|

시장보고서

상품코드

2063962

남미의 통합 시설 관리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

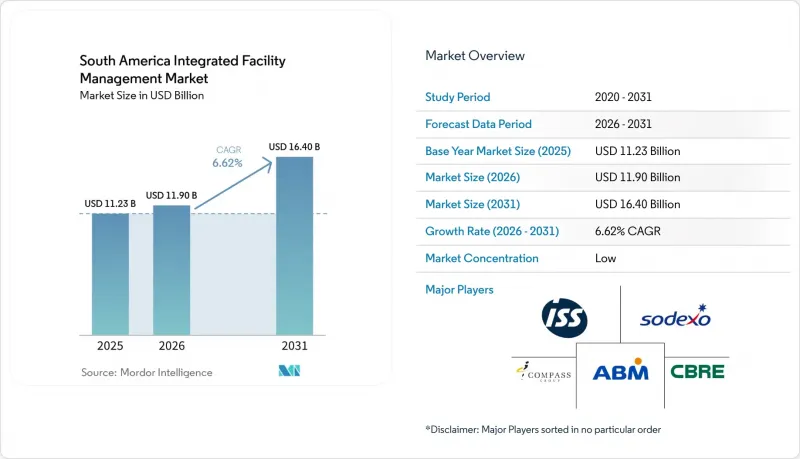

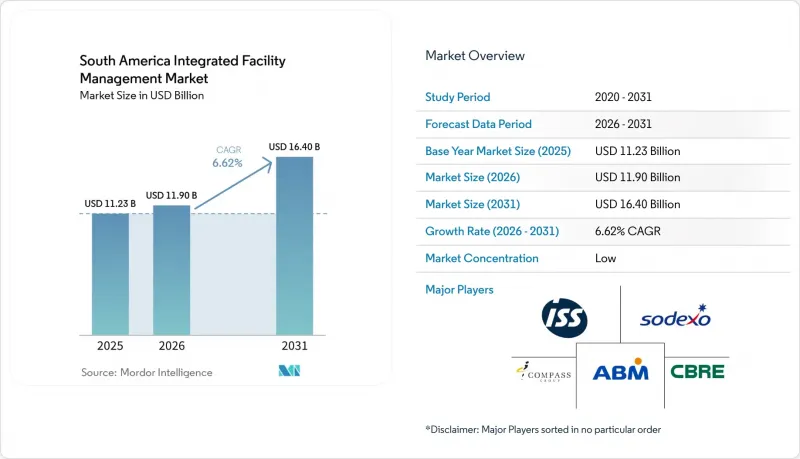

Mordor Intelligence에 의하면, 남미의 통합 시설 관리 시장 규모는 2025년에 112억 3,000만 달러로 평가되었고, 2026년 119억 달러로 추정되고, 2031년까지 164억 달러에 이를 것으로 예측되며, 2026-2031년 예측 기간 CAGR은 6.62%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(하드 시설 관리(자산 관리, MEP 및 HVAC 서비스 등), 소프트 시설 관리(사무 지원 및 보안, 청소 서비스, 케이터링 서비스 등)), 최종 사용자별(상업, 의료, 산업 및 공정 부문 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

남미의 통합 시설 관리 시장 동향과 인사이트

스마트 빌딩 플랫폼 도입 확대

스마트 빌딩의 도입은 통합형 계약에서 단기 수요의 가장 큰 요인으로 계속해서 자리 잡고 있습니다. 이는 운영 사업자가 정해진 유지보수 일정에만 의존하기보다는 입주 현황, HVAC, 조명 및 출입 관리 시스템을 매일의 서비스 제공 결정에 반영하려는 경향이 강해지고 있기 때문입니다. 브라질의 EPE는 상업시설 및 공공 건축물에서 전력 소비의 상당 부분을 HVAC와 조명이 차지하고 있다고 보고하고 있으며, 이는 건물 소유주에게 건물 시스템을 성과 중심의 FM 모델과 연계해야 할 명확한 비용상의 근거가 됩니다. Aureside사의 보고서에 따르면, 브라질의 신규 상업용 건축물 중 상당수가 이미 어느 정도의 자동화 시스템을 도입하고 있으며, 이는 리모델링 수요를 고려하기 전부터 플랫폼 연동형 IFM 계약의 대상이 될 수 있는 도입 기반이 확대되고 있음을 의미합니다. 더 큰 기회는 여전히 오래된 상업용 부동산에 있으며, 이곳에서는 진정한 단일 관리 계층이 구현되기 전에 기존의 개별 솔루션을 대체하거나 통합해야 합니다. 이러한 미처리 건들이 남미(SA)의 통합 시설 관리 시장에서 수년에 걸친 계약 파이프라인을 뒷받침하고 있습니다. 또한, 브라질의 기술 기준과 에너지 라벨 제도 역시 소유주에게 보다 체계적인 건물 관리 방식을 장려하고 있으며, 이에 따라 MEP 시스템과 디지털 제어를 통합적으로 관리할 수 있는 서비스 제공업체의 서비스 범위가 확대되고 있습니다. 따라서 이미 통합 대시보드나 원격 모니터링 도구를 운영하고 있는 서비스 제공업체들은 남미 IFM 시장 전체에서 자동화에 대한 투자를 장기적인 지속 계약으로 전환하는 데 있어 더 유리한 입장에 있습니다.

에너지 절약 시설에 대한 관심 증가

에너지 효율은 더 이상 단순한 지속가능성 목표로만 여겨지지 않습니다. 왜냐하면, 고객사는 현재 소비 목표, 모니터링 절차 및 운영상 페널티를 서비스 계약에 직접 명시하고 있기 때문입니다. 국제에너지기구(IEA)는 2025년에 건물용 센서와 모니터링 소프트웨어를 통해 상업시설의 에너지 소비를 최대 30%까지 줄일 수 있을 것이라고 발표했습니다. 이를 통해 조달 팀은 통합 FM 계약을 활용하여 기술 투자를 정당화할 수 있는 구체적인 근거를 확보할 수 있습니다. 이러한 변화가 남미에서 중요한 이유는 에너지 성능이 지금까지, 특히 소유주와 입주자가 책임을 분담하는 임대 구조에서 아웃소싱된 시설 서비스의 핵심 범위 밖으로 국한되는 경우가 많았기 때문입니다. 이러한 책임이 서비스 계약으로 이전됨에 따라, FM 제공업체는 자산 자체를 소유하지 않고도 측정 가능한 가치를 제공할 수 있게 되었으며, 이는 남미의 통합 시설 관리 시장에서 비즈니스 사례를 확대되고 있습니다. GBC 브라질은 또한 ESG 지표와 ABNT, ASHRAE 등의 기술 기준이 일상적인 시설 거버넌스의 일부로 자리 잡고 있다고 지적하고 있습니다. 이에 따라 에너지, 실내 환경, 규정 준수 분야의 성과를 단일 운영 체제 하에서 관리할 수 있는 인증을 받은 공급업체에 대한 수요가 증가하고 있습니다. 그 결과, 남미의 통합 시설 관리 시장에서는 노동력 중심의 계약에서 에너지 성능이 가치 제안의 일부가 되는 계약으로의 꾸준한 전환이 진행되고 있습니다.

숙련된 다분야 기술자 부족

이 지역의 노동력 제약은 단순히 유지보수 인력의 부족에만 그치는 것이 아닙니다. 왜냐하면 진정한 부족함은 MEP 시스템, 디지털 제어, 모니터링 도구, 그리고 규정 준수 요건을 동일한 역할로 다룰 수 있는 기술자가 부족하기 때문입니다. GBC 브라질은 2026년 2월, 시설 관리자의 역할이 사후 대응형 운영에서 데이터 주도형 전략적 거버넌스로 전환되었다고 밝히며, 이러한 변화를 일상 업무에서 ABNT, ASHRAE, CRI-204 규격의 활용 확대와 연관지었습니다. 이러한 변화로 인해 제공업체의 교육 부담이 커지고 있습니다. 왜냐하면, 고객은 현재 기술 직원들에게 단순한 물리적 유지보수 작업 수행뿐만 아니라, 건물 데이터 분석, 감사 지원, 성능 시스템 관리까지 기대하고 있기 때문입니다. 이 문제는 대도시권 이외의 지역에서는 더욱 심각합니다. 이러한 지역에서는 이용 가능한 노동력이 부족하고, 여러 거점에 걸친 계약에 필요한 채용에 시간이 걸리기 때문입니다. 이로 인해 2차 시장에서 통합 모델의 도입이 지연되고, 수요가 있더라도 복잡한 프로젝트의 시작 비용이 높아집니다. 실제로 이러한 인력 부족은 통합된 전문 지식, 원격 지원, 현장 실행을 단일 제공 모델로 통합할 수 있는 공급업체에 구조적인 우위를 가져다주고 있습니다.

부문별 분석

2025년, 남미의 통합 시설 관리 시장에서 소프트 시설 관리 서비스는 64.21%의 점유율을 차지했습니다. 이는 청소, 급식, 사무 지원, 보안 서비스가 여전히 대다수의 고객 기업에게 주요 아웃소싱 분야로 자리 잡고 있음을 뒷받침합니다. 청소 서비스는 고도의 기술력이 요구되는 업무에 비해 외부 위탁이 용이하기 때문에 특히 사내 운영에서 벗어나 첫걸음을 내딛는 중소기업에게 여전히 가장 광범위한 도입 기반을 형성하고 있습니다. 이에 따라 소프트 FM은 산업단지, 상업 빌딩, 병원, 교육 시설에 걸쳐 대규모 도입 기반을 갖추고 있으며, 특히 주변 국가들보다 아웃소싱이 더 성숙한 브라질에서 그 추세가 두드러집니다. 또한, 이 카테고리는 일상적인 시설 이용 현황, 직원의 체험, 시설에 대한 인상과 직접적으로 연결되어 있다는 점도 강점으로 작용하고 있어, 예산이 빠듯한 상황에서도 계약 갱신률은 비교적 견조한 추세를 보이고 있습니다. 따라서, 고객들이 서비스 설계에 대해 더욱 선택적인 태도를 보이고 있음에도 불구하고, 소프트 FM은 여전히 남미의 통합 시설 관리(IFM) 시장의 사업 규모를 지탱하는 기반이 되고 있습니다.

또한, 소프트 FM의 구성도 남미 IFM 업계에 있어 중요한 변화를 겪고 있습니다. 고객들은 고정된 업무 절차뿐만 아니라, 유연한 인력 배치, 이용 현황에 따른 일정 수립, 디지털 기술을 통한 서비스 가시화를 점점 더 기대하고 있기 때문입니다. 수요에 따른 청소 및 재실 상황에 연동된 업무 공간 지원은 요일이나 구역에 따라 가동률이 크게 변동하는 사무실이나 복합 시설에서 그 중요성이 점점 더 커지고 있습니다. 케이터링 분야도 마찬가지로 발전하고 있으며, 소덱소 브라질은 2025년에 기업, 병원, 학교, 공장 환경에서 자율형 마이크로마켓의 확대를 추진할 예정입니다. 이는 식품 관련 서비스가 하이브리드 근무나 장시간 근무 운영에 적합한, 편의성을 중시하는 모델로 전환되고 있음을 보여줍니다. 보안 및 사무 지원 분야도 비슷한 추세를 보이고 있으며, 고객들은 여러 거점에 걸친 관리, 보고 및 적응성 향상을 요구하고 있습니다. 이는 남미의 통합 시설 관리 시장에서 소프트 FM이 계속해서 가장 큰 서비스 부문으로 남을 가능성이 높다는 것을 의미합니다. 다만, 그러한 성장의 양상은 단순한 노동력의 규모뿐만 아니라 기술과 계약 설계에 의해 점점 더 형성되고 있습니다.

하드 시설 관리 시장은 2031년까지 연평균 성장률(CAGR) 7.43%로 확대될 것으로 예상되며, 고객들이 자산 가동 시간, 규정 준수 및 기술적 신뢰성에 대한 투자를 늘려감에 따라 남미 통합 시설 관리 시장에서 가장 빠르게 성장하는 분야가 될 전망입니다. 의료시설, 데이터센터, 산업 시설, 광산 자산에서 발생하는 가동 중단은 운영 및 안전 측면에 직접적인 영향을 미치기 때문에 MEP(기계·전기·배관) 및 HVAC(냉난방·공조) 서비스가 수요의 중심을 차지하고 있습니다. 또한, 소방 시스템과 안전 규정 준수 사항도 조달 과정에서 더욱 중요하게 여겨지고 있으며, 지역을 불문하고 공통된 기준을 요구하는 엔지니어나 다국적 입주사들은 2025년판으로 개정된 NFPA 72를 성능 벤치마크로 참고하고 있습니다. 이는 남미에서 중요한 의미를 지닙니다. 왜냐하면 많은 국제적인 임차인들이 북미나 유럽에서 요구하는 것과 동일한 수준의 유지보수 체계를 지역 서비스 제공업체에게도 요구하고 있기 때문입니다. 그 결과, 첨단 엔지니어링, 규정 준수 대응 능력, 모니터링 도구를 결합한 하드 FM 제안이 경쟁 입찰에서 더욱 중요하게 여겨지고 있습니다.

자산 관리가 예방 유지보수의 범위를 넘어 소프트웨어와 원격 데이터를 기반으로 한 장기적인 계획으로 전환됨에 따라, 하드 FM의 기회는 더욱 확대되고 있습니다. 텔레포니카는 상파울루 데이터센터의 냉각 시스템을 최적화하기 위해 AI를 활용한 디지털 트윈을 도입했으며, 이를 통해 15%에서 20%의 에너지 절감 효과가 있을 것으로 추정하고 있습니다. 이는 기술적 FM이 사후 대응적인 수리에서 지속적인 최적화로 전환되고 있음을 보여주는 실제 사례입니다. Leadec사도 2025 회계연도에 북미 및 남미 지역에서 견조한 실적을 보고했으며, 하드 FM 수요와 밀접하게 연동되는 에너지 관리, 배터리 저장, 태양광 발전, 스마트 팩토리 유지보수 활동을 통해 제공되는 ‘Green Factory Solutions’의 매출액이 1억 4,000만 유로(1억 5,800만 달러)에 달했음을 강조했습니다. 이러한 사례들은 남미의 통합 시설 관리 업계가 신뢰성, 에너지 활용도, 수명 주기 성과를 향상시키는 기술 서비스 분야에 더 큰 가치를 부여하고 있음을 보여줍니다. 따라서 남미의 통합 시설 관리 시장에서는 소프트 FM이 여전히 더 큰 수익 기반을 차지하고 있지만, 하드 FM이 가장 강력한 성장세를 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the south america integrated facility management market size was valued at USD 11.23 billion in 2025 and estimated to grow from USD 11.90 billion in 2026 to reach USD 16.40 billion by 2031, at a CAGR of 6.62% during the forecast period 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Healthcare, Industrial and Process Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Integrated Facility Management Market Trends and Insights

Increasing Adoption Of Smart-Building Platforms

Smart-building adoption remains the strongest near-term demand trigger for integrated contracts because operators are increasingly connecting occupancy, HVAC, lighting, and access systems to daily service delivery decisions rather than relying on fixed maintenance calendars. Brazil's EPE reported that HVAC and lighting represented a significant portion of electricity consumption in commercial and public buildings, which gives owners a clear cost reason to connect building systems with performance-led FM models. Aureside also reported that a substantial number of new commercial constructions in Brazil already include some level of automation, which means the installed base available for platform-linked IFM contracts is expanding even before retrofit demand is considered. The larger opportunity still sits in older commercial stock, where legacy point solutions need replacement or integration before a true single management layer becomes practical, and that backlog supports a multi-year contract pipeline for the SA integrated facility management market. Technical standards and energy-labeling programs in Brazil are also pushing owners toward more structured building management approaches, which broadens the service scope for providers that can manage MEP systems and digital controls together. Providers that already operate with integrated dashboards and remote visibility tools are therefore in a better position to convert automation spending into long-term recurring contracts across the South America IFM market.

Growing Emphasis On Energy-Efficient Facilities

Energy efficiency is no longer being treated only as a sustainability objective, because clients are now placing consumption targets, monitoring routines, and operating penalties directly into service agreements. The IEA stated in 2025 that building sensors and monitoring software can reduce commercial energy consumption by up to 30%, which gives procurement teams a concrete basis for using integrated FM contracts to justify technology spending. That change matters in South America because energy performance had often remained outside the core scope of outsourced facility services, especially in lease structures where owners and occupiers split responsibility. As those responsibilities move into the service contract, FM providers can add measurable value without owning the asset itself, and that is expanding the commercial case for the South America integrated facility management market. GBC Brasil also noted that ESG metrics and technical standards such as ABNT and ASHRAE are becoming part of day-to-day facilities governance, which raises the need for credentialed vendors that can manage energy, indoor environment, and compliance outcomes in one operating structure. The result is a steadier shift from labor-led contracts toward contracts where energy performance becomes part of the value proposition in the South America integrated facility management market.

Shortage Of Skilled Multidisciplinary Technicians

The regional labor constraint is not simply a shortage of maintenance workers, because the real gap lies in technicians who can handle MEP systems, digital controls, monitoring tools, and compliance requirements in the same role. GBC Brasil stated in February 2026 that the facility manager role had shifted from reactive operations toward data-led strategic governance, and it linked that change to rising use of ABNT, ASHRAE, and CRI-204 standards in daily practice. That shift increases the training burden for providers because clients now expect technical staff to interpret building data, support audits, and manage performance systems rather than only execute physical maintenance tasks. The problem is more acute outside the largest urban centers, where the available labor pool is smaller and recruitment for multi-site contracts takes longer. This slows the rollout of integrated models in secondary markets and raises the cost of ramping complex accounts even when demand is present. In practice, the talent gap gives a structural advantage to vendors that can combine centralized expertise, remote support, and field execution in one delivery model.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Hybrid Work Models Demanding Flexible IFM

- Rising Private-Equity Investments in FM Service Vendors

- Fragmented Local Vendor Landscape Limiting Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management services held 64.21% of the South America integrated facility management market share in 2025, which confirms that cleaning, catering, office support, and security remained the main outsourcing entry points for most client organizations. Cleaning services continue to form the broadest adoption base because they are easier to contract out than highly technical functions, especially for small and medium-sized firms taking their first step away from in-house operations. That gives soft FM a large installed base across industrial parks, commercial buildings, hospitals, and education sites, particularly in Brazil where outsourcing has matured further than in many neighboring countries. The category also benefits from its direct link to day-to-day occupancy, employee experience, and site presentation, which keeps renewal rates relatively resilient even when budgets tighten. For that reason, soft FM still anchors the operating scale of the South America integrated facility management market even as clients become more selective about service design.

The soft facility management mix is also changing in ways that matter for the South America IFM industry, because clients increasingly expect flexible staffing, usage-based scheduling, and digitally supported service visibility rather than fixed routines alone. Demand-led cleaning and attendance-linked workplace support are becoming more relevant in offices and mixed-use sites where occupancy changes materially by day and by zone. Catering is evolving as well, with Sodexo Brazil expanding autonomous micromarket formats across corporate, hospital, school, and factory environments in 2025, which shows how food-related services are moving toward convenience-led models that fit hybrid work and extended shift operations. Security and office support are following a similar path, where clients want better control, reporting, and adaptability across multiple locations. This means soft FM is likely to remain the largest service layer in the South America integrated facility management market, even though its growth profile is increasingly shaped by technology and contract design rather than labor scale alone.

Hard Facility Management is projected to expand at a CAGR of 7.43% through 2031, making it the fastest-growing part of the SA integrated facility management market size as clients spend more on asset uptime, compliance, and technical reliability. MEP and HVAC services sit at the center of that demand because downtime in healthcare facilities, data centers, industrial sites, and mining assets carries direct operating and safety consequences. Fire systems and safety compliance are also becoming more visible in procurement, and the 2025 edition updates to NFPA 72 are being referenced as a performance benchmark by engineers and multinational occupiers that expect common standards across geographies. That matters in South America because many international tenants want the same maintenance discipline from regional service providers that they require in North America or Europe. As a result, hard FM proposals that combine engineering depth, compliance capability, and monitoring tools are gaining more weight in competitive bids.

The hard FM opportunity is widening further because asset management is moving beyond preventive maintenance into longer-term planning supported by software and remote data. Telefonica is deploying AI-powered digital twins for cooling optimization at its Sao Paulo data centers and estimated potential energy reductions of 15% to 20%, which gives a practical example of how technical FM is moving into continuous optimization rather than reactive repair. Leadec also reported strong performance in the Americas in FY2025 and highlighted Green Factory Solutions revenue of EUR 140 million (USD 158 million) from energy management, battery storage, photovoltaic, and smart factory maintenance activities that align closely with hard FM demand. These examples show that the South America integrated facility management industry is assigning greater value to technical service lines that improve reliability, energy use, and life-cycle outcomes. Hard FM therefore has the strongest forward momentum even though soft FM continues to hold the larger revenue base in the South America integrated facility management market.

List of Companies Covered in this Report:

- Leadec Brasil

- ISS A/S

- Sodexo S.A.

- Compass Group PLC

- Grupo Eulen S.A.

- GDI Integrated Facility Services Inc.

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated (JLL)

- Cushman & Wakefield PLC

- Aramark Corporation

- Apleona GmbH

- OCS Group Ltd.

- Mitie Group PLC

- Manserv Facilities

- Grupo Verzani & Sandrini S/A

- Brasanitas Servicos Integrados

- Allonda Ambiental S.A.

- Grupo GPS Participacoes e Empreendimentos S.A.

- Quifel Holdings S.A. (Ecotrade)

- Engie SA (IFM Division)

- Veolia Environnement S.A. (FM Division)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Smart-Building Platforms

- 4.2.2 Growing Emphasis on Energy-Efficient Facilities

- 4.2.3 Post-Pandemic Hybrid Work Models Demanding Flexible IFM

- 4.2.4 Rising Private-Equity Investments in FM Service Vendors

- 4.2.5 Accelerated Digital Twin Deployments for Asset Optimization

- 4.2.6 Government-Backed Infrastructure Modernization Programs

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Multidisciplinary Technicians

- 4.3.2 Fragmented Local Vendor Landscape Limiting Standardization

- 4.3.3 Currency Volatility Inflating Service Contract Costs

- 4.3.4 Low End-User Awareness Outside Tier-1 Cities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial (BFSI, IT and telecom, retail and warehouses)

- 5.2.2 Hospitality (eateries, restaurants and large-scale hotels)

- 5.2.3 Institutional and Public Infrastructure (government, education, airports, railways)

- 5.2.4 Healthcare (public and private facilities)

- 5.2.5 Industrial and Process Sector (manufacturing, energy, mining)

- 5.2.6 Other End-User Industries (multi-house residential, entertainment, sports and leisure)

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Leadec Brasil

- 6.4.2 ISS A/S

- 6.4.3 Sodexo S.A.

- 6.4.4 Compass Group PLC

- 6.4.5 Grupo Eulen S.A.

- 6.4.6 GDI Integrated Facility Services Inc.

- 6.4.7 CBRE Group Inc.

- 6.4.8 Jones Lang LaSalle Incorporated (JLL)

- 6.4.9 Cushman & Wakefield PLC

- 6.4.10 Aramark Corporation

- 6.4.11 Apleona GmbH

- 6.4.12 OCS Group Ltd.

- 6.4.13 Mitie Group PLC

- 6.4.14 Manserv Facilities

- 6.4.15 Grupo Verzani & Sandrini S/A

- 6.4.16 Brasanitas Servicos Integrados

- 6.4.17 Allonda Ambiental S.A.

- 6.4.18 Grupo GPS Participacoes e Empreendimentos S.A.

- 6.4.19 Quifel Holdings S.A. (Ecotrade)

- 6.4.20 Engie SA (IFM Division)

- 6.4.21 Veolia Environnement S.A. (FM Division)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment