|

시장보고서

상품코드

2064469

미국의 멸균 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Sterilization Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

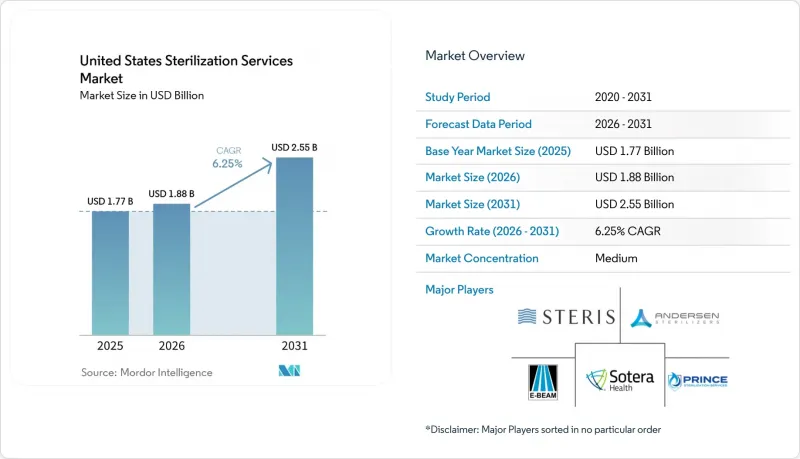

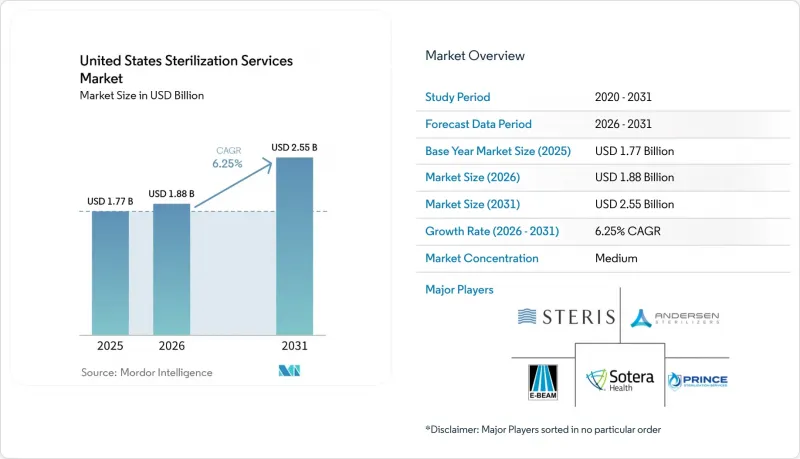

Mordor Intelligence에 의하면, 미국의 멸균 서비스 시장 규모는 2025년 17억 7,000만 달러로 평가되었습니다. 2026년 18억 8,000만 달러에서 2031년까지 25억 5,000만 달러로 확대되어 2026-2031년 CAGR은 6.25%를 나타낼 것으로 예측됩니다.

본 보고서는 방법(에톡실렌 멸균, 감마선 조사, 전자선 조사 등), 제공 형태(오프사이트, 온사이트/인하우스 애즈 어 서비스), 서비스 유형(위탁 멸균, 검증·시험 등), 최종 사용자(의료기기 제조업체, 제약 및 바이오의약품 기업, 병원·일일 수술센터 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 멸균 서비스 시장 동향 및 인사이트

증가하는 병원 내 감염으로 인한 부담과 시술 건수

의료 관련 감염(HAI)으로 인해 멸균 성능은 임상 현장에서 계속해서 엄격하게 모니터링되고 있으며, CDC의 2023년 전국 및 주별 보고서에 따르면, 의료기기 및 시술 관련 감염 관리는 급성기 의료 현장에서 여전히 중요한 과제로 남아 있습니다. 미국의 멸균 서비스 시장에서 이러한 압박은 중요한 의미를 지닙니다. 왜냐하면, 고도의 사내 인프라를 전면적으로 도입하지 않으면서도 병원 수준의 멸균 보증을 요구하는 외래 진료 시설에서의 시술이 증가하고 있기 때문입니다. 외래수술센터(ASC)로 중증도가 높은 사례가 이관됨에 따라, 검증된 처리 절차, 포장의 무결성, 그리고 문서화된 출하 관리의 필요성이 높아지고 있습니다. 많은 센터에서는 다기능 장비를 설치할 공간이 제한적이고, 공정 장애에 대한 허용 범위도 좁기 때문에 이러한 변화는 외부 위탁 수요 증가를 부추기고 있습니다. 따라서 미국의 멸균 서비스 시장은 시술 건수 증가와 감염 예방 기준의 향상이 동시에 진행됨에 따라 혜택을 볼 것입니다. 왜냐하면, 이 두 가지 모두 고객을 보다 공식적인 멸균 파트너십으로 이끌기 때문입니다.

의료기기 및 제약업체의 아웃소싱

QMSR로 인해 규정 준수에 부합하는 사내 멸균 업무의 운영 비용이 증가하고, 검사 시 공급업체에 대한 감독이 더욱 투명해짐에 따라 시장에서는 아웃소싱 추세가 강해지고 있습니다. RAPS의 보고서에 따르면, 2026년 5월 기준으로 완료된 100건 이상의 검사에서 아웃소싱 및 구매 관리가 QMSR 지적 사항 중 두 번째로 많이 언급되었으며, 이는 FDA가 공급업체 관리를 얼마나 엄격하게 심사하고 있는지를 보여줍니다. ISO 13485 : 2016의 4.1.5항은 현재 실무에서 더욱 중요한 위치를 차지하고 있습니다. 이는 아웃소싱된 프로세스에는 위험에 상응하는 관리가 필요하며, 멸균이 그 규칙의 가장 명확한 예 중 하나이기 때문입니다. 대규모 수탁 제공업체들은 이 체계 하에서 우위를 점하고 있습니다. 이는 서비스의 일환으로 문서화된 품질 시스템, 검증 기록 및 감사에 대응할 수 있는 추적성을 제공할 수 있기 때문입니다. 따라서 미국의 멸균 서비스 시장은 장기적인 아웃소싱 계약을 위한, 보다 대규모의 다중 모드 플랫폼으로 전환되고 있습니다.

에틸렌옥사이드(EtO) 배출 및 규정 준수 현황의 변동성

EtO는 여전히 많은 열에 민감한 제품에 있어 필수 불가결하지만, 배출에 관한 규제 체계가 급속히 변화하고 있으며 여전히 논란의 대상이 되고 있어, 미국의 멸균 서비스 시장은 불확실성에 직면해 있습니다. EPA의 2024년 최종 규정에서는 89개 상업용 EtO 시설 전체에 걸쳐 3억 1,300만 달러의 설비 투자와 7,400만 달러의 연간 규정 준수 비용이 예상되며, 이로 인해 개별 가스 사업의 경제성이 크게 변화했습니다. 그 후, 2026년 3월의 재검토안을 통해 위험 기반 기준, 밀폐 요건, 지속적인 모니터링과 같은 핵심적인 과제가 다시 대두되면서, 사업자와 고객 양측의 계획 기간이 단축되게 되었습니다. STERIS사는 2025년 1월, 일리노이주에서 진행되던 EtO 소송이 종결되었다고 발표했으며, 이는 주요 사업자들에게도 법적 리스크가 사업 환경의 일부가 되고 있음을 여실히 보여주고 있습니다. 미국의 멸균 서비스 시장에서 이러한 변동성으로 인해, 고객들은 필요한 곳에만 에톡실렌(EtO)을 제공하고, 나머지 처리는 방사선이나 기타 저온 처리 방식으로 전환할 수 있는 공급업체를 선호하고 있습니다.

부문별 분석

2025년 기준, 미국의 멸균 서비스 시장에서 에틸렌옥사이드(EtO) 멸균이 멸균 방법별 점유율의 45.31%를 차지했으며, 이러한 위상은 여전히 열에 민감한 의료기기 및 복잡한 조립품에 대한 적합성을 반영하고 있습니다. 미국 환경보호청(EPA)에 따르면, EtO는 국내에서 사용되는 전체 의료기기의 50%, 즉 매년 200억 대 이상을 멸균하고 있으며, 이는 규제가 강화되더라도 이 방법을 쉽게 대체하기 어려운 이유를 설명해 줍니다. 감마선 조사 기술은 확립된 고객 검증 프로세스와 코발트-60 관련 공급 역량을 바탕으로 시장 점유율 2위를 차지했습니다. 소테라 헬스(Sotera Health)는 2026년 1분기 노르디온(Nordion)의 코발트-60 매출이 환율 변동의 영향을 제외하면 25.8% 증가했다고 보고했으며, 이는 광범위한 멸균 생태계와 관련된 방사선 조사용 자재에 대한 수요가 지속되고 있음을 보여줍니다.

X선 조사법은 미국의 멸균 서비스 시장에서 가장 빠르게 성장하고 있는 기술로, 2031년까지의 예상 성장률은 9.38%입니다. Sterigenics와 STERIS 양사는 상업용 X선 설비의 용량을 확대하고 있으며, 이는 가속기 기반 방사선 기술이 수탁 서비스 분야에서 더욱 주류적인 역할을 맡기 시작하고 있음을 시사합니다. 또한, BGS 미국은 2025년에 펜실베이니아주에서 전자빔(E-Beam) 처리 능력을 확충함으로써, 북동부 및 중부 대서양 연안 지역의 제조업체들이 이용할 수 있는 방사선 처리 방법의 선택지가 확대되었습니다. VHP, NO₂, 전자빔 및 건열은 여전히 틈새 분야이지만, 고객이 저온 처리, 짧은 납기 또는 감광성 재료와의 높은 호환성을 필요로 하는 경우, 그 중요성이 커지고 있습니다.

2025년 기준으로, 배송 형태별로 살펴보면, 오프사이트 서비스 센터를 통한 멸균이 미국의 멸균 서비스 시장 점유율의 66.24%를 차지했습니다. 이는 각 생산 거점 내에 규정 준수를 충족하는 복합 운송 인프라를 유지하는 데 드는 비용이 높기 때문입니다. 이 모델은 고객이 시설을 완전히 소유하지 않더라도 검증된 공정, 훈련을 받은 운영자, 확립된 승인 문서를 활용할 수 있기 때문에 여전히 매력적입니다. 또한, 대규모 위탁 멸균 업체가 처리량을 안정적으로 유지할 수 있도록 하는 장기 서비스 계약에도 적합합니다. 실제로, 고객들이 더 높은 중복성과 생산 라인과의 근접성을 요구하게 되었음에도 불구하고, 이러한 요인들 덕분에 오프사이트 모델은 여전히 미국의 멸균 서비스 시장의 중심을 차지하고 있습니다.

온사이트 또는 ‘인하우스-어즈-어-서비스(In-house-as-a-service)’는 가장 빠르게 성장하고 있는 제공 모델이며, 이 부문의 미국의 멸균 서비스 시장 규모는 2031년까지 연평균 성장률(CAGR) 8.52%로 확대될 것으로 전망됩니다. 이 접근 방식에서는 서비스 제공업체가 고객의 현장에 설비를 설치·인증·운영하는 동시에, 외부 위탁 프로세스에 요구되는 품질의 추적성을 유지합니다. QMSR은 이러한 변화를 뒷받침하고 있습니다. 이는 QMSR이 외부 위탁 활동에 대한 문서화된 관리와 공급업체 관계 전반에 걸친 보다 명확한 책임 소재를 더욱 중시하기 때문입니다. 따라서 이 모델은 멸균 장치에 대한 규제상 책임을 전면적으로 부담하지 않으면서도, 공급망의 유연성이 더욱 필요한 대량 생산 의약품 프로그램이나 의료기기 라인에 특히 매력적인 선택지가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the united states sterilization services market size is projected to expand from USD 1.77 billion in 2025 and USD 1.88 billion in 2026 to USD 2.55 billion by 2031, registering a CAGR of 6.25% between 2026 to 2031.

This report is Segmented by Method (EtO Sterilization, Gamma Irradiation, E-Beam, and More), Mode of Delivery (Off-Site, On-site/In-house-as-a-Service), Service Type (Contract Sterilization, Validation & Testing, and More), and End User (Medical Device Manufacturers, Pharma & Biopharma, Hospitals & ASCs, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Sterilization Services Market Trends and Insights

Rising HAI Burden and Procedure Throughput

Healthcare-associated infections continue to keep sterilization performance under close clinical scrutiny, and the CDC's 2023 national and state report showed that device-related and procedure-related infection control remains a material issue for acute care settings. In the United States sterilization services market, that pressure matters because more procedures are moving through ambulatory settings that want hospital-grade sterility assurance without the full footprint of advanced in-house infrastructure. Higher-acuity case migration into ambulatory surgery centers increases the need for validated processing, packaging integrity, and documented release controls. That shift supports more off-site contract demand because many centers have limited space for multi-modal equipment and limited tolerance for process failure. The United States sterilization services market therefore benefits when procedure growth and infection prevention standards rise together, since both push customers toward more formal sterilization partnerships.

Outsourcing by Device and Pharma Manufacturers

The market is seeing stronger outsourcing momentum because QMSR raises the cost of running compliant internal sterilization operations and makes vendor oversight more visible during inspections. RAPS reported that outsourcing and purchasing controls ranked as the second-most-cited QMSR observation in more than 100 completed inspections as of May 2026, which shows how closely the FDA is reviewing supplier management. ISO 13485:2016 Clause 4.1.5 now carries more weight in practice because outsourced processes must be controlled in proportion to risk, and sterilization is one of the clearest examples of that rule. Large contract providers gain an advantage under this framework because they can offer documented quality systems, validation records, and audit-ready traceability as part of the service. That is why the United States sterilization services market is shifting toward bigger, multi-modal platforms for long-term outsourced agreements.

EtO Emissions and Compliance Volatility

EtO remains indispensable for many heat-sensitive products, but the United States sterilization services market faces uncertainty because the regulatory framework around emissions has changed quickly and remains contested. The EPA's 2024 final rule projected USD 313 million in capital investment and USD 74 million in annualized compliance costs across 89 commercial EtO facilities, which materially changed the economics of standalone gas operations. The March 2026 reconsideration proposal then reopened core issues including risk-based standards, enclosure requirements, and continuous monitoring, which shortened planning horizons for operators and customers alike. STERIS stated in January 2025 that an Illinois EtO trial had concluded, which highlights that legal exposure has become part of the operating environment for major participants as well. In the United States sterilization services market, this volatility pushes customers toward suppliers that can offer EtO only where needed and shift the rest of the load into radiation or other lower-temperature options.

Other drivers and restraints analyzed in the detailed report include:

- Single-Use and Minimally Invasive Device Expansion

- X-Ray Capacity Build-Outs Reducing EtO and Cobalt-60 Bottlenecks

- High Capex for Compliant Multi-Modal Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EtO sterilization accounted for 45.31% of the United States sterilization services market share by method in 2025, and that position still reflects its fit for heat-sensitive devices and complex assemblies. The EPA stated that EtO sterilizes 50% of all medical devices used in the country each year, or more than 20 billion units, which explains why the method remains hard to displace even under tighter regulation. Gamma irradiation held the second-largest position, supported by established customer validation pathways and cobalt-60-linked supply capacity. Sotera Health reported 25.8% constant-currency growth in Nordion cobalt-60 revenue in Q1 2026, which showed continued demand for radiation inputs tied to the broader sterilization ecosystem.

X-ray irradiation is the fastest-growing method in the United States sterilization services market, with forecast growth of 9.38% through 2031. Sterigenics and STERIS both expanded commercial X-ray capacity, which signals that accelerator-based radiation is moving into a more mainstream role for contract services. BGS US also added E-Beam capacity in Pennsylvania in 2025, which widened the radiation choice set for manufacturers in the Northeast and mid-Atlantic. VHP, NO2, E-Beam, and dry-heat remain smaller niches, but their role rises when customers need low-temperature processing, fast turnaround, or better compatibility with sensitive materials.

Off-site service-center sterilization held 66.24% of United States sterilization services market share by delivery mode in 2025, supported by the high cost of maintaining compliant multi-modal infrastructure inside each manufacturing site. The model remains attractive because it gives customers access to validated processes, trained operators, and established release documentation without full facility ownership. It also fits the long-duration service agreements that stabilize throughput for large contract sterilizers. In practice, this keeps the off-site model central to the United States sterilization services market even as customers ask for more redundancy and closer proximity to production lines.

On-site or in-house-as-a-service is the fastest-growing delivery model, with the United States sterilization services market size for this segment projected to grow at an 8.52% CAGR through 2031. Under this approach, the service provider installs, qualifies, and operates equipment at the customer site while maintaining the quality trail expected for outsourced processes. QMSR supports that shift because it places stronger emphasis on documented control over outsourced activities and clearer accountability across supplier relationships. That makes the model especially attractive for high-volume pharmaceutical programs and device lines that need more supply chain flexibility without taking on full regulatory responsibility for the sterilization unit.

List of Companies Covered in this Report:

- Advanced Sterilization Products (ASP)

- American Sterilizer Services

- BGS US LLC

- Cosmed Group

- Eagle Medical, Inc.

- E-BEAM Services, Inc.

- Infinity Laboratories / Eurofins Infinity Laboratory Group

- IsoTex, Inc.

- Life Science Outsourcing, Inc.

- Midwest Sterilization Corporation

- Noxilizer

- Prince Sterilization Services

- Quantum EBX

- Remington Medical

- SGS

- Sotera Health

- STERIS

- Steri-Tek

- VPT Rad, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising HAI Burden and Procedure Throughput

- 4.2.2 Outsourcing by Device and Pharma Manufacturers

- 4.2.3 FDA QMSR and ISO 13485 Alignment

- 4.2.4 Single-Use and Minimally Invasive Device Expansion

- 4.2.5 AI-Enabled Chain-of-Custody and Cycle-Tracking

- 4.2.6 X-Ray Capacity Build-Outs Reducing EtO and Cobalt-60 Bottlenecks

- 4.3 Market Restraints

- 4.3.1 EtO Emissions and Compliance Volatility

- 4.3.2 High Capex for Compliant Multi-Modal Capacity

- 4.3.3 Sterility-Assurance Talent Shortage

- 4.3.4 Material-Compatibility Failures When Shifting Modalities

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Method

- 5.1.1 Ethylene Oxide (EtO) Sterilization

- 5.1.2 Gamma Irradiation

- 5.1.3 Electron-Beam (E-beam) Irradiation

- 5.1.4 X-ray Irradiation

- 5.1.5 Steam (Moist-Heat) Sterilization

- 5.1.6 Dry-Heat Sterilization

- 5.1.7 Vaporized Hydrogen Peroxide / Gas Plasma Sterilization

- 5.1.8 Nitrogen Dioxide Sterilization

- 5.2 By Mode of Delivery

- 5.2.1 Off-site (Service-Center) Sterilization

- 5.2.2 On-site / In-house-as-a-Service Sterilization

- 5.3 By Service Type

- 5.3.1 Contract Sterilization Services

- 5.3.2 Sterilization Validation & Testing Services

- 5.3.3 Process Development, Advisory & Optimization Services

- 5.4 By End User

- 5.4.1 Medical Device Manufacturers

- 5.4.2 Pharmaceutical & Biopharmaceutical Manufacturers

- 5.4.3 Hospitals & Ambulatory Surgery Centers

- 5.4.4 Clinical Laboratories & Research Organizations

- 5.4.5 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Advanced Sterilization Products (ASP)

- 6.3.2 American Sterilizer Services

- 6.3.3 BGS US LLC

- 6.3.4 Cosmed Group

- 6.3.5 Eagle Medical, Inc.

- 6.3.6 E-BEAM Services, Inc.

- 6.3.7 Infinity Laboratories / Eurofins Infinity Laboratory Group

- 6.3.8 IsoTex, Inc.

- 6.3.9 Life Science Outsourcing, Inc.

- 6.3.10 Midwest Sterilization Corporation

- 6.3.11 Noxilizer, Inc.

- 6.3.12 Prince Sterilization Services, LLC

- 6.3.13 Quantum EBX

- 6.3.14 Remington Medical

- 6.3.15 SGS SA

- 6.3.16 Sotera Health

- 6.3.17 STERIS plc

- 6.3.18 Steri-Tek

- 6.3.19 VPT Rad, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment