|

시장보고서

상품코드

2063997

자궁 경부 근긴장 이상 치료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cervical Dystonia Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

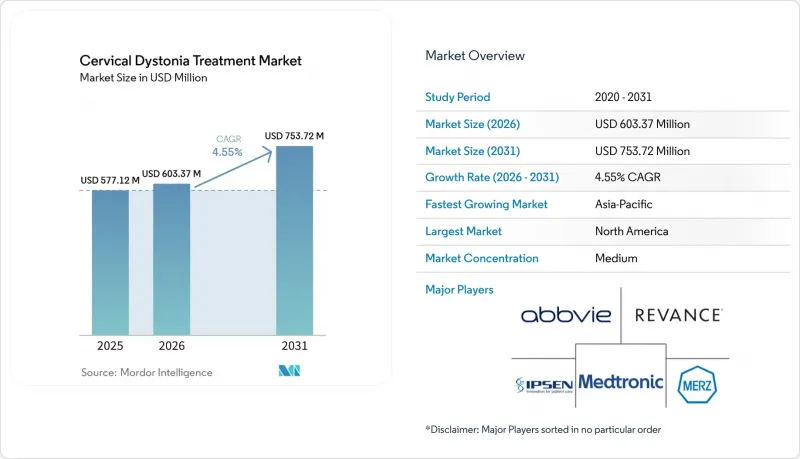

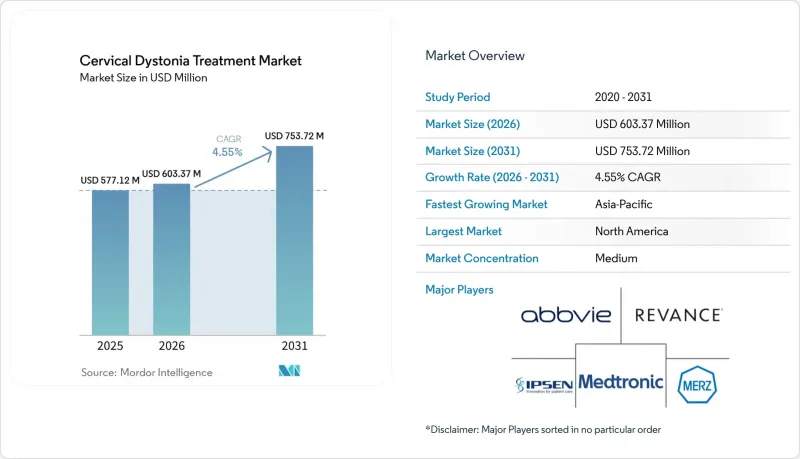

Mordor Intelligence에 의하면, 자궁 경부 근긴장 이상 치료 시장 규모는 2025년 5억 7,712만 달러로 평가되었고, 2026년에는 6억 337만 달러로 추정되고, 2026-2031년 CAGR 4.55%로 성장을 지속할 전망이며, 2031년까지 7억 5,372만 달러에 이를 것으로 예측됩니다.

본 보고서는 치료 유형별(보툴리눔툭신(보톡스) 주사(A형 신경독소(오나보툴리눔톡신 A 등) 등), 경구용 약물, 기타), 의료 제공 환경별(병원, 신경과 클리닉, 기타), 유통 채널별(병원, 소매, 온라인 약국), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 자궁 경부 근긴장 이상 치료 시장 동향 및 인사이트

중년층 신경과 환자의 진단율 증가

자궁 경부 근긴장 이상 치료 시장에서는 환자가 운동 장애 전문의를 만나기까지 일반 신경과를 계속 방문하는 기간이 수년에 달하기 때문에 여전히 수익 기회가 충분히 활용되지 못하고 있습니다. 중년층에서 조기 진단이 중요한 이유는 이 단계에서 지속적인 이상 자세, 진전 및 통증이 단순한 근골격계 문제가 아니라 치료 가능한 근긴장 이상증의 양상으로 인식되기 쉬워지기 때문입니다. 조기에 치료를 시작하는 환자는 경부 퇴행성 변화가 축적되지 않았으며, 기저 통증 부담도 낮은 경향이 있습니다. 이를 통해 보다 안정적인 경과 관찰이 가능해지며, 주사 주기 전반에 걸쳐 치료의 연속성이 향상됩니다. 이러한 변화는 치료의 지속 여부가 초기 진단뿐만 아니라 지속적인 치료에 대한 정착률에 좌우되기 때문에 직접적인 상업적 효과를 가져옵니다. 따라서, 의뢰 경로를 통해 초기 증상 발현부터 전문의의 확정 진단까지 걸리는 시간이 단축된다면, 자궁 경부 근긴장 이상 치료 시장은 그 혜택을 누리게 될 것입니다. 이러한 효과는 이미 신경과 분야의 네트워크가 밀접하고 확립된 의뢰 경로를 갖춘 의료 시스템에서 가장 먼저 나타날 가능성이 높다고 생각됩니다.

장시간 작용형 보툴리눔툭신(보톡스)의 혁신과 적응증 확대

지속 시간이 긴 보툴리눔툭신(보톡스)의 개발은 현재 자궁 경부 근긴장 이상 치료 시장을 형성하고 있는 가장 뚜렷한 제제적 변화입니다. DAXXIFY는 2023년 8월 미국에서 자궁 경부 근긴장 이상 치료제로 승인을 획득했으며, 2024년에 걸쳐 진행될 상업화를 통해 이 분야에서 30년 만에 처음으로 주요 치료제의 진전을 가져왔습니다. ASPEN-1 3상 임상시험에서 125단위의 투여량에서는 효과 지속 기간의 중앙값이 24주를 보였으며, 연하 장애 보고율은 1.6%였습니다. 이에 반해, 기존의 임상 실천 방식에서는 효과 지속 기간이 10-12주로 훨씬 짧은 것이 일반적이었습니다. 크라운 래버러토리즈는 2025년 2월, 레반스 테라퓨틱스를 9억 2,400만 달러에 인수하는 절차를 완료했습니다. 이는 장시간 작용형 보툴리눔툭신(보톡스)의 사용을 둘러싸고 현재 상업적 인프라가 구축되고 있음을 보여줍니다. 또한 레반스사는 DAXXIFY의 치료용 매출이 2024년에 318% 증가한 3,140만 달러에 달했다고 보고했습니다. 이는 절대적인 수치로 보면 다소 낮은 편이지만, 상업적 활용이 막 시작된 자산으로서는 매우 의미 있는 것입니다. 입센은 2025년 9월, 경부 디스토니아를 대상으로 한 콜라보타제의 2상 임상시험을 시작하며, 장기 작용형 파이프라인을 확충했습니다. 이로 인해 자궁 경부 근긴장 이상 치료 시장은 단일 신규 진출기업에 그치지 않는 확장세를 보였습니다.

고액의 지속적인 치료비와 보험금 지급상의 과제

브랜드 보톡스의 사용에는 장기간에 걸친 반복 투여가 필요하기 때문에 지속적인 비용은 여전히 자궁 경부 근긴장 이상 치료 시장에서 가장 중요한 제약 요인 중 하나입니다. 미국에서는 민간 보험 및 메디케어 어드밴티지 플랜의 사전 승인 절차에서 다음 투여 주기가 승인되기 전에 진단 확인, 근육 내 주사 기록, 그리고 과거 치료 효과에 대한 증명이 요구되는 경우가 많습니다. 행정 절차의 지연으로 인해 환자가 예정된 재치료 시기를 넘기게 되면, 증상 관리가 급격히 어려워져 장애가 재발할 우려가 있으며, 이로 인해 치료 중단 위험이 높아집니다. CMS(미국 의료보험 및 의료서비스 센터)의 정책은 일반적으로 주사 간격을 12주마다로 제한하고 있으며, 이는 기존의 보툴리눔툭신(보톡스) 사용 패턴을 전제로 수립된 것입니다. 그로 인해, 임상시험 데이터상 효과 지속 기간의 중앙값이 24주였던 DAXXIFY와 같은 제품과는 적합성이 낮은 상황이 발생하고 있습니다. 그 결과, 의사는 임상적 현실과 반드시 일치하지 않는 정책 주도형 치료의 격차에 대응하여 재치료 시기를 정당화하거나 환자의 기대치를 관리할 수밖에 없게 됩니다. 제약 회사가 지원 서비스를 제공하고 있는 경우에도, 자궁 경부 근긴장 이상 치료 시장은 이용률과 만족도 모두를 제한할 수 있는 지불 주체의 지급 시기와 관련된 규정의 영향을 계속 받고 있습니다.

부문별 분석

2025년, 보툴리눔툭신(보톡스) 주사는 매출의 68.2%를 차지했으며, 자궁 경부 근긴장 이상 치료 시장의 전체 치료 부문에서 확고한 1위 자리를 지켰습니다. 이러한 위상은 전문의들이 오랫동안 익숙하게 사용해 온 점, 확립된 보험 급여 체계, 그리고 증상 관리에 있어 여전히 가장 신뢰받는 1차 치료법으로 자리매김하고 있다는 사실을 반영하고 있습니다. 오나보툴리눔톡신 A는 일상 진료에서 투여자의 습관이나 처방 목록상의 선호도가 여전히 큰 영향력을 행사하고 있기 때문에 이 그룹 내에서 브랜드 리더십을 지속적으로 유지하고 있습니다. 인코보툴리눔톡신 A는 단백질을 포함하지 않는 제제라는 특징을 통해 독자적인 역할을 수행하고 있으며, 2025년 8월 메르츠 테라퓨틱스가 편두통 예방을 목적으로 한 제3상 임상시험 ‘MINT-E’ 및 ‘MINT-C’에 첫 환자를 등록함에 따라, 그 특성은 상업적 중요성을 한층 더 높였습니다. 리마보툴리눔톡신 B도 A형 2차 비반응자에 대한 적응증이 있어, 자궁 경부 근긴장 이상 치료 분야에서 구조적으로 중요한 위치를 계속 차지하고 있으며, MYOBLOC의 순매출액은 2024년에 전년 대비 10% 증가한 1억 110만 달러에 달했습니다.

경구용 약물은 2031년까지 연평균 7.0%의 성장률을 보일 것으로 예측되며, 자궁 경부 근긴장 이상 치료 시장에서 가장 빠르게 성장하는 치료제 군이 될 전망입니다. 이러한 성장은 대체가 아닌 병용에 기인한 것임이 시사되고 있습니다. 2025년 시범 연구에서 바르베나진은 보툴리눔 신경독소 치료에 병용 투여되었을 때 TWSTRS 점수를 개선하고, 치료 주기 종료 시 효과 감소를 완화했기 때문입니다. 항콜린제 및 벤조디아제핀 계열 약물의 제네릭 의약품 보급 확대 역시, 보툴리눔툭신(보톡스) 치료에 대한 접근성이 제한적이거나 도입이 지연되고 있는 지역에서 이러한 치료법의 채택을 촉진하고 있습니다. 기기 치료나 외과적 치료는 난치성 환자로 제한되어 있어 여전히 시장 규모는 작은 편이지만, 2025년 12월에 예정된 메드트로닉사의 DBS(뇌심부자극요법)에 대한 FDA의 적응증 변경으로 인해, 자궁 경부 근긴장 이상 치료 업계에서 이 분야에 대한 보험사의 급여 의지가 높아질 것으로 전망됩니다.

지역별 분석

2025년, 북미는 매출의 41.2%를 차지했으며 자궁 경부 근긴장 이상 치료 시장에서 가장 큰 점유율을 기록했습니다. 미국은 여전히 가장 큰 시장 기반을 차지하고 있으며, 애브비는 2025년 자사의 전체 치료제 포트폴리오 중 미국 내 치료용 신경독소 매출이 31억 5,100만 달러에 달했다고 보고했습니다. 지역적 성장은 여전히 성장의 한계에 직면해 있습니다. 이는 CMS(미국 의료보험 및 의료서비스 센터)의 투여 시기 관련 규정이, 임상 데이터에서 나타난 DAXXIFY의 더 긴 작용 지속 시간과 완전히 일치하지 않기 때문입니다. 반면, 북미는 전문의에 대한 접근성이 뛰어나고, 확립된 사전 승인 절차가 마련되어 있으며, 새로운 독소 제제의 조기 상업적 도입이 진행되고 있다는 점 등의 이점을 누리고 있습니다. 이러한 요인들로 인해, 지불 측의 저항으로 인해 장시간 작용형 제품의 완전한 활용이 지연되더라도, 해당 지역의 자궁 경부 근긴장 이상 치료 시장은 견조한 성장세를 유지하고 있습니다.

유럽은 주로 독일, 프랑스, 영국에 힘입어 자궁 경부 근긴장 이상 치료 시장에서 여전히 2위 지역 블록의 위치를 유지했습니다. 입센(Ipsen)은 2025년 유럽에서 디스포트 테라퓨틱스(Dysport Therapeutics)의 매출이 1억 5,840만 유로(1억 6,810만 달러 상당)를 기록하며, 고정 환율 기준으로 6.8%의 성장률을 보였습니다고 보고했습니다. 이 지역은 주요 국가들의 폭넓은 전문 지식과 유리한 보상 제도의 혜택을 누리고 있지만, 중앙집권적인 의뢰 체계로 인해 의료 제공업체 차원의 환자 처리 능력이 여전히 제한될 가능성이 있습니다. 또한, 메르츠는 2025년 8월, 제오민(Xeomin)과 관련된 두 건의 세계 3상 편두통 임상시험에서 첫 환자 등록을 시작하며, 유럽을 거점으로 한 신경학 분야에서의 폭넓은 입지를 강화했습니다.

아시아태평양은 2031년까지 연평균 6.3%의 성장률을 보일 것으로 예상되며, 자궁 경부 근긴장 이상 치료 시장에서 가장 빠르게 성장하는 지역이 될 것입니다. 이러한 성장은 전문의 인프라 확충, 지역 신경독소 제조업체들의 경쟁적인 활동, 그리고 몇년전과 비교해 다양해진 상업화 경로에 힘입어 이루어지고 있습니다. 휴겔사는 보툴리눔툭신(보톡스) 프로그램에서 경부 근긴장 이상증을 1상 개발 단계에 두고 있으며, 이는 해당 분야의 파이프라인이 미용 용도에서 치료 용도로 전환되고 있음을 보여줍니다. 남미, 중동 및 아프리카는 여전히 초기 단계에 있지만, 2025년 2월 오쿠마 제약이 사우디아라비아에서 ‘나보타’를 출시한 것은 확립된 주요 시장 이외의 지역에서도 지리적 확장이 계속되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the cervical dystonia treatment market size is expected to grow from USD 577.12 million in 2025 to USD 603.37 million in 2026 and is forecast to reach USD 753.72 million by 2031 at 4.55% CAGR over 2026-2031.

This report is Segmented by Treatment Type (Botulinum Toxin Injections [Type A Neurotoxins {OnabotulinumtoxinA, and More}, and More], Oral Medications, and More), Care Setting (Hospitals, Neurology Clinics, and More), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Cervical Dystonia Treatment Market Trends and Insights

Rising Diagnosis Rates in Mid-Life Neurology Cohorts

The cervical dystonia treatment market still leaves revenue on the table when patients spend years moving through general neurology visits before reaching a movement disorder specialist. Earlier diagnosis in mid-life cohorts matters because this is the stage when persistent abnormal posture, tremor, and pain are more likely to be recognized as a treatable dystonia pattern rather than a musculoskeletal complaint. Patients who enter treatment earlier often do so with less accumulated cervical degeneration and a lower baseline pain burden, which supports steadier follow-up and better continuity across injection cycles. That change has a direct commercial effect because recurring therapies depend on retention, not only on first diagnosis. The cervical dystonia treatment market therefore benefits when referral pathways shorten the lag between first symptoms and specialist confirmation. This effect is likely to emerge first in health systems that already have dense neurology networks and established referral routes.

Longer-Acting Toxin Innovation and Label Expansion

Longer-duration toxin development is the clearest formulation shift now shaping the cervical dystonia treatment market. DAXXIFY received U.S. approval for cervical dystonia in August 2023, and its commercial roll-out through 2024 introduced the first major therapeutic formulation advance in this class in more than 30 years. In the ASPEN-1 Phase 3 trial, the 125-unit dose showed a median duration of effect of 24 weeks, and dysphagia was reported at 1.6%, compared with the much shorter 10 to 12 week effect window often associated with older clinical practice patterns. Crown Laboratories completed its acquisition of Revance Therapeutics in February 2025 for USD 924 million, which showed that commercial infrastructure is now being built around extended-duration toxin use. Revance also reported that therapeutic revenue for DAXXIFY rose 318% in 2024 to USD 31.4 million, which was modest in absolute terms but meaningful for an asset that had only just entered commercial use. Ipsen added to the long-duration pipeline by initiating a Phase II study of corabotase in cervical dystonia in September 2025, which broadened the cervical dystonia treatment market beyond a single new entrant.

High Recurring Therapy Cost and Reimbursement Friction

Recurring cost remains one of the most important constraints on the cervical dystonia treatment market because branded toxin use requires repeat administration over long periods. In the United States, prior authorization under commercial and Medicare Advantage plans often requires diagnosis confirmation, muscle-level injection records, and proof of prior treatment response before another cycle is approved. When administrative delays push patients past planned retreatment timing, symptom control can fall sharply and disability can return, which raises the risk of discontinuation. CMS policy generally limits injections to every 12 weeks and was built around older toxin patterns, which creates a poor fit for products such as DAXXIFY that showed a 24-week median duration of effect in trial data. Physicians are then left to justify retreatment timing or manage expectations around a policy-driven care gap that does not always match clinical reality. Even when manufacturers provide support services, the cervical dystonia treatment market remains exposed to payer timing rules that can limit both utilization and satisfaction.

Other drivers and restraints analyzed in the detailed report include:

- Chronic First-Line Positioning of Botulinum Neurotoxins

- Ultrasound and EMG-Guided Injection Precision Gains

- Misdiagnosis and Limited Specialist Injector Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Botulinum toxin injections accounted for 68.2% of revenue in 2025, which kept them firmly in the lead across treatment categories in the cervical dystonia treatment market. Their position reflects long-standing specialist familiarity, durable reimbursement pathways, and the fact that they remain the most established first-line option for symptom control. OnabotulinumtoxinA continues to hold brand leadership within this group because injector habit and formulary preference still matter heavily in routine practice. IncobotulinumtoxinA keeps a distinct role through its protein-free formulation, and that profile gained added commercial relevance when Merz Therapeutics enrolled the first patients in its Phase III MINT-E and MINT-C migraine prevention trials in August 2025. RimabotulinumtoxinB also keeps a structurally important place in the cervical dystonia treatment industry because it serves Type A secondary non-responders, and MYOBLOC net product sales reached USD 101.1 million in 2024, up 10% year over year.

Oral medications are projected to expand at 7.0% through 2031, making them the fastest-growing treatment class in the cervical dystonia treatment market. That growth reflects adjunct use rather than replacement, since valbenazine improved TWSTRS scores and reduced end-of-cycle wearing-off when added to botulinum neurotoxin treatment in a 2025 pilot study. Generic penetration in anticholinergics and benzodiazepines also supports uptake where access to toxin treatment is limited or delayed. Device-based and surgical options remain smaller because they are reserved for refractory patients, yet the December 2025 FDA labeling change for Medtronic DBS should broaden payer willingness to cover this part of the cervical dystonia treatment industry.

Geography Analysis

North America held 41.2% of revenue in 2025, which gave the region the largest share in the cervical dystonia treatment market. The United States remained the largest country base, and AbbVie reported USD 3.151 billion in U.S. therapeutic neurotoxin revenue in 2025 across its full therapeutic portfolio. Regional growth still faces a reimbursement ceiling because CMS timing rules do not fully align with the longer duration shown for DAXXIFY in clinical data. At the same time, North America benefits from dense specialist access, established prior authorization pathways, and early commercial adoption of new toxin formats. These factors keep the cervical dystonia treatment market strong in the region even when payer friction slows full use of extended-duration products.

Europe remained the second-largest regional block in the cervical dystonia treatment market, supported mainly by Germany, France, and the United Kingdom. Ipsen reported EUR 158.4 million in European Dysport Therapeutics revenue in 2025, equal to USD 168.1 million, with 6.8% constant-exchange-rate growth. The region benefits from broad specialist expertise and favorable reimbursement in core countries, though centralized referral structures can still limit throughput at the provider level. Merz also enrolled the first patients in 2 global Phase III migraine trials for Xeomin in August 2025, which reinforced its broader neurology positioning from a European base.

Asia-Pacific is projected to expand at 6.3% through 2031, which makes it the fastest-growing regional part of the cervical dystonia treatment market. Growth is being supported by broader specialist infrastructure, competitive activity from regional neurotoxin manufacturers, and a wider set of commercialization pathways than the region had a few years ago. Hugel has cervical dystonia in Phase I development for its botulinum toxin program, which shows that the regional pipeline is moving beyond cosmetic use into therapeutic positioning. South America and the Middle East and Africa remain early-stage, though Daewoong's February 2025 launch of Nabota in Saudi Arabia shows that geographic expansion is continuing outside the largest established markets.

- Abbvie

- AEON Biopharma, Inc.

- Daewoong Pharmaceutical Co., Ltd.

- Fosun Pharma

- Ipsen

- Medtronic

- Medytox, Inc.

- Merz Pharma

- Mitra Bio, Inc.

- Revance Therapeutics, Inc.

- Sloan Pharma S.a.r.l.

- Solstice Neurosciences, LLC

- Supernus Pharmaceuticals

- Teijin Pharma Limited

- Vima Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diagnosis Rates in Mid-Life Neurology Cohorts

- 4.2.2 Longer-Acting Toxin Innovation and Label Expansion

- 4.2.3 Chronic First-Line Positioning of Botulinum Neurotoxins

- 4.2.4 Ultrasound and EMG-Guided Injection Precision Gains

- 4.2.5 Patient Affordability and Reimbursement-Support Programs

- 4.3 Market Restraints

- 4.3.1 High Recurring Therapy Cost and Reimbursement Friction

- 4.3.2 Misdiagnosis and Limited Specialist Injector Capacity

- 4.3.3 Secondary Non-Response and End-Of-Cycle Symptom Rebound

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Treatment Type

- 5.1.1 Botulinum Toxin Injections

- 5.1.1.1 Type A Neurotoxins

- 5.1.1.1.1 OnabotulinumtoxinA

- 5.1.1.1.2 AbobotulinumtoxinA

- 5.1.1.1.3 IncobotulinumtoxinA

- 5.1.1.1.4 Other Type A Neurotoxins

- 5.1.1.2 Type B Neurotoxins

- 5.1.1.2.1 RimabotulinumtoxinB

- 5.1.1.1 Type A Neurotoxins

- 5.1.2 Oral Medications

- 5.1.2.1 Anticholinergics

- 5.1.2.2 Benzodiazepines and GABAergic agents

- 5.1.2.3 Muscle relaxants

- 5.1.2.4 Dopaminergic and VMAT-modulating agents

- 5.1.3 Device-based and Surgical Interventions

- 5.1.3.1 Deep Brain Stimulation

- 5.1.3.2 Selective Peripheral Denervation

- 5.1.4 Supportive and Adjunctive Therapies

- 5.1.1 Botulinum Toxin Injections

- 5.2 By Care Setting

- 5.2.1 Hospitals

- 5.2.2 Specialty Neurology Clinics

- 5.2.3 Ambulatory Surgical Centers

- 5.2.4 Home Care and Rehabilitation Centers

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AbbVie Inc.

- 6.3.2 AEON Biopharma, Inc.

- 6.3.3 Daewoong Pharmaceutical Co., Ltd.

- 6.3.4 Fosun Pharma

- 6.3.5 Ipsen S.A.

- 6.3.6 Medtronic plc

- 6.3.7 Medytox, Inc.

- 6.3.8 Merz Pharma GmbH & Co. KGaA

- 6.3.9 Mitra Bio, Inc.

- 6.3.10 Revance Therapeutics, Inc.

- 6.3.11 Sloan Pharma S.a.r.l.

- 6.3.12 Solstice Neurosciences, LLC

- 6.3.13 Supernus Pharmaceuticals, Inc.

- 6.3.14 Teijin Pharma Limited

- 6.3.15 Vima Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment