|

시장보고서

상품코드

2064377

직원 경험 플랫폼 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Employee Experience Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

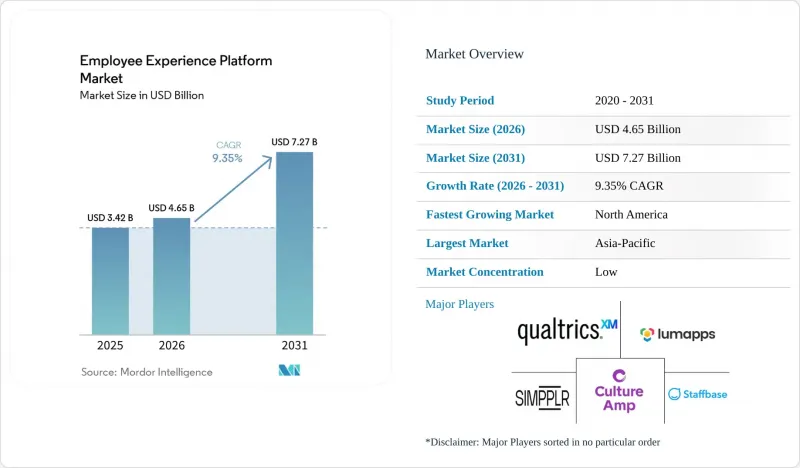

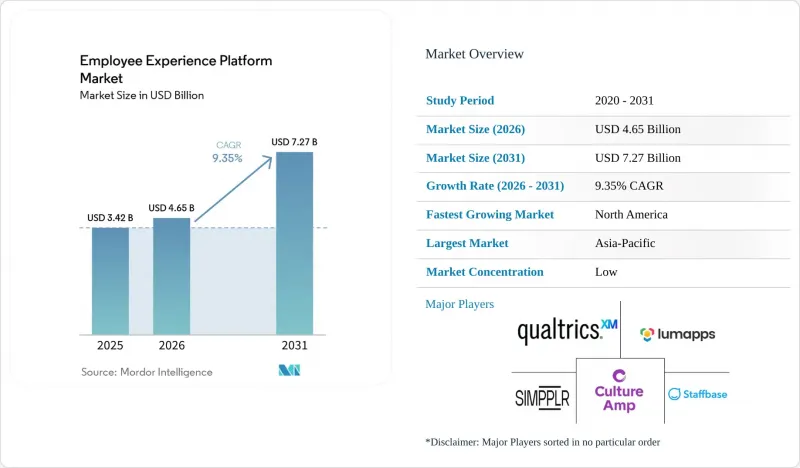

Mordor Intelligence에 의하면, 직원 경험 플랫폼 시장 규모는 2025년에 34억 2,000만 달러로 평가되었고, 2026년에 46억 5,000만 달러로 추정되며, 2031년까지 72억 7,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 9.35%로 성장할 것으로 전망됩니다.

본 보고서는 배포 방식별(클라우드 기반, 온프레미스 등), 기업 규모별(중소기업, 대기업), 용도별(직원 간 커뮤니케이션 및 협업, 직원 참여도 제고 및 시상 등), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), 의료, IT 및 통신 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 직원 경험 플랫폼 시장 동향 및 고찰

하이브리드 및 분산형 근무 방식의 정착

하이브리드 근무 방식은 대기업에서 표준적인 업무 모델로 자리 잡았으며, 직원 경험 플랫폼 시장은 일시적인 도입 열풍이 아니라 업무 공간의 재설계와 밀접하게 연결되어 있습니다. 2025년 전 세계 조사 결과에 따르면, 고용주의 88%가 어떤 형태로든 하이브리드 근무를 제공하고 있는 반면, 협업 기술에 충분한 투자를 하고 있는 곳은 불과 32%에 그치고 있어, 플랫폼 공급업체가 메워야 할 분명한 격차가 남아 있습니다. 이 조사에 따르면, 직원의 90%가 협업 도구를 중요하게 여기고 있으며, 77%는 엄격한 사무실 복귀 의무를 원격 근무의 생산성에 대한 신뢰 부족의 표현으로 보고 있는 것으로 나타났습니다. 이러한 격차로 인해 인사(HR) 및 IT 팀은 지사 간 소통, 피드백, 접근성을 개선할 수 있는 공유 플랫폼 도입을 추진해야 하는 상황에 놓여 있습니다. 직원 경험 플랫폼 시장은 유럽에서 은퇴로 인한 인력 부족 압박의 영향으로 혜택을 보고 있습니다. DACH 지역에서는 2030년대 중반까지 1,290만 명의 베이비붐 세대가 정년퇴직을 맞이할 것으로 예상되며, 이에 따라 인재 유지를 위한 인프라의 가치가 높아지고 있습니다. 그 결과, 구매자들은 직원 경험 도구를 단순한 참여 유도 소프트웨어가 아닌, 인력 유지 계획의 일환으로 인식하게 되었습니다.

AI를 활용한 개인 맞춤화 및 직원용 셀프 서비스

AI를 활용한 개인 맞춤화를 통해 플랫폼은 수동적인 설문조사 도구에서 요청을 전달하고 컨텐츠를 추천하며 일반적인 인사 업무를 실시간으로 해결하는 능동적인 시스템으로 전환되고 있습니다. 이러한 변화가 중요하게 여겨지는 이유는 조직이 현재 업무용 도구에 대해 일상적인 업무 흐름에서 더 빠르고, 관련성이 높으며, 사용하기 편리하기를 기대하고 있기 때문입니다. 한 플랫폼의 사례에 따르면, 2024년에 1,150만 건 이상의 문의를 처리하여 그중 94%를 시스템 내에서 해결했을 뿐만 아니라, 35억 달러 규모의 생산성 향상을 통한 비용 절감에 기여함으로써, 적절하게 구축된 셀프 서비스 모델이 가져다주는 가치의 규모를 입증하고 있습니다. 이러한 성과들은 직원 경험 플랫폼 시장에서 구매자의 기대치를 형성하고 있습니다. 특히, 지원 인력을 증원하지 않은 채 더 많은 직원을 관리해야 한다는 압박에 시달리고 있는 인사팀에게는 이는 매우 중요합니다. 또한, 이러한 성과는 자동화를 새로운 위험을 초래하지 않으면서 확대할 수 있도록, 벤더 측에 개인화 기능과 거버넌스 제어 기능을 연계할 것을 요구하고 있습니다. 그 결과, 청취 기능, 워크플로우 자동화, AI를 활용한 셀프 서비스를 단일 운영 계층에 통합한 플랫폼에 대한 수요가 높아지고 있습니다.

데이터 개인정보 보호와 시스템 간 통합의 복잡성

데이터 개인정보 보호 및 통합의 복잡성으로 인해 직원 경험 플랫폼 시장의 성장은 여전히 더딘 양상을 보이고 있습니다. 특히, 플랫폼이 여러 시스템에서 동시에 감정, 행동, 성과 데이터를 수집하는 경우에 두드러집니다. 유럽의 구매자들은 AI를 활용한 청취 및 분석 기능에 대해 더욱 엄격한 심사 기준을 적용하고 있으며, 이로 인해 도입 전 법적 및 기술적 검증 기간이 길어지고 있습니다. 또한, HRIS, 협업, 급여, 성과 관리, 보안 시스템은 직원 데이터를 서로 다른 형식이나 권한 설정으로 저장하는 경우가 많기 때문에 통합 작업은 많은 구매자가 당초 예상했던 것보다 부담이 커지고 있습니다. 이로 인해 많은 프로젝트가 시범 운영 단계에서 전사적 도입 단계로 전환되는 과정에서 지연이 발생합니다. 이러한 영향은 국경을 넘어 사업을 전개하는 조직에서 가장 두드러지며, 데이터 저장 위치, 로컬 호스팅, 그리고 직원 대표 위원회의 기대 사항이 모두 도입 설계에 영향을 미칩니다. ‘프라이버시 바이 디자인’의 제어 기능과 보다 간결한 통합 프레임워크를 제공하는 벤더는 이러한 제약을 조달상의 우위로 전환하는 데 있어 유리한 입장에 있습니다.

부문별 분석

2025년 기준으로 클라우드 기반 플랫폼은 직원 경험 플랫폼 시장의 67.42%를 차지했으며, 이는 분산된 팀을 지원하고 현대적인 HR 시스템 간에 지속적인 데이터 교환이 이루어지도록 할 필요성을 반영하고 있습니다. 클라우드 도입은 보다 신속한 업데이트, 손쉬운 통합, 그리고 지점을 초월한 광범위한 접근을 가능하게 함으로써, 직원 경험 플랫폼 시장의 현재 추세와 부합합니다. 또한, 실시간 데이터 흐름에 기반한 AI를 활용한 청취, 워크플로우 자동화 및 분석 기능에 대해 벤더가 더욱 견고한 기반을 제공합니다. 이러한 장점은 커뮤니케이션, 피드백, 평가, 지원 도구를 단일 통합 아키텍처를 통해 운영하고자 하는 조직에게 특히 중요합니다. 온프레미스 구축도 여전히 중요하지만, 엄격한 네트워크 분리나 극히 특수한 내부 통제가 클라우드 모델의 유연성을 능가하는 제한적인 사례로 점점 더 국한되고 있습니다.

하이브리드 모델은 연평균 성장률(CAGR) 11.38%를 기록하며 가장 빠르게 성장하고 있는 모델로, 이는 구매자들이 여전히 기밀성이 높은 직원 데이터의 저장 위치에 대해 더 큰 통제권을 원하고 있음을 보여줍니다. 규제 산업과 대기업들이 데이터 상주 요건과 클라우드 기반 분석 수요 간의 균형을 모색하는 가운데, 하이브리드 환경을 위한 직원 경험 플랫폼 시장이 확대되고 있습니다. 이는 현지 호스팅을 선호하는 경향이 계속해서 조달 설계에 영향을 미치고 있는 유럽 시장에서 특히 두드러집니다. 그 방향성은 여전히 ‘클라우드 우선’이지만, 이는 ‘어떤 대가를 치르더라도 오로지 클라우드만’을 의미하는 것이 아니라, 보다 강력한 거버넌스 체계를 갖춘 ‘클라우드 우선’입니다.

2025년, 대기업은 직원 경험 플랫폼 시장의 62.19%를 차지했습니다. 이는 사업 부문, 지역, 다층적인 보고 체계를 아우르는 대규모 직원을 관리해야 할 필요성을 반영한 것입니다. 이러한 조직에서는 일반적으로 HRIS(인사 정보 시스템), 학습 관리, 급여 계산, 성과 평가, ID 관리 시스템과의 긴밀한 통합이 요구되며, 이로 인해 도입 범위와 비용 모두 증가하게 됩니다. 이러한 복잡성은 더 강력한 도입 역량, 폭넓은 제품군, 그리고 명확한 거버넌스 관리 체계를 갖춘 공급업체에게 유리하게 작용합니다. 또한, 신규 구매자들이 시장에 진입하고 있음에도 불구하고 대기업이 여전히 직원 경험 플랫폼 시장의 주요 수익 기반으로 남아 있는 이유도 바로 여기에 있습니다. 대부분의 경우, 이러한 조직들은 단순히 하나의 기능을 구매하는 것이 아니라, 커뮤니케이션, 의견 수렴, 표창 및 관리자의 업무 흐름을 하나로 연결하는 통합 시스템을 구매하고 있는 것입니다.

중소기업은 가장 빠르게 성장하고 있는 부문으로, 2031년까지의 연평균 성장률(CAGR)은 12.74%로 예측되며, 이는 비용 및 도입 장벽이 점차 완화되고 있음을 보여줍니다. 직원 경험 플랫폼 시장에서 중소기업을 대상으로 한 시장 규모는 확대되고 있으며, 모듈식 클라우드 네이티브 제품이 직원 수 100-2,000명 규모의 기업들이 시장에 진입하는 데 따르는 장벽을 낮추고 있습니다. 이러한 인수 기업들은 특히 과거 소규모 기업들이 비공식적인 기업 문화를 주요 인재 유지 수단으로 삼았던 업계에서 치열해지는 경쟁과 높아지는 직원들의 기대에 부응하고자 하고 있습니다. 단일 제품 아키텍처로 엔터프라이즈 시장과 중견 시장의 요구를 모두 충족시킬 수 있는 벤더는 별도의 플랫폼을 구축하지 않고도 사업을 확장할 수 있는 견고한 입지를 확보하고 있습니다.

지역별 분석

2025년, 북미는 직원 경험 플랫폼 시장 점유율의 36.91%를 차지했으며, 최대의 지역 클러스터가 되었습니다. 이 지역은 기업 소프트웨어의 높은 도입률, 성숙한 HR 기술 기반, 그리고 하이브리드형 및 지식 집약형 인력을 지원하는 벤더들이 밀집해 있다는 이점을 누리고 있습니다. 미국이 여전히 주요 수익원인 한편, 고용주들이 북미 전역의 사업에서 플랫폼 표준화를 추진하는 가운데, 캐나다와 멕시코가 성장을 뒷받침했습니다. 이 시장 수요 역시 기본적인 참여도 조사에서 이직 예측, AI를 활용한 관리자용 도구, 그리고 보다 광범위한 인력 분석으로 점차 전환되고 있습니다. 기술 서비스, 비즈니스 서비스, 금융 및 보험 업계는 하이브리드 근무 도입률이 가장 높은 업계 중 하나로, 플랫폼을 활용한 직원 간 소통 및 협업에 대한 수요를 뒷받침하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 14.87%로, 가장 빠르게 성장이 전망되는 지역입니다. 아시아태평양 시장 규모는 기업의 급속한 디지털화, 모바일 우선 인력 전략, 그리고 제조, 소매, 물류 분야의 현장 직원들에 대한 막대한 미충족 수요를 배경으로 확대되고 있습니다. 인도의 거대한 IT 서비스 기반은 참여도와 성과 향상을 위한 도구 도입을 지속적으로 뒷받침하고 있는 반면, 중국과 한국에서는 현장용 커뮤니케이션 플랫폼에 대한 관심이 높아지고 있습니다. 이러한 지역적 추세로 인해, 사무실 중심의 도입에 그치지 않는 보다 광범위한 성장 기반이 시장에 마련되고 있습니다.

유럽은 독일, 영국, 프랑스, 네덜란드, 스페인의 견인 덕분에 여전히 2위 지역 클러스터의 위치를 유지하고 있습니다. 이 분야가 두드러지는 이유는 구매 결정 과정에서 직원 경험, 데이터 거버넌스 및 보고 요구 사항이 점점 더 밀접하게 연결되고 있기 때문입니다. ESRS S1 프레임워크는 근로 조건, 교육, 다양성, 웰빙에 초점을 맞춘 직원 정보 공개를 규정하고 있으며, 이에 따라 직원 데이터를 일관되게 수집·정리할 수 있는 시스템에 대한 수요가 증가하고 있습니다. 남미는 여전히 개발도상국 시장이며, 브라질과 아르헨티나에서는 금융 및 전문 서비스 분야에서 활발한 움직임이 나타나고 있습니다. 중동에서는 노동력 현지화 프로그램과 대기업 주도의 프로젝트가 증가함에 따라 체계적인 온보딩 및 커뮤니케이션의 필요성이 대두되면서 관련 투자가 확대되고 있습니다. 한편, 아프리카는 여전히 초기 단계에 있으며, 남아프리카공화국과 나이지리아가 국경을 넘어 사업을 전개하는 기업들에게 주요 진출 거점으로 자리 잡고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the employee experience platform market size is projected to be USD 3.42 billion in 2025, USD 4.65 billion in 2026, and reach USD 7.27 billion by 2031, growing at a CAGR of 9.35% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premises, and More), Enterprise Size (Small and Medium-Sized Enterprises, and Large Enterprises), Application (Employee Communication and Collaboration, Employee Engagement and Recognition, and More), End-User Industry (BFSI, Healthcare, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Employee Experience Platform Market Trends and Insights

Hybrid And Distributed Work Normalization

Hybrid work has become a standard operating model across large employers, tying the employee experience platform market to workplace redesign rather than a short-lived adoption wave. A 2025 global study found that 88% of employers offered some form of hybrid work, while only 32% invested adequately in collaboration technology, leaving a clear gap for platform vendors to fill. The same study showed that 90% of employees value collaboration tools and 77% view strict return-to-office mandates as a sign of low trust in remote productivity. This gap is pushing HR and IT teams to support shared platforms that improve communication, feedback, and access across locations. The employee experience platform market is also benefiting from retirement-driven labor pressure in Europe, where 12.9 million baby boomers in the DACH region are moving toward retirement through the mid-2030s, which raises the value of retention infrastructure. As a result, buyers are treating employee experience tools as part of workforce continuity planning, not just as engagement software.

AI-Powered Personalization And Employee Self-Service

AI personalization is moving platforms away from passive survey tools and toward active systems that route requests, recommend content, and resolve common HR tasks in real time. This shift matters because organizations now expect workplace tools to feel faster, more relevant, and easier to use across daily workflows. A platform example showed it handled more than 11.5 million interactions in 2024, resolving 94% of them within the system, and contributed USD 3.5 billion in productivity savings, demonstrating the scale of value that well-built self-service models can unlock. These results are shaping buyer expectations inside the employee experience platform market, especially where HR teams are under pressure to serve larger workforces without adding support headcount. They are also pushing vendors to connect personalization features with governance controls so that automation can scale without creating new risk. The result is a stronger demand for platforms that combine listening, workflow automation, and AI-assisted self-service into a single operating layer.

Data Privacy And Cross-System Integration Complexity

Data privacy and integration complexity continue to slow the employee experience platform market, especially when platforms pull sentiment, behavioral, and performance data from many systems at once. Buyers in Europe are applying stricter review standards to AI-enabled listening and analytics features, which extends legal and technical validation before rollout. Integration work is also heavier than many buyers first expect, because HRIS, collaboration, payroll, performance, and security systems often store workforce data in different formats and under different permissions. This creates delays at the point where many projects move from pilot use into enterprise-wide deployment. The effect is strongest in organizations that operate across borders, where data residency, local hosting, and works council expectations all shape implementation design. Vendors that offer privacy-by-design controls and cleaner integration frameworks are better placed to convert this restraint into a procurement advantage.

Other drivers and restraints analyzed in the detailed report include:

- Board-Level Focus On Retention And Productivity Metrics

- Frontline Workforce Digitization

- ROI Attribution And Change Fatigue

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based platforms held 67.42% of the employee experience platform market share in 2025, which reflects the need to support distributed teams and continuous data exchange across modern HR systems. Cloud deployment aligns with the current direction of the employee experience platform market by enabling faster updates, easier integration, and broader access across locations. It also provides vendors with a stronger foundation for AI-enabled listening, workflow automation, and analytics features that depend on real-time data flow. That advantage is especially important for organizations that want communication, feedback, recognition, and support tools to operate through one connected architecture. On-premises deployments remain relevant, but they are increasingly tied to narrow cases where strict network isolation or highly specific internal controls outweigh the flexibility of cloud models.

Hybrid deployment is the fastest-growing model, with a 11.38% CAGR, indicating that buyers still want greater control over where sensitive workforce data is stored. The employee experience platform market for hybrid deployment is growing as regulated industries and large enterprises seek to balance data residency requirements with the need for cloud-based analytics. This is especially visible in European markets where local hosting preferences continue to shape procurement design. The direction of travel is still cloud-first, but it is cloud-first with stronger governance layers rather than cloud-only at any cost.

Large enterprises captured 62.19% of the employee experience platform market in 2025, which reflects their need to manage large workforces across business units, geographies, and layered reporting structures. These organizations typically require deep integration with HRIS, learning, payroll, performance, and identity systems, which raises both the scope and cost of deployment. That complexity favors vendors with stronger implementation capacity, broader product suites, and clearer governance controls. It also explains why large enterprises remain the core revenue base of the employee experience platform market even as new buyers enter. In many cases, these organizations are not buying a single feature but a connected system that ties communication, listening, recognition, and manager workflows together.

Small and medium-sized enterprises are the fastest-growing cohort, with a CAGR of 12.74% through 2031, indicating that cost and setup barriers are easing. The employee experience platform market size for SMEs is growing as modular cloud-native products lower entry thresholds for companies with 100-2,000 employees. These buyers are responding to tighter labor competition and higher employee expectations, especially in sectors where smaller firms once depended on informal culture as their main retention tool. Vendors that can serve enterprise and mid-market needs with a single product architecture are in a stronger position to expand without building separate platforms.

Geography Analysis

North America held 36.91% of the employee experience platform market share in 2025, making it the largest regional cluster. The region benefits from high enterprise software adoption, a mature HR technology base, and a dense concentration of vendors serving hybrid and knowledge-based workforces. The United States remained the main revenue center, while Canada and Mexico supported expansion as employers standardized platforms across North American operations. Demand in this part of the market is also moving from basic engagement surveys toward predictive attrition, AI-supported manager tools, and broader workforce analytics. Technology services, business services, and finance and insurance had among the highest hybrid adoption rates, supporting continued demand for platform-enabled employee communication and coordination.

Asia-Pacific is the fastest-growing region with a CAGR of 14.87% through 2031. Market size in Asia-Pacific is rising on the back of rapid enterprise digitization, mobile-first workforce strategies, and significant unmet demand among frontline workers in manufacturing, retail, and logistics. India's large IT services base continues to support the adoption of engagement and performance tools, while China and South Korea are driving stronger interest in frontline communication platforms. This regional pattern provides the market with a broader growth base beyond office-led deployments.

Europe remained the second-largest regional cluster, supported by Germany, the United Kingdom, France, the Netherlands, and Spain. The region stands out because workforce experience, data governance, and reporting needs are becoming more closely linked in buying decisions. The ESRS S1 framework keeps workforce disclosures focused on working conditions, training, diversity, and well-being, which reinforces demand for systems that can collect and organize employee data more consistently. South America is still a developing market, with Brazil and Argentina showing stronger activity in financial and professional services. The Middle East is seeing more investment as workforce localization programs and large-employer projects increase the need for structured onboarding and communication, while Africa remains early-stage, with South Africa and Nigeria serving as the main entry points for cross-border employers.

- Qualtrics, LLC

- Culture Amp Pty Ltd

- Perceptyx, Inc.

- Medallia, Inc.

- WorkTango Inc.

- Achievers Solutions Inc.

- Lattice, Inc.

- 15Five, Inc.

- Quantum Workplace, Inc.

- Motivosity, Inc.

- Staffbase GmbH

- Simpplr Inc.

- LumApps SAS

- Unily Group Ltd.

- MangoApps Inc.

- Haiilo GmbH

- Firstup, Inc.

- Appspace Inc.

- Akumina, Inc.

- Powell Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid and Distributed Work Normalization

- 4.2.2 AI-Powered Personalization and Employee Self-Service

- 4.2.3 Board-Level Focus on Retention and Productivity Metrics

- 4.2.4 Frontline Workforce Digitization

- 4.2.5 CSRD and ESRS S1 Workforce Disclosure Readiness

- 4.2.6 Skills Graphs and Internal Talent Mobility Orchestration

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-System Integration Complexity

- 4.3.2 ROI Attribution and Change Fatigue

- 4.3.3 EU AI Act and Works Council Limits on Monitoring Features

- 4.3.4 Suite Bundling and Ecosystem Lock-In Pressure

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud-based

- 5.1.2 On-premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Small and Medium-sized Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Application

- 5.3.1 Employee Communication and Collaboration

- 5.3.2 Employee Engagement and Recognition

- 5.3.3 Employee Listening and Survey Analytics

- 5.3.4 Employee Wellbeing and Support

- 5.3.5 Other Applications

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 IT and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Qualtrics, LLC

- 6.4.2 Culture Amp Pty Ltd

- 6.4.3 Perceptyx, Inc.

- 6.4.4 Medallia, Inc.

- 6.4.5 WorkTango Inc.

- 6.4.6 Achievers Solutions Inc.

- 6.4.7 Lattice, Inc.

- 6.4.8 15Five, Inc.

- 6.4.9 Quantum Workplace, Inc.

- 6.4.10 Motivosity, Inc.

- 6.4.11 Staffbase GmbH

- 6.4.12 Simpplr Inc.

- 6.4.13 LumApps SAS

- 6.4.14 Unily Group Ltd.

- 6.4.15 MangoApps Inc.

- 6.4.16 Haiilo GmbH

- 6.4.17 Firstup, Inc.

- 6.4.18 Appspace Inc.

- 6.4.19 Akumina, Inc.

- 6.4.20 Powell Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment