|

시장보고서

상품코드

2063966

컨텐츠 제작 툴 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Content Authoring Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

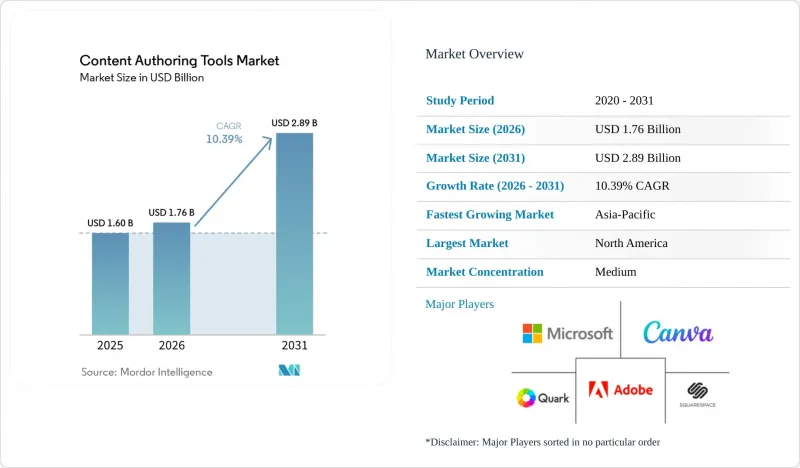

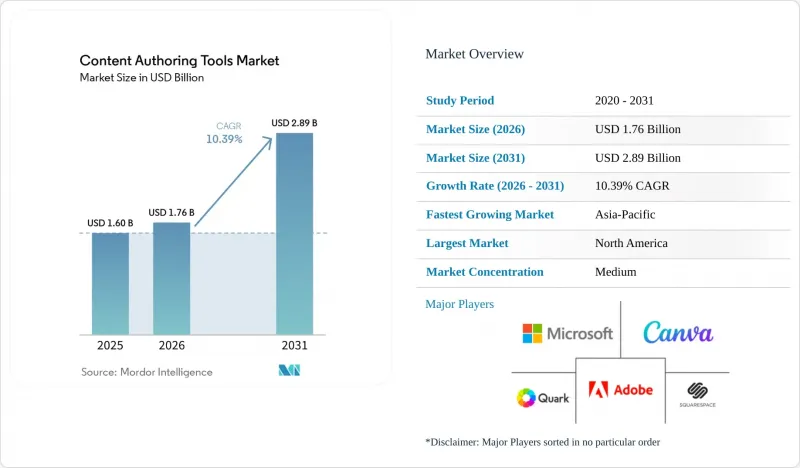

Mordor Intelligence에 의하면, 컨텐츠 제작 툴 시장 규모는 2025년 16억 달러, 2026년 17억 6,000만 달러에서 2031년까지 28억 9,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.39%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어/툴 및 서비스), 도입 모델(On-Premise, 클라우드 및 하이브리드), 조직 규모(중소기업 및 대기업), 최종 사용자 산업 분야(미디어 및 엔터테인먼트, e-러닝·교육, 마케팅 및 광고 대행사, 정부·공공 부문, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 컨텐츠 제작 툴 시장 동향 및 인사이트

생성형 AI를 활용한 저작 기능 강화

어도비는 2025년 10월, Creative Cloud에 Gemini, Veo, Imagen 모델을 통합하여 기존 워크플로우 내에서 텍스트를 기반으로 동영상을 생성하고 지능형 태그를 지정할 수 있게 했습니다. 마이크로소프트는 2025년에 Office 365 전체에 Copilot을 도입하여 슬라이드 자료, 문서 요약, 이메일 제작을 자동화했습니다. 파일럿 프로그램 보고서에 따르면, 이를 통해 제작 시간이 30% 단축되었다고 합니다. Canva는 2024년부터 2026년까지 Leonardo.ai, MangoAI, Cavalry, Simtheory, Ortto를 인수하며, AI의 비약적인 발전을 바탕으로 2026년 초까지 프리미엄 구독자 수를 40% 증가시켰습니다. 그 결과, 신뢰성이 높은 생성형 AI 도입이 지연되고 있는 플랫폼은 고객이 공급업체를 통합할 때 가격 압박에 직면할 위험이 있습니다. 규제 동향은 여전히 유동적이기 때문에 컨텐츠 출처 추적 툴와 상세한 모델 설정 기능을 제공하는 업체는 규제 대상 구매자에게 경쟁 우위를 확보할 수 있습니다.

동영상 기반 이러닝 컨텐츠에 대한 수요 증가

여러 LMS 제공업체에 따르면, 텍스트만 포함된 모듈에 비해 수료율이 75% 더 높기 때문에 기업의 교육 팀은 점점 더 동영상을 선택하고 있습니다. X-Pilot은 2024년 1월에 1,800만 달러를 조달했으며, 후원사가 코스 개발 속도가 50% 빨라졌다고 밝힌 데 힘입어 18개월 이내에 엔터프라이즈 라이선스 수를 3배로 늘렸습니다. Synthesia는 고가의 스튜디오 촬영을 대체할 수 있는 다국어 지원 AI 아바타 덕분에 2025년까지 포춘 100대 기업의 절반을 포함한 1,000개의 기업 고객을 확보했습니다. 이러한 변화로 인해 기존의 이러닝 제작 업체들은 네이티브 동영상 기능을 통합하지 않으면 전문 플랫폼에 시장을 빼앗길 위험에 직면해 있습니다. 제작이 조잡한 AI 동영상은 학습자의 신뢰를 떨어뜨릴 수 있으므로, 속도와 대본의 질 사이의 균형을 유지하는 것이 여전히 중요합니다.

엔터프라이즈용 플랫폼의 높은 총소유비용

Adobe Experience Manager의 연간 라이선스 비용은 종종 20만 달러에서 50만 달러에 달하며, 전문 서비스 비용도 비슷한 수준이 들기 때문에 예산은 당초 견적보다 40%에서 60% 정도 초과하게 됩니다. Sitecore 도입의 경우, 인프라 및 맞춤 설정을 고려하면 첫해에 100만 달러를 초과하는 경우도 있습니다. 벤더들이 영구 라이선스를 폐지하는 가운데, 구독 갱신 비용은 예산 증가율을 상회할 가능성이 있어, 구매자들은 참여도 향상으로 직결되는 투명성이 높은 비용 산정 툴와 ROI 지표를 요구하고 있습니다.

부문별 분석

2025년 기준으로 소프트웨어 및 툴는 컨텐츠 제작 툴 시장의 76.74%를 차지했으나, 전문 서비스 및 관리형 서비스는 2031년까지 연평균 성장률(CAGR) 11.48%를 기록하며 컨텐츠 제작 툴 시장 전체를 상회하는 성장세를 보일 것으로 전망됩니다. 기업이 헤드리스 CMS 아키텍처를 분석 및 마케팅 기술 스택과 통합하는 데 필요한 전문 기술을 보유하고 있는 경우는 드물기 때문에 해당 서비스에 대한 수요가 급증하고 있습니다. Adobe Experience Manager나 Sitecore의 심층적인 온보딩은 일반적으로 6-12개월에 걸쳐 진행되며, API 통합, 역할 기반 액세스 설정, 사용자 교육 등을 포괄하기 때문에 공인 통합 업체에 대한 의존도가 높아지고 있습니다.

매니지드 서비스는 자동 백업, 가동 시간 모니터링, 템플릿 라이브러리를 갖춘 턴키 환경을 제공함으로써 IT 인력이 없는 중소기업들로부터 지지를 받고 있습니다. 서비스 지출의 대부분은 북미와 유럽이 차지하고 있지만, 아시아태평양의 구매자들은 여전히 저렴한 라이선스와 셀프 서비스형 문서를 중요하게 여기고 있습니다. 도입을 부수적인 것이 아니라 핵심 수익원으로 삼는 벤더는 지속적인 수익을 확보하고 고객 이탈을 줄일 수 있을 것입니다.

2025년, 컨텐츠 제작 툴 시장에서 클라우드 도입 점유율은 54.62%를 유지했습니다. 이는 중소기업이 즉각적인 프로비저닝과 인프라 관련 부하가 없는 환경을 선호하기 때문입니다. 그러나 하이브리드 구성은 연평균 성장률(CAGR) 11.92%로 성장하고 있습니다. 이는 대기업이 기밀 데이터를 On-Premise에 보관하면서도 클라우드상에서 실시간 공동 편집이 가능하도록 하는 아키텍처를 채택하고 있기 때문입니다. 마이크로소프트는 Office 365와 On-Premise SharePoint 간의 선택적 동기화를 지원하므로, 기업은 편의성을 저해하지 않으면서 거버넌스를 유지할 수 있습니다.

GDPR(EU 개인정보보호규정)이나 새로운 AI 거버넌스 규정과 같은 규제 요인들은 지역별 호스팅이 국경을 초월한 데이터 요건을 충족할 수 있도록 함으로써 하이브리드 도입을 촉진하고 있습니다. 클라우드와 데이터센터 거점 전체에 걸쳐 모니터링, ID 관리, 버전 관리를 통합하는 벤더는 운영의 복잡성을 줄여줍니다. 강력한 하이브리드 오케스트레이션은 50만 달러를 초과하는 계약의 RFP 평가에서 결정적인 요인으로 작용하고 있습니다.

지역별 분석

북미는 SaaS 보급률이 높고, 기업들이 AI 저작 툴를 조기에 실험적으로 도입한 데 힘입어 2025년 매출의 40.36%를 차지했습니다. 2026년 4월, 어도비가 Semrush를 19억 달러에 인수한 것은 SEO 분석을 Creative Cloud의 워크플로우에 직접 연동함으로써 실리콘밸리에서의 리더십을 확고히 다지는 계기가 되었습니다. 캘리포니아주의 CPRA(캘리포니아주 개인정보보호법) 등 미국의 주 개인정보보호법은 하이브리드 도입을 촉진하고 있는 반면, 캐나다에서는 컨텐츠 제작량을 늘리는 이중 언어 컨텐츠 의무화가 호재로 작용하고 있습니다. 시장이 성숙기에 접어들면서 신규 고객 확보가 제한적이기 때문에 공급업체들은 업셀링과 크로스셀링에 주력할 수밖에 없게 되었습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR) 12.67%를 나타낼 것으로 전망됩니다. 인도의 ‘디지털 인디아’ 이니셔티브는 2025년까지 디지털 인프라에 12억 달러를 배정하여 국내 클라우드 도입을 촉진하고 있습니다. 중국에서는 데이터 주권에 관한 규제가 강화됨에 따라 국내산 소프트웨어가 선호되는 경향이 있으며, 이로 인해 현지 클라우드 업체들이 혜택을 보고 있습니다. 동남아시아의 디지털 경제는 2025년에 총상품가치(GMV) 2,180억 달러에 달할 것으로 예상되며, 이는 옴니채널 컨텐츠 툴에 대한 수요를 촉진하고 있습니다. 호주 및 뉴질랜드는 북미의 도입 패턴을 반영하고 있으며, 클라우드 오케스트레이션과 규정 준수 인증을 중시하고 있습니다.

유럽에서는 엄격하게 시행되고 있는 GDPR(EU 개인정보보호규정)에 따라, 국경을 넘는 데이터 흐름을 제한하는 하이브리드형 도입이 선호되고 있습니다. 독일에서는 제조 라이프사이클과 관련된 기술 문서가 우선시되고 있지만, 영국은 브렉시트 이후 규제 차이가 있음에도 불구하고 여전히 혁신의 중심지로 자리 잡고 있습니다. 남유럽에서는 레거시 시스템이나 예산 제약으로 인해 도입 속도가 더딘 임베디드니다. 중동 및 아프리카는 여전히 새로운 기회가 있는 지역이며, 사우디아라비아의 스마트시티 구상과 남아프리카공화국의 다언어 교육 프로그램이 공동 집필에 대한 초기 수요를 형성하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the content authoring tools market size is projected to expand from USD 1.60 billion in 2025 and USD 1.76 billion in 2026 to USD 2.89 billion by 2031, registering a CAGR of 10.39% between 2026 and 2031.

This report is Segmented by Component (Software/Tools, and Services), Deployment Model (On-Premises, Cloud, and Hybrid), Organization Size (SMEs, and Large Enterprises), End-User Industry (Media and Entertainment, E-Learning and Education, Marketing and Advertising Agencies, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Content Authoring Tools Market Trends and Insights

Generative AI-Powered Authoring Enhancements

Adobe embedded the Gemini, Veo, and Imagen models in Creative Cloud in October 2025, enabling text-to-video generation and intelligent tagging inside existing workflows. Microsoft deployed Copilot across Office 365 in 2025, automating slide decks, document summaries, and emails, which pilot programs reported cut production time by 30%. Canva absorbed Leonardo.ai, MangoAI, Cavalry, Simtheory, and Ortto between 2024 and 2026, translating AI breakthroughs into a 40% upswing in premium subscribers by early 2026. As a result, platforms that lag in credible generative AI risk price pressure when customers consolidate vendors. The compliance landscape remains fluid, so vendors that deliver content provenance tools and granular model settings gain an edge with regulated buyers.

Growing Demand for Video-Based E-Learning Content

Corporate learning teams increasingly choose video because completion rates run 75% higher than text-only modules, according to several LMS providers. X-Pilot raised USD 18 million in January 2024 and tripled enterprise licenses within 18 months after sponsors cited 50% faster course development. Synthesia crossed 1,000 enterprise customers by 2025, including half of the Fortune 100, thanks to multilingual AI avatars that replace expensive studio shoots. The pivot pressures legacy e-learning authoring vendors to integrate native video or risk displacement by specialist platforms. Balancing speed with script quality remains critical because poorly produced AI video can erode learner trust.

High Total Cost of Ownership for Enterprise-Grade Platforms

Annual licensing for Adobe Experience Manager often reaches USD 200,000 to USD 500,000, with professional services adding comparable expense, pushing budgets 40% to 60% above initial estimates. Sitecore deployments can exceed USD 1 million in year one once infrastructure and customization are considered. As vendors retire perpetual licenses, subscription renewals can outpace budget growth, prompting buyers to demand transparent calculators and ROI metrics tied to engagement lift.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of SaaS Content Suites Among SMEs

- Expansion of Remote and Hybrid Workflows

- Data-Privacy and IP Leakage Concerns in Cloud Workflows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software and tools controlled a 76.74% content authoring tools market share, yet professional and managed services are forecast to outpace the overall content authoring tools market at an 11.48% CAGR through 2031. Services demand has accelerated because enterprises seldom possess the specialized skills required to integrate headless CMS architectures with analytics and martech stacks. High-touch onboarding for Adobe Experience Manager or Sitecore typically spans 6-12 months, covering API integrations, role-based access configuration, and user training, driving increasing reliance on certified integrators.

Managed services appeal to SMEs that lack IT staff by delivering turnkey environments with automated backups, uptime monitoring, and template libraries. North America and Europe account for most service spending, whereas Asia-Pacific buyers still emphasize lower-cost licenses and self-service documentation. Vendors that treat implementation as a core revenue stream rather than an adjunct will capture recurring revenue and mitigate churn.

Cloud installations retained a 54.62% share of the content authoring tools market in 2025, as SMEs prefer instant provisioning and no infrastructure overhead. Hybrid configurations, however, are advancing at an 11.92% CAGR as large enterprises adopt architectures that keep sensitive data on-premises while enabling real-time collaborative editing in the cloud. Microsoft allows selective synchronization between Office 365 and on-premises SharePoint, enabling enterprises to maintain governance without sacrificing usability.

Regulatory drivers, notably GDPR and emerging AI governance rules, reinforce hybrid adoption because regional hosting satisfies cross-border data mandates. Vendors that unify monitoring, identity management, and version control across cloud and data-center sites reduce operational complexity. Strong hybrid orchestration has become a decisive factor in RFP evaluations for contracts exceeding USD 500,000.

Geography Analysis

North America controlled 40.36% of 2025 revenue, aided by deep SaaS penetration and early enterprise experimentation with AI authoring. Adobe's USD 1.9 billion Semrush acquisition in April 2026 cements Silicon Valley's leadership by connecting SEO analytics directly to Creative Cloud workflows. U.S. state privacy statutes such as California's CPRA spur hybrid adoption, while Canada benefits from bilingual content mandates that expand authoring volume. Market maturity forces vendors to focus on upsell and cross-sell because net-new logo growth is limited.

Asia-Pacific is the fastest-expanding region, set to log a 12.67% CAGR through 2031. India's Digital India initiative allocated USD 1.2 billion for digital infrastructure in 2025, spurring domestic cloud adoption. China's preference for domestic software following tightened data sovereignty rules benefits local cloud vendors. Southeast Asia's digital economy reached USD 218 billion gross merchandise value in 2025, energizing demand for omnichannel content tools. Australia and New Zealand mirror North American adoption patterns, emphasizing cloud orchestration and compliance certifications.

Europe's tightly enforced GDPR drives preference for hybrid deployments that restrict cross-border data flows. Germany prioritizes technical documentation linked to manufacturing lifecycles, while the United Kingdom remains an innovation hub despite post-Brexit regulatory divergence. Southern Europe shows slower adoption due to legacy systems and budget constraints. The Middle East and Africa remain emerging opportunities, with smart-city initiatives in Saudi Arabia and multilingual education programs in South Africa shaping early demand for collaborative authoring.

- Adobe Inc.

- Microsoft Corporation

- Canva Pty Ltd

- Squarespace, Inc.

- Quark Software, Inc.

- Figma, Inc.

- Atlassian Corporation Plc

- Notion Labs, Inc.

- Google LLC

- Apple Inc.

- Liferay, Inc.

- Sitecore Holding II A/S

- Acrolinx GmbH

- MadCap Software, Inc.

- TechSmith Corporation

- Articulate Global, LLC

- iSpring Solutions, Inc.

- ePublishing, Inc.

- Ceros, Inc.

- Upland Software, Inc.

- Bit.ai, Inc.

- Lucid Software Inc.

- Author-it Software Corporation

- Easygenerator B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Video-Based E-Learning Content

- 4.2.2 Rapid Adoption of SaaS Content Suites Among SMEs

- 4.2.3 Expansion of Remote and Hybrid Workflows

- 4.2.4 Increasing Investment in Interactive Marketing Experiences

- 4.2.5 Generative AI-Powered Authoring Enhancements

- 4.2.6 Emergence of Headless CMS Integrations for Omnichannel Delivery

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Enterprise-Grade Platforms

- 4.3.2 Data-Privacy and IP Leakage Concerns in Cloud Workflows

- 4.3.3 Skills Gap in Rich-Media Template Development

- 4.3.4 Vendor Lock-In Due to Proprietary File Formats

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software/Tools

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 Media and Entertainment

- 5.4.2 E-Learning and Education

- 5.4.3 Marketing and Advertising Agencies

- 5.4.4 Government and Public Sector

- 5.4.5 Others End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adobe Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Canva Pty Ltd

- 6.4.4 Squarespace, Inc.

- 6.4.5 Quark Software, Inc.

- 6.4.6 Figma, Inc.

- 6.4.7 Atlassian Corporation Plc

- 6.4.8 Notion Labs, Inc.

- 6.4.9 Google LLC

- 6.4.10 Apple Inc.

- 6.4.11 Liferay, Inc.

- 6.4.12 Sitecore Holding II A/S

- 6.4.13 Acrolinx GmbH

- 6.4.14 MadCap Software, Inc.

- 6.4.15 TechSmith Corporation

- 6.4.16 Articulate Global, LLC

- 6.4.17 iSpring Solutions, Inc.

- 6.4.18 ePublishing, Inc.

- 6.4.19 Ceros, Inc.

- 6.4.20 Upland Software, Inc.

- 6.4.21 Bit.ai, Inc.

- 6.4.22 Lucid Software Inc.

- 6.4.23 Author-it Software Corporation

- 6.4.24 Easygenerator B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment