|

시장보고서

상품코드

2065520

엣지 AI GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Edge AI GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

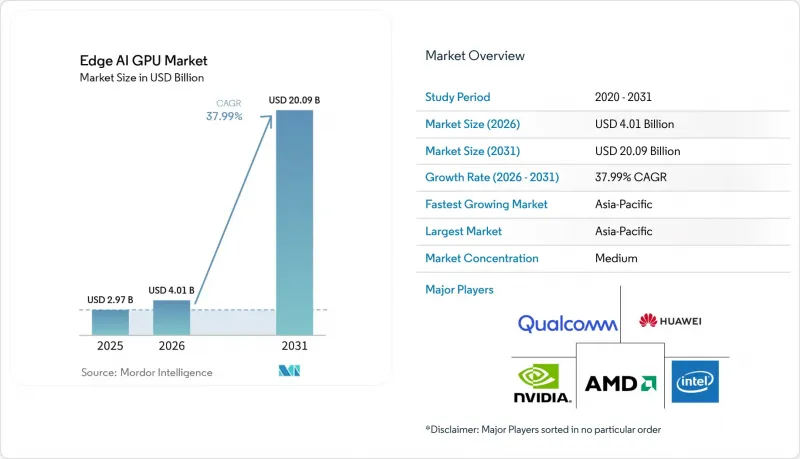

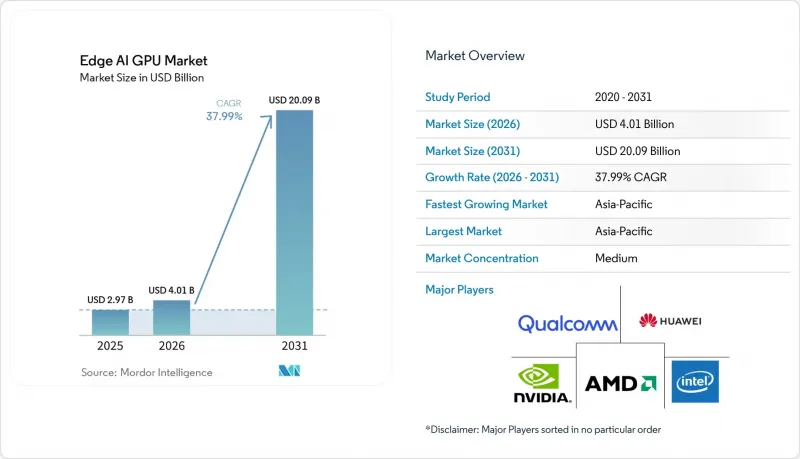

Mordor Intelligence에 의하면, 엣지 AI GPU 시장 규모는 2025년 29억 7,000만 달러로 평가되었고, 2031년에는 40억 1,000만 달러로 추정되고, 2026-2031년 CAGR 37.99%를 기록했습니다.

본 보고서는 GPU 유형별(통합형 GPU 및 디스크리트 GPU), 도입 형태별(엣지 서버, 게이트웨이 및 임베디드형 엣지 디바이스), 용도별(영상 분석 및 감시, 산업용 AI, 로봇 공학 및 자동화 등), 그리고 지역별(북미, 유럽, 아시아태평양, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 엣지 AI GPU 시장 동향 및 인사이트

저지연 AI 처리가 필요한 IoT 기기의 보급

디바이스에서 추론이 필요한 IoT 엔드포인트의 전 세계 도입 대수는 2025년에 150억 대를 돌파했으며, 기업들은 클라우드 중심의 워크플로우에서 벗어나지 않을 수 없게 되었습니다. 80-120밀리초의 왕복 지연 시간은 폐루프형 로봇, 외과용 기기 및 산업용 공정 제어에는 적합하지 않습니다. ABB의 현장 테스트에서 센서에 GPU 추론을 도입함으로써 지연 시간을 5밀리초 미만으로 단축하고, 협업 로봇의 사이클 타임을 40% 단축할 수 있었습니다. 현재 각 벤더사는 팬이 없는 산업용 설계에 대응하기 위해, 소비 전력을 15와트 미만으로 억제하는 동적 전압 스케일링 기능을 갖춘 5nm SoC를 개발하고 있습니다. 이러한 추세에 따라 자동차, 의료기기, 스마트 유틸리티 분야에서 엣지 AI GPU 시장의 잠재 수요가 크게 확대되고 있습니다.

5G의 급속한 확산이 엣지 대역폭을 강화합니다.

2025년 중반까지 독립형 5G의 도입이 대폭 확대되어, 엣지 추론을 위해 10밀리초 미만의 경로를 제공하는 네트워크 슬라이스가 구현되었습니다. 한국의 통신사는 2024년에 전국적인 서비스 확장을 완료했으며, 서울에 위치한 구로 디지털 콤플렉스에서는 실시간 품질 검사를 위해 2,000대 이상의 GPU 노드를 지원하고 있습니다. 유럽연합(EU)은 2025년, 이와 같은 확산을 촉진하기 위해 9억 유로(10억 1,000만 달러)를 예산에 편성하고, 통신 사업자들에게 기지국 쉘터에 GPU 서버를 함께 설치하도록 의무화했습니다. 신흥국에서는 독립형 셀 1개당 설비 투자(CAPEX)가 15만 달러로 여전히 고가이지만, 지연 시간에 민감한 분석 분야에서 그 가치가 이미 입증됨에 따라 통신 생태계 내에서 엣지 AI GPU의 도입이 확대되고 있습니다.

GPU의 높은 전력 소비와 열적 제약

75와트를 소비하는 디스크리트 GPU는 시간당 256 BTU의 열을 발생시키며, 이는 밀폐형 IP65 인클로저에 과도한 부하를 주게 됩니다. 각 벤더사가 칩의 클럭 속도를 낮추고 있기 때문에 실험실에서의 정격값과 비교했을 때 처리량이 최대 20% 감소했으며, 이로 인해 5와트 미만의 신경망 프로세서에 대한 우위가 줄어들고 있습니다. 인텔은 2025년에 50와트급 ‘Arc A380E’ 모델을 출시했으나, 가격 경쟁력을 중시하는 시장 부문에서는 엔비디아의 30와트급 ‘Orin NX’와 경쟁을 벌이고 있습니다. 유럽의 산업 시설에서는 75와트 노드 1대당 연간 95유로(107달러)의 전기 요금을 지불하고 있으며, 500대 이상의 설치 대수에 이 비용이 곱해집니다. 따라서 배터리 구동 방식의 필드 센서는 하이브리드 아키텍처에서 GPU를 우회하게 되며, 이로 인해 초저전력 엣지 분야에서의 단기적인 엣지 AI GPU 시장 침투율을 억제하게 될 것입니다.

부문별 분석

2025년, 엣지 AI GPU 시장 규모에서 통합형 GPU는 61.59%의 점유율을 차지했습니다. 이는 POS 단말기, 산업용 HMI 스크린, 자동차용 인포테인먼트 시스템에서의 채택 확대가 반영된 결과입니다. Snapdragon 8 Gen 3 및 Dimensity 9300 SoC는 5-15와트의 전력 소비 범위 내에 있어 팬이 없는 케이스에 최적입니다. 디스크리트 GPU는 출하 대수는 적지만, 30 FPS에서 12 TFLOPS가 필요한 4K 비디오 분석 스트림을 지원하기 위해 연평균 성장률(CAGR) 38.48%로 시장을 확대되고 있습니다. 애플의 40코어 ‘M3 Max’는 65 TFLOPS를 통합형 폼 팩터에 집약함으로써 카테고리 간의 경계를 모호하게 만들었고, 보급형 디스크리트 GPU 카드에 필적하는 성능을 실현했습니다. 2024년부터 시행되는 유럽의 에코디자인 라벨에 따라 공공 조달에서 통합형 실리콘이 우선적으로 채택됨에 따라, 이 부문은 엣지 AI GPU 시장 전체에서 더욱 확고한 입지를 다지게 될 것입니다.

순수한 병렬 처리 능력이 전력 소비 제한을 초과하는 분야에서는 여전히 개별 소자가 주류를 이루고 있습니다. 70와트 RTX A2000은 26 TFLOPS의 성능을 제공하며, 지자체 교통 분석에서 카메라 1대당 실시간 감지 건수를 2배로 늘립니다. 트랜스포머 기반 비전 모델의 파라미터 수가 1억 개를 넘어서는 규모로 급증하는 가운데, 전용 텐서 코어를 탑재한 디스크리트 SKU가 공장 및 스마트 시티에서의 도입을 가속화하고 있습니다. 하이브리드 로드맵에서는 SoC에 추가적인 GPU 타일을 적층함으로써, 통합형 솔루션과 디스크리트 솔루션의 성능 추세가 점차 수렴하고 있습니다.

지역별 분석

아시아태평양은 2025년에 엣지 AI GPU 시장 점유율의 66.71%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 38.83%로 성장할 것으로 전망됩니다. 중국은 ‘신 인프라’ 캠페인의 일환으로 스마트 시티 프로그램을 위해 GPU 지원 노드 80만 대를 발주했습니다. 일본은 엣지 AI로의 전환을 추진하는 중소 제조업체를 대상으로 500억 엔(3억 4,000만 달러)의 보조금을 편성했습니다. 한국은 2025년에 GPU 추론 기능을 탑재한 협동 로봇 4만 5,000대를 출하했습니다. 인도는 2027년까지 농업 및 의료 분야에 1만 대의 GPU 노드를 도입하는 것을 목표로 하고 있습니다.

북미는 2위를 차지했습니다. 미국 에너지부는 2025년, 송전망 에지 분석 시범 사업에 4억 5,000만 달러를 지원하여 변전소에 GPU 노드를 설치했습니다. 캐나다의 자동차 공장에서는 용접 시 비전 가이드 및 결함 부위의 트리밍에 GPU가 활용되었습니다. 유럽의 GDPR(EU 개인정보보호규정)에 명시된 데이터 최소화 원칙에 따라 기업들은 로컬 GPU 활용을 확대하고 있으며, 독일의 한 자동차 제조업체는 예측 유지보수를 통해 가동 중단 시간을 25% 줄였습니다.

남미의 점유율은 아직 작지만, 브라질의 농장과 칠레의 광산에서 GPU 기반 원격 감지 기술이 도입됨에 따라 그 비율은 점차 증가하고 있습니다. 중동 및 아프리카에서는 두바이에서 스마트 시티의 초기 도입이 진행되고 있으며, 교통 분석을 위해 5,000대의 GPU 노드가 도입되었습니다. 수출 규제로 인해 러시아 및 일부 시장으로의 출하가 제한되고 있어, 엣지 AI GPU 시장의 지리적 확산이 다소 저해되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the edge AI GPU market size expanded from USD 2.97 billion in 2025 to USD 4.01 billion in 2031, registering a 37.99% CAGR from 2026 to 2031.

This report is Segmented by GPU Type (Integrated GPUs and Discrete GPUs), Deployment Type (Edge Servers/Gateways and Embedded Edge Devices), Application (Video Analytics and Surveillance, Industrial AI, Robotics and Automation, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Edge AI GPU Market Trends and Insights

Proliferation of IoT Devices Requiring Low-Latency AI Processing

The global installed base of IoT endpoints needing on-device inference surpassed 15 billion units in 2025, forcing enterprises to abandon cloud-centric workflows. Round-trip latency of 80-120 milliseconds is incompatible with closed-loop robotics, surgical equipment, and industrial process control. Deploying GPU inference at the sensor collapses latency to under 5 milliseconds and cuts cycle times for collaborative robots by 40% in ABB field trials. Vendors now build 5 nm SoCs with dynamic voltage scaling to keep power under 15 watts, aligning with fanless industrial designs. The trend materially expands addressable edge AI GPU market demand across automotive lines, medical devices, and smart utilities.

Rapid Deployment of 5G Enhancing Edge Bandwidth

Standalone 5G deployments expanded significantly by mid-2025, enabling network slices that deliver sub-10-millisecond paths for edge inference. South Korean operators completed nationwide rollouts in 2024, supporting more than 2,000 GPU nodes at Seoul's Guro Digital Complex for real-time quality inspection. The European Union earmarked EUR 900 million (USD 1.01 billion) in 2025 to seed similar deployments, compelling carriers to co-locate GPU servers at base-station shelters. While the USD 150,000 CAPEX per standalone cell remains high in emerging economies, the value proposition for latency-sensitive analytics is now proven, widening the adoption of edge AI GPUs in telecom ecosystems.

High Power Consumption and Thermal Constraints of GPUs

Discrete GPUs drawing 75 watts generate 256 BTU per hour, overwhelming sealed IP65 enclosures. Vendors down-clock silicon, cutting throughput by up to 20% versus lab ratings, which narrows the advantage over sub-5-watt neural processors. Intel launched a 50-watt Arc A380E variant in 2025, but it faces NVIDIA's 30-watt Orin NX in cost-sensitive segments. European industrial sites pay EUR 95 (USD 107) in annual power for each 75-watt node, a charge that multiplies across 500-plus installations. Battery-powered field sensors, therefore, bypass GPUs for hybrid architectures, capping near-term edge AI GPU market penetration in ultra-low-power edge niches.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Real-Time Video Analytics in Smart Cities

- Growing Adoption of Autonomous Mobile Robots in Manufacturing

- Supply-Chain Shortages of Advanced Packaging Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated GPUs held 61.59% share of the edge AI GPU market size in 2025, reflecting design wins in point-of-sale terminals, industrial HMI screens, and automotive infotainment. Snapdragon 8 Gen 3 and Dimensity 9300 SoCs fall within the 5-15 watt envelope, ideal for fanless chassis. Discrete GPUs, although smaller in volume, are expanding at a 38.48% CAGR to support 4K video analytics streams that require 12 TFLOPS at 30 FPS. Apple's 40-core M3 Max blurred category lines by packing 65 TFLOPS into an integrated form factor, rivaling entry discrete cards. European Ecodesign labeling, effective from 2024, privileges integrated silicon in public procurements, further anchoring this segment within the broader edge AI GPU market.

Discrete devices still dominate where raw parallelism trumps power limits. An RTX A2000 at 70 watts offers 26 TFLOPS, doubling real-time detections per camera in municipal traffic analytics. As transformer-based vision models swell past 100 million parameters, discrete SKUs with dedicated tensor cores accelerate uptake in factories and smart cities. Heterogeneous roadmaps now see SoCs stacking extra GPU tiles, converging the performance vectors of integrated and discrete solutions.

Geography Analysis

Asia-Pacific held 66.71% of the edge AI GPU market share in 2025 and is projected to grow at 38.83% CAGR to 2031. China ordered 800,000 GPU-ready nodes for smart-city programs under the New Infrastructure campaign. Japan budgeted JPY 50 billion (USD 340 million) in subsidies for small and medium manufacturers upgrading to edge AI. South Korea shipped 45,000 collaborative robots with GPU inference in 2025. India's mission aims to deploy 10,000 GPU nodes by 2027 across the agriculture and health sectors.

North America ranks second. The U.S. Department of Energy funded USD 450 million in grid-edge analytics pilots in 2025, installing GPU nodes at substations. Canadian auto plants used GPUs for welding vision-guidance and defect trimming. Europe's GDPR data-minimization principle directs enterprises toward local GPUs, and Germany's automakers cut downtime by 25% through predictive maintenance.

South America's share is smaller but rising as Brazilian farms and Chilean mines adopt GPU-based remote sensing. The Middle East and Africa are seeing early smart-city deployments in Dubai, including 5,000 GPU nodes for traffic analytics. Export-control rules limit shipments to Russia and select markets, modestly tempering wider geographic uptake of the edge AI GPU market.

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices Inc.

- Qualcomm Technologies Inc.

- Huawei Technologies Co. Ltd.

- Samsung Electronics Co. Ltd.

- Apple Inc.

- MediaTek Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- Lenovo Group Ltd.

- Super Micro Computer Inc.

- ADLINK Technology Inc.

- Advantech Co. Ltd.

- Hailo Technologies Ltd.

- Kneron Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of IoT Devices Requiring Low-Latency AI Processing

- 4.2.2 Rapid Deployment of 5G Enhancing Edge Bandwidth

- 4.2.3 Rising Demand for Real-Time Video Analytics in Smart Cities

- 4.2.4 Growing Adoption of Autonomous Mobile Robots in Manufacturing

- 4.2.5 Regulatory Push for Data Privacy Favouring On-Device Processing

- 4.2.6 Emergence of Cold-Chain Edge Nodes in Pharmaceutical Logistics

- 4.3 Market Restraints

- 4.3.1 High Power Consumption and Thermal Constraints of GPUs

- 4.3.2 Supply-Chain Shortages of Advanced Packaging Capacity

- 4.3.3 Skills Gap in Deploying Containerised GPU Stacks at Edge Sites

- 4.3.4 Regulatory Export Controls Limiting GPU Availability

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By GPU Type

- 5.1.1 Integrated GPUs

- 5.1.2 Discrete GPUs

- 5.2 By Deployment Type

- 5.2.1 Edge Servers / Gateways

- 5.2.2 Embedded Edge Devices

- 5.3 By Application

- 5.3.1 Video Analytics and Surveillance

- 5.3.2 Industrial AI

- 5.3.3 Robotics and Automation

- 5.3.4 Healthcare AI

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 India

- 5.4.3.5 Southeast Asia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East

- 5.4.6 Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Intel Corporation

- 6.4.3 Advanced Micro Devices Inc.

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Huawei Technologies Co. Ltd.

- 6.4.6 Samsung Electronics Co. Ltd.

- 6.4.7 Apple Inc.

- 6.4.8 MediaTek Inc.

- 6.4.9 Dell Technologies Inc.

- 6.4.10 Hewlett Packard Enterprise Co.

- 6.4.11 Lenovo Group Ltd.

- 6.4.12 Super Micro Computer Inc.

- 6.4.13 ADLINK Technology Inc.

- 6.4.14 Advantech Co. Ltd.

- 6.4.15 Hailo Technologies Ltd.

- 6.4.16 Kneron Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment