|

시장보고서

상품코드

2064500

미국의 전자건강기록(EHR) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Electronic Health Records - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

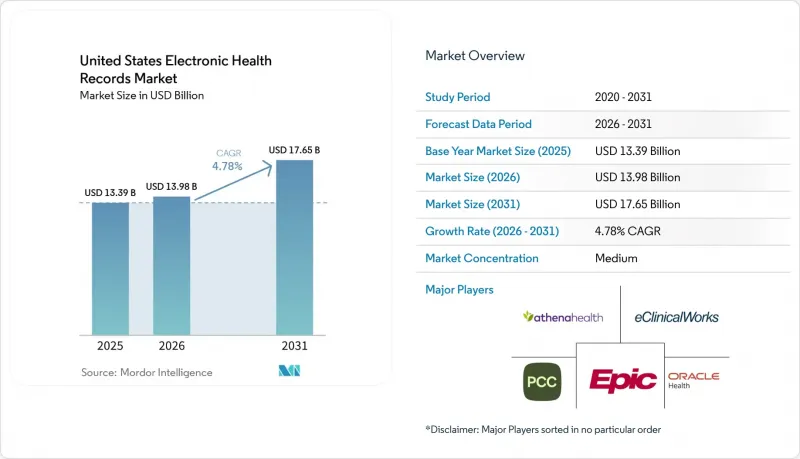

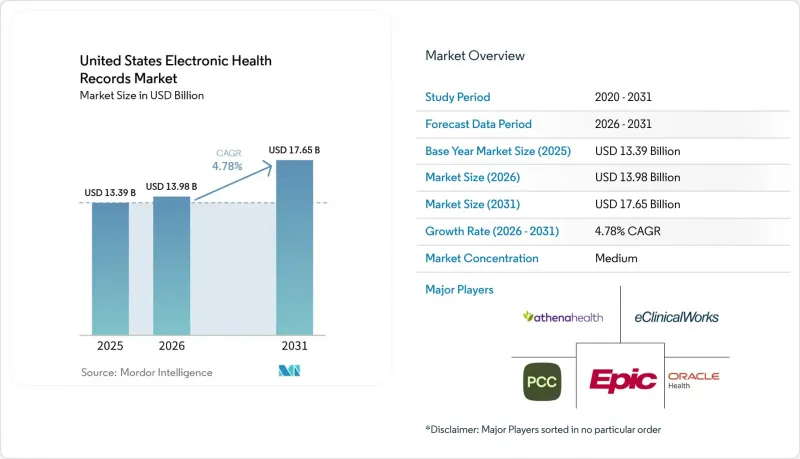

Mordor Intelligence에 의하면, 미국의 전자건강기록(EHR) 시장 규모는 2025년에 133억 9,000만 달러로 평가되었습니다. 2026년 139억 8,000만 달러에서 2031년까지 176억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 4.78%를 나타낼 전망입니다.

본 보고서는 제품별(웹/클라우드 기반 EHR, On-Premise형 EHR), 유형별(급성기 EHR, 외래 EHR, 급성기 후 EHR), 솔루션별(EHR 소프트웨어, 서비스) 및 최종 사용자별(병원, 진료소 및 전문 클리닉, 외래수술센터(ASC), 진단센터)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 전자건강기록(EHR) 시장 동향 및 인사이트

연방 정부에 의한 상호운용성 및 사전 승인 의무화

미국의 전자건강기록(EHR) 시장은 USCDI v1의 유효 기간이 2026년 1월 1일에 만료되고, ONC(국립의료정보기술조정국)의 요건에 따라 유효한 기준이 새로운 데이터 표준으로 전환됨에 따라 인증 재설정 시기를 맞이하고 있습니다. USCDI v3에서는 필요한 구조화 데이터 세트의 규모가 이전 버전보다 대폭 확대되고, 건강의 사회적 결정 요인 및 보험 데이터 등의 분야가 추가됨에 따라, 공급업체들은 데이터 아키텍처, 테스트 및 데이터 교환 워크플로우를 재검토해야 하는 상황에 놓여 있습니다. 그 후, ONC는 2025년 7월에 USCDI v6를 공개했으며, 2026년 1월 29일에는 USCDI v7 초안을 발표했습니다. 이로 인해 공급업체가 규정 준수를 일회성 작업으로 취급하는 것을 허용하지 않게 되며, 미국의 전자건강기록 시장은 연간 업그레이드 주기를 유지하게 될 것입니다. CMS는 ‘상호 운용성 및 사전 승인에 관한 최종 규정’을 통해 두 번째 기한을 추가했습니다. 이에 따라 사전 승인 API는 2027년 1월 1일까지 가동을 시작해야 하며, 이에 영향을 받는 워크플로우를 지원하는 모든 인증 공급업체의 개발 기간이 단축될 것입니다. 또한 HHS는 HTI-4 최종 규정에 따라 의료 제공업체가 인증 시스템 내에서 사전 승인을 보다 종합적으로 관리할 수 있게 됨에 따라, 향후 10년간 192억 달러의 관리 비용이 절감될 것으로 전망하고 있습니다. 이를 통해 컴플라이언스 대응 플랫폼의 운영 가치가 높아집니다. 그 결과, 미국의 전자건강기록 시장에서 플랫폼을 선정할 때는 안정적인 도입 실적뿐만 아니라, 공급업체가 적극적인 인증 로드맵을 제시할 수 있는지 여부와도 밀접한 관련이 있습니다.

클라우드 및 웹 기반 전환의 경제적 이점

클라우드 전환은 미국의 전자건강기록(EHR) 시장에서 실질적인 운영상의 결정 사항이 되고 있습니다. 이는 주요 EHR 워크로드를 On-Premise 인프라에서 마이그레이션한 후, 비용 절감, 성능 향상 및 보다 간소화된 업그레이드 경로가 실현되었습니다는 구체적인 사례가 의료 서비스 제공업체에게 제시되었기 때문입니다. 마이크로소프트는 2026년 3월, Azure를 통한 에픽(Epic) 도입이 전환 조직에 막대한 재무적 성과를 가져다주었다고 밝혔으며, 이는 클라우드에 대한 논의가 IT 현대화에서 이사회 차원의 자본 계획으로 전환되는 데 기여했습니다. 또한 마이크로소프트는 프란시스칸 헬스가 Azure로 전환한 후 5년 동안 4,500만 달러를 절감하고, 인프라 비용을 3분의 1로 줄였으며, 용도 응답 시간을 50% 개선했다고 밝혔습니다. 이는 의료 기관이 기존의 호스팅 모델에서 전환하는 데 도움이 되는 구체적인 사례가 됩니다. 이 점은 중요합니다. 이는 클라우드를 통한 서비스가 대규모 하드웨어 투자 주기를 보다 안정적인 운영 비용으로 전환하고, 공통 환경을 통해 분석, API 공개, 지속적인 규정 준수 업그레이드를 쉽게 지원할 수 있게 해주기 때문입니다. 또한, 이는 미국의 전자건강기록(EHR) 시장의 방향성과도 부합합니다. 해당 시장에서는 상호 운용성, 인증 갱신, AI 기능 도입 등 많은 On-Premise 환경이 대응할 수 있도록 설계된 범위를 넘어, 더욱 빈번한 제품 변경이 요구되고 있습니다. 따라서 상업적 논리가 정책적 논리를 뒷받침하고 있으며, 이것이 클라우드 서비스가 이 시장에서 규모 및 성장 양면에서 주도권을 쥐고 있는 이유입니다.

사이버 보안, 랜섬웨어 및 개인정보 침해

사이버 보안은 미국의 전자건강기록(EHR) 시장에서 여전히 가장 뚜렷한 하방 위험 요인으로 남아 있습니다. 왜냐하면, 사고로 인한 재무적 및 업무상의 영향은 IT 복구 단계에서 의료 서비스 제공 및 경영진의 감독 단계로 급속히 파급될 가능성이 있기 때문입니다. IBM의 보고서에 따르면, 2025년 의료 분야의 정보 유출 사고당 평균 복구 비용은 742만 달러로, 이로 인해 의료 분야는 중요 인프라 부문 중 가장 높은 비용 수준을 유지하고 있습니다. 미국병원협회(AHA)도 2025년 연례 종합 보고서에서 유출된 의료 기록의 90% 이상이 클리어링하우스, 수익 사이클 시스템, 제3자 커넥터 등 핵심 EHR 시스템 이외의 시스템에서 도난당한 것이라고 보고했습니다. 이는 위험이 더 이상 기록 자체에만 국한되지 않고, 보다 광범위한 용도 네트워크 전체로 확대되고 있음을 의미합니다. 이로 인해 공급업체 선정의 난이도가 높아지고 있습니다. 의료 시스템은 주요 EHR 용도뿐만 아니라 API 파트너 및 관련 워크플로 도구의 보안 태세도 평가해야 하기 때문입니다. 또한, HIPAA 준수 및 SOC 2 Type II 통제가 더 이상 제품의 차별화 요소가 아니라 계약상의 기본 요건이 된 이유도 바로 여기에 있습니다. 미국의 전자건강기록(EHR) 시장에서 이러한 보안상의 부담은 구매 결정 지연, 도입 심사 주기의 장기화, 그리고 더욱 긴밀하게 연계된 워크플로우로 플랫폼을 확장하는 데 드는 비용 증가를 초래할 가능성이 있습니다.

부문별 분석

웹/클라우드 기반 EHR은 2025년 미국의 전자건강기록 시장 규모의 81.79%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 6.30%로 가장 높은 성장률을 나타낼 것으로 전망됩니다. 이러한 조합은 미국의 전자건강기록 시장이 균등한 도입 모델로 나뉘어 있는 것이 아니라, 기본 운영 기반으로 클라우드로 더욱 확실하게 전환되고 있음을 보여줍니다. 이러한 전환 추세는 연방 정부의 상호 운용성 및 인증 요건에 힘입어 가속화되고 있습니다. 빈번한 표준 규격 업데이트와 API 요구 사항은 지속적인 릴리스를 전제로 구축된 환경에서 관리하기 쉽기 때문입니다. 또한, 클라우드 호스팅 방식의 기록은 로컬 인프라의 부담을 줄이고 대규모 임상 네트워크 전체의 성능 향상을 용이하게 할 수 있기 때문에 의료 제공업체의 경제적 요인에 의해서도 뒷받침되고 있습니다.

2025년 시점에서 On-Premise형 EHR은 나머지 18.21%를 차지했으며, 이는 미국의 전자건강기록 시장에서 규모는 작지만 여전히 견고한 도입 기반이 남아 있음을 보여줍니다. 이러한 기반은 보다 엄격한 관리 요건, 노후된 인프라, 또는 자본 계획 주기가 긴 조직에 집중되어 있으며, 일부 지방 정부 및 공공 부문 환경도 포함됩니다. 그렇긴 하지만, TEFCA 참여, API 공개, 임베디드 자동화 등의 요소가 분산된 사용자 전체에 걸쳐 보다 신속하게 업데이트할 수 있는 플랫폼에 유리하게 작용함에 따라, 제품 로드맵의 균형은 웹 및 클라우드 제공 쪽으로 이동하고 있습니다. 이로 인해 On-Premise 벤더들은 기존 계약 유지를 위해 분주한 반면, 클라우드 퍼스트를 추구하는 벤더들은 미국의 전자건강기록(EHR) 업계에서 업그레이드 및 교체 시장 점유율을 확대되고 있습니다.

2025년에는 급성기 EHR이 45.23%를 차지하며 유형별 구성에서 1위를 기록했으나, 2031년까지의 기간 동안에는 급성기 이후 EHR이 6.07%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측됩니다. 병원이 여전히 대규모 기업 계약, 주요 통합 예산, 그리고 가장 까다로운 상호운용성 요구 사항의 중심에 있기 때문에 급성기 의료는 여전히 미국의 전자건강기록 시장의 기반을 이루고 있습니다. 급성기 이후의 성장이 가속화되고 있는 것은 요양 시설이나 재택치료 현장에서 환자의 중증도가 높아지고 있는 데다, 병원에서 전원에 따른 임상적 복잡성이 증가함에 따라, 이러한 현장의 의료 제공업체들이 기록의 연속성을 더욱 강력히 요구하고 있기 때문입니다. 그 결과, 미국의 전자건강기록 시장에서는 입원 기간뿐만 아니라 치료의 전 과정을 지원해 줄 것을 요구하는 움직임이 확산되고 있습니다.

외래 EHR은 이 구조에서 여전히 큰 비중을 차지하고 있습니다. 이는 의료 서비스의 제공이 계속해서 입원 시설에서 의사의 진료소, 전문 클리닉 및 다중 거점 조직으로 이동하고 있기 때문입니다. eClinicalWorks가 2025년 3월에 PointClickCare 마켓플레이스와 통합한 것은 외래 진료 분야 벤더들이 의사의 업무 흐름과 장기 요양 또는 급성기 후 치료 환경 사이에 오랫동안 존재해 온 기록의 격차를 해소하려 하고 있음을 보여줍니다. 이러한 협력이 중요한 이유는 의료 기관 간 인계가 불충분할 경우 기록의 질, 후속 관리 계획 및 보험 급여의 지속성에 부정적인 영향을 미칠 수 있기 때문입니다. 따라서, 급성기 이후의 관리와 외래 진료를 연결하는 도구를 더욱 강력하게 갖춘 업체는 여전히 이러한 환경을 부차적인 시장으로 간주하는 업체보다 미국의 전자건강기록(EHR) 업계에서 유리한 입지를 차지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the united states electronic health records market size was valued at USD 13.39 billion in 2025 and is estimated to grow from USD 13.98 billion in 2026 to reach USD 17.65 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031).

This report is Segmented by Product (Web/Cloud-based EHR, On-Premise EHR), Type (Acute EHR, Ambulatory EHR, Post-Acute EHR), Solution (EHR Software, Services), and End Use (Hospitals, Physician Offices and Specialty Clinics, Ambulatory Surgical Centers, Diagnostic Centers). The Market Forecasts are Provided in Terms of Value (USD).

United States Electronic Health Records Market Trends and Insights

Federal Interoperability and Prior-Authorization Mandates

The United States electronic health records market is moving through a certification reset as USCDI v1 expired on January 1, 2026, and ONC requirements moved the active baseline to newer data standards. USCDI v3 expanded the required structured data set well beyond the earlier version, adding fields such as social determinants of health and insurance data that force vendors to rework data architecture, testing, and exchange workflows. ONC then published USCDI v6 in July 2025 and released draft USCDI v7 on January 29, 2026, which keeps the United States electronic health records market on an annual upgrade cycle instead of allowing vendors to treat compliance as a one-time exercise. CMS has added a second deadline through the Interoperability and Prior Authorization Final Rule, with Prior Authorization APIs required to go live on January 1, 2027, which shortens development windows for every certified vendor serving affected workflows. HHS also stated that the HTI-4 Final Rule is expected to generate USD 19.2 billion in administrative savings over 10 years by allowing providers to manage prior authorization more fully inside certified systems, which raises the operating value of compliance-ready platforms. As a result, platform selection in the United States electronic health records market is now closely tied to whether a vendor can show an active certification roadmap, not just a stable installed base.

Cloud And Web-Based Migration Economics

Cloud migration has become a practical operating decision in the United States electronic health records market because providers now have visible examples of cost savings, performance gains, and simpler upgrade paths after moving major EHR workloads off local infrastructure. Microsoft stated in March 2026 that Epic deployments on Azure delivered strong financial returns for migrating organizations, which helped shift cloud discussions from IT modernization into board-level capital planning. Microsoft also said Franciscan Health saved USD 45 million over 5 years after its Azure migration, while cutting infrastructure costs by one-third and improving application response time by 50%, which gives providers a concrete case for moving away from older hosting models. That matters because cloud delivery converts large hardware cycles into steadier operating expenses and makes it easier to support analytics, API exposure, and ongoing compliance upgrades from a common environment. It also supports the direction of the United States electronic health records market, where interoperability, certification updates, and AI features all require more frequent product changes than many on-premise footprints were designed to handle. The commercial logic is therefore reinforcing the policy logic, which is why cloud delivery leads on both scale and growth in this market.

Cybersecurity, Ransomware, and Privacy Exposure

Cybersecurity remains the clearest downside risk in the United States electronic health records market because the financial and operational impact of an incident can move quickly from IT recovery into care delivery and executive oversight. IBM reported average healthcare breach recovery costs of USD 7.42 million per incident in 2025, which kept healthcare at the highest cost level among critical infrastructure sectors. The American Hospital Association also reported in its 2025 year-in-review that more than 90% of breached health records were taken from systems outside the core EHR, including clearinghouses, revenue cycle systems, and third-party connectors, which means risk now sits across the broader application network rather than inside the record alone. That raises the difficulty of vendor selection because health systems must assess the security posture of API partners and adjacent workflow tools, not only the main EHR application. It also explains why HIPAA compliance and SOC 2 Type II controls are now basic contract expectations rather than points of product differentiation. For the United States electronic health records market, that security burden can slow purchase decisions, extend implementation review cycles, and raise the cost of platform expansion into more connected workflows.

Other drivers and restraints analyzed in the detailed report include:

- Outpatient Care Expansion and Multisite Coordination Needs

- AI-Enabled Documentation and Workflow Automation

- High Switching Costs and Implementation Disruption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Web/cloud-based EHR held 81.79% of the United States electronic health records market size in 2025 and is also forecast to post the fastest CAGR at 6.30% through 2031. That combination shows that the United States electronic health records market is not splitting between equal deployment models, but is moving more firmly toward cloud as the default operating base. The shift is reinforced by federal interoperability and certification demands, since frequent standards updates and API requirements are easier to manage in environments built for continuous releases. It is also reinforced by provider economics, because cloud-hosted records can reduce local infrastructure burden and simplify performance upgrades across large clinical networks.

On-premise EHR accounted for the remaining 18.21% in 2025, which shows that a smaller but durable installed base still remains in the United States electronic health records market. That base is concentrated in organizations with tighter control requirements, older infrastructure decisions, or slower capital planning cycles, including some rural and public-sector settings. Even so, the product roadmap balance has shifted toward web and cloud delivery because TEFCA participation, API exposure, and embedded automation all favor platforms that can be updated more quickly across distributed users. This leaves on-premise vendors under pressure to defend existing contracts while cloud-first vendors capture a larger share of upgrade and replacement activity in the United States electronic health records industry.

Acute EHR led the type mix with 45.23% in 2025, while post-acute EHR is expected to record the fastest CAGR at 6.07% through 2031. Acute care still anchors the United States electronic health records market because hospitals remain the center of large enterprise contracts, major integration budgets, and the strictest interoperability demands. Post-acute growth is rising because patient acuity in skilled nursing and home health settings is increasing, and providers in those settings need better continuity of records as transitions from hospital care become more clinically complex. The result is a broader push for the United States electronic health records market to support the full care path rather than only the hospital stay.

Ambulatory EHR remains a large middle layer in this structure because care volume continues to move out of inpatient settings and into physician offices, specialty clinics, and multisite organizations. eClinicalWorks' March 2025 integration with the PointClickCare marketplace showed how ambulatory vendors are trying to close the long-standing record gap between physician workflows and long-term or post-acute settings. That kind of connection matters because weak handoffs across care settings can hurt documentation quality, follow-up planning, and reimbursement continuity. Vendors with stronger post-acute and ambulatory bridge tools are therefore better positioned in the United States electronic health records industry than vendors that still treat those settings as side markets.

List of Companies Covered in this Report:

- AdvancedMD

- Altera Digital Health

- Amazing Charts

- athenahealth

- CareCloud

- Curemd Healthcare

- DrChrono

- Elation Health

- eClinicalWorks

- Epic Systems

- Greenway Health

- Medhost

- Meditech

- ModMed

- NextGen Healthcare

- Oracle Health

- PointClickCare

- Practice Fusion

- RXNT

- TruBridge

- Veradigm

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal Interoperability and Prior-Authorization Mandates

- 4.2.2 Cloud And Web-Based Migration Economics

- 4.2.3 Outpatient Care Expansion and Multisite Coordination Needs

- 4.2.4 AI-Enabled Documentation and Workflow Automation

- 4.2.5 TEFCA Network Effects Favor Exchange-Ready Platforms

- 4.2.6 USCDI And Certification Roadmap-Driven Upgrade Cycles

- 4.3 Market Restraints

- 4.3.1 Cybersecurity, Ransomware, and Privacy Exposure

- 4.3.2 High Switching Costs and Implementation Disruption

- 4.3.3 Uneven API And FHIR Readiness Across Smaller Providers

- 4.3.4 Vendor Lock-In from Concentrated Platform Ecosystems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Web / Cloud-based EHR

- 5.1.2 On-premise EHR

- 5.2 By Type

- 5.2.1 Acute EHR

- 5.2.2 Ambulatory EHR

- 5.2.3 Post-acute EHR

- 5.3 By Solution

- 5.3.1 EHR Software

- 5.3.1.1 Cloud-based

- 5.3.1.2 On-premise

- 5.3.2 Services

- 5.3.2.1 Consulting

- 5.3.2.2 Implementation & Integration

- 5.3.2.3 Support & Maintenance

- 5.3.1 EHR Software

- 5.4 By End Use

- 5.4.1 Hospitals

- 5.4.2 Physician Offices and Specialty Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Diagnostic Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AdvancedMD

- 6.3.2 Altera Digital Health

- 6.3.3 Amazing Charts

- 6.3.4 athenahealth

- 6.3.5 CareCloud

- 6.3.6 CureMD

- 6.3.7 DrChrono

- 6.3.8 Elation Health

- 6.3.9 eClinicalWorks

- 6.3.10 Epic Systems Corporation

- 6.3.11 Greenway Health

- 6.3.12 MEDHOST

- 6.3.13 MEDITECH

- 6.3.14 ModMed

- 6.3.15 NextGen Healthcare

- 6.3.16 Oracle Health

- 6.3.17 PointClickCare

- 6.3.18 Practice Fusion

- 6.3.19 RXNT

- 6.3.20 TruBridge

- 6.3.21 Veradigm

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment