|

시장보고서

상품코드

2064398

AI 기반 인력 계획 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)AI-Powered Workforce Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

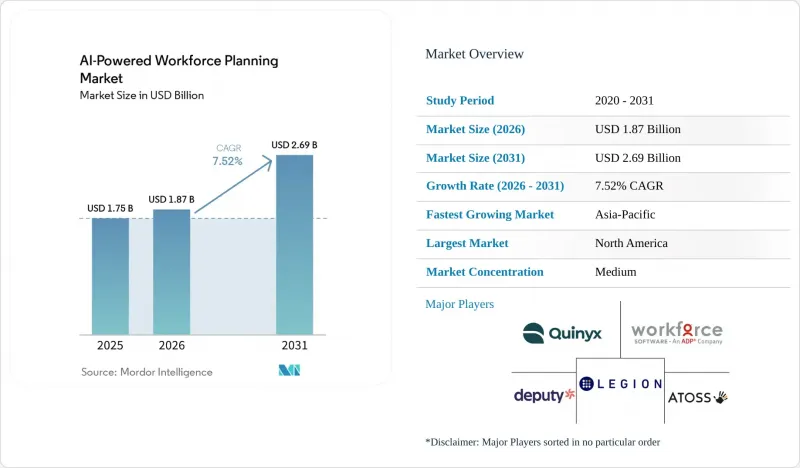

Mordor Intelligence에 의하면, AI 기반 인력 계획 시장 규모는 2025년 17억 5,000만 달러에서 2026년에는 18억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 7.52%로 성장을 지속하여, 2031년에는 26억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 소프트웨어 유형(인력 스케줄링·계획, 인력 분석 등), 도입 형태(클라우드 및 On-Premise), 조직 규모(대기업 및 중소기업), 최종 사용자 산업 분야(정부·공공 부문 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 AI 기반 인력 계획 시장 동향 및 인사이트

자율형 AI 조종사가 기업의 계획 주기를 단축

AI 기반 인력 계획 시장은 단순한 지원형 AI 도구의 범위를 넘어, 데이터 연동, 시나리오 실행, 그리고 인적 개입을 최소화한 조치 제안을 가능하게 하는 자율형 시스템으로 전환되고 있습니다. 2025년 및 2026년 제품 출시 일정은 자율적인 계획 워크플로가 실험적인 시범 단계에 머무르지 않고, 주요 인사 관리 소프트웨어의 로드맵에 점차 반영되고 있음을 보여줍니다. Legion은 2026년 1월에 90건 이상의 AI 인재 관리 혁신 사례를 발표했으며, Eightfold는 2026년 5월에 TalentForge를 도입하여 기업들이 자사의 인재 인텔리전스 레이어 위에서 맞춤형 HR 용도를 구축할 수 있도록 했습니다. 이러한 변화로 인해, 특히 인력 예측, 일정, 기술 데이터를 동시에 업데이트해야 하는 경우, 계획상의 과제와 운영상의 대응 간의 격차가 줄어듭니다. 또한, 구매자들이 정기적인 보고보다는 지속적인 계획 수립을 점점 더 기대하게 됨에 따라, 여전히 속도가 느리고 수동 검토가 수반되는 일괄 처리 워크플로우에 의존하고 있는 공급업체들은 압박을 받고 있습니다. 거버넌스가 일상적인 계획 수립 과정에 통합되어 있을 때에만, 고속 자동화가 AI 기반 인력 계획 시장을 뒷받침할 수 있으므로, 기업에는 여전히 강력한 오버라이드 규칙과 감사 가능한 워크플로가 필요합니다.

하이브리드 및 분산형 인력 환경에서 데이터 기반 인력 배치의 필요성

하이브리드 및 분산형 근무 모델의 등장으로 인해, AI 기반 인력 계획 시장에서 정적인 인력 현황에 대한 스냅샷의 유용성은 크게 떨어지고 있습니다. 구매자들은 거점, 팀, 직원 유형을 아우르는 인력 배치 수준, 일정, 사내 이동, 노동 수요, 예산 제약에 대해 실시간 가시성을 점점 더 필요로 하고 있습니다. SD Worx의 보고서에 따르면, 유럽 기업의 48.2%가 2026년의 우선 과제로 인력 계획을 선정한 주된 이유로 일정 관리의 효율화와 적절한 인력 배치를 꼽았습니다. 이러한 추세는 많은 고용주들이 단순히 디지털 실험을 하기 위해서가 아니라, 일상 업무의 연속성과 서비스 수준을 유지하기 위해 이러한 도구를 도입하고 있음을 보여줍니다. Oracle의 Fusion Cloud HCM에 내장된 AI 에이전트 역시, 공급업체가 사내 인사 이동, 경력 개발, 후계자 계획, 급여 계산의 이상 감지를 단일 통합 워크플로우로 통합하고 있음을 보여줍니다. 하이브리드 근무 형태가 정착되는 가운데, 인재의 가용성과 비즈니스 수요를 연결하는 플랫폼은 AI 기반 인력 계획 시장에서 그 입지를 공고히 하고 있습니다.

HR AI 모델의 데이터 개인정보 보호, 설명 가능성 및 편향 위험

AI 모델이 업무 배분, 성과 평가, 직원 모니터링 또는 역량 추론에 영향을 미치는 경우, 규정 준수 관련 압박은 AI 기반 인력 계획 시장에 여전히 실질적인 걸림돌로 작용하고 있습니다. EU AI법은 직장에서의 AI 활용 사례 중 일부를 고위험으로 분류하고 있으며, 도입 전에 구매자가 보다 엄격한 문서화, 모니터링 및 관리, 그리고 설명 책임 체계를 갖추도록 요구하고 있습니다. 미국에서는 캘리포니아주의 FEHA(공정 고용 및 주택법) 의무나 뉴욕시의 연례 편견 감사 요건 등의 규제로 인해, 기업들은 구매를 승인하기 전에 편견 테스트, 기록 보관 및 감사 가능한 의사결정 기록을 요구해야 하는 상황에 놓여 있습니다. 이러한 의무는 도입 비용을 증가시키며, 특히 전담 거버넌스 팀을 갖추지 않은 중소 벤더의 경우 판매 주기를 길어지게 하는 요인이 됩니다. 또한, 설명 가능성이 단순한 규정 준수 차원의 선택적 기능이 아니라 구매의 핵심 기준이 되어가고 있기 때문에 제품 설계에도 영향을 미치고 있습니다. 그 결과, 규제가 엄격한 환경에서는 도입 속도가 둔화되고 있지만, 한편으로 대형 벤더들은 거버넌스 체제 구축을 무기로 삼아 AI 기반 인력 계획 시장에서 차별화를 꾀하고 있습니다.

부문별 분석

2025년 기준으로, AI 기반 인력 계획 시장의 63.12%를 소프트웨어가 차지하고 있으며, 이는 스케줄링, 분석 및 계획 플랫폼이 기업 도입에 있어 여전히 핵심 기술 계층으로 자리 잡고 있음을 보여줍니다. 이 비율은 많은 벤더들이 채택하고 있는 ‘제품 주도형’ 구조를 반영하고 있으며, 소프트웨어 구독을 통해 고객 기반이 확립된 후, 서비스 업무를 통해 팀 및 지역 전체로 확대해 나가는 흐름을 보여줍니다. 그럼에도 불구하고 서비스 부문은 2031년까지 연평균 성장률(CAGR) 10.41%를 나타낼 것으로 예측되며, 이는 구성 부문 중 가장 빠른 성장 속도로서 도입이 점점 더 복잡해지고 있는 분야임을 보여줍니다. 소프트웨어의 규모와 서비스의 성장 사이에 발생하는 격차는 구매자가 더 이상 단순한 도구만을 구매하는 것이 아니라 설정, 거버넌스 지원, 운영 지원까지 함께 구매하고 있음을 시사합니다. 이러한 경향은 AI 기반 인력 계획 시장이 규칙 기반의 자동화에서 모델 주도형 계획 수립 및 지속적인 인력 인텔리전스로 전환됨에 따라 더욱 두드러지고 있습니다.

벤더가 노동 규정, 노동조합 조건, 산업 분류 등 플랫폼을 효과적으로 활용하기 전에 현지에서 설정이 필요한 업종이나 국가로 사업을 확장함에 따라 서비스 수요는 더욱 증가할 것입니다. ATOSS는 2024 회계연도에 3,590만 유로(3,880만 달러)의 컨설팅 매출을 기록하며 전년 대비 8% 증가했으나, 이러한 증가의 일부는 의료 및 물류 분야의 더 복잡한 시스템 도입에 기인한 것으로 분석됩니다. AI 기반 인력 계획 업계에서 이 결과는 많은 첨단 계획 및 스케줄링 이용 사례에서 제품 중심의 온보딩만으로는 여전히 불충분함을 보여줍니다. 또한, 서비스 계층은 가동 후 사라지는 일시적인 도입의 가교가 아니라, 계속해서 의미 있는 수익원이 될 수 있음을 의미합니다. 확장성이 뛰어난 소프트웨어와 강력한 설정, 통합, 변경 지원 기능을 결합할 수 있는 공급업체는 AI 기반 인력 계획 시장에서 보다 지속 가능한 수익을 창출할 가능성이 높을 것입니다.

2025년 기준으로 소프트웨어 유형별 부문에서 근태 관리가 37.14%를 차지했으나, 워크포스 애널리틱스는 2031년까지 연평균 성장률(CAGR) 9.33%를 나타낼 것으로 예측되며, 이는 관리 기능에서 의사결정 지원으로의 전환을 반영한 것입니다. 많은 기업 고객의 경우, 규정 준수, 근로 규정, 급여 계산과의 연동 및 일정 실행이 여전히 플랫폼 선정의 기준이 되고 있기 때문에 근태 관리는 계속해서 핵심적인 위치를 차지하고 있습니다. 워크포스 애널리틱스의 확대가 가속화되고 있는 이유는 구매자들이 워크포스 데이터를 비용, 위험, 기술 가용성 및 수용 능력과 관련된 의사결정에 연계할 수 있는 시스템을 점점 더 많이 요구하고 있기 때문입니다. 이로 인해 소프트웨어 예산 체계가 변화하고 있습니다. 왜냐하면 계획 도구는 단순한 인사 용도으로서뿐만 아니라 운영 인텔리전스 계층으로서도 평가받고 있기 때문입니다. AI 기반 인력 계획 시장에서 이러한 업그레이드 주기는 기본적인 기록 관리 기능보다 예측 및 처방 기능으로 더 많은 가치를 이동시키고 있습니다.

일정 관리, 휴가·결근 관리, 성과 관리 등의 트랜잭션 모듈은 일상 업무와 밀접하게 연관되어 있으며, 단기간 내에 대체하기 어렵기 때문에 여전히 널리 사용되고 있습니다. 다음 투자 단계에서는 이러한 모듈을 기반으로, 출근 현황, 성과, 인력 배치에 대한 신호를 통합된 계획 화면에서 해석하는 분석 도구로 전환하고 있습니다. Orgvue는 2025년 12월, 자동화된 역할 그룹화 및 조직 데이터용 자연어 어시스턴트를 포함한 ‘Henshaw AI 제품군’을 출시했습니다. 이로 인해 수작업에 소요되는 시간이 몇 개월에서 몇 분으로 단축되었습니다. 이러한 기능은 역할 클러스터링 속도를 높이고, 스킬 매핑의 정확도를 향상시키며, 용량 격차가 사업 연속성에 영향을 미치기 전에 이를 조기에 감지할 수 있게 해줍니다. 그 결과, AI 기반 인력 계획 시장에서는 운영 데이터를 단순한 정적 보고서가 아닌, 미래를 내다보는 계획적인 조치로 전환할 수 있는 벤더가 높이 평가받고 있습니다.

지역별 분석

2025년, 북미는 AI 기반 인력 계획 시장의 38.56%를 차지하며, 이 시장에서 가장 큰 비중을 차지하는 지역이 되었습니다. 이는 초기 단계부터 시작된 기업용 AI 투자, 성숙한 클라우드 HCM의 도입, 그리고 더욱 견고한 소프트웨어 조달 주기를 반영한 것입니다. 미국은 여전히 그 지위의 핵심을 차지하고 있습니다. 이는 대규모 의료 시스템, 기술 기업, 소매업체들이 분산된 인력과 복잡한 근무 모델을 아우르며 막대한 계획 수요를 안고 있기 때문입니다. 병원들은 여전히 높은 이직 비용을 감당하고 있으며, 인재 유출을 억제하기 위해 더욱 정밀한 인력 배치 예측과 스케줄링 관리가 필요하기 때문에 의료 시스템 내의 인력 문제는 여전히 특히 중요한 과제로 남아 있습니다. 캘리포니아주의 FEHA(공정 고용 및 주택법) 규정과 뉴욕시의 연례 편견 감사 요건 역시, 보다 명확한 관리 기능, 강력한 감사 대응 능력, 그리고 문서화된 의사결정 논리를 갖춘 플랫폼에 대한 수요를 촉진하고 있습니다. 국경을 초월한 인력의 가시화와 지역 간 노동력 조정이 기업의 노동력 전략에서 그 중요성이 커짐에 따라, 캐나다와 멕시코에서도 규모는 작지만 점차 확대되고 있는 수요가 더해지고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.67%를 기록하며 성장할 것으로 예상되며, AI 기반 인력 계획 시장에서 가장 빠르게 성장하는 지역이 될 것입니다. 이 지역의 성장은 중국의 기업용 AI 프로그램, 인도의 거대한 기술 서비스 기반, 그리고 고령화되는 노동력 구조 속에서 노동력 부족을 보다 엄격하게 관리해야 할 필요성이 있는 일본에 의해 주도되고 있습니다. 또한, 특히 기술 및 비즈니스 서비스 분야에서 광범위한 사업 거점에 걸쳐 있는 정규직, 계약직, 긱 워커 간의 조정이 필요하다는 점도 수요를 뒷받침하고 있습니다. 호주 및 뉴질랜드, 일본, 한국 및 기타 아시아태평양이 지역적 기반을 확대하고 있으며, 특히 한국에서는 전자 및 반도체 업계의 스케줄링 활용 사례에서 초기 진전이 나타나고 있습니다.

유럽은 AI 기반 인력 계획 시장에서 중요한 위치를 차지하고 있지만, 이 지역에서의 도입은 다른 몇몇 지역에 비해 더 엄격한 규정 준수 요건과 더 신중한 거버넌스 심사를 거쳐 이루어지고 있습니다. 워크데이(Workday)는 2026년 3월, 독일 기업의 41%가 2025년에 직원의 60% 이상이 AI 도구를 사용했다고 보고했으며, 이는 DACH 지역 전체에서 직장에서의 AI 보급률이 높음을 보여줍니다. 또한, 이와 같은 환경에서는 고용주가 AI 기반 인력 배치를 대규모로 도입하기 전에, 공동 결정 및 감시와 관련된 우려 사항을 해결해야 합니다. 남미에서는 도입이 아직 초기 단계에 있으며, 브라질의 금융 서비스 및 기술 부문이 점차 증가하는 수요를 뒷받침하고 있습니다. 한편, 중동에서는 보다 광범위한 디지털 전환 노력의 일환으로 AI 기반 인력 배치가 이루어지고 있습니다. 아프리카는 아직 개발도상국이지만, 남아프리카공화국이나 나이지리아 등 시장에서 금융 서비스 및 통신 업계가 AI 기반 인력 배치 시장에 초기 진입 기회를 창출하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

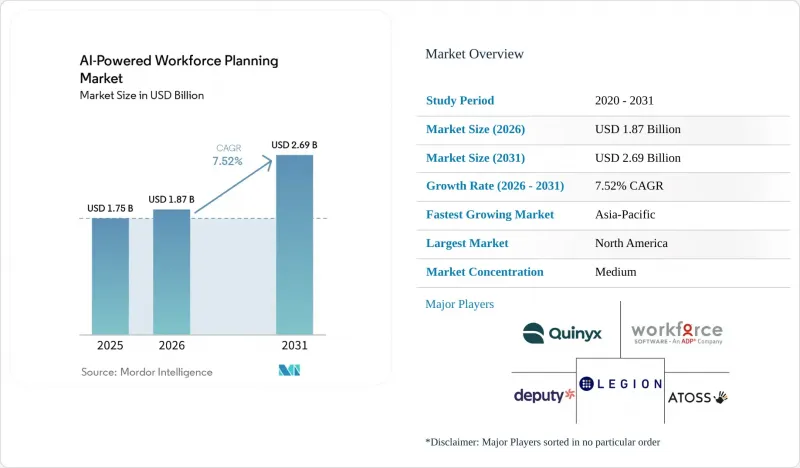

JHS 26.06.23According to Mordor Intelligence, the aI-powered workforce planning market size is expected to grow from USD 1.75 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.69 billion by 2031 at 7.52% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Software Type (Workforce Scheduling and Planning, Workforce Analytics, and More), Deployment Mode (Cloud, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Powered Workforce Planning Market Trends and Insights

Agentic AI Copilots Compress Enterprise Planning Cycles

The AI-powered workforce planning market is moving beyond assistive AI tools and toward agentic systems that can connect data, run scenarios, and recommend actions with less human intervention. Product launches in 2025 and 2026 show that autonomous planning workflows are moving into mainstream workforce software roadmaps rather than remaining in experimental pilots. Legion introduced more than 90 AI workforce innovations in January 2026, and Eightfold introduced TalentForge in May 2026 to enable enterprises to build custom HR applications on its talent intelligence layer. That shift reduces the distance between a planning question and an operating response, especially when labor forecasts, schedules, and skills data need to be updated together. It also puts pressure on vendors that still rely on slower, human-reviewed batch workflows, as buyers increasingly expect continuous planning rather than periodic reporting. Enterprises still need strong override rules and auditable workflows because faster automation only supports the AI-powered workforce planning market when governance is embedded into day-to-day planning processes.

Need for Data-Driven Talent Allocation in Hybrid and Distributed Workforces

Hybrid and distributed work models are making static workforce snapshots much less useful in the AI-powered workforce planning market. Buyers increasingly need live visibility into staffing levels, schedules, internal mobility, labor demand, and budget limits across locations, teams, and worker types. SD Worx reported that 48.2% of European organizations identified scheduling efficiency and adequate staffing as primary reasons for making workforce planning a 2026 priority. That pattern shows that many employers are buying these tools to protect day-to-day operating continuity and service levels, not simply to pursue digital experimentation. Oracle's prebuilt AI agents in Fusion Cloud HCM also demonstrate how vendors are integrating internal mobility, career development, succession planning, and payroll anomaly detection into a single, connected workflow. As hybrid work structures remain in place, platforms that connect talent availability with business demand are improving their position in the AI-powered workforce planning market.

Data Privacy, Explainability, and Bias Risks in HR AI Models

Compliance pressure remains a real brake on the AI-powered workforce planning market when AI models influence task allocation, performance review, workforce monitoring, or skill inference. The EU AI Act classifies several workplace AI uses as high-risk, requiring buyers to implement stronger documentation, oversight controls, and accountability before full deployment. In the United States, rules such as California's FEHA obligations and New York City's annual bias audit requirements are pushing enterprises to require bias testing, record retention, and auditable decision logs before approving purchases. These obligations raise implementation costs and often lengthen sales cycles, especially for smaller vendors without dedicated governance teams. They also affect product design, because explainability is becoming a core buying criterion rather than an optional compliance feature. The result is a slower rollout path in regulated settings, even as larger vendors use governance readiness to differentiate themselves inside the AI-powered workforce planning market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Skills-Based Workforce Planning and Internal Mobility

- Cloud HCM and ERP Integration Enable Continuous Workforce Forecasting

- Legacy Data Silos and Difficult Integration across HR, Finance, and Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 63.12% of the AI-powered workforce planning market share in 2025, indicating that scheduling, analytics, and planning platforms remain the foundational technology layer for enterprise deployment. This weight reflects the product-led structure used by many vendors, where software subscriptions establish the account footprint before service work expands it across teams and geographies. Even so, services are forecast to grow at a 10.41% CAGR through 2031, the fastest pace among component segments, indicating where implementation complexity is rising. The gap between software scale and services growth suggests that buyers are no longer purchasing only a tool; they are also purchasing configuration, governance support, and operating assistance. That pattern is becoming more visible as the AI-powered workforce planning market moves from rule-based automation toward model-driven planning and continuous workforce intelligence.

Service demand rises further when vendors expand into verticals and countries where labor rules, union terms, and sector taxonomies need local configuration before the platform can be used effectively. ATOSS reported consulting revenue of EUR 35.9 million (USD 38.8 million) in FY2024, up 8% year over year, and linked part of that increase to more complex deployments in healthcare and logistics. For the AI-powered workforce planning industry, the result shows that product-led onboarding is still insufficient for many advanced planning and scheduling use cases. It also means the services layer can remain a meaningful revenue stream rather than a short implementation bridge that fades after go-live. Vendors that can combine scalable software with strong configuration, integration, and change support are likely to capture more durable revenue within the AI-powered workforce planning market.

Time and attendance management accounted for 37.14% of the software type segment in 2025, while workforce analytics will grow at a 9.33% CAGR through 2031, reflecting a shift from control functions toward decision support. Time and attendance remained central because compliance, labor rules, payroll linkage, and schedule execution still anchor platform selection in many enterprise accounts. Workforce analytics is expanding faster because buyers increasingly want systems that connect workforce data to cost, risk, skill availability, and capacity decisions. This changes the way software budgets are framed, since planning tools are being evaluated not only as HR applications but also as operating intelligence layers. In the AI-powered workforce planning market, that upgrade cycle is moving more value toward predictive and prescriptive capabilities than toward basic record-keeping functions.

Transactional modules such as scheduling, leave and absence management, and performance management remain sticky because they sit close to daily operations and are difficult to replace quickly. The next layer of spending is moving into analytics tools that sit above those modules and interpret attendance, performance, and staffing signals in a combined planning view. Orgvue introduced the Henshaw AI suite in December 2025, including automated role grouping and a natural language assistant for organizational data, which reduced manual work from months to minutes. That type of functionality supports faster role clustering, better skill mapping, and earlier detection of capacity gaps before those gaps affect business continuity. As a result, the AI-powered workforce planning market is rewarding vendors that can turn operational data into forward-looking planning actions rather than static reports.

Geography Analysis

North America held 38.56% of the AI-powered workforce planning market share in 2025, which made it the largest regional contributor and reflected earlier enterprise AI spending, mature cloud HCM adoption, and stronger software procurement cycles. The United States remains the core of that position because large health systems, technology firms, and retailers have sizable planning needs across distributed workforces and complex labor models. Health system labor pressure remains especially important, since hospitals are still absorbing high turnover costs and need better staffing forecasts and scheduling control to contain labor leakage. California FEHA rules and New York City's annual bias audit requirements are also pushing buyers toward platforms with clearer controls, stronger auditability, and documented decision logic. Canada and Mexico add smaller but expanding demand as cross-border talent visibility and regional labor coordination become more relevant to enterprise workforce strategies.

Asia-Pacific is forecast to grow at 9.67% CAGR through 2031, which makes it the fastest-growing geography in the AI-powered workforce planning market size. Growth in the region is being shaped by China's enterprise AI programs, India's large technology services base, and Japan's need to manage labor scarcity more tightly across aging workforce structures. Demand also benefits from the need to coordinate permanent staff, contractors, and gig workers across large operating footprints, especially in technology and business services. Australia and New Zealand, Japan, South Korea, and the rest of Asia-Pacific broaden the regional base, while South Korea is showing early traction in electronics and semiconductor scheduling use cases.

Europe holds a material position in the AI-powered workforce planning market, but procurement there is shaped by stronger compliance demands and more careful governance review than in several other regions. Workday reported in March 2026 that 41% of German companies said more than 60% of their workforce used AI tools in 2025, which shows high workplace AI exposure across the DACH region. That same environment also requires employers to work through co-determination and monitoring concerns before deploying workforce AI at scale. South America remains earlier in adoption, with Brazil's financial services and technology sectors supporting incremental demand, while the Middle East is using AI workforce planning inside broader digital transformation agendas. Africa is still nascent, but financial services and telecommunications in markets such as South Africa and Nigeria are creating early openings for the AI-powered workforce planning market.

- ATOSS Software SE

- WorkForce Software, LLC

- Quinyx AB

- Legion Technologies, Inc.

- Deputechnologies Pty Ltd.

- Shiftboard, Inc.

- Sona Technologies Ltd.

- TeamOhana, Inc.

- Visier, Inc.

- Orgvue Limited

- Positive Circularity Inc. dba LIFELENZ

- Ando Technologies, Inc.

- Teambridge LLC

- Vemo, Inc.

- INOP B.V.

- JobRoute, Inc.

- Invero Holdings, LLC

- Gloat Ltd.

- Eightfold AI Inc.

- Career Engagement Group d/b/a Fuel50

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Need for Data-Driven Talent Allocation in Hybrid and Distributed Workforces

- 4.2.2 Rising Adoption of Skills-Based Workforce Planning and Internal Mobility

- 4.2.3 Cloud HCM and ERP Integration Enabling Continuous Workforce Forecasting

- 4.2.4 Labor Cost Pressure and Need for Productivity Optimization

- 4.2.5 Agentic AI Copilots Compressing Workforce Planning Cycle Times

- 4.2.6 AI-Led Workforce Redeployment for Enterprise Automation Programs

- 4.3 Market Restraints

- 4.3.1 Data Privacy, Explainability, and Bias Risks in HR AI Models

- 4.3.2 Legacy Data Silos and Difficult Integration Across HR, Finance, and Operations

- 4.3.3 Low Confidence in AI-Generated Skill Inference for Regulated and Unionized Roles

- 4.3.4 Diffuse Ownership Across HR, Finance, and Operations Slowing Enterprise Rollouts

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Software Type

- 5.2.1 Workforce Scheduling and Planning

- 5.2.2 Time and Attendance Management

- 5.2.3 Leave and Absence Management

- 5.2.4 Workforce Analytics

- 5.2.5 Employee Performance Management

- 5.2.6 Other Software Types

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-premises

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-user Industry

- 5.5.1 Banking, Financial Services, and Insurance

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 IT and Telecommunications

- 5.5.4 Manufacturing

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Australia and New Zealand

- 5.6.4.5 South Korea

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ATOSS Software SE

- 6.4.2 WorkForce Software, LLC

- 6.4.3 Quinyx AB

- 6.4.4 Legion Technologies, Inc.

- 6.4.5 Deputechnologies Pty Ltd.

- 6.4.6 Shiftboard, Inc.

- 6.4.7 Sona Technologies Ltd.

- 6.4.8 TeamOhana, Inc.

- 6.4.9 Visier, Inc.

- 6.4.10 Orgvue Limited

- 6.4.11 Positive Circularity Inc. dba LIFELENZ

- 6.4.12 Ando Technologies, Inc.

- 6.4.13 Teambridge LLC

- 6.4.14 Vemo, Inc.

- 6.4.15 INOP B.V.

- 6.4.16 JobRoute, Inc.

- 6.4.17 Invero Holdings, LLC

- 6.4.18 Gloat Ltd.

- 6.4.19 Eightfold AI Inc.

- 6.4.20 Career Engagement Group d/b/a Fuel50

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment