|

시장보고서

상품코드

2063984

병원 재고 관리 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Hospital Inventory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

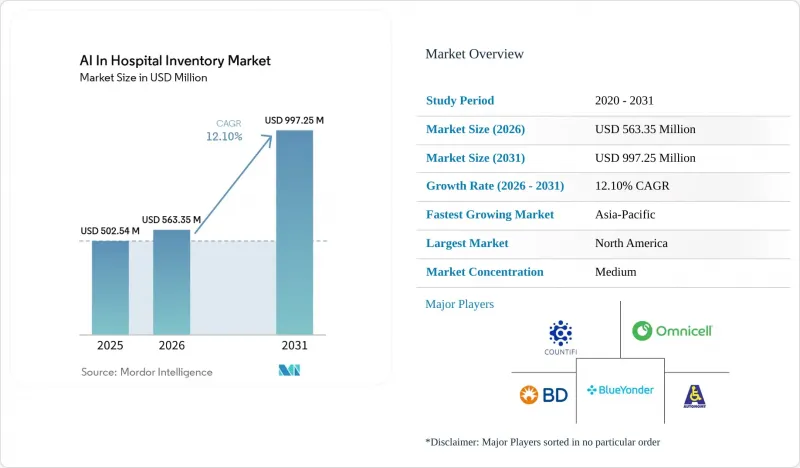

Mordor Intelligence에 의하면, 병원 재고 관리 AI 시장 규모는 2025년에 5억 254만 달러로 평가되었고, 2026년에 5억 6,335만 달러로 추정되며, 2031년까지 9억 9,725만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 12.10%로 성장할 것으로 전망됩니다.

본 보고서는 컴포넌트별(소프트웨어, 하드웨어, 서비스), 도입 모델별(클라우드 기반, 온프레미스형, 하이브리드형), 재고 유형별(의약품, 의료용품 등), 기술별(RFID, 바코드, AI/ML, 컴퓨터 비전, IoT 캐비닛), 병원 구역별(약국, 수술실, 간호, 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계의 병원 재고 관리 AI 시장 동향 및 인사이트

추적성 및 리콜 규정 준수 자동화

추적성은 규정 준수를 중시하는 노력에서 출발하여, 병원 재고 관리 AI 시장에서 중요한 운영 요건으로 자리 잡았습니다. FDA의 UDI 지침 등 규제 체계에 따라, 병원들은 임상 현장 전반에 걸쳐 의료기기의 품목별 가시성을 높일 것을 요구받고 있습니다. 또한, 상호 운용 가능한 데이터 표준에 UDI를 광범위하게 통합함에 따라, 스캔된 제품 데이터를 임상 기록 및 재고 기록과 연동해야 할 필요성이 더욱 커지고 있습니다. 그 결과, 병원 재고 관리 AI 시장에서는 규정 준수 추적을 넘어서는 시스템에 대한 수요가 증가하고 있습니다. 현재 병원들은 UDI 확보를 재고 보충, 리콜 관리, 청구 정확성 및 실시간 재고 가시성과 통합하는 AI 솔루션을 필요로 하고 있습니다.

폐기물 감축 및 재고 부족 방지 요청

병원들이 이익률 확보와 서비스 지속성 유지라는 압박에 직면한 가운데, 폐기물 감축 및 재고 부족 방지를 위한 노력은 병원 재고 관리 AI 시장 성장에 중요한 요인으로 작용하고 있습니다. 조사에 따르면, AI를 활용한 의약품 수요 예측은 단기간 내에 재고 부족 발생을 대폭 줄이고, 보유 비용을 절감할 수 있음이 입증되었습니다. 공공 조달 동향도 이러한 변화를 반영하고 있으며, 병원들은 높은 서비스율과 물류 비용의 대폭적인 절감을 실현하는 AI 재고 관리 솔루션을 도입하고 있습니다.

ERP/EHR/MMIS 통합에 따른 부담

통합은 AI를 활용한 병원 재고 관리 시장에서 여전히 중요한 과제입니다. 많은 병원에서는 클라우드 네이티브 데이터 교환이나 실시간 AI 워크플로우와의 호환성이 부족한 구식 ERP, EHR, 자재 관리 시스템을 여전히 사용하고 있습니다. Infor는 마스터 데이터 구조의 불일치로 인해 약제부, 수술실, 간호용품 공급 거점 간에 데이터를 통합하는 것이 어렵다고 지적하고 있습니다. 또한, UDI(의료기기 고유 식별자) 통합을 지원하기 위해서는 자원이 풍부한 조직이라 하더라도 막대한 비용과 오랜 시간이 소요되는 경우가 많습니다. 이러한 요인들로 인해 도입이 지연되고, 비용이 증가하며, 초기 활용 사례가 제한되고 있습니다.

부문별 분석

2025년, 병원 재고 관리 AI 부문에서는 기존 EHR, ERP 및 약국 시스템과의 통합 능력을 바탕으로 소프트웨어가 42.50%의 점유율을 차지했으며, 시장을 주도했습니다. 병원들은 하드웨어 투자에 앞서, 조직 전체의 가시화와 수요 예측을 실현하기 위해 소프트웨어 도입을 우선적으로 추진하고 있습니다. 옴니셀(Omnicell)의 ‘OmniSphere’는 클라우드 네이티브 플랫폼을 통해 로봇 기술, 스마트 기기, 워크플로우를 통합함으로써 이러한 추세를 구현하고 있습니다. 병원이 최적화나 업데이트를 공급업체에 의존하게 됨에 따라 서비스의 중요성이 커지고 있습니다. 2026년부터 2031년까지 연평균 성장률(CAGR) 12.88%로 성장할 하드웨어는 예측 계층에 필수적인 실시간 데이터를 생성하는 데 있어 매우 중요하며, 소프트웨어의 기반적인 역할을 보완하고 있습니다.

2025년에는 온프레미스 도입이 55.55%의 점유율을 차지한 것으로 평가되었으며, 이는 병원이 데이터 및 시스템에 대한 접근을 직접 관리하는 것을 선호하는 경향을 반영하고 있습니다. 이 모델은 데이터의 기밀성과 레거시 인프라의 존재로 인해 대학병원이나 정부 산하 병원 등에서 여전히 확고한 지지를 받고 있습니다. 2026-2031년 연평균 성장률(CAGR) 12.90%를 나타낼 것으로 예측되는 클라우드 기반 솔루션은 인프라 중복을 피하면서도 전사적인 가시성을 추구하는 여러 병원 시스템에서 지지를 넓혀가고 있습니다. 클라우드 아키텍처는 통합된 업데이트 및 분석을 가능하게 하여 도입을 촉진하고 있습니다. 그러나 클라우드 도입 속도는 데이터 거버넌스 및 통합과 관련된 과제의 해결 여부에 달려 있습니다.

지역별 분석

2025년, 북미는 병원 재고 관리 AI 시장에서 39.67%의 점유율을 차지했습니다. 이는 엄격한 규제, 성숙한 유통망, 그리고 병원의 막대한 기술 투자가 뒷받침된 결과입니다. DSCSA 시행, FDA의 UDI 의무화, 340B 감사 요건 등의 정책으로 인해 병원들은 추적 가능하고 감사 가능한 재고 관리 시스템의 도입을 요구받고 있습니다. 이를 통해 북미는 약국, 수술실, 공급망 전반에 걸친 워크플로우에 걸쳐 엔터프라이즈 솔루션을 구축하는 선도 기업으로서의 입지를 확고히 하고 있습니다.

유럽은 규제가 도입을 촉진하는 한편 구현 요건도 높아지고 있어, 병원 재고 관리 AI 시장에서 여전히 중요한 역할을 하고 있습니다. EU MDR 2017/745는 의료기기의 추적성을 강화하고 있으며, EU AI법 및 GDPR(EU 개인정보보호규정)은 더욱 엄격한 거버넌스 및 데이터 요건을 부과하고 있습니다. 독일이 이 분야를 선도하고 있으며, 병원에서는 AI를 활용한 수요 계획과 수술실 일정 관리, 물류를 통합함으로써 수요의 일관성을 확보하고, 벤더 솔루션에 대한 기대감을 높이고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 중국, 일본, 한국, 인도 등 각국의 병원 디지털화가 급속히 진행됨에 힘입어 2026-2031년 연평균 성장률(CAGR) 14.15%를 나타낼 것으로 전망됩니다. 중국의 국가위생건강위원회는 HIS(병원 정보 시스템), SPD(수술실 공급) 공급망 플랫폼 및 운영 데이터 시스템의 통합을 추진하고 있는 반면, 일본은 디지털화 및 AI 보조금 프로그램을 통해 도입을 촉진하고 있습니다. 시장은 북미가 주도하던 기반에서 아시아태평양 지역이 성장을 주도하는 보다 균형 잡힌 세계 구조로 전환되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the aI in hospital inventory market size is projected to be USD 502.54 million in 2025, USD 563.35 million in 2026, and reach USD 997.25 million by 2031, growing at a CAGR of 12.10% from 2026 to 2031.

This report is Segmented by Component (Software, Hardware, Services), Deployment Model (Cloud-Based, On-Premises, Hybrid), Inventory Type (Pharmaceuticals, Medical Supplies, Iand More), Technology (RFID, Barcode, AI/ML, Computer Vision, Iot Cabinets), Hospital Area (Pharmacy, OR, Nursing, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global AI In Hospital Inventory Market Trends and Insights

Traceability and Recall Compliance Automation

Traceability has transitioned from being a compliance-focused initiative to a critical operational requirement in the AI-driven hospital inventory management market. Regulatory frameworks, such as the FDA's UDI guidelines, have driven hospitals to enhance item-level visibility for devices across clinical settings. Additionally, broader UDI integration into interoperable data standards has strengthened the need to link scanned product data with clinical and inventory records. As a result, the AI in the hospital inventory management market is experiencing increased demand for systems that go beyond compliance tracking. Hospitals now seek AI solutions that integrate UDI capture with replenishment, recall management, billing accuracy, and real-time stock visibility.

Waste and Stockout Reduction Mandates

Efforts to reduce waste and prevent stockouts have become significant growth drivers for the AI in hospital inventory management market, as hospitals face mounting pressure to protect margins and maintain service continuity. Studies have demonstrated that AI-driven pharmaceutical demand forecasting can significantly reduce stockout incidents and lower holding costs within a short period. Public procurement trends also reflect this shift, with hospitals adopting AI inventory solutions that deliver high service rates and substantial logistics cost reductions.

ERP / EHR / MMIS Integration Burden

Integration remains a key challenge in the AI-driven hospital inventory management market. Many hospitals still use outdated ERP, EHR, and materials management systems that lack compatibility with cloud-native data exchanges and real-time AI workflows. Infor highlights difficulties in unifying data across pharmacy, operating room, and nursing supply points due to inconsistent master data structures. Additionally, supporting UDI integration is often costly and time-intensive, even for well-resourced organizations. These factors lead to slower deployments, higher costs, and limited initial use cases.

Other drivers and restraints analyzed in the detailed report include:

- Clinician Time Recovery from Manual Inventory Work

- Growing Adoption of Smart Hospitals and Digital Healthcare

- Cybersecurity and Interoperability Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software led the AI in hospital inventory management market with a 42.50% share, driven by its ability to integrate with existing EHR, ERP, and pharmacy systems. Hospitals prioritize software-first deployments for enterprise visibility and forecasting before investing in hardware. Omnicell's OmniSphere exemplifies this trend by integrating robotics, smart devices, and workflows through a cloud-native platform. Services are gaining importance as hospitals rely on vendors for optimization and updates. Hardware, growing at 12.88% CAGR from 2026 to 2031, is critical for generating live data essential for predictive layers, complementing software's foundational role.

On-premises deployment held a 55.55% share in 2025, reflecting hospitals' preference for direct control over data and system access. This model remains strong in academic and government systems due to data sensitivity and legacy infrastructure. Cloud-based solutions, growing at 12.90% CAGR from 2026 to 2031, are gaining traction as multi-hospital systems seek enterprise-wide visibility without duplicating infrastructure. Cloud architecture enables centralized updates and analytics, driving adoption. However, the pace of cloud adoption depends on resolving data governance and integration challenges.

Geography Analysis

In 2025, North America held a 39.67% share of the AI-driven hospital inventory management market, driven by stringent regulations, mature distributor networks, and significant hospital technology investments. Policies such as DSCSA enforcement, FDA's UDI mandates, and 340B audit requirements have pushed hospitals to adopt traceable and auditable inventory systems. This has positioned North America as a leader in deploying enterprise solutions across pharmacies, operating rooms, and supply chain workflows.

Europe remains a key player in the AI-driven hospital inventory management market, with regulations driving adoption while increasing implementation demands. The EU MDR 2017/745 enhances device traceability, while the EU AI Act and GDPR impose stricter governance and data requirements. Germany leads the region, with hospitals integrating AI-driven demand planning with operating room scheduling and logistics, creating consistent demand and higher expectations for vendor solutions.

Asia-Pacific is the fastest-growing region, with a 14.15% CAGR projected for 2026-2031, supported by rapid hospital digitalization in countries like China, Japan, South Korea, and India. China's National Health Commission is advancing the integration of HIS, SPD supply chain platforms, and operational data systems, while Japan promotes adoption through digitalization and AI subsidy programs. The market is transitioning from a North America-led base to a more balanced global structure, with Asia-Pacific driving growth.

- Autonomi

- Beckton Dickinson

- Blue Yonder Group, Inc.

- Cardinal Health

- Clarium

- Countifi

- DARVIS

- GHX

- IDENTI Medical

- Infor

- Jump Technologies

- Mckesson

- Mobile Aspects

- Omnicell

- Oracle

- SAP

- SmartPAR

- Tecsys

- Terso Solutions

- Zebra Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Traceability and Recall Compliance Automation

- 4.2.2 Waste and Stockout Reduction Mandates

- 4.2.3 Clinician Time Recovery from Manual Inventory Work

- 4.2.4 OR Consignment and Bill-Only Capture Blind Spots

- 4.2.5 Growing Adoption of Smart Hospitals and Digital Healthcare Infrastructure

- 4.2.6 Drug-Shortage Substitute Orchestration

- 4.3 Market Restraints

- 4.3.1 ERP / EHR / MMIS Integration Burden

- 4.3.2 Cybersecurity and Interoperability Concerns

- 4.3.3 Resistance to Technology Adoption Among the Hospital Staff

- 4.3.4 Poor Item-Master and UDI Data Quality

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Inventory Type Managed

- 5.3.1 Pharmaceuticals

- 5.3.2 Medical Supplies & Consumables

- 5.3.3 Implants & High-Value Devices

- 5.3.4 Tissues & Biologics

- 5.3.5 Laboratory Supplies

- 5.4 By Technology

- 5.4.1 RFID-Enabled Inventory Systems

- 5.4.2 Barcode & Mobile Scanning

- 5.4.3 AI/ML Predictive Inventory Systems

- 5.4.4 Computer Vision / Image Recognition

- 5.4.5 IoT Smart Cabinets / Smart Shelves

- 5.5 By Hospital Area of Use

- 5.5.1 Central Pharmacy

- 5.5.2 Operating Rooms & Procedural Areas

- 5.5.3 Nursing Units / Floor Stock

- 5.5.4 Cath Lab / Interventional Radiology / Electrophysiology Labs

- 5.5.5 Central Supply / Warehouse

- 5.5.6 Laboratories

- 5.5.7 Emergency Department

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Autonomi

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Blue Yonder Group, Inc.

- 6.3.4 Cardinal Health Inc.

- 6.3.5 Clarium

- 6.3.6 Countifi

- 6.3.7 DARVIS

- 6.3.8 GHX

- 6.3.9 IDENTI Medical

- 6.3.10 Infor

- 6.3.11 Jump Technologies

- 6.3.12 McKesson Corporation

- 6.3.13 Mobile Aspects

- 6.3.14 Omnicell

- 6.3.15 Oracle

- 6.3.16 SAP

- 6.3.17 SmartPAR

- 6.3.18 Tecsys

- 6.3.19 Terso Solutions

- 6.3.20 Zebra Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment