|

시장보고서

상품코드

2063992

AI 기반 감염 관리 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI-based Infection Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

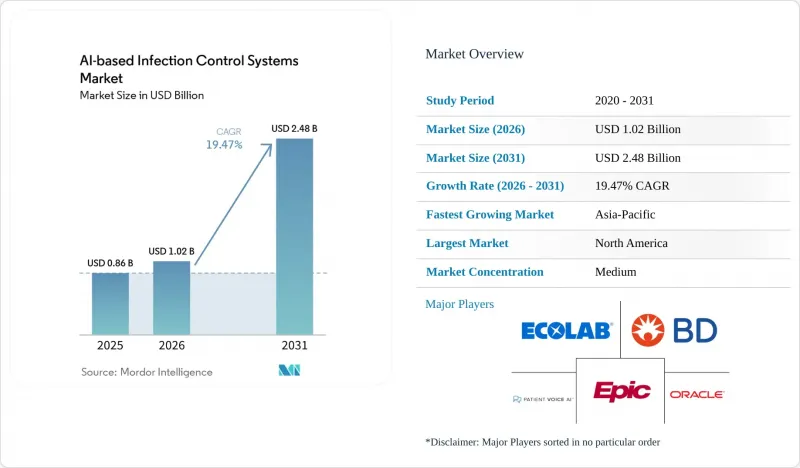

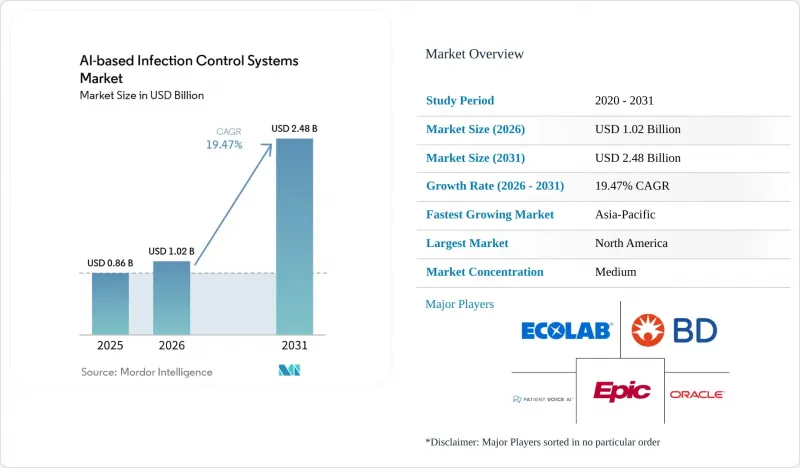

Mordor Intelligence에 의하면, AI 기반 감염 관리 시스템 시장 규모는 2025년 8억 6,000만 달러로 평가되었고, 2026년에는 10억 2,000만 달러로 추정되고, 2026-2031년 CAGR 19.47%로 성장을 지속할 전망이며, 2031년까지 24억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제공 유형별(소프트웨어, 하드웨어, 서비스), 배포 모델별(클라우드 기반, 온프레미스형, 하이브리드형), 최종 사용자별(급성기 병원, 장기 요양 시설, 외래수술센터(ASC), 클리닉 및 전문 의료 센터), 그리고 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 AI 기반 감염 관리 시스템 시장 동향 및 인사이트

증가하는 병원 내 감염(HAI) 및 항생제 내성(AMR)의 부담

AI 기반 감염 관리 시스템 시장의 임상적 근거는 수동 감시만으로는 충분히 억제하지 못하고 있는 부담에서 비롯됩니다. 2024년 체계적 문헌고찰에 따르면, 감염 예방 담당자들은 근무 시간의 거의 절반을 감시 관련 업무에 할애하고 있는 반면, 중환자실(ICU)의 병원 내 감염(HAI) 발생률은 전 세계적으로 신생아 병동의 17%에서 성인 중환자실의 68%에 이르는 것으로 나타났습니다. 해당 리뷰에서는 병원 내 혈류 감염의 사망률이 10%에서 20%에 달하며, 생존 환자 1명당 약 4만 달러의 추가 비용이 발생한다는 점도 지적되고 있어, 조기 발견의 경제적 이점은 매우 명백합니다. 발표된 연구에 따르면, AI를 활용한 감시를 통해 병원 내 감염 발생률을 1.31%에서 0.58%로 낮출 수 있으며, 수작업에 의한 진료 기록 확인 업무 부담을 83.9% 줄일 수 있는 것으로 나타났으며, 이를 통해 병원의 구매 담당자는 자동화와 노동 부담 경감 사이에 직접적인 연관성을 확인할 수 있습니다. 항생제 내성이 여전히 정책의 핵심 초점으로 남아 있으며, 유엔의 목표는 2019년 기준치인 495만 명의 사망자 수와 연동되어 있고, 2030년까지 전 세계 항생제 소비량이 30% 이상 증가할 것으로 예상에 따라 그 압박은 더욱 커지고 있습니다. 이러한 요인들이 복합적으로 작용함에 따라, AI 기반 감염 관리 시스템 시장 전체에서 예측적 감시 및 관리 도구가 도입 결정의 핵심으로 자리 잡고 있습니다.

강화되는 감염 보고 의무

규제 강화로 인해 AI 기반 감염 관리 시스템 시장에서 많은 병원에 있어 조달 활동은 규정 준수 측면에서 필수적인 결정 사항이 되어가고 있습니다. 2024년 1월 이후, CMS(미국 의료보험·의료서비스센터)의 ‘메디케어 상호운용성 촉진 프로그램(PIP)’은 대상 병원 및 크리티컬 액세스 병원에 대해 항생제 사용 및 내성 관련 데이터를 CDC(미국 질병통제예방센터)의 NHSN(국립병원감시네트워크)에 제출할 것을 의무화하고 있습니다. 2024년 기준으로, 병원의 73%가 자동화 및 수동 방식을 결합하여 이 요건을 충족하고 있었으나, 57%는 AUR(항생제 사용 및 내성) 보고를 가장 어려운 공중보건 보고 업무로 꼽았으며, 이는 수동 워크플로가 여전히 제대로 작동하지 않는 부분이 있음을 보여줍니다. 또한 CMS는 HAC 감축 프로그램에 따라 2026 회계연도의 지급액을 HAI 관련 성과와 연계시켰습니다. 여기에는 CLABSI, CAUTI, MRSA 균혈증, CDI 및 수술 후 상처 감염 지표가 포함됩니다. 2026 회계연도 IPPS 규정안은 FHIR 표준을 활용한 디지털 품질 측정으로의 전환을 더욱 촉진하고 있으며, 이에 따라 감염 데이터를 실시간으로 수집, 정규화 및 전송할 수 있는 플랫폼의 가치가 높아질 것입니다.

높은 도입 및 검증 비용

AI 기반 감염 관리 시스템 시장에서 비용은 여전히 실질적인 장벽으로 남아 있습니다. 왜냐하면 도입에는 라이선싱 이상의 작업이 필요하기 때문입니다. 병원에서는 감염 감시 모델이 일상 진료에서 신뢰할 수 있는 수준에 도달하기까지, 데이터 통합 작업, 워크플로우 재설계, 사용자 교육, 그리고 현장 검증을 수행해야 합니다. 디지털 성숙도가 낮은 시스템에서는 그 부담이 더욱 커집니다. 독일의 DigitalRadar 2024에서 평균 점수가 100점 만점에 42점이라는 사실은 자금 지원을 받고 있는 병원 시스템이라 하더라도 AI를 쉽게 도입하는 데 필요한 기반이 여전히 부족할 가능성이 있음을 보여줍니다. 또한, 검증 역시 여전히 중요한 우려 사항입니다. 독립적인 검토 결과, 통제된 도입 환경 이외의 곳에서는 AI의 성능이 저하될 가능성이 있는 것으로 나타났으며, 이로 인해 의료 기관은 가동 개시 후 모니터링 및 재훈련에 필요한 예산을 확보할 수밖에 없습니다. 이러한 요인들로 인해 감염 관리의 필요성은 높지만, 자금이나 기술 인력이 제한적인 중규모 병원, 지방의 의료시설, 자원이 부족한 환경에서는 의사 결정이 지연되고 있습니다.

부문별 분석

2025년 기준으로, AI 기반 감염 관리 시스템 시장 점유율의 67.42%를 소프트웨어가 차지했으며, 이는 하드웨어 중심의 도입과 비교했을 때 분석 및 모니터링 플랫폼의 확장성을 반영한 것입니다. 이러한 우위는 병원의 구매 경향도 반영하고 있습니다. 왜냐하면 대부분의 의료 기관은 물리적 인프라를 교체하기보다는 기존의 전자의무기록(EHR), 검사, 약품 관리 시스템 위에 중첩하여 사용할 수 있는 소프트웨어 계층을 선호하기 때문입니다. Wolters Kluwer사의 Sentri7과 같은 제품은 소프트웨어가 여전히 자리 잡고 있는 이유를 보여줍니다. 이 플랫폼은 2026년 KLAS 평가에서 감염 관리 및 모니터링 부문 1위를 차지하며, 임상 팀에게 실용적인 감시 워크플로우의 가치를 입증했습니다. 또한, 소프트웨어 중심의 구성은 감염 예방 팀이 수작업에 따른 검토 및 보고 부담과 반복적인 후속 조치를 줄여주는 자동화 도구를 지속적으로 우선시하는 예산 추세와도 부합합니다.

AI 기반 감염 관리 시스템 업계의 서비스 시장은 2031년까지 연평균 성장률(CAGR) 21.9%로 확대될 것으로 예상되며, 서비스 구성 요소 중 가장 빠르게 성장하고 있는 분야입니다. 이러한 성장은 초기 도입 후에도 검증, 조정, 워크플로우 적용이 지속적으로 이루어지는 다양한 시스템이 혼재된 병원 환경에 AI를 통합해야 하는 실무상의 과제를 반영하고 있습니다. 서비스 제공업체는 모델의 성능 유지, 경보 시스템을 현지 임상 관행에 맞추는 일, 그리고 변화하는 규정 준수 요건에 보고 결과를 일관되게 부합시키는 데 지원이 필요하기 때문에 관리형 지원의 중요성이 커지고 있습니다. 하드웨어는 AI 기반 감염 관리 시스템 업계에서 여전히 지원 단계에 머물러 있지만, Vitalacy의 Gen5 웨어러블이나 BioVigil의 AccuWash 도입과 같은 제품 혁신은 손 위생 및 직원 행동 모니터링이 주요 이용 사례인 상황에서 배지, 싱크 비콘, 센싱 디바이스가 여전히 중요함을 보여주고 있습니다.

지역별 분석

2025년 기준으로 북미는 AI 기반 감염 관리 시스템 시장 점유율의 39.23%를 차지했습니다. 이는 견고한 규제 인프라, NHSN(전미 병원 감염 감시 네트워크)에 보고를 제출하는 병원의 기반이 광범위하다는 점, 그리고 미국을 중심으로 한 공급업체 생태계가 존재한다는 점을 반영하고 있습니다. 이 지역 수요는 CMS(미국 의료보험·의료서비스센터)가 ‘상호운용성 촉진 프로그램(PIP)’에 따라 2024년 1월부터 대상 병원 및 크리티컬 액세스 병원에 대해 AUR(자동 감염 보고) 제출을 의무화한 데 힘입어 가속화되었습니다. 2024년까지 병원의 73%가 이미 AUR 데이터를 제출했으나, 57%는 여전히 이 요건을 가장 어려운 보고 업무로 꼽고 있으며, 이는 자동화된 감시 플랫폼에 대한 수요를 직접적으로 뒷받침하고 있습니다. 또한 북미는 이미 입지를 다진 공급업체와 레퍼런스 사이트가 밀집해 있다는 장점이 있어, 다른 많은 지역에 비해 도입 시 실험적인 요소가 없습니다는 이점이 있습니다. Sentri7이나 Premier의 임상 감시 도구와 같은 플랫폼은 병원들이 측정 가능한 워크플로우의 효율화와 보다 용이한 공중보건 보고를 요구하고 있기 때문에 이러한 환경의 혜택을 지속적으로 누리고 있습니다.

유럽은 지역 내 도입 현황에 차이가 있기는 하지만, 자금 지원, 공공 디지털 헬스 정책, 연구 네트워크가 같은 방향으로 나아가고 있기 때문에 AI 기반 감염 관리 시스템 시장에서 여전히 중요한 위치를 차지하고 있습니다. 독일의 ‘Krankenhauszukunftsgesetz(병원 미래법)’은 병원의 변혁을 위해 500억 유로(535억 달러 상당) 규모의 기금을 조성했으나, 2024년 DigitalRadar 평가에서 평균 점수가 100점 만점에 42점에 그친 것으로 보아, 디지털 대응 준비는 여전히 미흡한 것으로 나타났습니다. RISK PRINCIPE 컨소시엄과 샤리테(Charite)의 감시 연구는 상호 운용 가능한 데이터 파이프라인을 통해 이미 대규모 병원 내 원인성 균혈증 모니터링이 가능함을 보여주고 있으며, 이를 통해 유럽에서는 조사 단계에서 실용화 단계로 이어지는 견고한 가교가 마련되었습니다. 프랑스의 AP-HP 역시 2025년 중반까지 약 300건의 내부 AI 이니셔티브를 시행할 것이라고 보고했습니다. 한편, EU AI법 및 유럽 헬스 데이터 스페이스에 따라 엄격한 인증 및 데이터 거버넌스 요건을 충족하는 공급업체를 중심으로 성장이 집중될 가능성이 높습니다.

아시아태평양의 AI 기반 감염 관리 시스템 시장 규모는 2031년까지 연평균 성장률(CAGR) 23.5%로 확대될 것으로 예상되며, 가장 빠르게 성장하는 지역 블록이 될 전망입니다. 이 지역의 성장은 단순히 병원 내 감염(HAI)의 부담이 표면화되고 있다는 사실 이상의 요인을 반영하고 있습니다. 이는 각국 정부와 의료 시스템이 더욱 견고한 감염병 정보 체계와 병원 데이터 인프라를 구축하고 있기 때문입니다. 2025년 4월 일본이 ‘일본 보건안보연구소’를 설립한 것은 보다 일원화된 감염병 정보 체계 구축을 통해 이러한 방향성을 뒷받침하는 조치입니다. 한편, 병원 차원의 AI 도입 준비 상황도 이에 발맞추어 지속적으로 개선되고 있습니다. 인도 및 기타 아시아 신흥 시장에서는 ICU 감염률이 여전히 높은 데다, 완전한 전자건강기록(EHR) 통합이 아직 실현되지 않은 상황에서 보다 가벼운 모니터링 도구가 주목받는 등, 서로 다른 수요 패턴이 나타나고 있습니다. 중동 및 아프리카 및 남미는 AI 기반 감염 관리 시스템 시장에서 여전히 작은 점유율을 차지하고 있지만, 병원의 디지털화, GCC(걸프협력회의) 국가들의 의료 인프라 투자, 그리고 브라질 등 국가들의 공공 네트워크 단계적 현대화에 힘입어 성장이 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aI-based infection control systems market size is expected to grow from USD 0.86 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at 19.47% CAGR over 2026-2031.

This report is Segmented by Offering (Software, Hardware, Services), Deployment Model (Cloud-Based, On-Premise, Hybrid), End User (Acute Care Hospitals, Long-Term Care Facilities, Ambulatory Surgical Centers, Clinics and Specialty Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI-based Infection Control Systems Market Trends and Insights

Rising HAI and AMR Burden

The clinical case for the AI-based infection control systems market starts with a burden that manual surveillance has not contained. A 2024 systematic review found that infection preventionists spend nearly half of their work hours on surveillance-related tasks, while HAI incidence in ICUs ranged from 17% in neonatal units to 68% in adult critical care units globally. The same review noted that hospital-acquired bloodstream infections carry a 10% to 20% mortality rate and add nearly USD 40,000 in cost per surviving patient, which keeps the financial case for earlier detection very clear. Published studies also show that AI-enabled surveillance can reduce HAI incidence from 1.31% to 0.58% and cut manual chart review workloads by 83.9%, which gives hospital buyers a direct link between automation and labor relief. The pressure rises further as antimicrobial resistance remains a central policy focus, with the UN target tied to the 2019 baseline of 4.95 million deaths and global antibiotic consumption expected to rise by more than 30% by 2030. That combination keeps predictive surveillance and stewardship tools near the center of adoption decisions across the AI-based infection control systems market.

Tightening Infection Reporting Mandates

Regulation is turning procurement into a compliance decision for many hospitals in the AI-based infection control systems market. Since January 2024, the CMS Medicare Promoting Interoperability Program has required eligible hospitals and critical access hospitals to submit antimicrobial use and resistance data to the CDC's NHSN. By 2024, 73% of hospitals were meeting the requirement through a mix of automated and manual methods, but 57% identified AUR reporting as their most difficult public health reporting task, which shows where manual workflows still break down. CMS also tied fiscal year 2026 payment exposure to HAI-related performance under the HAC Reduction Program, including CLABSI, CAUTI, MRSA bacteremia, CDI, and surgical site infection measures. The fiscal year 2026 proposed IPPS rule moves further toward digital quality measurement using FHIR standards, which will increase the value of platforms that can capture, normalize, and transmit infection data in real time.

High Deployment and Validation Costs

Cost remains a real barrier in the AI-based infection control systems market because implementation goes well beyond software licensing. Hospitals still need data integration work, workflow redesign, user training, and local validation before infection surveillance models can be trusted in daily practice. The burden is heavier in systems with limited digital maturity, and Germany's DigitalRadar 2024 average of 42 out of 100 shows that even funded hospital systems can still lack the foundation needed for easy AI deployment. Validation also remains a live concern because independent reviews have shown that AI performance can weaken outside controlled deployment settings, which forces providers to budget for monitoring and retraining after go-live. These factors slow decisions in mid-sized hospitals, rural facilities, and lower-resource settings where infection control needs are high, but capital and technical staffing remain limited.

Other drivers and restraints analyzed in the detailed report include:

- EHR and Clinical Data Interoperability Expansion

- Growth in Cloud-Based Surveillance Adoption

- Data Privacy and Cybersecurity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 67.42% of the AI-based infection control systems market share in 2025, which reflects the scalability of analytics and surveillance platforms compared with hardware-led deployments. This lead also mirrors how hospitals buy, because most providers prefer a software layer that can sit on top of existing EHR, laboratory, and pharmacy systems instead of replacing physical infrastructure. Products such as Wolters Kluwer's Sentri7 show why software remains entrenched, with the platform ranking first in KLAS for infection control and monitoring in 2026 and reinforcing the value of usable surveillance workflows for clinical teams. The software-heavy mix also fits a budget pattern where infection prevention teams continue to prioritize automation tools that reduce manual review, reporting burden, and repetitive follow-up work.

Services in the AI-based infection control systems industry are projected to expand at a 21.9% CAGR through 2031, which makes them the fastest-rising part of the service mix. The growth reflects the practical challenge of integrating AI into heterogeneous hospital environments where validation, tuning, and workflow adaptation continue well after the initial installation. Managed support is becoming more important because providers need help maintaining model performance, aligning alerts to local clinical practice, and keeping reporting outputs consistent with evolving compliance rules. Hardware remains a supporting layer in the AI-based infection control systems industry, but product refreshes such as Vitalacy's Gen5 wearable and BioVigil's AccuWash rollout show that badges, sink beacons, and sensing devices still matter where hand hygiene and staff behavior monitoring are core use cases.

Geography Analysis

North America held 39.23% of the AI-based infection control systems market share in 2025, which reflects strong regulatory infrastructure, a large NHSN-reporting hospital base, and a vendor ecosystem centered in the United States. The region's demand accelerated after CMS made AUR reporting mandatory from January 2024 for eligible hospitals and critical access hospitals under the Promoting Interoperability Program. By 2024, 73% of hospitals were already submitting AUR data, but 57% still identified that requirement as their most difficult reporting task, which directly supports demand for automated surveillance platforms. North America also benefits from a dense field of established vendors and reference sites that make procurement less experimental than in many other regions. Platforms such as Sentri7 and Premier's clinical surveillance tools continue to benefit from this environment because hospitals want measurable workflow savings and easier public health reporting.

Europe remains an important part of the AI-based infection control systems market because funding support, public digital health policy, and research networks are moving in the same direction, even if implementation is uneven across the region. Germany's Krankenhauszukunftsgesetz created a EUR 50 billion fund, equivalent to USD 53.5 billion, for hospital transformation, yet the 2024 DigitalRadar average of 42 out of 100 still shows that digital readiness remains incomplete. The RISK PRINCIPE consortium and the Charite surveillance work show that interoperable data pipelines can already produce hospital-onset bacteremia monitoring at scale, which gives Europe a solid research-to-deployment bridge. France's AP-HP also reported nearly 300 internal AI initiatives by mid-2025, while the EU AI Act and the European Health Data Space are likely to concentrate growth around vendors that can meet strict certification and data governance requirements.

Asia-Pacific AI-based infection control systems market size is projected to expand at 23.5% CAGR through 2031, making it the fastest-growing regional block. Growth in this region reflects more than headline HAI burden, because governments and health systems are also building stronger infectious disease intelligence and hospital data infrastructure. Japan's establishment of the Japan Institute for Health Security in April 2025 supports that direction by creating a more centralized infectious disease intelligence framework, while hospital-level AI readiness continues to improve in parallel. India and other emerging Asian markets add a different demand profile, where ICU infection rates remain high and lighter surveillance tools can be attractive when full EHR integration is not yet available. The Middle East and Africa and South America remain smaller parts of the AI-based infection control systems market, but growth should follow hospital digitization, GCC healthcare infrastructure investment, and gradual modernization of public networks in countries such as Brazil.

- Ascom

- BioVigil Hygiene Technologies LLC

- Beckton Dickinson

- Baxter

- Cognosos, Inc.

- Epic Systems

- Ecolab

- GOJO Industries, Inc.

- Inovalon Holdings, Inc.

- Kontakt.io, Inc.

- Oracle

- Sonitor Technologies

- Softgent SRL

- SwipeSense, Inc.

- Premier, Inc.

- PatientVoice AI, Inc.

- Vitalacy, Inc.

- Wolters Kluwer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising HAI and AMR Burden

- 4.2.2 Tightening Infection Reporting Mandates

- 4.2.3 EHR and Clinical Data Interoperability Expansion

- 4.2.4 Growth in Cloud-Based Surveillance Adoption

- 4.2.5 Infection Prevention Workforce Shortages

- 4.2.6 Privacy-Preserving Ambient Sensing Adoption

- 4.3 Market Restraints

- 4.3.1 High Deployment and Validation Costs

- 4.3.2 Data Privacy and Cybersecurity Concerns

- 4.3.3 Workflow Integration and Interoperability Gaps

- 4.3.4 Alert Fatigue and Model Generalizability Limits

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By End User

- 5.3.1 Acute Care Hospitals

- 5.3.2 Long-Term Care Facilities

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Clinics and Specialty Centers

- 5.3.5 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Ascom Holding AG

- 6.3.2 BioVigil Hygiene Technologies LLC

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Baxter International Inc.

- 6.3.5 Cognosos, Inc.

- 6.3.6 Epic Systems Corporation

- 6.3.7 Ecolab Inc.

- 6.3.8 GOJO Industries, Inc.

- 6.3.9 Inovalon Holdings, Inc.

- 6.3.10 Kontakt.io, Inc.

- 6.3.11 Oracle Corporation

- 6.3.12 Sonitor Technologies

- 6.3.13 Softgent SRL

- 6.3.14 SwipeSense, Inc.

- 6.3.15 Premier, Inc.

- 6.3.16 PatientVoice AI, Inc.

- 6.3.17 Vitalacy, Inc.

- 6.3.18 Wolters Kluwer N.V.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment