|

시장보고서

상품코드

2063983

농약 첨가제 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agrochemical Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

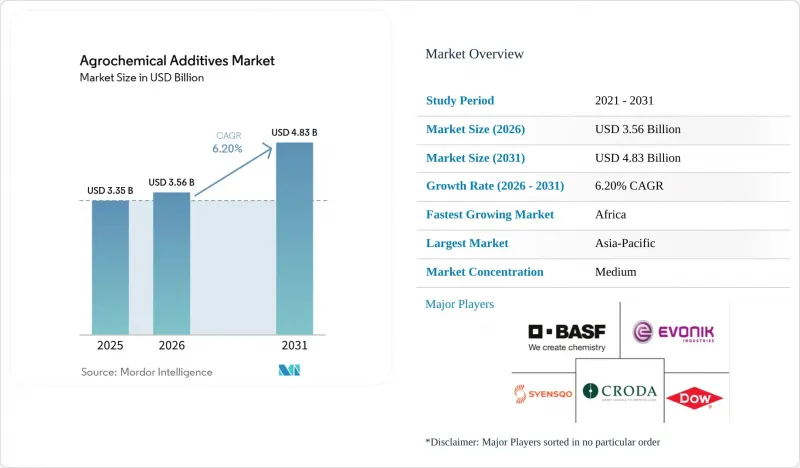

Mordor Intelligence에 의하면, 농약 첨가제 시장 규모는 2025년 33억 5,000만 달러로 평가되었고, 2026년에는 35억 6,000만 달러로 추정되고, 2031년까지 48억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.2%를 기록할 전망입니다.

본 보고서는 첨가제 유형별(계면활성제, 분산제 등), 형태별(액체 및 고체), 용도별(농약, 비료 등), 작물 유형별(곡물, 과일 및 채소 등), 그리고 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 농약 첨가제 시장 동향 및 인사이트

농작물 수확량 증대를 위한 수요 증가

작물 수확량 향상을 위한 수요가 증가하고 있다는 사실은 유엔 식량농업기구(FAO)의 데이터를 통해 명확히 드러나고 있습니다. 해당 기관의 보고서에 따르면, 전 세계 곡물 생산량은 2024년 28억 4,900만 톤에서 2025년에는 29억 1,100만 톤으로 증가하여 전년 대비 2.1%의 성장률을 기록했습니다. 이러한 성장은 주로 경작지 확대가 아니라 수확량 증가에 기인한 것이며, 효율성을 중시하는 농업 관행에 주력한 결과를 반영하고 있습니다. 이러한 생산성 향상은 정밀 농업과 투입 자재의 최적화에 달려 있으며, 그중에서도 농약 첨가제는 농약의 효과, 영양분 흡수 및 살포 효율을 높이는 데 중요한 역할을 하고 있습니다. 이러한 추세가 농약 첨가제 시장 수요 증가에 기여하고 있습니다.

정밀 살포와 나노 제제의 급속한 보급

정밀 살포 기술은 살포 정확도와 작업 효율을 향상시키는 능력 덕분에 빠르게 보급되고 있습니다. 아라하바드의 인도 정보기술연구소 연구진은 2025년 시점에서 UAV(무인항공기) 기반 살포 시스템이 최대 95%의 살포 피복 효율을 달성했고, 드리프트를 80% 가까이 줄였다고 보고하며, 표적 집중 살포 방식의 장점을 강조하고 있습니다. 이러한 수준의 성능을 실현하기 위해서는 점도, 안정성 및 분무 특성이 최적화된 제형이 필요하며, 그 결과 첨단 첨가제 및 나노 제형에 대한 수요가 증가하고 있습니다. 또한, 드론을 활용한 살포가 확대됨에 따라 현대 농업 기기와 호환되는 고정밀 제제 기술에 대한 수요가 높아지고 있습니다.

에톡시화 노닐페놀에 대한 규제 당국의 감시 강화

규제 당국은 에톡시화 노닐페놀이 환경에 미치는 광범위한 영향과 건강 피해를 고려하여 관련 규제를 강화하고 있습니다. 2025년 조사에서 Toxics Link는 검사 대상이었던 40개 제품 중 15개 제품에서 노닐페놀 에톡실레이트를 검출했습니다. 제품 내 농도는 최대 957 mg/kg에 달했으며, 하천수에서는 70마이크로g/L가 기록되어 오염의 심각성을 여실히 보여주고 있습니다. 이러한 사실이 밝혀짐에 따라, 내분비 교란 작용 및 환경 내 화합물의 잔류성에 대한 우려가 커지고 있으며, 규제 당국의 감시도 강화되고 있습니다. 그 결과, 제조업체들은 보다 안전한 제품 성분으로 전환하고 있습니다. 이러한 변화로 인해 규정 준수 비용이 증가하고, 승인까지 걸리는 기간이 길어지며, 시장 성장이 저해되고 있습니다.

부문별 분석

2025년, 농약 첨가제 시장에서 계면활성제 부문은 44%라는 최대 점유율을 차지했으며, 농약 살포 시 살포 피복률 향상 및 제제의 안정성 확보에 중요한 역할을 수행함으로써 그 우위를 유지했습니다. 유화 농축제 및 현탁제 시스템에서 광범위하게 사용됨에 따라 주요 농업 지역에서 안정적인 수요가 유지되고 있습니다. 살포 효율과 환경 안전성에 대한 규제의 관심이 높아지는 가운데, 드리프트 억제제의 중요성이 커지고 있습니다. 정밀 살포 기술의 도입이 확대됨에 따라, 액적 제어를 개선하는 기능성 첨가제에 대한 수요가 더욱 증가하고 있으며, 현대 제제 전략에서 성능을 중시하는 화학 물질이 수행하는 역할이 부각되고 있습니다.

드리프트 억제제 부문은 살포 시 발생하는 드리프트를 최소화하고 살포 정밀도를 높이기 위한 규제 요건의 강화에 힘입어, 2026-2031년 연평균 성장률(CAGR) 9.5%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 드론과 정밀 살포 장비를 포함한 첨단 살포 기술의 급속한 보급이 점도 조절용 폴리머 수요를 견인하고 있습니다. 이러한 폴리머는 효과를 보장할 뿐만 아니라, 엄격한 환경 기준도 충족하고 있습니다. 또한, 지속가능성 분야의 동향이 생분해성 및 친환경 첨가제의 혁신을 촉진하고 있습니다. 규제를 준수하는 전문적인 솔루션으로의 이러한 전환은 경쟁 구도를 변화시키고, 고성능 첨가제 시스템에 유리한 위치를 마련해 주고 있습니다.

2025년, 농약 첨가제 시장 점유율의 최대 61%를 차지한 것은 액제였습니다. 이는 신속한 분산성, 취급의 용이성, 그리고 최신 살포 시스템과의 호환성 덕분입니다. 이러한 제제는 대용량 분무기나 정밀 기술과 원활하게 통합될 수 있기 때문에 대규모 농업 경영에서 선호되는 선택지가 되고 있습니다. 이러한 우위는 기계화의 진전과 엽면 살포법의 도입에 힘입어 더욱 강화되고 있습니다. 농약이나 양분 살포 시 성능을 최적화하기 위해서는 균일한 혼합과 안정적인 살포가 필수적이기 때문입니다.

액체 제제는 정밀 농업 및 드론을 활용한 살포 시스템의 발전에 힘입어, 2026-2031년 예측 기간 동안 연평균 성장률(CAGR) 6.8%를 기록하며 가장 빠른 성장세를 유지할 것으로 예측됩니다. 한편, 고형 제제는 안정성이 뛰어나고 운송상의 문제가 적기 때문에 종자 처리나 물류에 민감한 지역에서 인기가 높아지고 있습니다. 포장재 감축이나 유통기한 연장 같은 환경적 요인들도 고형 제제의 단계적 도입에 기여하고 있습니다. 그러나 액제제는 그 운용 효율과 진화하는 농업 기술과의 호환성 덕분에 앞으로도 주도적인 위치를 유지할 것으로 예측됩니다.

지역별 분석

아시아태평양은 급속한 농업 현대화와 정밀 기술의 광범위한 도입에 힘입어, 2025년 농약 첨가제 시장에서 34%라는 최대 점유율을 차지했습니다. 중국이나 인도 등에서는 정책 지원과 기술 통합을 통해 농업의 기계화를 추진하고, 투입 자재의 효율적인 이용을 촉진하고 있습니다. 이 지역의 광대한 경작 기반과 생산성 향상에 대한 관심이 높아짐에 따라, 성능을 중시하는 솔루션에 대한 수요가 뒷받침되고 있습니다. 또한, 현지 생산 확대와 정부 주도의 노력으로 지역 공급망이 강화되고, 선진적인 농업 기법의 도입이 촉진되고 있습니다.

아프리카 시장 규모는 농업 생산성에 대한 투자 확대와 농업 투입재에 대한 접근성 개선에 힘입어, 2026-2031년 연평균 성장률(CAGR) 7.8%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 금융 포용 프로그램 및 보조금 연계형 사업을 통해 소규모 농가 공동체에서 현대적인 농업 자재의 도입이 확대되고 있습니다. 또한, 투입 자원의 효율적인 활용과 작물 보호에 대한 인식이 높아지면서 수요가 증가하고 있습니다. 한편, 남미는 대규모 상업 농업과 선진적인 작물 관리 기술의 보급 확대에 힘입어 계속해서 강력한 성장 잠재력을 보여주고 있습니다.

북미는 높은 기술 도입률과 잘 갖춰진 농업 시스템 덕분에 중요한 위치를 차지하고 있습니다. 미국 농무부(USDA)에 따르면, 2024년 미국의 작물 재배지 총 면적은 3억 2,800만 에이커로, 이는 집약적인 농업과 지속 가능한 농업 자재의 이용 규모를 여실히 보여주고 있습니다. 이러한 방대한 경작 기반이 성능 향상형 제제에 의존하는 작물 보호 솔루션에 대한 꾸준한 수요를 이끌고 있습니다. 유럽은 규제가 엄격하지만 여전히 혁신을 중시하는 시장으로 남아 있는 반면, 중동에서는 수자원 효율화 노력과 환경 제어형 농업에 힘입어 완만한 성장세를 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the agrochemical additives market size is projected to grow from USD 3.35 billion in 2025 to USD 3.56 billion in 2026 and is projected to reach USD 4.83 billion by 2031, registering a CAGR of 6.2% during 2026-2031.

This report is Segmented by Additive Type (Surfactants, Dispersants, and More), by Form (Liquid and Solid), by Application (Pesticides, Fertilizers, and More), by Crop Type (Cereals and Grains, Fruits and Vegetables, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Agrochemical Additives Market Trends and Insights

Growing Demand for Higher Crop Yield Intensification

The increasing demand for higher crop yield intensification is highlighted by data from the Food and Agriculture Organization (FAO), which reports that global cereal production rose from 2,849 million metric tons in 2024 to 2,911 million metric tons in 2025, representing a 2.1% year-on-year increase. This growth is primarily attributed to improved yields rather than the expansion of cultivated land, reflecting a focus on efficiency-driven farming practices. These productivity improvements rely on precision agriculture and optimized input usage, where agrochemical additives play a critical role in enhancing pesticide effectiveness, nutrient absorption, and spray efficiency. This trend is contributing to rising demand in the agrochemical additives market.

Rapid Uptake of Precision Spraying and Nano-Formulations

Precision spraying technologies are experiencing significant adoption due to their capability to improve application accuracy and operational efficiency. Researchers from the Indian Institute of Information Technology, Allahabad, reported that UAV-based spraying systems achieved up to 95% spray coverage efficiency while reducing drift by nearly 80% as of 2025, emphasizing the advantages of targeted application methods. This level of performance necessitates formulations with optimized viscosity, stability, and spray characteristics, thereby increasing the demand for advanced additives and nano-formulations. Additionally, the expanding use of drone-based spraying is driving the need for precision-grade formulation technologies that are compatible with modern agricultural equipment.

Increasing Regulatory Scrutiny on Ethoxylated Nonylphenols

Regulatory bodies are tightening their grip on ethoxylated nonylphenols, given their prevalent environmental footprint and the health hazards they pose. In a 2025 investigation, Toxics Link uncovered nonylphenol ethoxylates in 15 of the 40 products tested. Concentrations peaked at 957 mg/kg in products and reached 70 µg/L in river water, underscoring the severity of contamination. Such revelations amplify worries about endocrine disruption and the compounds' longevity in the environment, leading to heightened regulatory vigilance. Consequently, manufacturers are pivoting towards safer product formulations. This shift increases compliance costs, lengthens approval timelines, and restrains market growth.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidy Shift Toward Adjuvant-Optimized Formulations

- Expansion of Glyphosate-Tolerant Crops Needing Adjuvant Compatibility

- Volatility in Ethylene Oxide and Alcohol-Ethoxylate Feedstock Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The surfactants segment held the largest 44% share of the agrochemical additives market in 2025, maintaining its dominance due to its critical role in enhancing spray coverage and ensuring formulation stability in pesticide applications. Their widespread use in emulsifiable concentrates and suspension systems supports consistent demand in major agricultural regions. With a regulatory focus on spray efficiency and environmental safety, the importance of drift-control agents has increased. The growing adoption of precision spraying technologies has further boosted the demand for functional additives that improve droplet control, emphasizing the role of performance-oriented chemistries in modern formulation strategies.

The drift control agents segment is projected to grow at the fastest CAGR of 9.5% during 2026-2031, driven by stricter regulatory requirements to minimize spray drift and enhance application accuracy. The rapid adoption of advanced spraying technologies, including drones and precision tools, is fueling demand for viscosity-modifying polymers. These polymers not only ensure effectiveness but also meet stringent environmental standards. Furthermore, sustainability trends are fostering innovation in biodegradable and eco-friendly additives. This shift toward specialized, regulation-compliant solutions is transforming the competitive landscape, favoring high-performance additive systems.

Liquid formulations accounted for the largest 61% of the agrochemical additives market share in 2025, driven by their rapid dispersion, ease of handling, and compatibility with modern spraying systems. These formulations are the preferred choice in large-scale agricultural operations due to their seamless integration with high-capacity sprayers and precision technologies. Their dominance is further supported by increasing mechanization and the adoption of foliar application methods, where uniform mixing and consistent delivery are essential for optimizing performance in pesticide and nutrient applications.

Liquid formulations are anticipated to maintain the fastest growth trajectory, registering a CAGR of 6.8% during the forecast period 2026-2031, fueled by advancements in precision agriculture and drone-based spraying systems. Meanwhile, solid formulations are gaining popularity in seed treatment and regions sensitive to logistics due to their stability and reduced transportation challenges. Environmental factors, such as packaging reduction and improved shelf life, are also contributing to the gradual adoption of solid formats. However, liquids are projected to maintain their leading position owing to their operational efficiency and compatibility with evolving agricultural technologies.

Geography Analysis

Asia-Pacific held the largest 34% agrochemical additives market share in 2025, supported by rapid agricultural modernization and the widespread adoption of precision technologies. Countries such as China and India are advancing mechanized farming and promoting efficient input utilization through policy support and technology integration. The region's extensive cultivation base and growing emphasis on productivity enhancement are sustaining demand for performance-focused solutions. Additionally, the expansion of local manufacturing and government-supported initiatives is bolstering regional supply chains and facilitating the adoption of advanced agricultural practices.

Africa market size is projected to grow at the fastest 7.8% CAGR from 2026 to 2031, driven by increasing investments in agricultural productivity and improved access to farming inputs. Financial inclusion programs and subsidy-linked initiatives are enhancing the adoption of modern farming inputs among smallholder communities. Furthermore, rising awareness of efficient input usage and crop protection is driving demand. Meanwhile, South America continues to exhibit strong growth potential, supported by large-scale commercial farming and the growing adoption of advanced crop management techniques.

North America holds a prominent position due to its high level of technological adoption and well-structured agricultural systems. According to the United States Department of Agriculture (USDA), the total cropland used for crops in the United States was 328 million acres in 2024, highlighting the scale of intensive farming and consistent input utilization. This extensive cultivation base drives steady demand for crop protection solutions reliant on performance-enhancing formulations. Europe remains a regulated but innovation-focused market, while the Middle East exhibits gradual growth, supported by water-efficiency initiatives and controlled-environment agriculture.

- BASF SE

- Evonik Industries AG

- Croda International Plc

- Dow Inc.

- Syensqo SA

- Stepan Company

- Clariant AG

- Nouryon Holding B.V.

- Huntsman International LLC

- Ingevity Corporation

- Sasol Limited

- Innospec Inc.

- LEVACO Chemicals GmbH

- Precision Laboratories LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for higher crop yield intensification

- 4.2.2 Rapid uptake of precision spraying and nano-formulations

- 4.2.3 Government subsidy shift toward adjuvant-optimized formulations

- 4.2.4 Expansion of glyphosate-tolerant crops needing adjuvant compatibility

- 4.2.5 Rising drone-based foliar application requiring low-viscosity additives

- 4.2.6 Carbon-credit monetization for fertilizer reduction via additives

- 4.3 Market Restraints

- 4.3.1 Increasing regulatory scrutiny on ethoxylated nonylphenols

- 4.3.2 Volatility in ethylene oxide and alcohol-ethoxylate feedstock costs

- 4.3.3 Farmer reluctance toward premium bio-based adjuvants

- 4.3.4 Ag-chem distributor consolidation squeezing additive margins

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Additive Type

- 5.1.1 Surfactants

- 5.1.2 Dispersants

- 5.1.3 Emulsifiers

- 5.1.4 Antifoaming Agents

- 5.1.5 Drift Control Agents

- 5.1.6 Others

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid

- 5.3 By Application

- 5.3.1 Pesticides

- 5.3.2 Fertilizers

- 5.3.3 Seed Treatment

- 5.3.4 Soil Conditioners

- 5.4 By Crop Type

- 5.4.1 Cereals and Grains

- 5.4.2 Fruits and Vegetables

- 5.4.3 Oilseeds and Pulses

- 5.4.4 Others

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 Russia

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Evonik Industries AG

- 6.4.3 Croda International Plc

- 6.4.4 Dow Inc.

- 6.4.5 Syensqo SA

- 6.4.6 Stepan Company

- 6.4.7 Clariant AG

- 6.4.8 Nouryon Holding B.V.

- 6.4.9 Huntsman International LLC

- 6.4.10 Ingevity Corporation

- 6.4.11 Sasol Limited

- 6.4.12 Innospec Inc.

- 6.4.13 LEVACO Chemicals GmbH

- 6.4.14 Precision Laboratories LLC