|

시장보고서

상품코드

2064447

미국의 헬스케어 IT : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Healthcare IT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

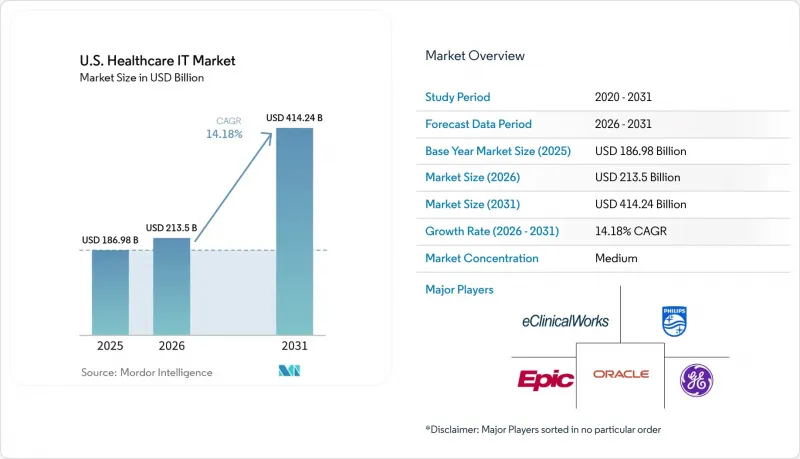

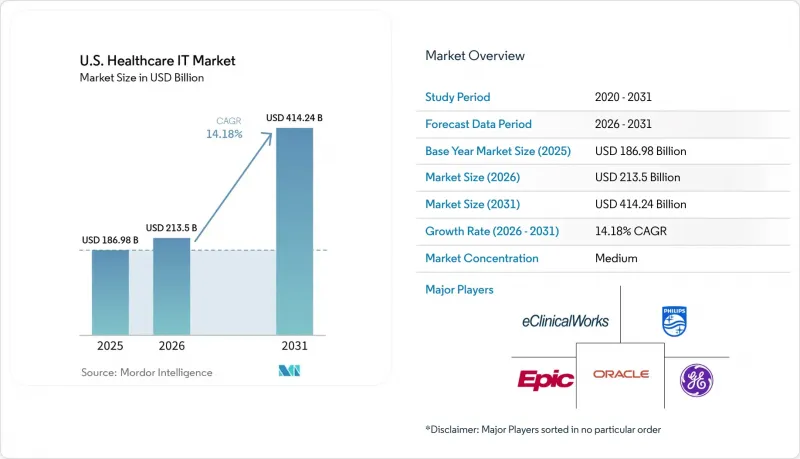

Mordor Intelligence에 의하면, 미국의 헬스케어 IT 시장 규모는 2025년 1,869억 8,000만 달러로 평가되었습니다. 2026년에는 2,135억 달러로 확대되어 2031년까지 4,142억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 14.18%를 나타낼 전망입니다.

본 보고서는 솔루션 유형(프로바이더용 솔루션, 페이어용 솔루션, IT 아웃소싱), 구성 요소(소프트웨어, 하드웨어, 서비스), 도입 모델(On-Premise, 웹 기반, 클라우드/SaaS, 하이브리드), 최종 사용자(의료 제공업체, 보험사, 생명과학 등), 용도(임상 워크플로우, 관리 업무 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 헬스케어 IT 시장 동향 및 인사이트

AI를 활용한 임상 및 관리 업무의 워크플로우 자동화

미국의 헬스케어 IT 시장에서 의료 시스템은 임상 및 관리 시스템의 측정 가능한 워크플로우 개선을 실현하기 위해 앰비언트 AI 스크라이빙 및 에이전트형 오케스트레이션과 같은 AI 기반 솔루션을 우선적으로 도입하고 있습니다. Oracle 헬스는 2026년 3월에 ‘Clinical AI Agent’를 도입하여, 의사의 업무 시간을 대폭 단축하고 문서 작성 부담을 줄였다고 보고했습니다. 이러한 기능들이 기업의 EHR(전자건강기록)에 통합됨에 따라, 독립형 도구는 가격 면에서 압박을 받는 반면, 확고한 플랫폼을 보유한 공급업체들은 자동화를 보다 광범위한 계약에 연계함으로써 우위를 점하고 있습니다. HHS의 HTI-5 규정안 등 규제 동향은 AI를 활용한 데이터 접근이 규정 준수 측면에서 갖는 가치를 더욱 강조하고 있습니다.

상호운용성 및 정보 차단 규제에 대한 대응 의무

미국의 헬스케어 IT 시장에서 상호운용성 규정 준수는 전략적 목표에서 운영상의 필수 요건으로 전환되고 있으며, 규정을 준수하지 않을 경우 금전적 벌금이나 인증 취소 등의 제재가 부과됩니다. HHS와 OIG는 정보 차단에 대한 제재 조치를 적극적으로 집행할 것이라고 발표했습니다. 한편, HTI-5안에서는 예외 규정이 강화되어, 보다 광범위한 데이터 교환을 위해 레거시 API의 업데이트가 의무화되었습니다. 이러한 시급성으로 인해 예측 기간 동안 TEFCA 연결, FHIR 업그레이드 및 상호 운용성 미들웨어에 대한 지속적인 지출이 촉진될 것입니다.

사이버 보안과 개인정보 보호에 미치는 부담

새로운 API, 클라우드 연결, AI 도구로 인해 조직이 관리해야 할 공격 표면이 확대되는 가운데, 사이버 보안 관련 과제가 계속해서 미국의 헬스케어 IT 시장을 위축시키고 있습니다. 2025년에는 의료 데이터 유출로 인한 평균 비용이 742만 달러에 달했으며, 이에 따른 재정적 영향이 부각되었습니다. 1억 9,270만 명에게 영향을 미친 Change Healthcare의 데이터 유출 사건과 같은 사이버 사고는 제3자에 의한 장애가 청구, 지급 및 의료 서비스 이용에 얼마나 큰 차질을 빚을 수 있는지를 보여주고 있습니다. 이러한 과제로 인해 의료 시스템은 감시, ID 관리, 사고 대응에 대한 지출을 우선시할 수밖에 없게 되어, 새로운 용도 도입이 지연되고 있습니다. 또한, AI 도입은 거버넌스의 복잡성을 가중시키고 있으며, 시장 확대에 더 큰 영향을 미치고 있습니다.

부문별 분석

2025년, 미국의 헬스케어 IT 시장에서 ‘의료 제공업체용 솔루션’은 48.12%를 차지했습니다. 이는 임상 정보 시스템, EHR 플랫폼, 수익 주기 관리 도구 및 환자용 용도에 대한 투자가 주도한 결과입니다. 핵심 임상 시스템은 기록, 지시, 처방, 업무 조정 측면에서 여전히 필수적이며, 해당 시스템의 업데이트는 AI 통합, 워크플로우 재설계, 클라우드 전환, 상호 운용성에 중점을 두고 있습니다.

의료보험사 대상 솔루션은 가장 빠르게 성장하고 있는 부문으로, 사전 승인, 케어 매니지먼트, 부정 분석, 지급 적정성 확보를 위한 도구의 성장에 힘입어 2031년까지의 예상 연평균 성장률(CAGR)은 15.20%에 달할 전망입니다. 연방 정부의 규정 준수 요건이 보험사의 투자를 촉진하고 있으며, 의료 서비스 제공업체의 업무 흐름과의 연동이 진행되고 있습니다.

2025년, 미국의 헬스케어 IT 시장에서 서비스는 71.7%의 점유율을 차지하며, 이는 아웃소싱, 매니지드 서비스, 컨설팅 및 수익 주기 업무에 대한 의존도를 반영했습니다. 대규모 의료 시스템은 인프라, 사이버 보안, 클라우드 전환 및 워크플로우 혁신을 관리하기 위해 서비스 집약형 모델을 선호하며, 운영 위험을 외부 파트너와 분담하고 있습니다.

2031년까지 연평균 성장률(CAGR) 15.99%를 나타낼 것으로 예측되는 ‘소프트웨어 및 플랫폼’ 분야는 AI 기반 전자건강기록(EHR), 클라우드 분석, 상호운용성 미들웨어에 의해 주도되고 있습니다. 구매자들은 문서 작성 자동화, 환자 접근성 향상, 업무 흐름 효율화를 도모하기 위해 소프트웨어에 대한 투자를 확대되고 있습니다. 소프트웨어의 급속한 성장에도 불구하고, 통합, 변경 관리, 교육 분야의 서비스는 여전히 필수적이며, 최대 수익원으로서의 역할을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the u.S. healthcare iT market size is expected to increase from USD 186.98 billion in 2025 to USD 213.5 billion in 2026 and reach USD 414.24 billion by 2031, growing at a CAGR of 14.18% over 2026-2031.

This report is Segmented by Solution Type (Provider Solutions, Payer Solutions, IT Outsourcing), Component (Software, Hardware, Services), Deployment Model (On-Premises, Web-Based, Cloud/SaaS, Hybrid), End User (Providers, Payers, Life Sciences, and More), Application (Clinical Workflow, Administrative, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

U.S. Healthcare IT Market Trends and Insights

AI-Enabled Clinical and Administrative Workflow Automation

In the United States Healthcare IT market, health systems are prioritizing AI-driven solutions like ambient AI scribing and agentic orchestration to achieve measurable workflow improvements in clinical and administrative systems. Oracle Health introduced its Clinical AI Agent in March 2026, reporting significant physician time savings and reduced documentation efforts. As these capabilities integrate into enterprise EHRs, standalone tools face pricing pressures, while vendors with established platforms gain an advantage by linking automation to broader contracts. Regulatory momentum, such as HHS's HTI-5 proposed rule, further emphasizes the compliance value of AI-enabled data access.

Interoperability and Information-Blocking Compliance Mandates

Interoperability compliance in the United States Healthcare IT market has transitioned from a strategic goal to an operational necessity, with financial and certification penalties for non-compliance. HHS and OIG announced active enforcement of information-blocking penalties, while the HTI-5 proposal tightened exceptions and required legacy API updates for broader data exchange. This urgency drives sustained spending on TEFCA connectivity, FHIR upgrades, and interoperability middleware throughout the forecast period.

Cybersecurity and Privacy Burden

Cybersecurity challenges continue to restrain the United States Healthcare IT market as new APIs, cloud connections, and AI tools expand the attack surface organizations must manage. The average cost of a healthcare data breach reached USD 7.42 million in 2025, highlighting the financial impact. Cyber incidents, such as the Change Healthcare breach affecting 192.7 million individuals, demonstrate how third-party disruptions can compromise claims, payments, and care access.These challenges force health systems to prioritize spending on monitoring, identity controls, and incident response, slowing the adoption of new applications. Additionally, AI adoption adds governance complexities, further impacting market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Value-Based Care and Population Health Analytics

- Electronic Prior Authorization and Payer API Buildout

- High Implementation Cost and Legacy Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Healthcare Provider Solutions accounted for 48.12% of the United States Healthcare IT market, driven by investments in clinical information systems, EHR platforms, revenue cycle tools, and patient-facing applications. Core clinical systems remain essential for documentation, orders, prescribing, and operational coordination, with updates focusing on AI integration, workflow redesign, cloud transitions, and interoperability.

Healthcare Payer Solutions is the fastest-growing segment, with a forecast CAGR of 15.20% through 2031, fueled by tools for prior authorization, care management, fraud analytics, and payment integrity. Federal compliance requirements are driving payer-side investments, aligning them with provider workflows.

In 2025, services dominated the United States Healthcare IT market with a 71.7% share, reflecting reliance on outsourcing, managed services, consulting, and revenue cycle operations. Large health systems prefer service-intensive models to manage infrastructure, cybersecurity, cloud migrations, and workflow transformations, ensuring operational risk is shared with external partners.

Software and Platforms, growing at a CAGR of 15.99% through 2031, are driven by AI-enabled EHRs, cloud analytics, and interoperability middleware. Buyers are increasing software investments to automate documentation, enhance patient access, and streamline workflows. Despite rapid software growth, services remain critical for integration, change management, and training, maintaining their role as the largest revenue contributor.

List of Companies Covered in this Report:

- Altera Digital Health

- Athenahealth

- eClinicalWorks LLC

- Epic Systems

- GE Healthcare

- Greenway Health

- Innovaccer

- Inovalon Holding Inc.

- InterSystems Corp.

- Koninklijke Philips

- Medical Information Technology, Inc.,

- Netsmart Technologies

- NextGen Healthcare

- Optum

- Oracle

- R1 RCM

- Surescripts LLC

- TruBridge Inc.

- Veradigm Inc.

- Waystar Holding Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Enabled Clinical and Administrative Workflow Automation

- 4.2.2 Interoperability and Information-Blocking Compliance Mandates

- 4.2.3 Shift to Value-Based Care and Population Health Analytics

- 4.2.4 Continued Digitization of Provider Workflows and Patient Access

- 4.2.5 Electronic Prior Authorization and Payer API Buildout

- 4.2.6 Data-Liquidity Buildout Across Post-Acute and Behavioral Settings

- 4.3 Market Restraints

- 4.3.1 Cybersecurity And Privacy Burden

- 4.3.2 High Implementation Cost and Legacy Integration Complexity

- 4.3.3 AI Governance and Workflow-Level Liability Concerns

- 4.3.4 Sensitive-Data Consent Complexity in Specialty Care Exchange

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Solution & Service Type

- 5.1.1 Healthcare Provider Solutions

- 5.1.1.1 Clinical Information Systems

- 5.1.1.1.1 EHR / EMR Systems

- 5.1.1.1.2 Computerized Provider Order Entry Systems

- 5.1.1.1.3 Clinical Decision Support Systems

- 5.1.1.1.4 e-Prescribing Systems

- 5.1.1.1.5 Medication Administration / Pharmacy Information Systems

- 5.1.1.1.6 Laboratory Information Systems

- 5.1.1.1.7 Radiology Information Systems / PACS / VNA

- 5.1.1.1.8 Cardiology Information Systems

- 5.1.1.1.9 Other Specialty Departmental Systems

- 5.1.1.2 Non-clinical Provider Solutions

- 5.1.1.2.1 Revenue Cycle Management

- 5.1.1.2.2 Practice Management

- 5.1.1.2.3 Scheduling and Patient Flow Management

- 5.1.1.2.4 Workforce Management

- 5.1.1.2.5 Claims, Billing and Payment Collection

- 5.1.1.3 Patient-Facing and Virtual Care Solutions

- 5.1.1.3.1 Patient Portals

- 5.1.1.3.2 Telehealth / Virtual Care Platforms

- 5.1.1.3.3 Remote Patient Monitoring Platforms

- 5.1.1.3.4 Digital Front Door / Self-scheduling / Contact Center Tools

- 5.1.1.4 Data, Analytics and Interoperability Solutions

- 5.1.1.4.1 Health Information Exchange

- 5.1.1.4.2 Population Health Management

- 5.1.1.4.3 Care Management Platforms

- 5.1.1.4.4 Clinical Data Repositories / Data Platforms

- 5.1.1.4.5 Interoperability / FHIR / API Management

- 5.1.1.4.6 AI-enabled Documentation, Coding and Workflow Automation

- 5.1.1.1 Clinical Information Systems

- 5.1.2 Healthcare Payer Solutions

- 5.1.2.1 Claims Management

- 5.1.2.2 Care Management

- 5.1.2.3 Fraud, Waste and Abuse Analytics

- 5.1.2.4 Utilization Management / Prior Authorization

- 5.1.2.5 Member Engagement / CRM

- 5.1.2.6 Payment Integrity, Risk Adjustment and Quality Analytics

- 5.1.3 Healthcare IT Outsourcing and Managed Services

- 5.1.3.1 Revenue Cycle Outsourcing

- 5.1.3.2 IT Consulting and Implementation

- 5.1.3.3 Managed Infrastructure, Cloud and Security Services

- 5.1.3.4 Application Management and Support

- 5.1.3.5 Clinical Documentation and Coding Outsourcing

- 5.1.1 Healthcare Provider Solutions

- 5.2 By Component

- 5.2.1 Software and Platforms

- 5.2.2 Hardware, Devices and Infrastructure

- 5.2.3 Services

- 5.3 By Deployment Model

- 5.3.1 On-premises

- 5.3.2 Web-based / Hosted

- 5.3.3 Cloud-based / SaaS

- 5.3.4 Hybrid

- 5.4 By End User

- 5.4.1 Healthcare Providers

- 5.4.2 Healthcare Payers

- 5.4.3 Life Sciences and Research Organizations

- 5.4.4 Government and Public Health Agencies

- 5.4.5 Employers, Purchasers and TPAs

- 5.5 By Application / Workflow

- 5.5.1 Clinical Workflow Management

- 5.5.2 Financial and Administrative Workflow

- 5.5.3 Patient Engagement and Access

- 5.5.4 Data Exchange, Analytics and Intelligence

- 5.5.5 Imaging, Diagnostics and Departmental Informatics

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Altera Digital Health Inc.

- 6.3.2 athenahealth Inc.

- 6.3.3 eClinicalWorks LLC

- 6.3.4 Epic Systems Corporation

- 6.3.5 GE HealthCare

- 6.3.6 Greenway Health LLC

- 6.3.7 Innovaccer

- 6.3.8 Inovalon Holding Inc.

- 6.3.9 InterSystems Corp.

- 6.3.10 Koninklijke Philips N.V.

- 6.3.11 Medical Information Technology, Inc.,

- 6.3.12 Netsmart Technologies Inc.

- 6.3.13 NextGen Healthcare Inc.

- 6.3.14 Optum Inc.

- 6.3.15 Oracle Corporation

- 6.3.16 R1 RCM Inc.

- 6.3.17 Surescripts LLC

- 6.3.18 TruBridge Inc.

- 6.3.19 Veradigm Inc.

- 6.3.20 Waystar Holding Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment