|

시장보고서

상품코드

2065448

의약품 스크리닝용 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Drug Screening - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

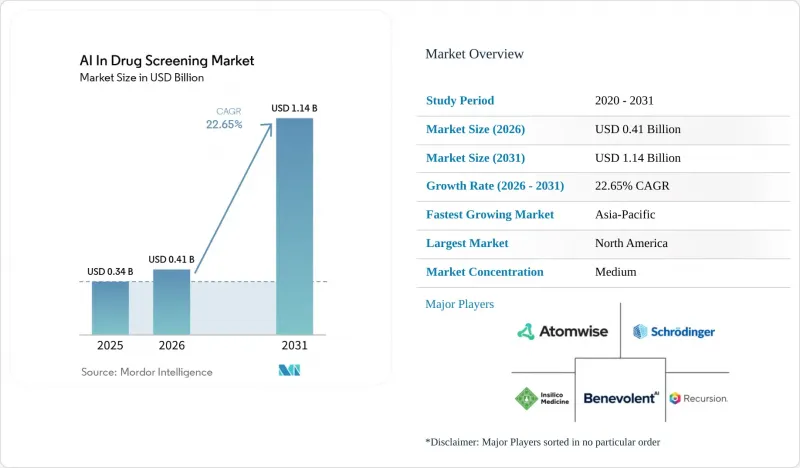

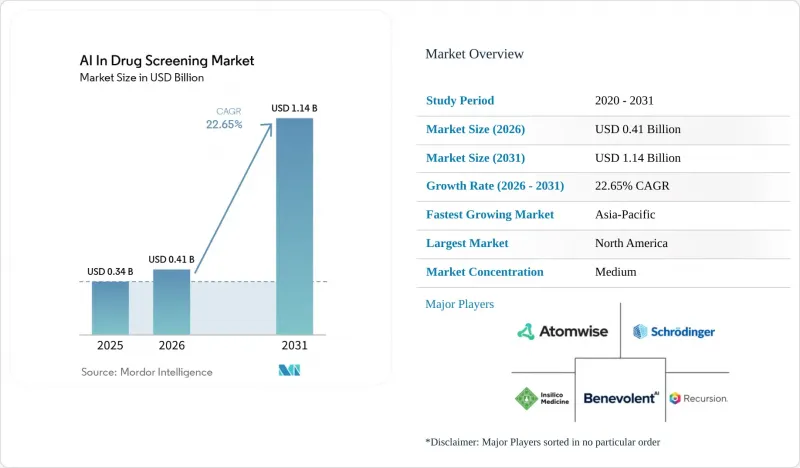

의약품 스크리닝용 인공지능(AI) 시장 규모는 2025년 3억 4,000만 달러로 평가되었습니다. 2026년에는 4억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 22.65%로 성장을 지속하여, 2031년까지 11억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제공 형태(소프트웨어, 서비스), 기술(머신러닝, 딥러닝 및 생성형 AI, 자연어 처리), 용도(표적 식별, 히트 식별, 리드 창출, 적응증 확대, 전임상 선정), 치료 분야(종양학, 감염증, 신경학, 순환기, 대사, 면역학), 최종 사용자(제약·바이오기술, CRO/CDMO, 학술 기관, 병원), 지역(북미, 유럽, 기타)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계의 의약품 스크리닝용 인공지능(AI) 시장 동향 및 인사이트

신약 개발 비용 및 개발 기간 단축에 대한 압박

평균 신약 개발 비용은 여전히 26억 달러에 육박하고, 개발 기간은 종종 10년을 넘으며, 임상 후보 물질의 90%가 승인 전에 실패로 끝나기 때문에 제약 파이프라인은 계속해서 구조적인 효율성 문제에 직면해 있습니다. AI를 활용한 신약 스크리닝 시장은 이러한 압박으로부터 직접적인 혜택을 보고 있습니다. 왜냐하면 구매자들은 현재 AI를 실험적인 신기술이 아니라, 명확한 비용 및 시간 기준에 따라 평가하고 있기 때문입니다. 일부 AI 기반 워크플로에서는 이미 특정 신약 개발 단계를 12-18개월로 단축하고, 기존 방식에 비해 최대 40%의 비용 절감을 실현하고 있습니다. 이러한 단축으로 인해 초기 연구 예산의 배분 방식이 변화하고 있으며, 물리적 화합물 라이브러리의 확충뿐만 아니라 플랫폼 구독, 모델 이용 및 컴퓨팅 인프라에 대한 자금 배분이 증가하고 있습니다. 그 결과, 신약 개발 주기의 초기 단계에서 안전성, 유효성 및 스크리닝 신호를 도출할 수 있는 플랫폼의 상업적 가치가 높아지고 있습니다.

생성형 AI와 분자 설계 모델의 진화

신약 개발 스크리닝 분야에서 AI는 모델 성능의 비약적인 향상 덕분에 더욱 힘을 얻고 있습니다. 특히 초기 리드 화합물 발굴 단계에서는 생성형 시스템이 물리적 스크리닝의 일부에 필적하는 성과를 내고 있습니다. Chai Discovery사는 자사의 Chai-2 모델이 데 노보 항체 설계에서 실험적 적중률이 20%에 육박했다고 보고했으며, 이는 기존의 0.1%라는 계산상 벤치마크에 비해 크게 향상된 수치입니다. VantAI는 2025년 3월, 데 노보 분자 생성 및 멀티모달 구조 예측을 단일 아키텍처에 통합한 원자 수준 기반 모델 ‘Neo-1’을 출시했습니다. 이로 인해 플랫폼 사용자가 다룰 수 있는 타겟의 범위가 확대되고 있습니다. 슈뢰딩거사도 2026년 여름에 ‘Bunsen’이라는 에이전트형 AI 공동 연구자를 얼리 액세스용으로 제공할 것이라고 발표했으며, 이는 플랫폼 공급업체들이 단일 작업 모델에서 신약 개발 워크플로의 더 광범위한 부분을 수행할 수 있는 시스템으로 전환하고 있음을 보여줍니다. 이러한 도구의 발전이 실험실의 합성 능력을 능가하는 속도로 진행됨에 따라, 다음 투자 주기는 자동화된 화학 합성 및 검증 인프라로 전환되고 있습니다. 이러한 추세는 프로플루언트(Profluent)사가 AI 설계를 통한 재조합 효소 개발을 두고 일라이 릴리(Eli Lilly)사와 22억 5,000만 달러 규모의 제휴를 체결한 사실에서도 입증되고 있습니다.

데이터 사일로화, 개인정보 보호 제약, 그리고 낮은 상호운용성

신약 개발 스크리닝 분야에서 AI는 여전히 근본적인 데이터 문제에 직면해 있습니다. 많은 공개 ADMET 데이터셋은 서로 다른 실험 조건을 적용한 20-50편의 개별 논문에서 수집된 것이기 때문에 연구 간 재현성이 낮기 때문입니다. 『Collaborative Drug Discovery』지의 보고에 따르면, ADMET 모델은 내부 테스트 세트에서는 R² 값이 0.9에 근접하는 반면, 분석 기법이 다른 외부 벤치마크에서는 0.75 수준까지 떨어지는 것으로 나타났으며, 이는 조직 간 일반화 가능성이 여전히 제한적임을 보여줍니다. 멀티오믹스 데이터의 통합 역시 또 다른 장벽이 되고 있습니다. 유전체, 전사체, 단백체 데이터는 호환되지 않는 메타데이터와 함께 종종 각 기관의 사일로에 고립되어 있어, 연구 분야를 아우르는 교육을 시작하기 전에 수작업으로 데이터를 조율해야 하기 때문입니다. 이로 인해 모델 개발이 지연될 뿐만 아니라, 이미 대규모의 독자적인 데이터 자산을 통합하고 실용적인 훈련 환경을 구축한 기업들에게 지속적인 경쟁 우위가 제공됩니다. 그 결과, 신약 스크리닝 분야의 AI 시장에서 장기적인 경쟁 우위를 확보하기 위해서는 모델 설계와 마찬가지로 데이터 거버넌스가 점점 더 중요해지고 있습니다.

부문별 분석

2025년, 소프트웨어 플랫폼은 신약 스크리닝 분야의 AI 시장 규모에서 62.31%를 차지했으며, 이는 확장 가능한 모델에 대한 접근이 여전히 구매자들에게 주요한 상용화 형태임을 뒷받침하고 있습니다. 현재의 수익 기반이 소프트웨어에 유리한 이유는 클라우드 도입을 통해 신약 개발 팀이 실험 비용을 비례적으로 늘리지 않고도 매우 대규모의 가상 라이브러리를 스크리닝할 수 있기 때문입니다. 단일 플랫폼 구독으로 여러 프로그램을 동시에 지원할 수 있으므로, 사내 연구개발 그룹의 경우 프로젝트 기반 서비스 계약보다 비용 구조를 예측하기 쉬워집니다. 이 모델 덕분에 소프트웨어는 의약품 스크리닝용 인공지능(AI) 시장에서 계속해서 중심적인 위치를 차지하고 있으며, 플랫폼 구매자들은 표적 발굴 및 스크리닝 과정에서 다양한 워크플로우 조합을 지속적으로 시도하고 있습니다.

서비스 부문은 가장 빠르게 성장하고 있는 제공 부문으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 27.38%를 나타낼 것으로 전망됩니다. 이러한 성장은 완전한 신약 개발 플랫폼을 자체적으로 운영하기 위해 필요한 사내 데이터, 계산 자원 또는 전문 팀을 아직 갖추지 못한 중견 바이오기술 기업들의 아웃소싱 수요 증가를 반영하고 있습니다. 이에 대응하여 CRO와 CDMO는 AI를 활용한 스크리닝, 데이터 분석, 맞춤형 모델 훈련을 자사의 신약 개발 패키지에 추가함으로써 이에 대응하고 있습니다. 앞으로 소프트웨어 기능의 재현이 용이해지고, 차별화의 초점이 고객 소유 데이터를 기반으로 한 통합 워크플로우 실행으로 이동함에 따라, 신약 스크리닝 분야의 AI 시장 균형은 서비스 주도형 가치 창출로 전환될 것으로 보입니다.

2025년 기준으로, 머신러닝은 기술 부문의 46.24%를 차지했으며, 이는 실용적인 신약 개발 워크플로우에서 ADMET 예측, 특성 스코어링 및 정량적 구조-활성 상관관계(QSAR) 모델링 분야에서 머신러닝이 확고한 역할을 수행하고 있음을 반영합니다. 신약 스크리닝 분야의 AI 시장에서 이러한 도입 실적이 중요한 이유는 머신러닝 기법이 이미 일상적인 스크리닝 업무에 통합되어 있으며, 재현성이 높은 평가 기능으로서 여전히 신뢰를 받고 있기 때문입니다. 또한, 기존의 연구개발 시스템과도 원활하게 호환되므로, 신약 개발 프로세스 전체를 재구축하지 않고도 실질적인 성과를 추구하는 구매자에게는 전환 장벽이 낮아집니다. 바로 이러한 도입 실적이, 새로운 모델 클래스가 주목을 받고 있는 상황에서도 머신러닝이 여전히 현재 기술 구조의 기반을 이루고 있는 이유를 설명해 줍니다.

딥러닝과 생성형 AI는 2026년부터 2031년까지 연평균 성장률(CAGR) 28.52%를 기록하며, 가장 빠르게 성장하고 있는 기술 분야입니다. Chai Discovery사의 ‘Chai-2’ 모델은 데 노보 항체 설계에서 약 20%에 달하는 실험적 적중률을 보여주고 있으며, 이는 생성형 AI 시스템이 단순한 선택적 설계 지원 도구가 아니라 실용적인 1차 스크리닝 도구로 자리매김하고 있음을 시사합니다. 또한 Receptor.AI는 자사의 ADMET 모델 제품군이 2025년 TDC 벤치마크 과제 16개 항목 중 10개 항목에서 1위를 차지했다고 보고했으며, DILI, hERG, CYP450 평가 지표에서도 우수한 결과를 보여주었습니다. 자연어 처리 및 그래프 기반 기법은 문헌 마이닝과 단백질-리간드 모델링을 뒷받침하는 기반으로서 계속해서 기능하고 있지만, 신약 스크리닝 업계에서 AI는 기존 분야의 경계를 모호하게 만들고, 각 벤더들이 워크플로우 전반에 걸쳐 경쟁하도록 이끄는 멀티모달 아키텍처로 전환되고 있습니다.

지역별 분석

2025년, 북미는 신약 스크리닝 분야의 AI 시장 점유율 43.24%를 차지하며 여전히 최대 지역 거점으로서의 위상을 유지했습니다. 이 지역은 AI 기반 신약 개발 기업의 밀집도가 가장 높으며, 풍부한 벤처 자금뿐만 아니라 생명공학 플랫폼, 대형 제약사, 연구 기관 간의 긴밀한 협력이라는 이점을 누리고 있습니다. 2026년 4월, FDA는 의약품 개발을 위한 AI 시범 프로그램을 시작했습니다. 이는 임상시험의 실시간 모니터링을 지원하는 것으로, AI를 활용한 규제 워크플로우로의 광범위한 전환을 반영하고 있습니다. 또한, NIH의 Complement-ARIE 프로그램도 동물 모델을 대체할 수 있는 AI 기반 예측 시스템에 1억 5,000만 달러를 투자했습니다. 이를 통해 신뢰성이 높은 검증 경로가 필요한 공급업체의 경우, 도입 위험이 줄어듭니다. 캐나다와 멕시코는 학술, 생명공학, 제조 분야에서 유익한 협력을 이끌어내고 있지만, 이 지역은 여전히 미국을 거점으로 하는 플랫폼과 자본 형성을 중심으로 발전하고 있습니다.

유럽은 신약 스크리닝 분야의 AI 시장에서 여전히 중요한 중심지 역할을 하고 있으며, 관련 활동은 영국, 독일, 스위스 일대에 점점 더 집중되고 있습니다. 영국은 ‘AI 퍼스트’ 바이오기술 분야에서 두각을 나타내고 있으며, 2026년 5월 Isomorphic Labs가 21억 달러 규모의 시리즈 B 자금 조달을 성사시킨 것은 장기적인 비전을 가진 AI 신약 개발 플랫폼이 현재 매우 대규모의 기관 투자자 자금으로 지원받고 있음을 보여줍니다. FDA와 EMA는 2026년 1월, 의약품 개발에 있어 AI와 관련된 10가지 지침을 공동으로 발표했습니다. 이를 통해 유럽의 개발자들에게는 설명 가능성, 감독 및 데이터 처리에 관한 보다 명확한 거버넌스 체계가 마련되었습니다. 독일과 프랑스는 강력한 CRO 및 대학 부속 병원의 역량을 갖추고 있는 반면, 스페인과 이탈리아는 바이오기술 클러스터의 확대와 AI를 활용한 의약품 개발 도구의 조기 도입을 통해 성장세를 보이고 있습니다.

아시아태평양은 AI를 활용한 신약 스크리닝 시장에서 가장 빠르게 성장하고 있는 지역 부문이며, 2026년부터 2031년까지 연평균 성장률(CAGR)이 26.53%를 나타낼 것으로 전망됩니다. 중국과 인도가 주요 성장 동력으로 작용하고 있는데, 이는 지역 전체의 생태계에서 신약 개발 아웃소싱 역량, 연구개발(R&D) 분야의 AI 도입, 그리고 플랫폼 통합이 향상되고 있기 때문입니다. 일본과 한국은 제약 업계의 디지털화 추진과 정부가 지원하는 AI 바이오기술 이니셔티브를 통해 시장의 깊이를 더하고, 혁신 기반 전반을 강화하고 있습니다. 중동 및 아프리카은 대규모 AI 의약품 설계 자금 조달에 GCC(걸프협력회의) 회원국들이 자본을 투자함으로써 부분적으로 뒷받침되고 있으며, 남미 지역은 브라질의 신생 CRO 네트워크가 주도적인 역할을 하고 있습니다. 이 지역들은 현재로서는 규모가 작지만, AI를 활용한 신약 스크리닝 시장의 장기적인 확장에 있어 여전히 중요한 역할을 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the aI in drug screening market size is expected to grow from USD 0.34 billion in 2025 to USD 0.41 billion in 2026 and is forecast to reach USD 1.14 billion by 2031 at 22.65% CAGR over 2026-2031.

This report is Segmented by Offering (Software, Services), Technology (ML, Deep Learning & Gen AI, NLP), Application (Target ID, Hit ID, Lead Gen, Repurposing, Preclinical Selection), Therapeutic Area (Oncology, Infectious Dis, Neurology, Cardiovasc, Metabolic, Immunology), End User (Pharma/Biotech, CROs/CDMOs, Academic, Hospitals), and Geography (North America, Europe, and More). Forecasts in Value (USD).

Global AI In Drug Screening Market Trends and Insights

Pressure to Cut Discovery Cost and Cycle Time

Pharmaceutical pipelines continue to face a structural efficiency problem because average drug development cost still approaches USD 2.6 billion, timelines often exceed 10 years, and 90% of clinical candidates fail before approval. The AI in drug screening market is benefiting directly from this pressure because buyers now evaluate AI against a clear cost and time benchmark rather than against experimental novelty. Some AI-driven workflows have already reduced selected discovery stages to 12 to 18 months and delivered cost reductions of up to 40% against traditional methods. That compression is changing how early research budgets are assigned, with more capital moving toward platform subscriptions, model access, and compute infrastructure instead of only physical compound library expansion. The result is a stronger commercial case for platforms that can surface safety, efficacy, and screening signals earlier in the discovery cycle.

Better Generative AI and Molecular Design Models

The AI in drug screening market is also being lifted by a step change in model capability, especially in early lead generation where generative systems now produce outputs that can compete with parts of physical screening. Chai Discovery reported that its Chai-2 model achieved a near-20% experimental hit rate in de novo antibody design, a major increase over the prior 0.1% computational benchmark. VantAI launched Neo-1 in March 2025 as an atomistic foundation model that combines de novo molecular generation with multimodal structure prediction in one architecture, which broadens the range of tractable targets for platform users. Schrodinger has also positioned its Bunsen agentic AI co-scientist for early access in summer 2026, showing how platform vendors are moving from single-task models toward systems that can execute larger parts of discovery workflows. As these tools improve faster than wet-lab synthesis capacity, the next investment cycle is shifting toward automated chemistry and validation infrastructure, a pattern reinforced by Profluent's USD 2.25 billion collaboration with Eli Lilly for AI-designed recombinases.

Siloed Data, Privacy Constraints, and Poor Interoperability

The AI in drug screening market still faces a core data problem because many public ADMET datasets are assembled from 20 to 50 separate papers that use different experimental conditions and show weak reproducibility across studies. Collaborative Drug Discovery reported that ADMET models can reach R2 near 0.9 on internal test sets but fall to around 0.75 on external benchmarks when assay methods differ, which shows that transfer across organizations is still limited. Multi-omics integration adds another layer of friction because genomic, transcriptomic, and proteomic data often sit in separate institutional silos with incompatible metadata and require manual harmonization before cross-study training can begin. This slows model development and also gives a lasting advantage to firms that have already federated large proprietary data assets into usable training environments. As a result, data governance in the AI in drug screening market is becoming just as important as model design for long-term competitive positioning.

Other drivers and restraints analyzed in the detailed report include:

- AlphaFold-Scale Structure Maps Improving Target Enablement

- Rising Pharma-Tech Partnerships and Licensing Activity

- Limited Explainability and Wet-Lab Translation Confidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms captured 62.31% of AI in drug screening market size in 2025, which confirms that scalable model access still represents the main commercial format for buyers. The current revenue base favors software because cloud deployment lets drug discovery teams screen very large virtual libraries without a matching increase in laboratory cost. One platform subscription can support multiple programs at the same time, which gives internal R&D groups a more predictable cost structure than project-based service engagements. This model has kept software at the center of the AI in drug screening market while platform buyers continue to test different workflow combinations across target discovery and screening.

Services are the fastest-growing offering segment, with a projected CAGR of 27.38% from 2026 to 2031. This rise reflects stronger outsourcing demand from mid-size biotech firms that do not yet have the internal data, compute, or specialist teams needed to operate full discovery platforms on their own. CROs and CDMOs are responding by adding AI-enabled screening, data interpretation, and bespoke model training into their discovery packages. Over time, the balance in the AI in drug screening market is likely to move toward more service-led value capture as software functionality becomes easier to replicate and differentiation shifts toward integrated workflow execution on client-owned data.

Machine learning held 46.24% of the technology segment in 2025, which reflects its established role across ADMET prediction, property scoring, and quantitative structure-activity relationship modeling in production discovery workflows. In the AI in drug screening market, this installed base matters because machine learning methods are already embedded in day-to-day screening tasks and remain trusted for repeatable scoring functions. They also fit well into existing R&D systems, which lowers switching friction for buyers that want practical gains without rebuilding entire discovery stacks. That installed position explains why machine learning still anchors the current technology mix even as newer model classes gain attention.

Deep learning and generative AI is the fastest-growing technology segment, with a CAGR of 28.52% from 2026 to 2031. Chai Discovery's Chai-2 model showed a near-20% experimental hit rate in de novo antibody design, which signals that generative systems are becoming viable first-pass screening tools rather than optional design aids. Receptor.AI also reported first-place ranking on 10 of 16 TDC benchmark tasks in 2025 for its ADMET model family, including strong results on DILI, hERG, and CYP450 endpoints. Natural language processing and graph-based methods continue to serve as enabling layers for literature mining and protein-ligand modeling, but the AI in drug screening industry is moving toward multimodal architectures that blur old segment boundaries and push vendors toward full workflow competition.

Geography Analysis

North America held 43.24% of AI in drug screening market share in 2025, which kept it as the largest regional base. The region benefits from the highest concentration of AI-native drug discovery firms, deep venture funding, and close ties between biotech platforms, major pharmaceutical companies, and research institutions. In April 2026, the FDA launched an AI pilot program for drug development that supports real-time trial monitoring and reflects a broader move toward AI-enabled regulatory workflows. The NIH Complement-ARIE program also committed USD 150 million to AI-driven predictive systems that can act as alternatives to animal models, which lowers adoption risk for vendors that need credible validation pathways. Canada and Mexico add useful academic, biotech, and manufacturing links, but the region remains centered on U.S.-based platforms and capital formation.

Europe remains an important center of the AI in drug screening market, with activity increasingly concentrated around the UK, Germany, and Switzerland. The UK stands out in AI-first biotech, and Isomorphic Labs' USD 2.1 billion Series B in May 2026 showed that very large pools of institutional capital are now backing long-horizon AI drug design platforms. The FDA and EMA jointly issued 10 guiding principles for AI in medicine development in January 2026, which gave European developers a clearer governance framework for explainability, oversight, and data handling EMA. Germany and France provide strong CRO and academic medical center capacity, while Spain and Italy are building momentum through growing biotech clusters and earlier adoption of AI-enabled drug development tools.

Asia-Pacific is the fastest-growing regional segment in the AI in drug screening market, with a CAGR of 26.53% from 2026 to 2031. China and India are the main growth engines because discovery outsourcing capacity, AI adoption in R&D, and platform integration are improving across regional ecosystems. Japan and South Korea add depth through pharmaceutical digitalization efforts and government-backed AI biotech initiatives that strengthen the broader innovation base. Middle East and Africa, supported in part by GCC capital participation in large AI drug design financings, and South America, led by Brazil's developing CRO network, remain smaller today but still matter for long-term expansion of the AI in drug screening market.

- Absci

- Atomwise

- BenchSci

- Benevolent AI

- CytoReason

- Deep Genomics

- Generate:Biomedicines

- Genesis Molecular AI

- Iktos

- Insilico Medicine

- insitro

- Isomorphic Labs

- Lantern Pharma

- Owkin

- Recursion Pharmaceuticals

- Schrodinger

- Standigm

- Valo Health

- WuXi App Tec

- XtalPi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pressure to Cut Discovery Cost and Cycle Time

- 4.2.2 Expanding Multi-Omics and Clinical Training Datasets

- 4.2.3 Rising Pharma-Tech Partnerships and Licensing Activity

- 4.2.4 Better Generative AI and Molecular Design Models

- 4.2.5 Alphafold-Scale Structure Maps Improving Target Enablement

- 4.2.6 Benchmark-Grade ADMET and Protein-Ligand Datasets Improving Model Reliability

- 4.3 Market Restraints

- 4.3.1 Siloed Data, Privacy Constraints, and Poor Interoperability

- 4.3.2 Limited Explainability and Wet-Lab Translation Confidence

- 4.3.3 Rising FDA and EMA Documentation Expectations for AI-Enabled Evidence

- 4.3.4 Noisy Public Datasets and Weak Scaffold Transfer in Real-World Screening

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Software Platforms

- 5.1.2 Services

- 5.2 By Technology

- 5.2.1 Machine Learning

- 5.2.2 Deep Learning and Generative AI

- 5.2.3 Natural Language Processing

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Target Identification and Validation

- 5.3.2 Hit Identification and Virtual Screening

- 5.3.3 Lead Generation and Optimization

- 5.3.4 Drug Repurposing

- 5.3.5 Preclinical Candidate Selection and Toxicity Prediction

- 5.3.6 Biomarker Discovery and Companion Insights

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 Infectious Diseases

- 5.4.3 Neurology and Psychiatric Disorders

- 5.4.4 Cardiovascular Disorders

- 5.4.5 Metabolic and Endocrine Disorders

- 5.4.6 Immunology and Inflammatory Disorders

- 5.4.7 Other Therapeutic Areas

- 5.5 By End User

- 5.5.1 Pharmaceutical and Biotechnology Companies

- 5.5.2 CROs and CDMOs

- 5.5.3 Academic and Research Institutes

- 5.5.4 Hospitals and Clinical Research Networks

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Absci

- 6.3.2 Atomwise

- 6.3.3 BenchSci

- 6.3.4 BenevolentAI

- 6.3.5 CytoReason

- 6.3.6 Deep Genomics

- 6.3.7 Generate:Biomedicines

- 6.3.8 Genesis Molecular AI

- 6.3.9 Iktos

- 6.3.10 Insilico Medicine

- 6.3.11 insitro

- 6.3.12 Isomorphic Labs

- 6.3.13 Lantern Pharma

- 6.3.14 Owkin

- 6.3.15 Recursion Pharmaceuticals

- 6.3.16 Schrodinger

- 6.3.17 Standigm

- 6.3.18 Valo Health

- 6.3.19 WuXi AppTec

- 6.3.20 XtalPi

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment