|

시장보고서

상품코드

2064014

독일의 통합 시설 관리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

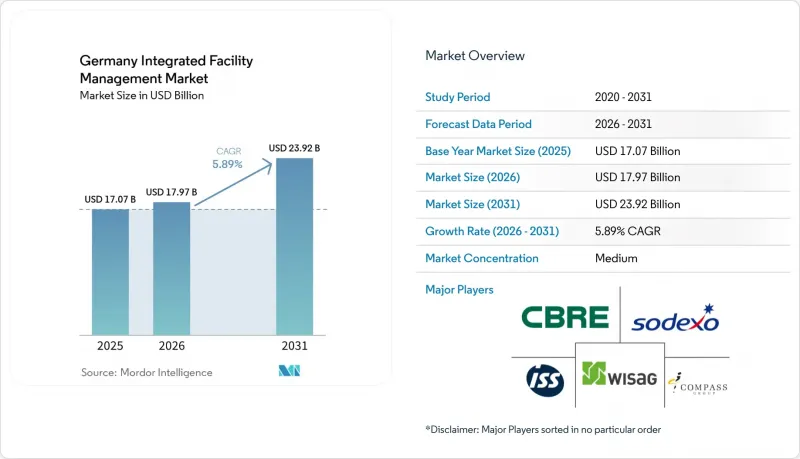

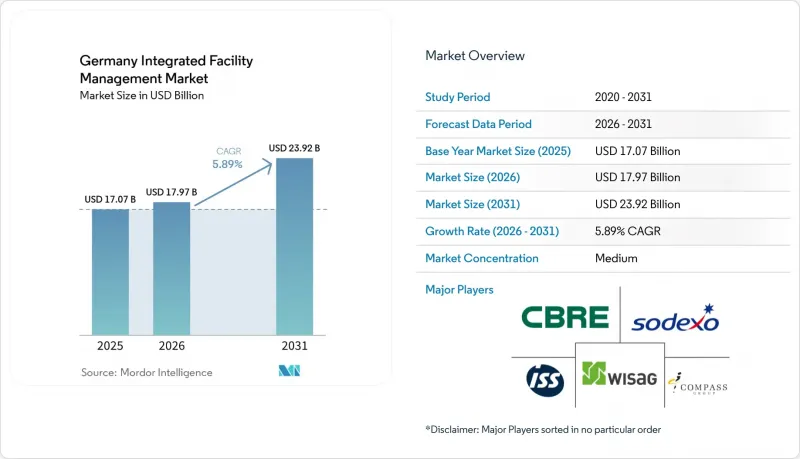

Mordor Intelligence에 의하면, 독일의 통합 시설 관리 시장 규모는 2025년 170억 7,000만 달러로 평가되었고, 2026년에는 179억 7,000만 달러로 추정되고, 2031년까지 239억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.89%로 성장할 전망입니다.

본 보고서는 서비스 유형별(하드 시설 관리(자산 관리, MEP 및 HVAC 서비스 등), 소프트 시설 관리(사무 지원 및 보안, 청소 서비스, 케이터링 서비스 등)) 및 최종 사용자 산업별(상업, 호스피탈리티, 헬스케어, 공공기관 및 공공 인프라 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

독일의 통합 시설 관리 시장 동향과 인사이트

강화되는 에너지 효율 규제와 지속가능성

에너지 규제는 규정 준수 의무를 일회성 설치 프로젝트가 아닌 지속적인 운영 업무로 전환시키기 때문에 독일 IFM 시장에서 가장 뚜렷한 단기 성장 요인으로 작용하고 있습니다. GEG 제71a조는 290kW를 초과하는 냉난방 또는 환기 시스템을 갖춘 비주거용 건물에 대해 2024년 12월 31일까지 인증된 빌딩 자동화 및 제어 시스템의 도입을 의무화하고 있으며, 이에 따라 사무실, 공장, 병원, 대학, 소매 시설 등 기술 기반 FM 제공업체의 잠재 고객 기반이 확대되었습니다. 이러한 시스템이 도입된 후에도 건물 소유주는 성능 모니터링, 에너지 데이터 분석, 제어 시스템 유지보수, 개방형 인터페이스를 통한 정기적인 운영 기록 작성 등을 수행할 수 있는 서비스 제공업체가 필요합니다. 이로 인해 계약의 가치는 단순한 기본 유지보수 업무의 범위를 넘어섭니다. 이러한 규정 준수 열풍은 독일 국내에만 그치지 않습니다. 2024년 EPBD(에너지 성능 지침) 및 공공 건축물에 적용되는 관련 에너지 효율 의무에 따라, 소유주는 더욱 엄격한 건축물 성능 기준과 더 우수한 운영 규율을 준수해야 하기 때문입니다. 이로 인해 현장 엔지니어링, 소프트웨어 기반 모니터링, 에너지 최적화를 단일하고 책임 있는 서비스 체계 하에 통합할 수 있는 기업들에게 독일의 통합 시설 관리 시장은 더욱 매력적인 시장이 되고 있습니다.

데이터센터의 성장이 전문적인 하드 FM 수요를 견인하고 있습니다.

데이터센터는 일반적인 상업용 건물 계약으로는 쉽게 구현할 수 없는 가동 시간을 중시하는 서비스 모델을 필요로 하기 때문에 독일의 통합 시설 관리 시장의 기술적 한계를 넓혀가고 있습니다. 독일의 데이터센터 설치 용량은 2025년에 약 3000MW에 달할 것으로 보이며, 2030년까지 국내 용량은 더욱 확대될 것으로 예측됩니다. 이로 인해 냉각, 전력 배전, 화재 예방, 유지보수 계획 및 연중무휴 24시간 사고 대응에 대한 지속적인 수요가 발생하고 있습니다. 구글은 2026-2029년 독일에서 55억 유로(64억 달러) 규모의 투자 프로그램을 시행할 예정입니다. 이 프로그램은 주요 사업자들이 여전히 신규 사이트 개설 및 에너지 효율 향상에 주력하고 있음을 보여주며, 디지털 인프라 분야에서 향후 기술적 시설 관리(FM) 수요의 파이프라인을 확대하는 계기가 될 것입니다. AI 중심 환경에서의 랙 밀도는 기존의 HVAC 계약으로는 효율적으로 관리할 수 없는 수준을 넘어서는 추세입니다. 따라서, 인터넷 서비스 제공업체는 경쟁력을 유지하기 위해 액체 냉각에 대한 지식, DCIM 통합 능력, 그리고 폐열 규제에 대한 대응 전문 지식이 필요합니다. 따라서 독일 IFM 시장의 이 분야에서는 전문 엔지니어링 팀, 신속한 대응 체계, 그리고 중요 환경에서의 운영 역량에 조기에 투자하는 기업이 유리한 입지를 차지하게 됩니다.

FM 인력의 만성적인 부족과 임금 상승

독일의 통합 시설 관리 시장에서 인력 확보는 여전히 주요 실행 위험 요인으로 남아 있습니다. 이는 소프트웨어 서비스와 하드웨어 서비스 양 분야에서 수요 증가 속도가, 서비스 제공업체가 자격을 갖춘 직원을 채용·육성·유지하는 속도를 앞지르고 있기 때문입니다. 독일 빌딩 청소 업계 보고서에 따르면, 45.3%의 기업이 인력 부족을 이유로 신규 수주를 정기적으로 거절하고 있으며, 47.4%의 기업이 인력 부족으로 인해 최대 10%의 수익 손실을 입고 있다고 응답했습니다. 이는 노동력 부족이 단순히 비용을 상승시킬 뿐만 아니라, 이미 서비스 제공 자체를 제한하고 있음을 보여줍니다. 이러한 압박은 초급 직종에만 국한된 것이 아닙니다. 자동화 지원, 기술적 시설 관리(FM), 데이터센터 운영 분야에서도 확보하기 어렵고 유지 비용도 높은 전문 기술을 갖춘 인력이 요구되고 있기 때문입니다. 2025년 3월에 발생한 Charite Facility Management의 노사 분쟁은 임금 조정이 연간 인건비를 급격히 상승시켜 대규모 포트폴리오 전체에 걸쳐 계약 가격 재검토나 이익률 축소를 불가피하게 만들 수 있음을 보여주었습니다. 그 결과, 독일의 통합 시설 관리 시장의 서비스 제공업체들은 고객의 강력한 수요와 이를 신뢰할 수 있는 서비스 수준으로 충족시키기 위해 필요한 인력 사이에서 해소하기 어려운 격차를 겪고 있습니다.

부문별 분석

2025년, 소프트 시설 관리 부문은 독일 통합 시설 관리 시장 점유율의 61.64%를 차지했으며, 독일의 상업 및 산업, 공공시설 건물 인프라 전반에 걸쳐 타 부문을 압도적인 차이로 제치고 최대 서비스 그룹으로서의 위상을 유지했습니다. 이러한 규모는 청소, 급식, 안내, 폐기물 처리, 부지 관리에서 비롯된 것으로, 이 모든 업무는 일상적인 건물 운영에 필수적이며, 고급 부동산부터 노후 건물에 이르기까지 모든 부동산에서 필요로 하고 있습니다. 서비스 기반은 광범위하고 지속적이며 노동 집약적이기 때문에 대형 사업자는 전국 규모의 계약에서 일상 업무를 패키지화함으로써, 설비 투자 주기가 둔화되더라도 안정적인 수익 흐름을 유지할 여지가 있습니다. 그렇긴 하지만, 독일의 통합 시설 관리 시장은 노동 집약적인 패키지 계약에서 소프트 서비스와 기술적 감독, 보고 요건, 지속가능성과 연계된 성과 지표를 결합한 계약으로 점차 전환되고 있습니다. 이러한 변화가 중요한 이유는 고객들이 개별 서비스를 관리하는 여러 개의 단편적인 공급업체가 아니라, 여러 거점으로 구성된 포트폴리오 전체에 걸쳐 시설 기준을 일관되게 관리할 수 있는 책임감 있는 단일 운영 파트너를 점점 더 많이 찾고 있기 때문입니다.

하드 시설 관리(Hard Facility Management)는 독일 통합 시설 관리 시장에서 가장 빠르게 성장하고 있는 서비스 부문이며, 독일 통합 시설 관리 시장 규모는 2031년까지 연평균 성장률(CAGR) 6.59%로 확대될 것으로 전망됩니다. 가장 큰 견인 요인은 빌딩 자동화의 의무화, 에너지 개보수 프로그램, 중요 환경 관리, 그리고 비주거용 부동산 전반에 걸쳐 기술 자산의 규정 준수, 효율성 및 디지털 가시성을 유지해야 하는 광범위한 요구에 있습니다. GEFMA의 보고서에 따르면, 독일의 부동산 관련 FM 소프트웨어 시장은 2025년에 12.8% 성장했으며, 공급업체의 70%가 CAFM 또는 IWMS 도구를 제공하고 있었습니다. 이는 기술 서비스 제공이 과거보다 훨씬 더 소프트웨어 기반의 모니터링과 체계적인 작업 지시 관리에 의존하고 있음을 보여줍니다. 실무 측면에서 볼 때, 독일의 통합 시설 관리 업계는 기본적인 유지보수에서 특히 첨단 제어 시스템을 갖춘 건물에 있어 데이터 품질, 가동 시간 확보 및 에너지 성능을 핵심으로 하는 서비스 모델로 전환되고 있습니다. 소규모 기술 전문 업체들도 여전히 유용한 틈새 시장을 차지하고 있지만, 독일의 통합 시설 관리 시장에서는 엔지니어, 디지털 시스템, 24시간 서비스 제공을 단일 계약 구조 내에서 통합할 수 있는 공급업체에 대한 평가가 높아지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the germany integrated facility management market size is expected to increase from USD 17.07 billion in 2025 to USD 17.97 billion in 2026 and reach USD 23.92 billion by 2031, growing at a CAGR of 5.89% over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Healthcare, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Integrated Facility Management Market Trends and Insights

Rising Energy Efficiency Regulations and Sustainability

Energy regulation is the clearest near-term growth force in the Germany IFM market because it turns compliance obligations into recurring operating work rather than one-time installation projects. GEG Section 71a required non-residential buildings with heating, cooling, or ventilation systems above 290 kW to install certified building automation and control systems by December 31, 2024, which widened the addressable base for technical FM providers across offices, factories, hospitals, universities, and retail assets. Once these systems are in place, building owners still need providers that can monitor performance, interpret energy data, maintain controls, and produce regular operating records through open interfaces, which lifts contract value above basic maintenance work. The compliance cycle also extends beyond Germany because the 2024 EPBD and related energy efficiency obligations in public buildings keep pushing owners toward tighter building performance standards and better operating discipline. This makes the Germany integrated facility management market more attractive for firms that can combine field engineering, software-enabled monitoring, and energy optimization within one accountable service structure.

Growth Of Data Centers Fueling Specialized Hard FM Demand

Data centers are pushing the technical edge of the Germany integrated facility management market because they require uptime-focused service models that standard commercial building contracts cannot easily replicate. Germany reached ~3000 MW of installed data center capacity in 2025, and national capacity is expected to expand further by 2030, which creates recurring demand for cooling, power distribution, fire protection, maintenance planning, and 24/7 incident response. Google's EUR 5.5 billion (USD 6.40 billion) investment program in Germany for 2026-2029. The program underlines how large operators are still adding new sites and upgrading energy profiles, which extends the pipeline for future technical FM demand in digital infrastructure. Rack densities in AI-oriented environments are moving beyond levels that conventional HVAC contracts can manage efficiently, so providers need liquid cooling knowledge, DCIM integration capability, and waste heat compliance expertise to stay relevant. This part of the Germany IFM market therefore favors firms that invest early in specialized engineering teams, faster response structures, and operational depth in critical environments.

Persistent FM Talent Shortage and Wage Inflation

Labor availability remains the main execution risk in the Germany integrated facility management market because demand growth is arriving faster than providers can recruit, train, and retain qualified staff across soft and hard services. Germany's building cleaning trade reported that 45.3% of firms regularly turned away new orders because they lacked staff, while 47.4% said the shortage caused revenue losses of up to 10%, which shows how labor scarcity is already limiting service delivery rather than only raising costs. The pressure is not limited to entry-level roles because automation support, technical FM, and data center operations also require workers with specialized skills that are harder to source and more expensive to keep. The Charite Facility Management labor dispute in March 2025 showed how wage alignment can sharply raise annual labor costs and force contract repricing or margin compression across large portfolios. As a result, providers in the Germany integrated facility management market face a persistent gap between strong client demand and the labor base needed to deliver it at reliable service levels.

Other drivers and restraints analyzed in the detailed report include:

- ESG-Driven Outsourcing to Achieve Scope 3 Emission Reductions

- Sustainability and Procurement Initiatives by German Companies

- Volatile Energy Prices Pressuring FM Contract Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management segment held 61.64% of the Germany integrated facility management market share in 2025, which kept it as the largest service group by a clear margin across the country's commercial, industrial, and institutional building base. That scale comes from cleaning, catering, reception, waste handling, and grounds maintenance, all of which remain embedded in day-to-day building operations and are required across both premium assets and older building stock. The service base is broad, recurring, and labor intensive, which gives larger operators room to bundle routine activities across national contracts and maintain steady revenue flows even when capital spending cycles soften. Even so, the Germany integrated facility management market is gradually moving beyond labor-heavy bundles toward contracts that connect soft services with technical oversight, reporting requirements, and sustainability-linked performance measures. That change matters because clients increasingly want one accountable operating partner that can manage site standards consistently across multi-location portfolios rather than several fragmented vendors with separate service controls.

Hard facility management is the fastest-growing service category in the Germany integrated facility management market, and its Germany integrated facility management market size is projected to expand at a 6.59% CAGR through 2031. The strongest pull comes from building automation mandates, energy retrofit programs, critical environment management, and the broader need to keep technical assets compliant, efficient, and digitally visible across non-residential properties. GEFMA reported that Germany's real estate-related FM software market grew 12.8% in 2025, while 70% of providers offered CAFM or IWMS tools, which shows how technical service delivery now depends far more on software-enabled monitoring and coordinated work-order management than in the past. In practical terms, the Germany integrated facility management industry is moving from basic maintenance toward service models built around data quality, uptime assurance, and energy performance, especially in buildings with more advanced controls. Smaller technical specialists still hold useful niches, but the Germany integrated facility management market increasingly rewards providers that can combine engineers, digital systems, and round-the-clock service coverage within one contract structure.

List of Companies Covered in this Report:

- ISS A/S

- Sodexo SA

- Compass Group PLC

- Dussmann Stiftung & Co. KGaA

- Wisag Facility Service Holding GmbH

- Gegenbauer Holding SE & Co. KG

- SPIE Deutschland & Zentraleuropa GmbH

- Strabag PFS GmbH

- Hectas Facility Services Stiftung & Co. KG

- Apleona GmbH

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- Engie SA

- Cofely Deutschland GmbH

- Gegenbauer Holding SE & Co. KG

- WISAG Sicherheit & Service Holding GmbH & Co. KG

- KOTTER Services

- Sasse Group

- Kluh Service Management GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainability-Linked Procurement Mandates by German Corporates

- 4.2.2 Aging Commercial Real Estate Stock Requiring Retrofit FM Solutions

- 4.2.3 Rising Energy-Efficiency Regulations in Bundeslander

- 4.2.4 Growth of Data Centers Fueling Specialized Hard FM Demand

- 4.2.5 Expansion of Integrated FM Bundling by Global FM Providers

- 4.2.6 ESG-Driven Outsourcing to Achieve Scope 3 Emission Reductions

- 4.3 Market Restraints

- 4.3.1 Persistent FM Talent Shortage and Wage Inflation

- 4.3.2 Volatile Energy Prices Pressuring FM Contract Margins

- 4.3.3 Fragmented Regulatory Codes Across Federal States

- 4.3.4 Limited Digital Maturity in Mid-Sized German Enterprises

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industries

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ISS A/S

- 6.4.2 Sodexo SA

- 6.4.3 Compass Group PLC

- 6.4.4 Dussmann Stiftung & Co. KGaA

- 6.4.5 Wisag Facility Service Holding GmbH

- 6.4.6 Gegenbauer Holding SE & Co. KG

- 6.4.7 SPIE Deutschland & Zentraleuropa GmbH

- 6.4.8 Strabag PFS GmbH

- 6.4.9 Hectas Facility Services Stiftung & Co. KG

- 6.4.10 Apleona GmbH

- 6.4.11 CBRE Group Inc.

- 6.4.12 Jones Lang LaSalle Incorporated

- 6.4.13 Cushman & Wakefield plc

- 6.4.14 Engie SA

- 6.4.15 Cofely Deutschland GmbH

- 6.4.16 Gegenbauer Holding SE & Co. KG

- 6.4.17 WISAG Sicherheit & Service Holding GmbH & Co. KG

- 6.4.18 KOTTER Services

- 6.4.19 Sasse Group

- 6.4.20 Kluh Service Management GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment