|

시장보고서

상품코드

2064009

수의 감염증 진단 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Veterinary Infectious Disease Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

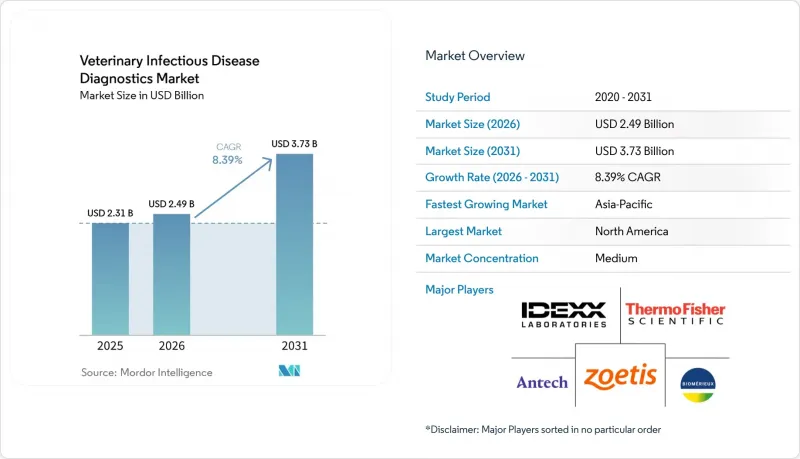

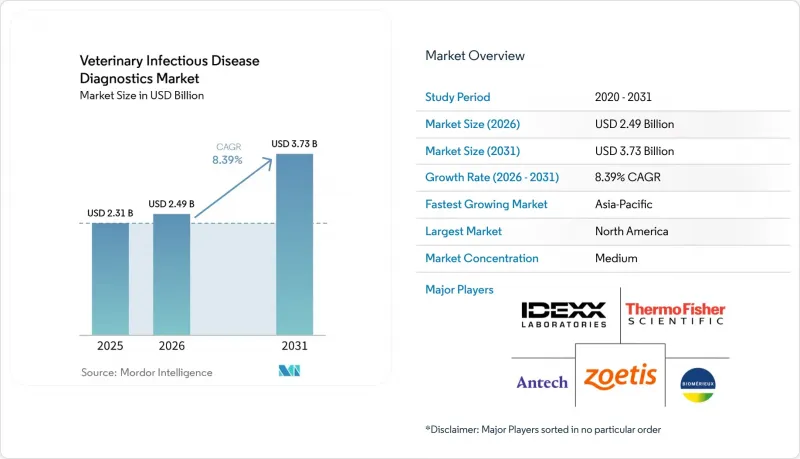

Mordor Intelligence에 의하면, 수의 감염증 진단 시장 규모는 2025년 23억 1,000만 달러, 2026년 24억 9,000만 달러에서 2031년까지 37억 3,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 8.39%를 나타낼 것으로 예측됩니다.

본 보고서는 기술별(면역 진단, 분자진단 등), 동물 종별(반려동물 및 식용 동물), 감염증 유형별(세균성, 바이러스성 등), 최종 사용자별(검사 기관, 동물병원 및 진료소 등), 그리고 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 수의 감염증 진단 시장 동향 및 인사이트

수의학 검사실에서의 AI 기반 영상 분석 도입

AI의 도입으로 인해, 검사실에서의 소견 판정은 주관적인 수작업 검토에서 데이터 기반의 자동화로 점차 전환되고 있습니다. Zoetis사의 ‘Vetscan Imagyst’와 같은 플랫폼을 통해 림프절이나 피부 종괴의 천자액을 몇 분 만에 선별 검사할 수 있게 되었습니다. 이는 과거에는 외부 검사 기관에서 며칠이 걸리던 과정이었는데, 이를 통해 치료 방침 결정이 신속해졌으며, 반려인의 치료 준수율도 향상되고 있습니다. 미국 수의사의 약 30%는 이미 영상 진단 및 기록 관리 업무에 AI를 활용하고 있습니다. 그러나 규제 당국은 임상 현장에서의 광범위한 활용에 앞서 엄격한 검증을 요구하고 있으며, 인증된 방사선과 전문의와 정확도를 비교하는 공동 연구를 추진하고 있습니다. 초기 도입자들로부터 진단에 대한 확신도가 높아졌습니다는 보고가 있었으며, 숙련된 전문가의 부족이 우려되는 상황에서 이는 매우 중요한 장점입니다. 진료 보수가 여전히 검사 항목별로 결정되는 구조이기 때문에 품질을 저하시키지 않으면서 결과를 신속하게 도출해 주는 AI 도구는 경쟁 우위 요소에서 필수 요건으로 자리 잡을 것으로 예상되며, 이는 수의 감염증 진단 시장 전체 수요를 뒷받침하게 될 것입니다.

동물용 첨단 진단 장비

다중 PCR 및 카트리지 방식의 POC 시스템은 검사 시간을 며칠에서 몇 분으로 단축시켜, 이를 통해 진료소에서는 재진료를 피하고 항생제 오남용을 줄일 수 있습니다. 2025년에 개발된 돼지 호흡기 질환용 삼중 실시간 PCR 검사는 국가 기준과 100% 일치율을 달성하여 분자진단의 신뢰성을 입증하고 있습니다. 조에티스의 ‘Vetscan OptiCell’은 이러한 효율성을 10분 미만의 전혈구 계수 검사까지 확대하여, 진료소 내에서 검사 기관 수준의 정확도를 제공합니다. 가축 건강 관리 프로그램에 통합된 유전체 선별 도구는 질병에 대한 감수성과 항생제 의존도를 낮추며, 진단과 생산 지표의 개선을 직접적으로 연결합니다. 이러한 장비에 투자하는 동물병원에서는 고객 유지율을 높이고 프리미엄 서비스 요금을 청구할 수 있게 되어, 수의 감염증 진단 시장을 뒷받침하는 설비 투자 사이클이 강화되고 있습니다.

숙련된 수의사 부족

미국에서만 해도 2032년까지 7만 92명의 수의사가 부족할 것으로 예측되며, 졸업생 수는 5만 2,926명에 그칠 것으로 전망됩니다. 이러한 부족 현상은 지방에서의 이직이나 생활 방식의 선호로 인해 발생하고 있습니다. 특히 큰 타격을 받고 있는 분야는 대형 동물 진료 분야입니다. 가축을 전문으로 하는 수의사의 수는 제2차 세계대전 이후 90% 감소하여, 현재는 전체 수의사의 2% 미만을 차지할 뿐입니다. 임상의의 감소는 검사 의뢰 감소로 이어지고 있으며, 특히 외진 지역에서는 이동식 검사실이나 원격 진단을 통해 이를 보완해야 합니다. 검체 채취의 자동화 및 검사 결과 해석을 효율화하는 기술이 인력 부족을 일부 보완하고 있지만, 지속적인 인력 부족은 장기적인 검사 건수에 큰 부담으로 작용하여 수의 감염증 진단 시장의 성장을 둔화시키고 있습니다.

부문별 분석

면역 진단 분야는 일상적인 선별 검사에서 ELISA 및 화학발광법이 널리 보급되어 있는 덕분에, 2025년에도 매출 점유율 43.78%를 유지했습니다. 그럼에도 불구하고, 분자진단 분야는 가장 빠른 성장세를 기록하며 연평균 성장률(CAGR) 10.07%를 나타낼 것으로 예측되는데, 이는 정밀 의학으로의 광범위한 전환을 반영한 것입니다. 다중 PCR을 도입한 진료소에서는 판정 불가 결과가 줄어들고 항생제 오용이 감소하고 있는 것으로 보고되고 있으며, 이로 인해 고객의 신뢰가 높아지면서 수의 감염증 진단 시장에서의 고객 충성도가 강화되고 있습니다. 추출과 증폭 과정을 통합한 카트리지는 워크플로우를 간소화하여, 소규모 진료소에서도 이전에는 복잡했던 검사를 실시할 수 있게 해줍니다. 각 벤더사는 AI를 활용한 결과 해석 기능을 추가로 도입함으로써 오류율과 교육 부담을 줄이고 있습니다. 예측 기간 동안, 혈청학, PCR, 혈액학 기능을 통합한 워크스테이션이 신규 장비 구매의 주류를 이룰 것으로 예상되며, 이 분야의 융합 추세가 두드러지게 나타날 것입니다.

시장의 성장세는 병원체 발견 및 AMR(항생제 내성) 유전자 추적이 가능한 차세대 염기서열 분석(NGS)의 도입에서도 기인하고 있습니다. 검체당 비용은 여전히 높은 편이지만, 가축 군의 건강 관리에 풀 검사 전략을 적용함으로써 고부가가치 축산 사업에서 NGS를 경제적으로 실현할 수 있게 되었습니다. 클라우드 기반 바이오정보학은 On-Premise형 인프라의 필요성을 줄여주며, 자원이 제한된 지역에서의 도입을 촉진합니다. 면역 진단법은 고처리량 감시나 비용 효율성을 중시하는 환경에서 계속해서 활용될 것이지만, 수의 감염증 진단 시장 전반에 걸쳐 신속한 분자진단 플랫폼이 보급됨에 따라 그 점유율은 점차 감소할 것으로 예측됩니다.

2025년에는 반려동물의 ‘인간화’가 진전되고 보험 가입이 확대된 것을 배경으로, 반려동물이 전 세계 매출의 56.92%를 차지했습니다. 그러나 989년 미국 소 사육군에 영향을 미친 H5N1형 조류인플루엔자 젖소 발생 사례 등을 계기로 규제 당국이 엄격한 감시를 실시하는 가운데, 2031년까지 연평균 성장률(CAGR) 11.69%로 가장 빠르게 성장할 분야는 식용 동물 분야가 될 것으로 보입니다. 축산 농가들은 도태로 인한 손실이나 수출 금지를 피하기 위해, 가축 군 관리 절차에 진단 과정을 포함시키는 경향이 강해지고 있습니다. 정부의 감시 키트 보조금 지원으로 비용 측면의 장벽이 낮아지면서 축사 내 PCR 판독기 도입 기반이 확대되고 있으며, 이는 결과적으로 해당 부문의 수의 감염증 진단 시장 규모를 견인하고 있습니다.

유전체 선별은 질병 저항성 대립유전자를 특정함으로써 진단 기능을 강화하고, 장기적인 약제비 및 잔류 위험을 줄여줍니다. 병원체 검출과 유전자 프로파일링을 통합한 플랫폼은 생산자가 AMR(항생제 내성) 보고 의무 및 지속가능성 인증 요건을 준수하는 데 도움이 됩니다. 경제적 압박으로 인해 검사가 선택적으로 이루어지는 경향이 있지만, 반려동물 시장의 성장은 속도는 둔화되겠지만 지속될 전망입니다. 백신 접종과 진단을 결합한 패키지를 제공하는 동물병원은 비용에 민감한 시장에서도 진료 건수를 유지할 수 있으며, 수의 감염증 진단 시장에서 입지를 계속 지켜나갈 것입니다.

지역별 분석

북미는 성숙한 수의학 인프라, 높은 반려동물 보험 보급률, 그리고 가축 모니터링에 대한 꾸준한 자금 투입 덕분에 2025년에는 40.12%의 점유율로 수의 감염증 진단 시장을 주도했습니다. 연방 정부의 H5N1 대책 프로그램이 조류 및 소용 검사 패널에 대한 지속적인 수요를 촉진하여 소모품 매출을 유지하고 있습니다. 유럽도 이러한 추세를 따르고 있으며, 스웨덴 등 일부 국가에서는 엄격한 동물 복지 규제가 시행되고 있고, 거의 모든 반려견을 대상으로 하는 반려견 보험이 특징인데, 이러한 요소들이 종합적인 진단 방식의 보급을 뒷받침하고 있습니다. 또한, EU 전역의 AMR(항생제 내성)에 관한 지침 역시 분자진단 및 유전체 검사의 도입을 뒷받침하고 있습니다.

아시아태평양은 중국, 인도, 동남아시아의 가처분 소득 증가와 급속한 도시화에 힘입어 9.16%라는 가장 높은 연평균 성장률(CAGR)을 기록하며 두드러지고 있습니다. 정부 주도의 가축 현대화 프로그램에서는 지속적인 병원체 모니터링이 필요한 반면, 중산층 반려동물 주인들 사이에서는 서유럽식 예방 의료에 대한 수요가 높아지고 있어, 이로 인해 수의 감염증 진단 시장이 확대되고 있습니다. 규제 체계의 다양성과 가격에 대한 민감도를 고려할 때, 시장 침투를 위해서는 현지 유통업체와의 제휴 및 가격대에 맞춘 제품 라인의 구축이 필수적입니다. 라틴아메리카, 중동 및 아프리카에서는 가축 질병 대책 노력과 반려동물 사육 마릿수 증가로 인해 점진적인 성장이 예상되지만, 인프라의 제약으로 인해 그 잠재력을 최대한 발휘하기 위해서는 이동식 검사실이나 위성 네트워크 모델이 필요합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the veterinary infectious disease diagnostics market size is projected to expand from USD 2.31 billion in 2025 and USD 2.49 billion in 2026 to USD 3.73 billion by 2031, registering a CAGR of 8.39% between 2026 to 2031.

This report is Segmented by Technology (Immunodiagnostics, Molecular Diagnostics, and More), Animal Type (Companion Animals and Food-Producing Animals), Infection Type (Bacterial, Viral, and More), End User (Reference Laboratories, Veterinary Hospitals & Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Veterinary Infectious Disease Diagnostics Market Trends and Insights

AI-Powered Image Analysis Adoption In Vet Labs

AI integration is moving laboratory interpretation from subjective, manual review to data-driven automation. Platforms such as Zoetis' Vetscan Imagyst now screen lymph-node and skin-mass aspirates in minutes, a process that previously required days at external labs, enabling faster treatment decisions and improving client adherence. Nearly 30% of U.S. veterinarians already apply AI for imaging or record management tasks. Regulatory bodies, however, insist on rigorous validation before broad clinical use, promoting collaborative studies that benchmark AI accuracy against board-certified radiologists. Early adopters report sharper diagnostic confidence, a crucial benefit given the looming shortage of skilled practitioners. As reimbursements remain procedure-driven, AI tools that speed results without compromising quality are expected to shift from competitive advantage to baseline requirement, fuelling demand across the veterinary infectious disease diagnostics market.

Advanced Diagnostic Devices For Animals

Multiplex PCR and cartridge-based POC systems are compressing test windows from days to minutes, helping clinics avoid follow-up visits and reduce antibiotic misuse. A 2025 triplex real-time PCR assay for swine respiratory diseases achieved 100% agreement with national standards, underlining molecular reliability. Zoetis' Vetscan OptiCell extends this efficiency to complete blood counts in less than 10 minutes, offering reference-lab precision in-clinic. Genomic selection tools embedded within herd-health programs reduce disease susceptibility and antibiotic dependency, directly tying diagnostics to improved production metrics. Clinics that invest in such devices report higher client retention and the ability to charge premium service fees, reinforcing capital-investment cycles that sustain the veterinary infectious disease diagnostics market.

Shortage of Skilled Veterinarians

The United States alone is projected to lack 70,092 veterinarians by 2032, with only 52,926 graduates expected, a gap driven by rural attrition and lifestyle preferences. Large-animal practice is hardest hit; livestock-focused vets have declined 90% since World War II, now representing under 2% of the profession. Fewer clinicians limit test ordering, especially in remote areas where mobile labs or tele-diagnostics must compensate. Technology that automates sample collection or streamlines interpretation partly offsets manpower gaps, but sustained shortages weigh on long-term volumes and slow expansion of the veterinary infectious disease diagnostics market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Companion Animal Population

- One-Health AMR Surveillance Regulations

- High Pet-Care Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Immunodiagnostics retained a 43.78% revenue share in 2025 due to entrenched ELISA and chemiluminescent assays across routine screening. Nevertheless, molecular diagnostics recorded the quickest gains and are forecast to post a 10.07% CAGR, mirroring the broader shift toward precision medicine. Clinics adopting multiplex PCR report fewer inconclusive results and lower antibiotic misuse, boosting client confidence and strengthening loyalty within the veterinary infectious disease diagnostics market. Cartridges that integrate extraction and amplification simplify workflows, allowing smaller practices to perform formerly complex assays. Vendors further add AI-driven result interpretation, reducing error rates and training demands. Over the forecast window, integrated workstations that merge serology, PCR, and hematology functionalities are expected to dominate new-equipment purchases, underscoring the sector's convergence trend.

Market momentum also stems from next-generation sequencing (NGS) rollouts that enable pathogen discovery and AMR gene tracking. While cost per sample remains high, pooled testing strategies in herd health make NGS economically viable for high-value livestock operations. Cloud-based bioinformatics reduces on-premise infrastructure needs, fostering adoption across resource-constrained geographies. Immunodiagnostics will persist for high-throughput surveillance and cost-sensitive settings; however, their share is projected to decline gradually as rapid molecular platforms become ubiquitous across the veterinary infectious disease diagnostics market.

Companion animals generated 56.92% of global revenue in 2025, anchored by rising pet humanization and insurance uptake. Yet food-producing animals will expand fastest at 11.69% CAGR to 2031 as regulators impose stringent monitoring after incidents such as the H5N1 dairy-cattle outbreak that affected 989 U.S. herds. Livestock producers increasingly embed diagnostics in herd-health protocols to avoid culling losses and export bans. Governments subsidize surveillance kits, narrowing cost barriers and enlarging install bases for barn-side PCR readers, which, in turn, fuel the veterinary infectious disease diagnostics market size for this segment.

Genomic selection augments diagnostics by identifying disease-resistance alleles, reducing long-term medication costs and residue risks. Integrated platforms that merge pathogen detection with genetic profiling help producers comply with AMR-reporting mandates and sustainability certifications. Companion-animal growth will continue, albeit at a lower rate, as economic pressures spur selective testing behaviour. Clinics that offer bundled vaccination-plus-diagnostic packages should preserve volumes even in cost-sensitive markets, sustaining their position within the veterinary infectious disease diagnostics market.

Geography Analysis

North America led the veterinary infectious disease diagnostics market in 2025 with 40.12% share due to mature veterinary infrastructure, high pet-insurance penetration, and robust livestock surveillance funding. Federal H5N1 mitigation programs drive continual demand for avian and bovine panels, sustaining consumable sales. Europe follows closely, characterised by stringent welfare rules and near-universal canine insurance in nations like Sweden, which support comprehensive diagnostic uptake. Pan-EU AMR directives also bolster molecular and genomic test adoption.

Asia-Pacific stands out with the quickest 9.16% CAGR, fuelled by rising disposable incomes and rapid urbanisation in China, India, and Southeast Asia. Government-backed livestock modernisation programs require continuous pathogen monitoring, while middle-class pet owners increasingly demand Western-style preventive care, expanding the veterinary infectious disease diagnostics market. Partnerships with local distributors and price-tiered product lines are essential for penetration, given heterogeneous regulatory regimes and price sensitivity. Latin America, the Middle East, and Africa offer incremental growth via livestock disease-control initiatives and rising companion-animal ownership, but infrastructure limitations necessitate mobile-lab or satellite-network models to unlock full potential.

- IDEXX

- Zoetis

- Thermo Fisher Scientific

- bioMerieux

- Neogen

- Virbac

- Randox Laboratories

- INDICAL Bioscience

- ID Vet

- QIAGEN N.V

- Antech Diagnostics

- VCA Inc.

- GD Animal Health

- Eurofins Technologies

- QuidelOrtho (Vet Lab)

- Fujifilm Wako

- Mindray Bio-Medical (Vet)

- BioNote

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advanced Diagnostic Devices For Animals

- 4.2.2 Growing Demand For Pet Insurance

- 4.2.3 Increasing Companion Animal Population

- 4.2.4 AI-Powered Image Analysis Adoption In Vet Labs

- 4.2.5 One-Health AMR Surveillance Regulations

- 4.2.6 Tele-Veterinary Sample-Collection Networks

- 4.3 Market Restraints

- 4.3.1 High Pet-Care Costs

- 4.3.2 Shortage Of Skilled Veterinarians

- 4.3.3 Cross-Border Specimen Shipping Regulations

- 4.3.4 Data-Privacy Risks In Digital Lab Platforms

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Immunodiagnostics (ELISA, CLIA)

- 5.1.2 Molecular Diagnostics (PCR, RT-PCR, NGS)

- 5.1.3 Rapid / Point-of-Care Tests

- 5.1.4 Hematology & Clinical Chemistry

- 5.2 By Animal Type

- 5.2.1 Companion Animals

- 5.2.1.1 Canines

- 5.2.1.2 Felines

- 5.2.1.3 Equines

- 5.2.2 Food-Producing Animals

- 5.2.2.1 Bovine

- 5.2.2.2 Porcine

- 5.2.2.3 Poultry

- 5.2.2.4 Ovine & Caprine

- 5.2.1 Companion Animals

- 5.3 By Infection Type

- 5.3.1 Bacterial

- 5.3.2 Viral

- 5.3.3 Parasitic

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Reference Laboratories

- 5.4.2 Veterinary Hospitals & Clinics

- 5.4.3 Point-of-Care / In-house Testing

- 5.4.4 Research Institutes & Universities

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 IDEXX Laboratories

- 6.3.2 Zoetis Inc.

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 bioMerieux

- 6.3.5 Neogen

- 6.3.6 Virbac

- 6.3.7 Randox Laboratories

- 6.3.8 INDICAL Bioscience

- 6.3.9 ID Vet

- 6.3.10 QIAGEN N.V

- 6.3.11 Antech Diagnostics

- 6.3.12 VCA Inc.

- 6.3.13 GD Animal Health

- 6.3.14 Eurofins Technologies

- 6.3.15 QuidelOrtho (Vet Lab)

- 6.3.16 Fujifilm Wako

- 6.3.17 Mindray Bio-Medical (Vet)

- 6.3.18 BioNote

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment