensors, EPCIS), Application (Serialization, Aggregation, Verification, Compliance, SC Visibility), End-Use (Pharma, Medical Devices, Consumer Goods, Others), and Geography (North America, Europe, Asia-Pacific, and More). Forecasts are Provided in Value (USD).

Global AI In Track And Trace Solutions Market Trends and Insights

Global Serialization and Traceability Mandates

The AI in track and trace solutions market is being pushed first by law, because federal and regional serialization rules directly trigger procurement cycles. DSCSA enforcement milestones covered manufacturers in May 2025, wholesale distributors in August 2025, and large dispensers in November 2025, which kept spending active across the supply chain during the year. In the AI in track and trace solutions market, data exchange success rates between manufacturers and distributors reached 90%-95% by mid-2025, but exception handling and master data problems still caused many of the remaining failures. This means the same regulatory burden that forced compliance is also creating the large event datasets needed for anomaly detection and more precise recalls. FDA surveillance activity stayed high in FY 2025, with more than 50 DSCSA inspections conducted alongside CGMP audits, which supports continued spending through the small-dispenser deadline in November 2026.

GS1 Sunrise 2027 and 2D Barcode Migration

The market is also being shaped by the move from 1D to 2D codes across retail and packaged goods. GS1 Sunrise 2027 requires compliant retail point-of-sale systems to be able to read 2D barcodes by December 31, 2027, and that requirement is already affecting packaging plans in 2026. In the AI in track and trace solutions market, brands in the dual-marking phase are finding that 2D codes can carry serial numbers, batch data, and expiry dates in one carrier, which turns each scan into a traceability event. That richer data structure creates direct demand for AI print verification and machine vision inspection at production-line speed. The same carrier logic also supports upcoming EU battery passport requirements from February 2027, so packaging investment can serve more than one mandate at the same time.

High Implementation and Validation Costs

The AI in track and trace solutions market still faces a hard cost barrier at the packaging line. Line-level retrofits cost USD 150,000 to USD 400,000 per line, and that remains difficult for small and mid-sized manufacturers that need several lines upgraded at once. In the AI in track and trace solutions market, the burden rises further because IQ, OQ, PQ, and computer system validation work can add 30%-50% to total project cost under regulated conditions. RFID chipset prices also rose 40%-60% in 2024, which made hardware planning more difficult just as new mandates were expanding the addressable base. Buyers are responding by reviewing supplier geography and near-shoring options, but those choices still add qualification time and delay deployment.

Other drivers and restraints analyzed in the detailed report include:

- Counterfeit, Diversion, and Recall-Risk Pressure

- Digital Product Passport Expansion Beyond Pharma

- Fragmented Standards and Legacy-System Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The market showed a clear tilt toward software in 2025, with AI Software Platforms holding 45.2% share. In the AI in track and trace solutions market, that mix reflects a reversal in enterprise buying behavior because orchestration layers are now often purchased before hardware rollouts are fully complete. Buyers are placing more value on multi-enterprise connectivity, workflow control, and data reuse than on stand-alone line equipment. This keeps the AI in track and trace solutions industry focused on software layers that can scale across partners without repeated site-level development.

The market is also seeing the Services segment grow fastest at 26.9% CAGR through 2031 as cloud delivery replaces older on-premise models. Managed subscriptions that bundle software, validation support, and partner onboarding are gaining ground because many users want continuous compliance support rather than one-time installation. Hardware and Edge Capture Systems still matter at the line for printing, inspection, and scanning, but their share is falling as downstream software captures more value from the event stream. TraceLink's OPUS platform showed how that value can extend beyond serialization, with 16 transaction types across 5 business orchestrations and 182 live transactions in 2025. The AI in track and trace solutions industry is therefore rewarding vendors that can monetize network activity after the compliance event is recorded.

The market remained anchored by 2D Barcodes and DataMatrix, which held 35.2% share in 2025. That position is being reinforced by GS1 Sunrise 2027, which is pushing retailers and brands to update packaging and scanning infrastructure across global supply chains. In the AI in track and trace solutions market, 2D codes matter because they let one label carry more identity data, more expiry data, and more event data without a full change in package format. This also supports the shift toward consumer-facing traceability where a single scan can serve compliance, product information, and authentication.

The market is expanding fastest in IoT Sensors and Environmental Monitoring, which is projected to grow at 28.1% CAGR through 2031. That growth is tied to cold-chain control in biologics, vaccines, and temperature-sensitive consumer goods, where condition monitoring matters as much as identity capture. The Identiv and Tag-N-Trac partnership launched in April 2025 combined BLE smart labels with the RELATIVITY SaaS platform for real-time cold-chain tracking and later won a 2025 IoT platform award. RFID and NFC are also progressing in regulated use cases, with a Michigan State pilot reporting full traceability across a simulated pharmaceutical supply chain using GS1 interoperability standards in June 2025. AI computer vision is scaling alongside these carriers, with Cognex positioning its In-Sight 8900 series for code inspection and audit-trail needs in regulated manufacturing.

Geography Analysis

The market was led by North America with 38.2% revenue share in 2025. The region's lead came from the most mature pharmaceutical serialization regime, where DSCSA created a long procurement cycle across manufacturers, distributors, and dispensers. In the AI in track and trace solutions market, North American buyers are now moving beyond basic compliance toward optimization uses such as predictive analytics, agentic orchestration, and broader enterprise visibility. FDA's Office of Compliance completed more than 50 DSCSA surveillance inspections in FY 2025 and kept enforcement pressure visible, which supports continued spending after go-live.

The market is expanding fastest in Asia-Pacific at 26.4% CAGR through 2031. The region benefits from staggered policy maturity across China, India, Japan, South Korea, Thailand, and Indonesia, because overlapping compliance cycles create repeated purchase windows rather than one single wave. India's February 2025 move to consolidate pharmaceutical export traceability under CDSCO simplified the compliance path and strengthened demand for GS1-aligned platforms. China's NMPA drug traceability system is also supporting demand for exception management and EPCIS-compatible deployments in a very large manufacturing base. In the AI in track and trace solutions market, greenfield pharmaceutical investment in Southeast Asia gives some suppliers a clean starting point without the legacy retrofit burden seen in older markets.

The market also holds a significant position in Europe, where EU FMD maturity remains high and compliance rates in major markets exceeded 95% in 2025. The more important next step is the Digital Product Passport under ESPR, which starts with batteries in February 2027 and then extends to other categories through delegated acts planned for 2026 and 2027. This creates a new buying cycle across consumer goods, electronics, and industrial manufacturers that did not previously need full serialization stacks. OPTEL's February 2026 partnership with Techno Service for Egyptian Drug Authority compliance also shows how the Middle East and Africa are building national traceability systems, while Brazil and Saudi Arabia remain active emerging pockets outside the main European core.

- ACG Worldwide

- Antares Vision Group

- Avery Dennison

- Axway

- Cognex

- Honeywell

- Kezzler

- Korber Pharma

- Laetus

- Mettler-Toledo

- OPTEL Group

- SAP

- SATO Holdings

- SEA Vision

- Siemens Healthineers

- Systech

- TraceLink

- Zebra Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global Serialization and Traceability Mandates

- 4.2.2 Counterfeit, Diversion, and Recall-Risk Pressure

- 4.2.3 Shift From Compliance to Cloud Visibility and Analytics

- 4.2.4 RFID, 2D Code, and Machine-Vision Upgrades

- 4.2.5 GS1 Sunrise 2027 and 2D Barcode Migration

- 4.2.6 Digital Product Passport Expansion Beyond Pharma

- 4.3 Market Restraints

- 4.3.1 High Implementation and Validation Costs

- 4.3.2 Fragmented Standards and Legacy-System Interoperability

- 4.3.3 DSCSA and FSMA Data-Quality / Partner-Readiness Gaps

- 4.3.4 Cybersecurity and Data-Governance Burden for Shared Event Networks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 AI Software Platforms

- 5.1.2 Hardware and Edge Capture Systems

- 5.1.3 Services

- 5.2 By Technology / Data Carrier

- 5.2.1 2D Barcodes and DataMatrix

- 5.2.2 RFID and NFC

- 5.2.3 AI Computer Vision, OCR, and OCV

- 5.2.4 IoT Sensors and Environmental Monitoring

- 5.2.5 EPCIS, Event Repositories, and Blockchain

- 5.3 By Application / Workflow

- 5.3.1 Serialization

- 5.3.2 Aggregation

- 5.3.3 Verification and Authentication

- 5.3.4 Compliance Reporting and Recall Management

- 5.3.5 Supply-Chain Visibility and Exception Management

- 5.4 By End-use Industry

- 5.4.1 Pharmaceuticals and Biopharmaceuticals

- 5.4.2 Medical Devices

- 5.4.3 Consumer Goods and Cosmetics

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 ACG

- 6.3.2 Antares Vision Group

- 6.3.3 Avery Dennison

- 6.3.4 Axway

- 6.3.5 Cognex

- 6.3.6 Honeywell

- 6.3.7 Kezzler

- 6.3.8 Korber Pharma

- 6.3.9 Laetus

- 6.3.10 Mettler-Toledo

- 6.3.11 OPTEL Group

- 6.3.12 SAP

- 6.3.13 SATO Holdings

- 6.3.14 SEA Vision

- 6.3.15 Siemens

- 6.3.16 Systech

- 6.3.17 TraceLink Inc.

- 6.3.18 Zebra Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment