|

시장보고서

상품코드

2064013

영국의 통합 시설 관리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

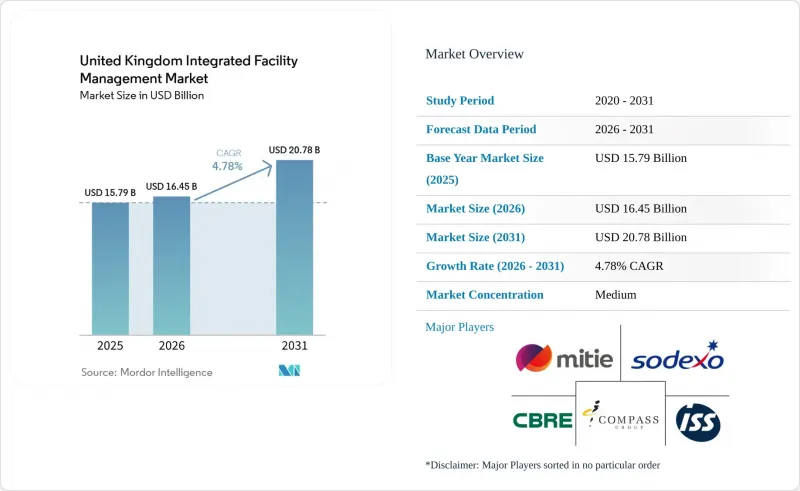

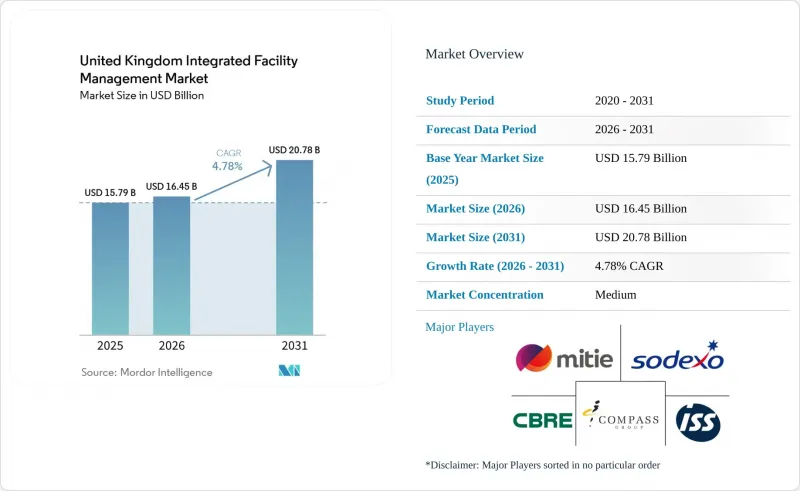

Mordor Intelligence에 의하면, 영국의 통합 시설 관리 시장 규모는 2025년에 157억 9,000만 달러로 평가되었고, 2026년 164억 5,000만 달러로 추정되고, 2031년까지 207억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 예측 기간 CAGR은 4.78%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(하드 시설 관리(자산 관리, MEP 및 HVAC 서비스 등), 소프트 시설 관리(사무 지원 및 보안, 청소 서비스, 케이터링 서비스 등)) 및 최종 사용자별(상업, 호텔 및 관광, 공공기관 및 공공 인프라 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

영국의 통합 시설 관리 시장 동향 및 인사이트

데이터센터 확장이 새로운 FM 수요 분야를 창출

2024년에 영국의 데이터센터가 중요 국가 인프라로 재분류됨에 따라, 가동 시간, 내결함성, 물리적 보안과 관련된 서비스에 대한 기대가 변화했습니다. 2025년 1월의 ‘AI 기회 행동 계획’은 디지털 역량 확대를 새로운 기술 시설 및 지원 인프라와 연계함으로써 그 방향성을 한층 더 강화했습니다. 영국의 통합 시설 관리 시장의 경우, 이는 수요가 24시간 체제의 M&E(기계·전기) 유지보수, 냉각 모니터링, 고전압 전기 관리, 소화 제어, 그리고 기밀성이 높은 환경을 위한 전문 청소 서비스로 이동하고 있음을 의미합니다. 2026년 2월 AECOM의 평가에 따르면, 런던에서 전문 기계·전기 및 공중위생 분야의 하도급업체에 대한 수요가 이미 공급을 초과하고 있다고 경고하고 있으며, 이는 주요 분야에서 수요가 노동력 공급을 얼마나 급속히 부족하게 만들고 있는지를 보여줍니다. 2024년 12월 CBRE가 Kao Data의 영국 포트폴리오 전체에서 수주한 프로젝트는 임차인들이 이러한 거점에서 하드 서비스와 소프트 서비스를 모두 관리할 수 있는 단일 공급업체를 점점 더 선호하고 있음을 보여줍니다. 이로 인해 영국의 통합 시설 관리 시장에서는 이미 중요한 환경 대응 역량을 갖춘 대규모 공급업체와, 아직 그러한 역량을 구축해야 하는 종합 서비스 제공업체 사이에 뚜렷한 양극화가 나타나고 있습니다.

스마트 빌딩의 IoT 및 CAFM 플랫폼이 생산성 기준을 높이고 있습니다.

영국의 통합 시설 관리(IFM) 시장은 IoT 센서, BMS 플랫폼, CAFM 시스템이 운영 중인 부동산 전반에서 더욱 긴밀하게 연계됨에 따라, 사후 대응형 작업 지시 모델에서 벗어나고 있습니다. ESOS 및 SECR은 정기적인 에너지 모니터링, 문서화 및 자산 수준의 가시화에 대한 필요성을 높이기 위해 이러한 변화를 지속적으로 뒷받침하고 있습니다. 2025년 8월 에든버러의 퀸 마가렛 대학교에서 도입된 IES 디지털 트윈을 통해, 저비용의 일정 조정 및 제어 변경을 통해 연간 6만 4,000파운드(8만 1,280달러), 즉, 해당 건물의 에너지 지출의 11%에 해당하는 에너지 절감 효과가 확인되었습니다. 또한, 고객사가 서비스 계약에 에너지 및 탄소 관련 KPI를 포함시키는 사례가 늘어나고 있으며, 이에 따라 지속가능성 보고는 독립적인 ESG 목표가 아닌 계약상의 성과 과제로 변화하고 있습니다. 2025년 하반기 조사 결과에 따르면, 많은 FM 리더는 여전히 규정 준수 업무의 상당 부분을 추적하거나 자동화하지 못하고 있으며, 이로 인해 보고 누락, 대응 누락, 계약 갱신 시 협의 부족과 같은 위험이 높아지고 있습니다. 영국의 IFM 시장에서는 실시간 데이터를 활용해 자산의 성과를 입증할 수 있는 공급업체들이 입찰 및 계약 갱신 과정에서 더욱 뚜렷한 우위를 점하고 있습니다.

기술 부족은 단순한 채용 문제가 아닙니다.

영국의 통합 시설 관리 시장은 단순히 채용 주기가 짧다는 점뿐만 아니라 구조적인 인력 부족에 직면해 있습니다. 이는 코로나19 사태 이후의 이직, 노동력의 고령화, 그리고 신규 시장 진출기업의 감소가 복합적으로 영향을 미치고 있기 때문입니다. 2025년 기준으로 FM 리더의 3분의 2 이상이 직원 채용 및 유지에 어려움을 겪고 있다고 응답했으며, 이는 서비스 수준 미달 및 일상적인 계약 관리의 약화로 직접 이어지고 있습니다. 이 문제의 기술적 측면은 더욱 심각합니다. 왜냐하면 HVAC, M&E 및 소방 시스템 업무의 경우, 직원이 독립적으로 업무를 수행할 수 있게 되기까지 전문적인 교육과 수년에 걸친 자격 취득 과정이 필요하기 때문입니다. 상업적인 영향은 심각합니다. 왜냐하면, 클라이언트는 계약을 평가할 때, 도급업체가 노력이나 의도를 보여줄 수 있는지 여부뿐만 아니라 실제 서비스 품질을 중시하기 때문입니다. 따라서, 인터넷 서비스 제공업체가 계약상 업무의 대부분을 여전히 수행하고 있더라도, 서비스에 대한 불만이나 계약이 갱신되지 않을 위험이 높아지고 있습니다. 영국의 IFM 시장에서는 탄탄한 교육 체계, 견습 제도 수용 능력, 우수한 스케줄링 시스템을 갖춘 기업들이 여전히 제한된 외부 인력에 의존하고 있는 기업들과의 격차를 점점 더 벌리고 있습니다.

부문별 분석

하드 FM은 영국 통합 시설 관리 시장에서 가장 빠르게 성장하고 있는 서비스 유형으로, 2026-2031년 연평균 성장률(CAGR) 5.38%를 나타낼 것으로 전망됩니다. 이러한 성장은 데이터센터, 생명과학 시설, NHS(국민보건서비스) 시설, 그리고 더욱 엄격한 안전 및 규정 준수 요건에 직면해 있는 노후화된 건물에서 기술적 요구 사항이 높아지고 있는 것과 관련이 있습니다. 건물 구조 공사, 공조 설비 유지보수, 고전압 전기 관리, 화재 안전 규정 준수는 모두 기술 및 문서화 측면에서 더욱 높은 요구 사항이 부과되고 있으며, 이로 인해 서비스의 복잡성과 인증 팀의 가치가 모두 높아지고 있습니다. M&A 동향도 비슷한 추세를 보였는데, 영국의 FM 분야에서 에너지 서비스 관련 거래는 2021-2024년 67% 증가한 반면, 2025년 FM 거래의 약 3분의 1은 화재 방지 시스템 및 엘리베이터 서비스가 차지했습니다. 배관 및 하드 서비스 도급업체의 기반도 여전히 탄탄하며, 관련 시장 규모는 2024년에 270억 파운드(343억 달러)를 넘어 2029년까지 325억 파운드(413억 달러)에 달할 것으로 전망됩니다.

2025년 기준으로 소프트 FM은 영국 통합 시설 관리(IFM) 시장 규모의 55.41%를 차지했으며, 이는 지속적인 현장 서비스가 여전히 영국 IFM 시장의 주요 기반을 형성하고 있음을 보여줍니다. 하이브리드 근무는 이러한 서비스에 대한 수요를 감소시킨 것이 아니라, 그 형태를 변화시켰습니다. 현재 청소는 입주 상황에 따라 이루어지고 있으며, 보안은 CCTV 및 출입 관리와 연계되는 경우가 늘어나고, 케이터링 서비스는 허브 앤 스포크 방식의 사무실 이용에 맞추어 재설계되고 있기 때문입니다. 2024년 11월 NHS Shared Business Services가 시작한 사업에는 리넨 및 세탁, 부지 관리, 보안이 포함되어 있으며, 그 총액은 3억 7,500만 파운드(4억 7,630만 달러)에 달할 전망입니다. 이는 공공 부문 수요가 얼마나 견고하고 대규모인지를 여실히 보여주고 있습니다. 또한, 공공 부문의 구매 담당자들은 감사, 안전 및 보건, 감염 예방 요건을 통해 진입 장벽을 높이고 있으며, 이로 인해 성숙한 관리 시스템과 공공 부문에서의 실적을 갖춘 공급업체에게 우위가 생기고 있습니다. 통합 시설 관리 업계에서는 이에 따라 소프트 FM이 규모의 기반이 되고, 하드 FM은 대체 수단이 아닌 기술적 성장 동력으로서의 역할을 맡게 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the united kingdom integrated facility management market size was valued at USD 15.79 billion in 2025 and is estimated to grow from USD 16.45 billion in 2026 to reach USD 20.78 billion by 2031, at a CAGR of 4.78% during the forecast period 2026-203.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Integrated Facility Management Market Trends and Insights

Data Centre Expansion is Creating a New FM Demand Category

The 2024 reclassification of UK data centers as critical national infrastructure changed the service expectations around uptime, resilience, and physical security. January 2025 AI Opportunities Action Plan reinforced that direction by linking digital capacity expansion to new technical facilities and supporting infrastructure. For the United Kingdom integrated facility management market, this means demand is shifting toward round-the-clock M&E maintenance, cooling oversight, high-voltage electrical management, fire suppression controls, and specialist cleaning for sensitive environments. A February 2026 AECOM assessment warned that specialist mechanical, electrical, and public health subcontractor demand was already outstripping supply in London, which shows how quickly critical-environment demand is tightening labor capacity. CBRE's December 2024 appointment across Kao Data's UK portfolio showed that occupiers increasingly want one provider that can manage both hard and soft services across these sites. This leaves the UK integrated facility management market with a clear divide between scaled providers that already have critical-environment capability and generalists that still need to build it.

Smart Building IoT and CAFM Platforms are Raising the Productivity Baseline

The United Kingdom integrated facility management (IFM) market is moving away from a reactive work-order model as IoT sensors, BMS platforms, and CAFM systems become more closely connected across occupied estates. ESOS and SECR continue to support that shift because both frameworks increase the need for regular energy monitoring, documentation, and asset-level visibility. An IES digital twin deployment at Queen Margaret University in Edinburgh, which began in August 2025, identified annual energy savings of GBP 64,000 (USD 81,280), or 11% of the building's energy spend through low-capital scheduling and control changes. Clients are also writing energy and carbon KPIs into service agreements more often, which turns sustainability reporting into a contract performance issue rather than a separate ESG ambition. Late 2025 survey evidence showed that many FM leaders still had a large share of compliance tasks untracked or unautomated, which raises the risk of poor reporting, missed actions, and weak renewal discussions. In the United Kingdom IFM market, providers that can prove asset performance with live data are gaining a clearer edge in tenders and renewals.

Skills Shortage is More Than a Recruitment Problem

The United Kingdom integrated facility management market faces a structural labor gap rather than a short hiring cycle, because the issue now combines post-COVID attrition, an ageing workforce, and weak new entrant volumes. More than two-thirds of FM leaders said in 2025 that recruiting and retaining staff was difficult, and this fed directly into missed service levels and weaker day-to-day contract control. The technical side of the problem is even sharper, because HVAC, M&E, and fire systems roles need specialist training and multi-year qualification paths before staff can work independently. The commercial effect is severe because clients judge contracts on live service quality, not only on whether the contractor can point to effort or intent. That is why service complaints and non-renewal risk are rising even where providers are still delivering most contracted tasks. In the United Kingdom IFM market, the firms with stronger training pipelines, apprenticeship capacity, and better scheduling systems are pulling away from those that still rely on a thin external labor pool.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Procurement Consolidation is Compressing the Supplier Base

- Public Sector Estate Backlog is Driving Non-Discretionary FM Demand

- Cost Escalation in Hard FM Is Eroding Contract Profitability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard FM is the fastest-growing service type in the United Kingdom integrated facility management market, with a projected 5.38% CAGR over 2026-2031. That growth is tied to higher technical intensity across data centers, life sciences sites, NHS estates, and older buildings that now face firmer safety and compliance requirements. Building fabric work, HVAC servicing, high-voltage electrical management, and fire safety compliance are all becoming more demanding in skill and documentation, which lifts both service complexity and the value of accredited teams. Deal activity points in the same direction, because energy services transactions in UK FM M&A rose by 67% between 2021 and 2024, while fire systems and lift services made up nearly one-third of 2025 FM deals. The plumbing and hard services contractor base also remains large, with an adjacent market valued at more than GBP 27 billion (USD 34.3 billion), in 2024 and projected to reach GBP 32.5 billion (USD 41.3 billion) by 2029.

Soft FM held 55.41% of the United Kingdom integrated facility management market size in 2025, which shows that recurring frontline services still form the volume base of the United Kingdom IFM market. Hybrid working has changed the pattern of those services rather than reduced their needs, because cleaning is now more occupancy-led, security is increasingly layered with CCTV and access control, and catering is being redesigned around hub-and-spoke office use. November 2024 NHS Shared Business Services launch covered linen and laundry, grounds maintenance, and security with a combined value of GBP 375 million (USD 476.3 million), underlining how institutional demand remains steady and large. Public-sector buyers are also raising entry thresholds through audit, health and safety, and infection-control requirements, which gives an advantage to providers with mature management systems and repeat public-sector experience. Within the integrated facility management industry, this leaves Soft FM as the scale anchor and Hard FM as the technical growth engine rather than a substitute.

List of Companies Covered in this Report:

- Mitie Group plc

- ISS Facility Services Ltd.

- Sodexo Limited

- CBRE Group, Inc.

- Compass Group PLC

- Equans UK and Ireland

- Integral UK Ltd.

- Atalian Servest Group Ltd.

- VINCI Facilities

- Kier Group plc

- G4S Limited

- OCS Group Limited

- Bouygues Energies and Services UK

- Serco Group plc

- EMCOR UK

- Bellrock Property and Facilities Management Ltd.

- Skanska UK Plc

- Aramark UK Ltd.

- JLL Integrated Facilities Management UK

- Sodexo Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outsourcing of Non-Core Activities Among U.K. Corporates

- 4.2.2 Energy-Efficiency Compliance Under U.K. Net-Zero Mandate

- 4.2.3 Growth of Data Centers Driving Specialized FM Demand

- 4.2.4 Rise of Performance-Based IFM Contracts in Public Sector

- 4.2.5 Adoption of Smart Building IoT Platforms for Predictive FM

- 4.2.6 Increased Private Equity Consolidation in Mid-Tier FM Firms

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Tradespeople for MEP Services

- 4.3.2 Inflation-Linked Cost Pressures on Soft FM Margins

- 4.3.3 Cyber-Security Risks in Connected Building Systems

- 4.3.4 Post-Brexit Labor Mobility Constraints

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Segmentation by Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 Segmentation by End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mitie Group plc

- 6.4.2 ISS Facility Services Ltd.

- 6.4.3 Sodexo Limited

- 6.4.4 CBRE Group, Inc.

- 6.4.5 Compass Group PLC

- 6.4.6 Equans UK and Ireland

- 6.4.7 Integral UK Ltd.

- 6.4.8 Atalian Servest Group Ltd.

- 6.4.9 VINCI Facilities

- 6.4.10 Kier Group plc

- 6.4.11 G4S Limited

- 6.4.12 OCS Group Limited

- 6.4.13 Bouygues Energies and Services UK

- 6.4.14 Serco Group plc

- 6.4.15 EMCOR UK

- 6.4.16 Bellrock Property and Facilities Management Ltd.

- 6.4.17 Skanska UK Plc

- 6.4.18 Aramark UK Ltd.

- 6.4.19 JLL Integrated Facilities Management UK

- 6.4.20 Sodexo Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment