|

시장보고서

상품코드

2064536

미국의 장기요양 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)United States Long Term Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

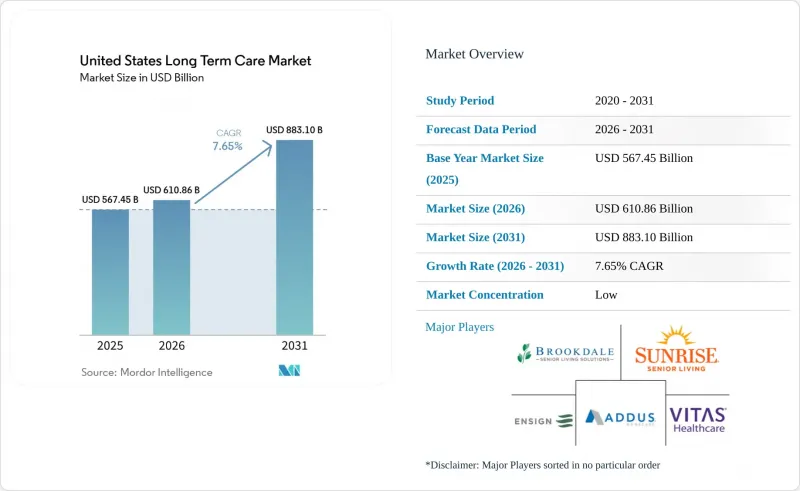

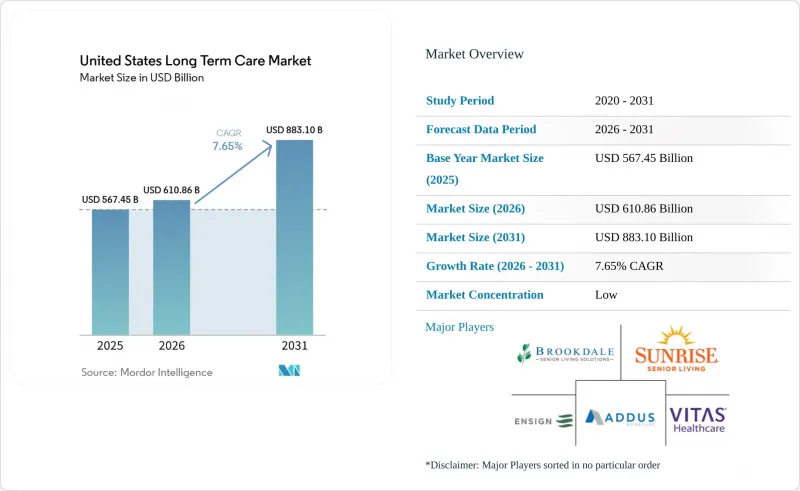

Mordor Intelligence에 의하면, 미국의 장기요양 시장 규모는 2025년 5,674억 5,000만 달러로 평가되었고, 2026년 6,108억 6,000만 달러로 추정되고, 2031년까지 8,831억 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 7.65%를 나타낼 전망입니다.

본 보고서는 서비스별(재택의료, 호스피스, 요양, 요양형 주거시설, 성인 주간보호센터), 보험자별(공적 보험, 민간 보험, 본인 부담 및 자비, 매니지드 케어 및 가치 기반 계약), 연령대별(0-29세, 30-64세, 65-74세, 75-84세, 85세 이상)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 장기 요양 시장 동향 및 인사이트

고령화와 장수화가 구조적인 수요 증가를 주도하고 있습니다.

미국의 장기 요양 시장을 지탱하는 인구 기반은 많은 서비스 제공업체의 계획 주기나 자본 예산이 감당할 수 있는 속도를 뛰어넘는 속도로 확대되고 있습니다. 2024년 기준 65세 이상 인구는 6,120만 명에 달했고, 미국 전체 인구의 18.0%를 차지했습니다. 2024년까지 11개 주와 미국 내 카운티의 약 45%에서 노인 인구가 아동 인구를 넘어섰습니다. 이는 이러한 연령 구성의 변화가 지역 요양 시장에 얼마나 빠르게 확산되고 있는지를 보여줍니다. 브루킹스 연구소의 보고서에 따르면, 65세 이상 성인의 5명 중 1명 가까이가 적어도 한 가지 일상생활 활동(ADL)을 스스로 수행할 수 없는 상태인 반면, 85세 이상 연령층에서는 그 비율이 5명 중 2명에 육박하고 있으며, 이것이 공식적인 장기 요양 서비스 이용을 직접적으로 유발하는 요인이 되고 있습니다. 이러한 고령화 추세가 선벨트 지역의 주와 지방 카운티에 동시에 확산되고 있기 때문에 미국의 장기 요양 시장에서는 기존 시설과 수요가 가장 빠르게 증가하고 있는 카운티 사이에 입지상의 불일치가 발생하고 있습니다. 개발, 라이선싱, 인재 확보 모두 진전이 더딘 만큼, 이 격차를 메우려면 수년이 걸릴 것입니다.

메디케이드 및 메디케어의 재택 및 지역 밀착형 서비스(HCBS) 재조정으로 서비스 체계를 재구축

시설 돌봄에서 재택 및 지역사회 밀착형 돌봄으로의 전환은 현재 미국 장기 요양 시장의 자금, 수용 능력 및 돌봄 조정 배분 방식에 반영되어 있습니다. 2023년에는 970만 명의 메디케이드 장기 요양 서비스(LTSS) 이용자 중 87%가 HCBS(재택·지역 밀착형 서비스)를 이용했으며, HCBS는 총 2,286억 달러에 달하는 LTSS 지출의 63.8%를 차지했습니다. 이는 서비스 제공이 이미 시설 중심 모델에서 얼마나 멀어졌는지를 보여주는 것입니다. 11개 주를 제외한 모든 주에서 적어도 일부 재택 간호 서비스 제공에 관리형 의료를 도입하고 있으며, 2025년에는 26개 주가 관리형 의료 체계 하에서 1915(c)조 면제 조치를 적용하고 있었습니다. 이는 2024년의 22개 주에서 증가한 수치로, MLTSS 도입이 여전히 진행 중임을 보여줍니다. 이러한 정책 방향은 재택 간호, 성인 주간 보호, 기타 지역 밀착형 서비스에 대한 수요를 촉진하는 동시에, 미국 장기 요양 시장의 사업자들이 기록 관리, 네트워크 참여 및 성과 관리에 어떻게 투자하는지에 대해서도 변화를 가져오고 있습니다. KFF의 예측에 따르면, 2025년 조정법에 따라 향후 10년 동안 연방 메디케이드 지출이 9,110억 달러 감소할 것으로 전망됩니다. 또한, HCBS 프로그램은 선택 사항이므로, 예산 압박이 심화될 경우 각 주에서는 가입 요건을 강화하거나 보상액을 인하하는 등의 조치를 취할 가능성이 있습니다. 또한, CMS는 2028년판 HCBS 품질 측정 기준을 확정했으며, 2026년 가을부터 보고가 의무화됩니다. 이로 인해 규정 준수 업무가 증가하게 되어, 기술 인프라가 제한적인 소규모 HCBS 제공 사업자에게는 더 큰 부담이 될 것입니다.

직접 돌봄 종사자의 부족이 공급 측의 수용 능력을 제약하고 있습니다.

노동 수요가 신규 노동력 공급을 앞지르는 속도로 증가하고 있기 때문에 인력 확보는 미국 장기 요양 시장에서 여전히 가장 뚜렷한 운영상의 제약 요인으로 남아 있습니다. PHI의 예측에 따르면, 2024-2034년 성장, 이직 및 노동력 이탈로 인해 발생하는 직무를 포함해 890만 건의 직접 돌봄 직무 채용 수요가 발생할 것으로 전망됩니다. 또한 PHI는 재택 돌봄 종사자가 2014년 140만 명에서 2024년에는 320만 명으로 증가한 후, 2034년까지 재택 돌봄 분야에서만 610만 건의 구인 수요가 발생할 것이라고 보고하고 있습니다. ANCOR는 2025년에 지역 밀착형 서비스 제공업체의 88%가 중등도 또는 심각한 인력 부족에 직면해 있으며, 62%는 인력 부족을 이유로 소개를 거절할 수밖에 없고, 52%는 상황이 개선되지 않을 경우 추가적인 프로그램 축소를 검토하고 있다고 보고했습니다. 또한 PHI의 보고서에 따르면, 2024년 재택 요양 종사자의 시간당 임금 중앙값은 16.77달러이며, 15%는 빈곤선 이하의 생활을 영위하고 있고, 40% 이상이 저소득 가구에 속해 있다고 합니다. 이는 문제가 임금에 그치지 않고, 업무의 질, 경력 이동성, 근로 시간, 복리후생에까지 미치고 있음을 보여줍니다.

부문별 분석

2025년 기준으로, 재택의료는 미국 장기요양 시장 점유율의 45.31%를 차지했으며, 이는 지역 밀착형 서비스 제공의 강점, 공공 HCBS(재택·지역사회 기반 서비스) 자금, 그리고 재택 간호를 선호하는 가족들의 의향을 반영한 결과입니다. 리치먼드 연방준비은행은 2026년 1월, CMS(미국 의료보험·의료서비스센터) 프로그램이 미국 재택의료 총지출의 50% 이상을 상환하고 있으며, 2023년에는 메디케이드가 재택의료 지출의 3분의 2에 가까운 비중을 차지했다고 보고했습니다. 이는 해당 부문이 공적 자금을 바탕으로 탄탄한 기반을 갖추고 있음을 뒷받침합니다. 요양 시설 및 요양 서비스가 제공되는 주택은 여전히 두 번째로 큰 서비스 그룹이지만, 미국의 장기 요양 시장 내에서는 다른 방향으로 움직이고 있습니다. 요양 시설은 점점 더 많은 가족들이 입소를 미루고 우선 재택 서비스를 이용하기를 선호함에 따라, 증상이 경미한 사례에서 점차 압박을 받고 있습니다. 한편, 간병 서비스가 제공되는 주택은 일상적인 돌봄은 필요하지만 본격적인 의료적 개입까지는 필요하지 않은 고령자들에게 인기를 얻고 있으며, 브룩데일 경영진은 2026년 평균 입주율이 90%를 나타낼 것으로 전망하고 있는데, 이는 해당 시설 수요가 꾸준히 회복되고 있음을 시사합니다.

성인 주간보호센터는 미국의 장기 요양 시장 규모에서 2026-2031년 연평균 성장률(CAGR) 9.38%로 성장할 것으로 전망됩니다. 이 성장세는 시장 전체의 성장률을 173베이시스포인트 상회하며, 재택 간호와 완전한 시설 입소 사이의 감독 하에 이루어지는 가교 역할로서 해당 부문의 기능을 반영하고 있습니다. CareScout의 보고서에 따르면, 2025년 성인 주간 보호 서비스의 전국 평균 1일 이용 요금은 95달러이며, 이는 저렴한 비용으로 집중적인 돌봄을 원하는 가족과 공공 프로그램에게 이 서비스가 제공하는 가치를 입증해 줍니다. 또한, 이 부문은 HCBS(가정 및 지역사회 기반 서비스) 면제 제도와 시설 입소를 방지하기 위한 각 주의 노력과도 밀접하게 부합하며, 미국 장기 요양 업계 전반에서 돌봄 서비스가 지속적으로 지역사회로 전환되는 가운데, 수요의 지속을 뒷받침하고 있습니다. 호스피스의 매출 점유율은 여전히 낮은 수준이지만, 85세 이상 인구가 증가하고 완화 치료에 대한 수용도가 높아짐에 따라 견실한 이익률 잠재력을 유지하고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the united states long term care market size is projected to expand from USD 567.45 billion in 2025 and USD 610.86 billion in 2026 to USD 883.10 billion by 2031, registering a CAGR of 7.65% between 2026 to 2031.

This report is Segmented by Service (Home Healthcare, Hospice, Nursing Care, Assisted Living Facilities, Adult Day-Care Centers), Payer (Public, Private Insurance, Out-of-Pocket/Self-Funded, Managed-Care & Value-Based Contracts), Age Group (0-29 Years, 30-64 Years, 65-74 Years, 75-84 Years, 85 Years & Above). The Market Forecasts are Provided in Terms of Value (USD).

United States Long Term Care Market Trends and Insights

Aging Population and Longevity Driving Structural Demand Expansion

The demographic base supporting the United States long term care market is expanding faster than most provider planning cycles and capital budgets can adjust. The population aged 65 and older reached 61.2 million in 2024, represented 18.0% of the U.S. population. By 2024, 11 states and nearly 45% of U.S. counties had more older adults than children, which shows how quickly this age shift has spread across local care markets. Brookings reported that nearly 1 in 5 adults aged 65 and older could not perform at least 1 activity of daily living, while the figure approached 2 in 5 among those aged 85 and older, which is a direct trigger for formal long term care use. As this aging pattern spreads across Sun Belt states and rural counties at the same time, the United States long term care market faces a location mismatch between existing facilities and the counties where demand is rising most quickly, and that gap will take years to close because development, licensing, and staffing all move slowly.

Medicaid and Medicare HCBS Rebalancing Reshaping Service Architecture

The shift from institutional care toward home and community-based care is now built into how the United States long term care market deploys funding, capacity, and care coordination. In 2023, 87% of 9.7 million Medicaid LTSS users received HCBS, and HCBS accounted for 63.8% of total LTSS spending of USD 228.6 billion, which confirms how far service delivery has already moved away from institutional models. All but 11 states used managed care for at least some home care delivery, and 26 states included 1915(c) waivers under managed care arrangements in 2025, up from 22 states in 2024, which shows that MLTSS adoption is still advancing. This policy direction is reinforcing demand for home care, adult day care, and other community-based formats while also changing how providers in the United States long term care market invest in documentation, network participation, and outcomes management. KFF projected that the 2025 reconciliation law will reduce federal Medicaid spending by USD 911 billion over 10 years, and because HCBS programs are optional, states may respond by tightening enrollment or lowering reimbursement if budget pressure deepens. CMS also finalized the 2028 HCBS Quality Measure Set with mandatory reporting beginning in fall 2026, which creates added compliance work that will weigh more heavily on smaller HCBS providers with limited technology infrastructure.

Direct-Care Workforce Shortages Constraining Supply-Side Capacity

Workforce availability remains the clearest operating restraint across the United States long term care market because labor demand is growing faster than new worker supply. PHI projected 8.9 million direct-care job vacancies between 2024 and 2034, including roles created by growth, turnover, and labor force exits. PHI also reported that home care alone will face 6.1 million job openings by 2034, after the home care workforce expanded from 1.4 million in 2014 to 3.2 million in 2024. ANCOR reported in 2025 that 88% of community-based providers were experiencing moderate or severe staffing shortages, 62% had turned away referrals because of inadequate staffing, and 52% were considering additional program cuts if conditions did not improve. PHI further reported that the median hourly wage for home care workers was USD 16.77 in 2024, with 15% living below the poverty line and more than 40% living in low-income households, which shows that the constraint extends beyond pay and into job quality, career mobility, work hours, and benefits.

Other drivers and restraints analyzed in the detailed report include:

- Aging-in-Place Preference Creating Durable Uplift for Home-Based Services

- Chronic Disease and Dementia Burden Raising Per-Beneficiary Intensity

- Wage Inflation and Reimbursement Lag Compressing Provider Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Home Healthcare held 45.31% of the United States long term care market share in 2025, which reflects the strength of community-based delivery, public HCBS funding, and family preference for care at home. Richmond Fed reported in January 2026 that CMS programs reimburse more than 50% of total U.S. home health expenditures, and Medicaid accounted for nearly two-thirds of home care spending in 2023, which confirms the segment's deep public funding base. Nursing Care and Assisted Living Facilities remained the next largest service groups, but they are moving in different directions within the United States long term care market. Nursing care faces gradual pressure in lower-acuity cases because more families prefer to delay institutional placement and use home-based services first. Assisted living is benefiting from seniors who need daily supervision but not full clinical intervention, and Brookdale management said average occupancy was tracking toward 90% in 2026, which signals steady demand recovery in that setting.

Adult Day-Care Centers are projected to grow at an 9.38% CAGR between 2026 and 2031 within the United States long term care market size. That pace stands 173 basis points above the overall market growth rate and reflects the segment's role as a supervised bridge between home care and full institutional admission. CareScout reported that the national median daily rate for adult day health care was USD 95 in 2025, which supports its value case for families and public programs seeking lower-cost care intensity. The segment also fits closely with HCBS waiver structures and state efforts to prevent institutional admission, which supports continued demand as care continues to move into community settings across the United States long term care industry. Hospice remained smaller in revenue share, but it retained solid margin potential as the 85+ population expanded and palliative care acceptance broadened.

List of Companies Covered in this Report:

- AccentCare

- Addus HomeCare

- Atria Senior Living

- Aveanna Healthcare

- BAYADA Home Health Care

- Brookdale Senior Living

- Discovery Senior Living

- Diversicare Healthcare Services

- Erickson Senior Living

- Gentiva

- Home Instead Inc.

- LCS

- National HealthCare Corporation

- Sonida Senior Living

- Sunrise Senior Living

- The Ensign Group

- The Pennant Group

- VITAS Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Longevity

- 4.2.2 Medicaid and Medicare HCBS Rebalancing

- 4.2.3 Aging-In-Place Preference

- 4.2.4 Chronic Disease and Dementia Burden

- 4.2.5 Value-Based LTSS Contracting

- 4.2.6 Immigrant Labor Access Sustaining Capacity

- 4.3 Market Restraints

- 4.3.1 Direct-Care Workforce Shortages

- 4.3.2 Wage Inflation and Reimbursement Lag

- 4.3.3 Immigration Policy Tightening Caregiver Supply

- 4.3.4 Cyber And Privacy Risk in Connected Care

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service

- 5.1.1 Home Healthcare

- 5.1.2 Hospice

- 5.1.3 Nursing Care

- 5.1.4 Assisted Living Facilities

- 5.1.5 Adult Day-Care Centers

- 5.2 By Payer

- 5.2.1 Public

- 5.2.2 Private Insurance

- 5.2.3 Out-of-Pocket / Self-Funded

- 5.2.4 Managed-Care & Value-Based Contracts

- 5.3 By Age Group

- 5.3.1 0-29 Years

- 5.3.2 30-64 Years

- 5.3.3 65-74 Years

- 5.3.4 75-84 Years

- 5.3.5 85 Years & Above

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AccentCare

- 6.3.2 Addus HomeCare

- 6.3.3 Atria Senior Living

- 6.3.4 Aveanna Healthcare

- 6.3.5 BAYADA Home Health Care

- 6.3.6 Brookdale Senior Living

- 6.3.7 Discovery Senior Living

- 6.3.8 Diversicare Healthcare Services

- 6.3.9 Erickson Senior Living

- 6.3.10 Gentiva

- 6.3.11 Home Instead Inc.

- 6.3.12 LCS

- 6.3.13 National HealthCare Corporation

- 6.3.14 Sonida Senior Living

- 6.3.15 Sunrise Senior Living

- 6.3.16 The Ensign Group

- 6.3.17 The Pennant Group

- 6.3.18 VITAS Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment