|

시장보고서

상품코드

2064473

미국의 의료기기 제조업체 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Medical Device Manufacturers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

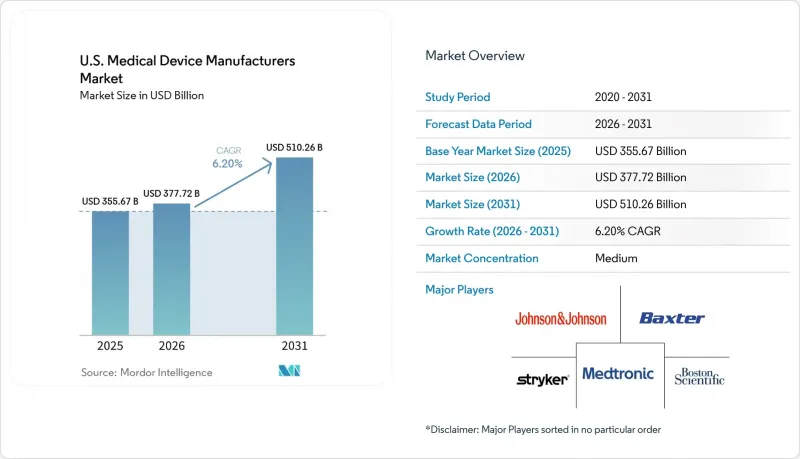

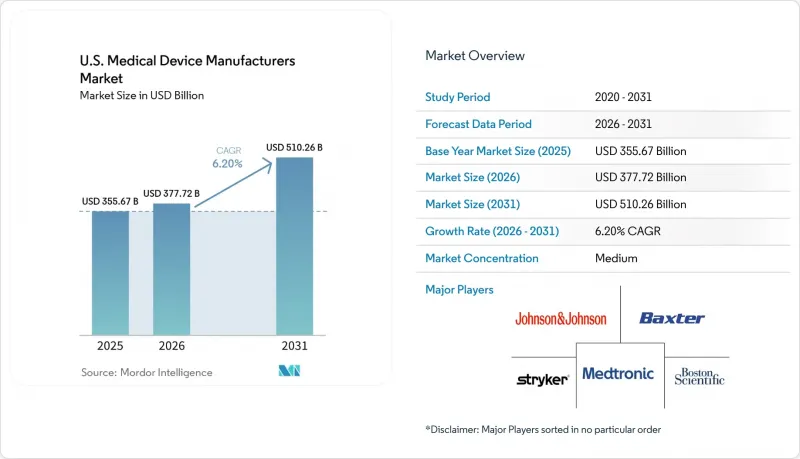

Mordor Intelligence에 의하면, 미국의 의료기기 제조업체 시장 규모는 2025년 3,556억 7,000만 달러로 평가되었습니다. 2026년에는 3,777억 2,000만 달러로 확대되어 2031년까지 5,102억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.20%를 나타낼 전망입니다.

본 보고서는 기기 유형(진단용, 치료용, 외과용, 모니터링용 기기), 기술 플랫폼(기존, 웨어러블, 원격의료, 로봇 수술, 3D 프린팅, AR/VR, 나노기술, 기타), 치료 용도(심장학, 정형외과, 신경학, 안과, 외과, 종양학), 그리고 최종 사용자(병원, 당일 수술센터, 진료소, 검사실, 재택 간호)에 따라 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

미국의 의료기기 제조업체 시장 동향 및 인사이트

고령화와 만성 질환 : 수요의 구조적 기반

미국의 의료기기 제조업체 시장은 지속적인 진단, 치료적 개입 및 모니터링이 필요한 만성 질환에 힘입어 견고한 수요 기반의 혜택을 누리고 있습니다. 이러한 수요는 여러 질환을 앓고 있는 고령층에서 특히 두드러지며, 영상 진단, 심장 보조 장치, 정형외과용 임플란트 및 모니터링 시스템의 이용을 증가시키고 있습니다. 여러 질환을 앓고 있는 환자의 경우, 자본 설비와 소모품 모두를 충당하기 위한 광범위한 조달이 필요하지만, 만성 질환 치료비는 선택적 지출에 비해 경제 변동의 영향을 덜 받는 경향이 있습니다.

저침습 및 영상 유도 수술로의 전환

로봇 지원 및 영상 유도 수술로의 전환은 모든 의료기기 부문에 걸쳐 수요를 변화시키고 있습니다. 로봇 시스템을 도입한 병원에서는 최소 침습 수술 시행률이 60.5%에서 65.8%로 상승하며, 수술 구성에서 차지하는 비중이 확대되고 있습니다. 이러한 추세는 에너지 기기, 시각화 도구, 내비게이션 시스템, 수술 중 영상 진단에 대한 수요를 견인하고 있으며, 한편 통합된 수술실 생태계는 수술 처리 능력과 회복 시간을 향상시키고 있습니다. 종합적인 제품 포트폴리오를 제공하는 기업은 단일 제품만을 취급하는 기업보다 유리한 입장에 있습니다.

FDA의 엄격한 증거, 품질 및 시판 후 규제로 인한 부담

의료기기 제조업체에 대한 규제 당국의 감시가 강화되고 있으며, 품질 시스템과 공급업체 관리에 대한 관심이 높아지고 있습니다. 2025년도에는 44건의 의료기기 경고서 중 38건에서 Part 820이 언급되었으며, 2026년 2월 발효일로부터 75일 이내에 100건 이상의 QMSR(품질관리시스템 심사)이 실시되었습니다. 이로 인해 중소 제조업체의 고정비가 증가하게 되며, 리스크 파일, CAPA(시정 조치) 시스템 및 지속적인 모니터링에 대한 투자가 필요하게 됩니다. 미국의 의료기기 제조업체 시장에서 대기업은 규정 준수를 경쟁 우위로 활용하기 쉬운 입장에 있는 반면, 중소 제조업체는 성장과 규제 대응 준비 사이의 균형을 맞추어야 하는 과제에 직면해 있습니다.

부문별 분석

2025년, 진단용 의료기기는 미국의 의료기기 제조업체 시장의 38.45%를 차지했습니다. 이는 병원 및 외래 진료 센터에서의 지속적인 영상 진단 수요, 체외 진단, 그리고 영상 유도 워크플로우에 힘입은 결과입니다. 이러한 시스템은 순환기, 종양학, 신경학 및 일상적인 모니터링 분야의 치료 경로에 필수적이며, 그 도입에는 처리 능력, 워크플로우 효율성 및 소프트웨어 통합이 영향을 미치고 있습니다.

모니터링 기기 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.23%를 기록하며 성장할 것으로 예상되며, 미국의 의료기기 시장에서 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 성장은 원격 환자 모니터링의 도입, 외래 진료 현장에서의 활용 확대, 그리고 Sibel Health사의 ‘ANNE Maternal’ 플랫폼과 같은 무선 소형 시스템으로의 전환에 힘입어 이루어지고 있습니다.

2025년 기준으로, 미국의 의료기기 시장의 기술 구성 중 55.9%를 기존의 전기기계식 및 일회용 플랫폼이 차지했으며, 이는 대량으로 소비되는 소모품과 표준 기기에 대한 의존도를 반영했습니다. 이 부문은 BD의 미국 내 제조 시설에 대한 투자와 네브래스카주 주사기 공장 확장 사례에서 볼 수 있듯이, 생산량, 신뢰성, 그리고 끊김 없는 공급에 의해 뒷받침되고 있습니다.

나노기술 및 스마트 소재 시장은 수동형 장치에서 정밀도를 높이고 조직에 가해지는 부담을 줄여주는 시스템으로의 전환에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.11%를 기록하며 성장할 것으로 예측됩니다. 반응형 시스템 및 소재를 통한 성능 향상 혁신은 상업적 선례에 힘입어 구상 단계를 넘어 발전하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the u.S. medical device manufacturers market size is expected to increase from USD 355.67 billion in 2025 to USD 377.72 billion in 2026 and reach USD 510.26 billion by 2031, growing at a CAGR of 6.20% over 2026-2031.

This report is Segmented by Device Type (Diagnostic, Therapeutic, Surgical, Monitoring Devices), Technology Platform (Conventional, Wearable, Telehealth, Robotic Surgery, 3-D Printing, AR/VR, Nanotechnology, Samd), Therapeutic Application (Cardiology, Orthopedics, Neurology, Ophthalmology, Surgery, Oncology), and End User (Hospitals, Ascs, Phys. Offices, Labs, Home Care). Forecasts in Value (USD).

U.S. Medical Device Manufacturers Market Trends and Insights

Aging Population and Chronic Disease: Structural Foundation for Demand

The United States medical device manufacturers market benefits from a strong demand base driven by chronic conditions requiring ongoing diagnostics, therapeutic interventions, and monitoring. This demand is particularly significant among older populations managing multiple conditions, increasing the use of imaging, cardiac support devices, orthopedic implants, and monitoring systems. Multimorbid patients necessitate broader procurement, supporting both capital equipment and consumables, while chronic disease care remains less impacted by economic fluctuations compared to elective spending.

Shift Toward Minimally Invasive and Image-Guided Procedures

The shift to robotic-assisted and image-guided procedures is transforming demand across device categories. Hospitals adopting robotic systems have increased minimally invasive surgery rates from 60.5% to 65.8%, expanding procedure mixes. This trend drives demand for energy devices, visualization tools, navigation systems, and intraoperative imaging, while integrated operating room ecosystems enhance throughput and recovery times. Companies offering comprehensive portfolios are better positioned than those with standalone products.

Stringent FDA Evidence, Quality, and Post-Market Burden

Regulatory scrutiny is tightening for medical device manufacturers, with deeper focus on quality systems and supplier controls. In FY2025, 38 out of 44 device warning letters cited Part 820, and over 100 QMSR inspections were conducted within 75 days of the February 2026 effective date. This increases fixed costs for smaller manufacturers, requiring investments in risk files, CAPA systems, and ongoing surveillance. Larger firms in the United States medical device manufacturers market are better positioned to use compliance as a competitive advantage, while smaller players face challenges balancing growth and regulatory readiness.

Other drivers and restraints analyzed in the detailed report include:

- Hospital Capital Refresh for Imaging, Monitoring, and Robotics

- Expansion of Outpatient and Home-Monitoring Pathways

- Recall, Cybersecurity, and Remediation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Diagnostic Devices accounted for 38.45% of the United States medical device manufacturers market, driven by consistent imaging demand, in-vitro diagnostics, and image-guided workflows in hospitals and outpatient centers. These systems are integral to care pathways in cardiology, oncology, neurology, and routine monitoring, with procurement influenced by throughput, workflow efficiency, and software integration.

Monitoring Devices are projected to grow at a 7.23% CAGR from 2026 to 2031, making them the fastest-growing segment in the United States medical device market. Growth is fueled by remote patient monitoring adoption, expanded use in ambulatory settings, and the shift toward wireless, compact systems like Sibel Health's ANNE Maternal platform.

In 2025, Conventional Electro-mechanical and Disposable platforms represented 55.9% of the technology mix in the United States medical device market, reflecting reliance on high-volume consumables and standard equipment. This segment thrives on volume, reliability, and uninterrupted supply, as seen in BD's investment in U.S. manufacturing and expansion of its Nebraska syringe plant.

Nanotechnology and Smart Materials are expected to grow at an 8.11% CAGR from 2026 to 2031, driven by a shift from passive devices to systems enhancing precision and reducing tissue burden. Innovations in responsive systems and material-enabled performance are advancing beyond concept stages, supported by commercial precedents.

List of Companies Covered in this Report:

- Abbott Laboratories

- Baxter

- Beckton Dickinson

- Boston Scientific

- Conmed

- Dexcom

- Edwards Lifesciences Inc.

- GE Healthcare

- Hologic

- ICU Medical

- Insulet

- Intuitive Surgical

- Johnson & Johnson

- Medtronic

- Penumbra

- Resmed

- Siemens Healthineers

- Stryker

- Teleflex

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Chronic Disease Burden

- 4.2.2 Shift Toward Minimally Invasive and Image-Guided Procedures

- 4.2.3 Hospital Capital Refresh for Imaging, Monitoring, and Robotics

- 4.2.4 Expansion of Outpatient and Home-Monitoring Pathways

- 4.2.5 CMS Pass-Through Pathway Lift for Breakthrough Devices

- 4.2.6 Stabilizing EtO Sterilization Capacity for Single-Use Devices

- 4.3 Market Restraints

- 4.3.1 Stringent FDA Evidence, Quality, and Post-Market Burden

- 4.3.2 Recall, Cybersecurity, and Remediation Costs

- 4.3.3 Medicare Coverage Lag After FDA Authorization

- 4.3.4 QMSR Transition Compliance Burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Industry rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Diagnostic Devices

- 5.1.1.1 Diagnostic Imaging Devices

- 5.1.1.1.1 MRI Systems

- 5.1.1.1.2 CT Scanners

- 5.1.1.1.3 Ultrasound

- 5.1.1.2 In-Vitro Diagnostics

- 5.1.1.1 Diagnostic Imaging Devices

- 5.1.2 Therapeutic Devices

- 5.1.2.1 Implants

- 5.1.2.2 Drug-Delivery Pumps

- 5.1.3 Surgical Devices

- 5.1.3.1 Robotics & Navigation

- 5.1.3.2 Energy-based Devices

- 5.1.4 Monitoring Devices

- 5.1.4.1 Multiparameter Monitors

- 5.1.4.2 Remote Patient Monitors

- 5.1.5 Others

- 5.1.1 Diagnostic Devices

- 5.2 By Technology Platform

- 5.2.1 Conventional Electro-mechanical & Disposable

- 5.2.2 Wearable & Remote Monitoring

- 5.2.3 Telehealth & mHealth

- 5.2.4 Robotic Surgery

- 5.2.5 3-D Printing

- 5.2.6 Augmented / Virtual Reality

- 5.2.7 Nanotechnology & Smart Materials

- 5.2.8 AI-as-a-Medical-Device (SaMD)

- 5.3 By Therapeutic Application

- 5.3.1 Cardiology

- 5.3.2 Orthopedics & Sports Medicine

- 5.3.3 Neurology

- 5.3.4 Ophthalmology

- 5.3.5 General & Laparoscopic Surgery

- 5.3.6 Oncology

- 5.3.7 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgery Centers

- 5.4.3 Physician Offices and Specialty Clinics

- 5.4.4 Diagnostic Laboratories and Imaging Centers

- 5.4.5 Home Care and Remote Monitoring Settings

- 5.4.6 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Baxter

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Boston Scientific Inc.

- 6.3.5 CONMED Corporation

- 6.3.6 Dexcom

- 6.3.7 Edwards Lifesciences Inc.

- 6.3.8 GE HealthCare

- 6.3.9 Hologic Inc.

- 6.3.10 ICU Medical

- 6.3.11 Insulet

- 6.3.12 Intuitive Surgical

- 6.3.13 Johnson & Johnson

- 6.3.14 Medtronic plc

- 6.3.15 Penumbra

- 6.3.16 ResMed Inc.

- 6.3.17 Siemens Healthineers AG

- 6.3.18 Stryker Corporation

- 6.3.19 Teleflex

- 6.3.20 Zimmer Biomet

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment