|

시장보고서

상품코드

2063968

중동 및 아프리카의 통합 시설 관리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Middle East And Africa Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

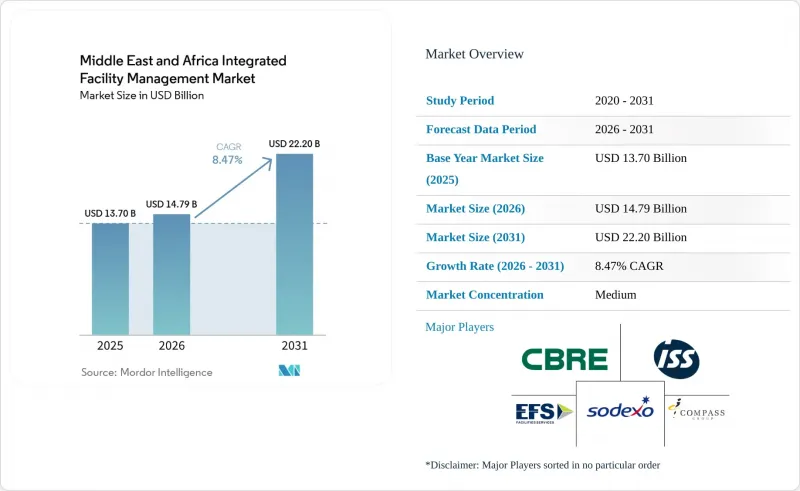

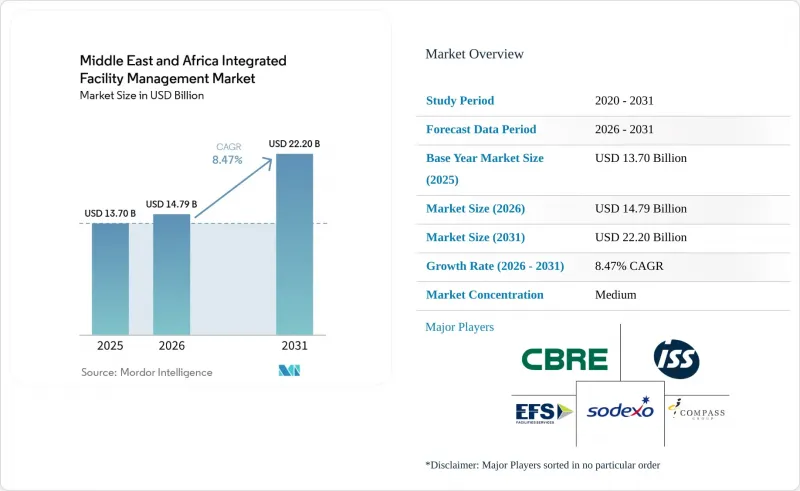

Mordor Intelligence에 의하면, 중동 및 아프리카 통합 시설 관리 시장 규모는 2025년 137억 달러, 2026년 147억 9,000만 달러에서 2031년까지 222억 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.47%를 나타낼 것으로 예측됩니다.

본 보고서는 서비스 유형(하드 시설 관리(자산 관리, MEP 및 HVAC 서비스 등), 소프트 시설 관리(사무 지원 및 보안, 청소 서비스, 케이터링 서비스 등)), 최종 사용자(상업, 의료 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 아프리카의 통합 시설 관리 시장 동향 및 인사이트

스마트 인프라를 추진하는 정부의 비전 프로그램

사우디아라비아의 ‘비전 2030’ 및 UAE의 장기 개발 프레임워크에 따라, 운영, 유지보수 및 업무 공간 서비스를 통합하여 제공해야 할 자산 기반이 확대되고 있습니다. 2025년, 사우디아라비아의 비석유 부문 활동은 실질 GDP의 55.6%를 차지하고 있으며, 이는 관광, 서비스, 물류, 공공 인프라와 관련된 건축 자산이 탄화수소 기반 산업을 넘어 확대되고 있음을 보여줍니다. 같은 해 연차 보고서에 따르면, 2025년 관광객 수는 1억 2,300만 명에 달했고, 소비액은 810억 달러에 이르렀다고 합니다. 이에 따라 호텔, 엔터테인먼트 지구, 교통 시설 및 공공시설은 지속적인 운영 상태를 유지하고 있습니다. 중동 및 아프리카 통합 시설 관리 시장(MEA IFM)에서 이러한 변화는 더 대규모의 종합적 계약 체결을 촉진하고 있습니다. 왜냐하면 새로운 지역이나 복합 용도 프로젝트에서는 청소, 경비, 엔지니어링, 수명 주기 성과를 통합적으로 관리할 수 있는 단일 공급업체가 필요하기 때문입니다. 중동 및 아프리카의 통합 시설 관리(MEA FM) 시장 역시 성과 기반 조달 방식으로 전환되고 있습니다. 이는 공공 부문의 고객들이 계약업체에 자산 가치 보호, 서비스 수준 달성, 그리고 운영 주기 전반에 걸친 현지화 목표 달성을 지원해 줄 것을 요구하고 있기 때문입니다. 이로 인해 여러 거점에 걸쳐 기술적 전문성, 인력 규모, 디지털 모니터링을 결합할 수 있는 제공업체의 경쟁력이 높아지고 있습니다.

상업용 부동산의 에너지 효율 개선 공사 증가

건물 소유주들이 에너지 비용 절감과 지속가능성 목표 달성을 추구하는 가운데, 에너지 효율 개선 공사는 중동 및 아프리카의 통합 시설 관리 시장에서 정기적인 서비스 항목으로 자리 잡고 있습니다. 국제에너지기구(IEA)는 전 세계 에너지 소비량의 40%를 건물이 차지한다고 밝혔으며, 이로 인해 에너지 성능은 부동산 소유주와 공공기관에게 여전히 중요한 과제로 남아 있습니다. 2025년 10월에 발표된 동료 심사를 거친 연구에 따르면, 주거 및 상업용 건물은 UAE의 국내 에너지 소비량의 39%를 차지하고 있으며, 이로 인해 개보수 수요는 명확한 운영 비용 기반과 밀접하게 연관되어 있습니다. Emrill Energy는 2025년 10월, 두바이와 샤르자 각 사업장에서 실시된 AI 기반 HVAC(냉난방 공조) 개조를 통해 18개월 동안 14%의 검증된 전력 절감 효과를 달성했으며, 사업장별 평균 효율 향상률은 21%에 달했다고 발표했습니다. 중동 및 아프리카의 통합 시설 관리 시장에서 이러한 개보수 프로그램은 단순히 설비를 개선하는 데 그치지 않고, 초기 프로젝트 완료 후에도 장기간에 걸친 모니터링, 유지보수 및 검증 업무를 창출합니다. 이러한 추세에 따라 계약은 일회성 엔지니어링 업무에서 성과에 연동된 다년간의 운영 계약으로 점차 전환되고 있습니다.

표준화를 가로막는 분열된 벤더 생태계

중동 및 아프리카의 통합 시설 관리 시장에서는 아프리카와 중동의 많은 2선 도시에서 여전히 하도급 업체가 다층적으로 개입하는 구조로 운영되고 있습니다. 이러한 구조로 인해 여러 거점에 걸친 계약에서 서비스 품질, 인력 배치 기준, 보고 체계에 차이가 발생하고 있습니다. 나이지리아의 상업 지구와 나이로비의 확대되는 사무실 공급 시장에는 여전히 가격 경쟁을 심화시키는 수많은 소규모 사업자들이 진입하고 있어, ISO 인증을 받은 서비스 제공업체들이 표준화된 서비스를 제공하기가 어려워지고 있습니다. 공급업체가 서로 다른 건축 기준, 안전 규정, 인증 관행을 동시에 관리해야 하는 경우, 국경을 넘는 업무는 더욱 복잡해집니다. 중동 및 아프리카의 통합 시설 관리 시장에서 CAFM 시스템을 도입하고 보다 엄격한 공급업체 자격 기준을 적용하는 기업은 일관성을 높일 수 있지만, 시스템 통합 및 직원 교육에 드는 비용이 초기 수익을 압박하고 있습니다. 그 결과, 여러 아프리카 시장에서 통일된 서비스 모델을 구축하려는 지역 플랫폼의 확장 속도가 둔화되고 있습니다.

부문별 분석

하드 시설 관리(Hard FM)는 중동 및 아프리카의 통합 시설 관리 시장에서 가장 빠르게 성장하고 있는 서비스 유형으로, 2026년부터 2031년까지의 예상 연평균 성장률(CAGR)은 8.53%입니다. 이러한 성장은 MEP, HVAC 및 소방 시스템에 대한 전문적인 관리가 필요한 데이터센터 단지, 의료시설, 산업 단지 및 대규모 상업용 건물에서 수요 증가를 반영하고 있습니다. 2025년에 도입된 새로운 안전 및 건설 규정 준수 요건으로 인해, 주요 도시 자산, 특히 기술 규제가 적용되는 건물에서 예방적 유지보수 및 점검 활동의 범위가 확대되었습니다. 기가 프로젝트의 운영 모델은 고장 대응형 활동이 아닌 장기적인 예방 유지보수 작업에 의존하고 있기 때문에 자산 관리, MEP 및 HVAC 서비스는 여전히 하드 FM 서비스의 가장 큰 축을 이루고 있습니다. 중동 및 아프리카의 통합 시설 관리 시장에서 데이터센터는 현재 하드 FM 수요 부문에서 1위를 차지하고 있습니다. 이는 기존의 상업시설보다 전문 인력과 지속적인 감시, 그리고 더욱 엄격한 환경 관리가 필요하기 때문입니다.

소프트 시설 관리(Soft FM)는 2025년 중동 및 아프리카 통합 시설 관리 시장 규모의 62.33%를 차지했습니다. 이는 호텔·관광, 의료, 정부 자산 분야의 청소, 급식, 사무 지원, 보안과 같은 업무의 노동 집약성에 힘입은 결과입니다. 많은 지역 포트폴리오에서는 대규모 공공시설, 복합 용도 커뮤니티, 공공시설에서 여전히 많은 인력이 필요한 서비스 제공이 요구되기 때문에 이러한 경쟁력은 여전히 중요합니다. 파넥사는 2025년 9월, UAE 전역에서 하이브리드 청소 모델을 확대했습니다. 30대 이상의 로봇 청소기를 도입했으며, 추가로 60대를 발주한 상태이며, 2026년 중반까지 100대 이상으로 늘리겠다는 목표를 세웠습니다. 이는 규모를 해치지 않으면서 소프트웨어 서비스가 어떻게 자동화되고 있는지를 보여줍니다. 사우디아라비아의 관광 활동 역시 리조트, 엔터테인먼트 시설, 복합 휴양 시설에서 케이터링 및 지원 서비스에 대한 수요를 지속적으로 뒷받침하고 있습니다. 이 나라에는 2025년에 1억 2,300만 명의 관광객이 방문하여 810억 달러의 소비가 발생한 것으로 보고되었습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the middle east and Africa integrated facility management market size is projected to expand from USD 13.70 billion in 2025 and USD 14.79 billion in 2026 to USD 22.20 billion by 2031, registering a CAGR of 8.47% between 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Middle East And Africa Integrated Facility Management Market Trends and Insights

Government Vision Programs Driving Smart Infrastructure

Saudi Arabia's Vision 2030 and the UAE's long-range development frameworks are expanding the asset base that needs bundled operations, maintenance, and workplace services. In 2025, Saudi Arabia's non-oil activities made up 55.6% of real GDP, which shows how the building stock tied to tourism, services, logistics, and public infrastructure is widening beyond the hydrocarbon base.The same annual report stated that tourism reached 123 million arrivals and USD 81 billion in spending in 2025, which keeps hotels, entertainment districts, transport assets, and public venues in continuous operating mode. In the Middle East and Africa integrated facility management market (MEA IFM), that shift supports larger bundled contracts because new districts and mixed-use projects need one provider to manage cleaning, security, engineering, and lifecycle performance together. The Middle East and Africa integrated facility management (MEA FM) market is also moving closer to outcome-based procurement because public clients want contractors to protect asset value, meet service levels, and support localization goals through the full operating cycle. This raises the advantage of providers that can combine technical depth, workforce scale, and digital oversight across multiple sites.

Rise in Energy-Efficiency Retrofits Across Commercial Real Estate

Energy-efficiency retrofits are turning into a recurring service line for the Middle East and Africa integrated facility management market as owners try to cut utility spend and meet sustainability targets. The IEA stated that buildings account for 40% of global energy consumption, which keeps energy performance high on the agenda for property owners and public authorities. A peer-reviewed study published in October 2025 found that residential and commercial buildings represented 39% of the UAE's national energy use, which keeps retrofit demand tied to a clear operating cost base. Emrill Energy stated in October 2025 that AI-driven HVAC retrofits across sites in Dubai and Sharjah delivered 14% verified electricity savings over 18 months, with average site efficiency gains of 21%. In the Middle East and Africa integrated facility management market, these retrofit programs do more than improve equipment, because they create longer monitoring, maintenance, and verification work after the first project is complete. That pattern is moving more contracts away from one-time engineering jobs and toward multi-year operating agreements tied to performance.

Fragmented Vendor Ecosystem Limiting Standardization

The Middle East and Africa integrated facility management market still works through dense subcontractor layers in many African and tier-2 Middle Eastern locations. This structure creates variation in service quality, staffing standards, and reporting discipline across multi-site contracts. Nigeria's commercial corridors and Nairobi's expanding office stock still attract many small operators that compete strongly on price, which makes standardized delivery harder for ISO-aligned providers. Cross-border work becomes more complex when providers must manage different building codes, safety rules, and certification practices at the same time. In the Middle East and Africa integrated facility management market, firms that deploy CAFM systems and stricter vendor qualification rules can improve consistency, but the cost of systems integration and workforce training weighs on early returns. The result is a slower scaling path for regional platforms that want to build uniform service models across several African markets.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Data Centers Demanding Specialized FM Services

- Increasing Adoption Of IoT-Enabled Predictive Maintenance

- Skilled-Labor Shortages in HVAC And MEP Trades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard Facility Management (Hard FM) is the fastest-growing service type in the Middle East and Africa integrated facility management market, with a forecast CAGR of 8.53% from 2026 to 2031. The expansion reflects rising demand from data center campuses, healthcare facilities, industrial sites, and large commercial buildings that need specialist management of MEP, HVAC, and fire systems. New safety and construction compliance requirements in 2025 widened the scope of preventive maintenance and inspection activity across major urban assets, especially in technically regulated buildings. Asset management, MEP, and HVAC services remain the largest hard service anchors because giga-project operating models depend on long-duration preventive work rather than break-fix activity. In the Middle East and Africa integrated facility management market, data centers now sit at the top end of hard FM demand because they require specialist staffing, continuous oversight, and tighter environmental control than conventional commercial properties.

Soft Facility Management (Soft FM) held 62.33% of the Middle East and Africa integrated facility management market size in 2025, supported by the labor intensity of cleaning, catering, office support, and security across hospitality, healthcare, and government assets. That lead remains important because many regional portfolios still need high-headcount service delivery across large public venues, mixed-use communities, and institutional facilities. Farnek expanded its hybrid cleaning model across the UAE in September 2025, with more than 30 robotic cleaners deployed, 60 more on order, and a target of over 100 units by mid-2026, which shows how soft services are being automated without losing scale. Saudi Arabia's tourism activity also keeps catering and support services active across resorts, entertainment assets, and hospitality complexes, with the kingdom reporting 123 million tourist arrivals and USD 81 billion in spending in 2025.

List of Companies Covered in this Report:

- CBRE Group Inc.

- ISS A/S

- Compass Group plc

- Sodexo SA

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- G4S plc

- Serco Group plc

- EFS Facilities Services Group

- Emrill Services LLC

- Farnek Services LLC

- Imdaad LLC

- Khidmah LLC

- Transguard Group LLC

- Atalian Servest Group Ltd

- Veolia Environnement SA

- Bouygues Energies & Services

- ENGIE Solutions

- Aden Group

- Al Shirawi Facilities Management LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Energy-Efficiency Retrofits Across Commercial Real Estate

- 4.2.2 Growing Regulatory Mandates for Building Safety Compliance

- 4.2.3 Expansion of Data Centers Demanding Specialized FM Services

- 4.2.4 Increasing Adoption of IoT-Enabled Predictive Maintenance

- 4.2.5 Government Vision Programs Driving Smart Infrastructure (e.g., Saudi Vision 2030, UAE Vision 2031)

- 4.2.6 Upsurge in Public-Private Partnership Models for Social Infrastructure Upkeep

- 4.3 Market Restraints

- 4.3.1 Fragmented Vendor Ecosystem Limiting Standardization

- 4.3.2 Skilled-Labor Shortages in HVAC and MEP Trades

- 4.3.3 Volatile Oil-Linked Budgets Curtailing OPEX in Government Facilities

- 4.3.4 Cyber-Security Concerns Around Connected Building Systems

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

- 5.3 By Geography

- 5.3.1 Middle East

- 5.3.1.1 Saudi Arabia

- 5.3.1.2 United Arab Emirates

- 5.3.1.3 Qatar

- 5.3.1.4 Kuwait

- 5.3.1.5 Rest of Middle East

- 5.3.2 Africa

- 5.3.2.1 South Africa

- 5.3.2.2 Nigeria

- 5.3.2.3 Kenya

- 5.3.2.4 Egypt

- 5.3.2.5 Rest of Africa

- 5.3.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 ISS A/S

- 6.4.3 Compass Group plc

- 6.4.4 Sodexo SA

- 6.4.5 Jones Lang LaSalle Incorporated

- 6.4.6 Cushman & Wakefield plc

- 6.4.7 G4S plc

- 6.4.8 Serco Group plc

- 6.4.9 EFS Facilities Services Group

- 6.4.10 Emrill Services LLC

- 6.4.11 Farnek Services LLC

- 6.4.12 Imdaad LLC

- 6.4.13 Khidmah LLC

- 6.4.14 Transguard Group LLC

- 6.4.15 Atalian Servest Group Ltd

- 6.4.16 Veolia Environnement SA

- 6.4.17 Bouygues Energies & Services

- 6.4.18 ENGIE Solutions

- 6.4.19 Aden Group

- 6.4.20 Al Shirawi Facilities Management LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment